Vector Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

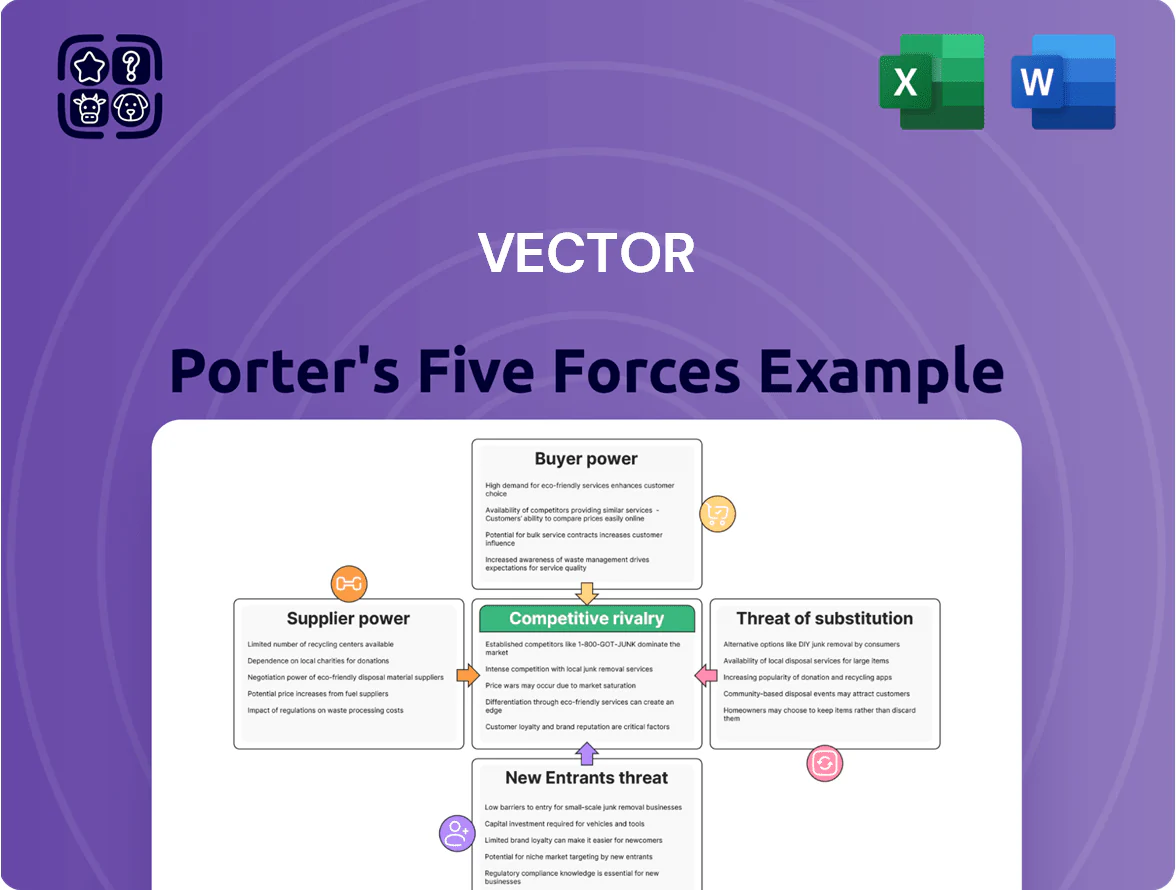

Vector’s Porter's Five Forces snapshot highlights how supplier leverage, buyer bargaining, competitive rivalry, substitute threats, and entry barriers shape its strategic position, revealing pockets of strength and vulnerability that inform tactical choices.

This brief overview teases force-level dynamics and market pressures but stops short of the granular ratings, data visualizations, and scenario implications you need for confident decisions.

Unlock the full Porter's Five Forces Analysis for Vector to access force-by-force scores, charts, and actionable recommendations—perfect for investor presentations, strategic planning, or execution.

Suppliers Bargaining Power

Concentration of Specialized Technology Providers

Vector relies on a handful of global suppliers for smart meters and grid software; by 2025 about 70% of its new smart meter rollouts use two vendors, raising supplier leverage.

Reliance on Transpower for Transmission Services

As sole owner of New Zealand’s national grid, Transpower supplies all high-voltage transmission to Vector’s network, creating strong supplier power despite regulated pricing; Vector paid about NZD 322m in transmission charges in FY2024, 24% of its operating costs. Vector remains exposed to Transpower’s investment timing and outages, and the Commerce Commission’s 2024 transmission pricing methodology reset could lift Vector’s annual transmission bill by an estimated NZD 10–30m.

Shortage of Specialized Technical Labor

The New Zealand infrastructure sector faces a persistent shortage of skilled electrical engineers and technicians for network maintenance and upgrades; MBIE reported a 23% vacancy rate in electrical trades in 2024. By end-2025, competition from global renewable projects has pushed average contractor rates up 18%, raising Vector’s labor cost per FTE by ~NZD 15k annually. Vector must offer competitive pay and 3–5 year contracts to meet Commerce Commission reliability standards.

Volatility in Raw Material Costs

Volatility in copper, transformer cores, and utility pole prices—copper up 35% in 2024 and global electrification demand rising 18% in 2025—raises Vector’s capex by an estimated 12% year-over-year despite long-term contracts.

Suppliers gain leverage when geopolitical or climate disruptions shrink supply; they can pass costs through, pressuring margins and forcing Vector to renegotiate or absorb higher unit costs.

- Copper +35% (2024)

- Electrification demand +18% (2025)

- Estimated capex pressure +12% YoY

- Supply shocks increase supplier pass-through risk

Strategic Partnerships in Fiber Infrastructure

Vector’s telecom arm relies on a small set of hardware suppliers for fiber-optic transceivers and high-speed routers, creating supplier leverage as 2025 standards push >800 Gbps links; top vendors control ~60–70% market share in key components (2024 data).

Rapid obsolescence forces Vector to keep preferred vendor relationships and pre-buy capacity, raising capex and working-capital needs and allowing suppliers to set premium lead times and pricing.

Here’s the quick math: if 2025 upgrade requires 30% more high-capacity modules, supplier-driven price increases of 10–15% raise upgrade bill by ~3–4.5% of network capex.

- Dependency on few suppliers: 60–70% market share

- 2025 capacity target: >800 Gbps links

- Price risk: suppliers can add 10–15%

- Capex impact: ~3–4.5% increase

Supplier squeeze: Transpower, vendor concentration and rising copper push Vector costs up

Vector faces high supplier power: Transpower transmission costs were NZD 322m (FY2024, 24% of opex), two smart‑meter vendors supply ~70% of rollouts (2025), copper rose 35% (2024) and electrification demand +18% (2025), pushing capex ~+12% YoY and contractor rates +18%, forcing prebuys, premium lead times and renegotiation risk.

| Metric | Value |

|---|---|

| Transpower charges (FY2024) | NZD 322m |

| Smart‑meter vendor concentration (2025) | ~70% |

| Copper price change (2024) | +35% |

| Electrification demand (2025) | +18% |

| Estimated capex pressure | +12% YoY |

| Contractor rate rise | +18% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Vector, revealing competitive intensity, buyer and supplier power, entry barriers, substitute threats, and strategic levers to strengthen market position and profitability.

Concise five-forces summary that highlights competitive pressures at a glance—ideal for fast strategic decisions and investor briefings.

Customers Bargaining Power

Regulatory Oversight as a Buyer Proxy

In NZ’s regulated electricity and gas distribution, the Commerce Commission sets price-quality paths and acts as a buyer proxy, capping Vector’s price-setting freedom and boosting customers’ collective bargaining power via regulation.

Regulatory limits mean Vector cannot unilaterally raise prices; the 2023–28 Default Price-Quality Path constrained allowed revenue growth to about CPI+1.0% annually, tying increases to service outcomes.

By 2025, stricter transparency rules require detailed cost-justifications and performance metrics; any price adjustments face public consultation and Commission scrutiny, reducing pricing leeway.

Concentration of Energy Retailers

Vector’s direct customers are a few large energy retailers who bundle distribution for end-users; Mercury NZ and Genesis Energy together accounted for roughly 40–50% of retail market volumes in 2024, concentrating bargaining power.

Those dominant retailers can press for tighter service-levels and lower operational charges; in 2024 retailer-led negotiations influenced Vector’s proposed price paths in the Commerce Commission review.

Retailers’ analytics teams routinely push back on Vector’s cost allocations and seek favorable terms, raising regulatory risk and margin pressure on Vector’s distribution revenues.

Price Sensitivity of Industrial Consumers

Large industrial customers in Auckland—many drawing 10–50 MW and representing ~25–30% of Vector Limited’s (NZX: VCT) distribution revenue—can switch to behind-the-meter generation or third-party suppliers if Vector raises transmission charges, so they wield strong price sensitivity and exit threats.

Low Switching Costs in Fiber Services

Unlike the physical electricity monopoly, Vector’s fiber customers face low switching costs and can choose among multiple Auckland broadband providers, reducing customer lock-in.

In 2025 Auckland market data shows ~4 national and 20+ regional retail ISPs; retailers can shift to alternative wholesalers if Vector’s pricing or reliability lags, pressuring margins.

This forces Vector to keep high uptime (target ≥99.95% SLA), competitive wholesale MRCs and product innovation to retain wholesale clients and limit churn.

- Multiple ISPs: ~24 in Auckland (2025)

- Required SLA: ≥99.95% uptime

- Wholesale margin pressure if prices not competitive

- Retention via product innovation and reliability

Growing Consumer Demand for Transparency

Modern residential customers use smart meters and apps to track energy in real time; 65% of UK households had smart meters by end-2024, raising service expectations for Vector.

They demand proactive outage alerts and network transparency; missed SLAs increase complaints and can shift regulators—Ofgem fines reached £64m in 2023 across utilities, showing political risk.

Vector must invest in customer tech and communications; a circa £20–50m program (example capex range for medium network upgrades) would cut churn and regulatory exposure.

- 65% smart-meter adoption (UK, 2024)

- Ofgem fines £64m (2023)

- Estimated upgrade capex £20–50m

Regulation caps Vector growth; concentrated buyers and low-switching fiber force tight SLAs

Regulation (Commerce Commission DPP 2023–28) caps Vector’s allowed revenue to ~CPI+1.0% pa, cutting unilateral pricing power; large retailers (Mercury, Genesis ~40–50% retail volumes in 2024) and Auckland industrials (~25–30% of VCT distribution revenue) concentrate bargaining leverage; fiber customers face low switching costs (~24 ISPs in Auckland, 2025) forcing uptime targets ≥99.95% and product/price competitiveness.

| Metric | Value |

|---|---|

| DPP allowed revenue growth | CPI+1.0% pa (2023–28) |

| Retailer concentration | Mercury+Genesis ~40–50% (2024) |

| Industrial revenue share | ~25–30% of VCT distribution rev (2024) |

| ISPs in Auckland | ~24 (2025) |

| Uptime SLA | ≥99.95% |

Full Version Awaits

Vector Porter's Five Forces Analysis

This preview shows the exact Vector Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Vector’s Porter's Five Forces snapshot highlights how supplier leverage, buyer bargaining, competitive rivalry, substitute threats, and entry barriers shape its strategic position, revealing pockets of strength and vulnerability that inform tactical choices.

This brief overview teases force-level dynamics and market pressures but stops short of the granular ratings, data visualizations, and scenario implications you need for confident decisions.

Unlock the full Porter's Five Forces Analysis for Vector to access force-by-force scores, charts, and actionable recommendations—perfect for investor presentations, strategic planning, or execution.

Suppliers Bargaining Power

Concentration of Specialized Technology Providers

Vector relies on a handful of global suppliers for smart meters and grid software; by 2025 about 70% of its new smart meter rollouts use two vendors, raising supplier leverage.

Reliance on Transpower for Transmission Services

As sole owner of New Zealand’s national grid, Transpower supplies all high-voltage transmission to Vector’s network, creating strong supplier power despite regulated pricing; Vector paid about NZD 322m in transmission charges in FY2024, 24% of its operating costs. Vector remains exposed to Transpower’s investment timing and outages, and the Commerce Commission’s 2024 transmission pricing methodology reset could lift Vector’s annual transmission bill by an estimated NZD 10–30m.

Shortage of Specialized Technical Labor

The New Zealand infrastructure sector faces a persistent shortage of skilled electrical engineers and technicians for network maintenance and upgrades; MBIE reported a 23% vacancy rate in electrical trades in 2024. By end-2025, competition from global renewable projects has pushed average contractor rates up 18%, raising Vector’s labor cost per FTE by ~NZD 15k annually. Vector must offer competitive pay and 3–5 year contracts to meet Commerce Commission reliability standards.

Volatility in Raw Material Costs

Volatility in copper, transformer cores, and utility pole prices—copper up 35% in 2024 and global electrification demand rising 18% in 2025—raises Vector’s capex by an estimated 12% year-over-year despite long-term contracts.

Suppliers gain leverage when geopolitical or climate disruptions shrink supply; they can pass costs through, pressuring margins and forcing Vector to renegotiate or absorb higher unit costs.

- Copper +35% (2024)

- Electrification demand +18% (2025)

- Estimated capex pressure +12% YoY

- Supply shocks increase supplier pass-through risk

Strategic Partnerships in Fiber Infrastructure

Vector’s telecom arm relies on a small set of hardware suppliers for fiber-optic transceivers and high-speed routers, creating supplier leverage as 2025 standards push >800 Gbps links; top vendors control ~60–70% market share in key components (2024 data).

Rapid obsolescence forces Vector to keep preferred vendor relationships and pre-buy capacity, raising capex and working-capital needs and allowing suppliers to set premium lead times and pricing.

Here’s the quick math: if 2025 upgrade requires 30% more high-capacity modules, supplier-driven price increases of 10–15% raise upgrade bill by ~3–4.5% of network capex.

- Dependency on few suppliers: 60–70% market share

- 2025 capacity target: >800 Gbps links

- Price risk: suppliers can add 10–15%

- Capex impact: ~3–4.5% increase

Supplier squeeze: Transpower, vendor concentration and rising copper push Vector costs up

Vector faces high supplier power: Transpower transmission costs were NZD 322m (FY2024, 24% of opex), two smart‑meter vendors supply ~70% of rollouts (2025), copper rose 35% (2024) and electrification demand +18% (2025), pushing capex ~+12% YoY and contractor rates +18%, forcing prebuys, premium lead times and renegotiation risk.

| Metric | Value |

|---|---|

| Transpower charges (FY2024) | NZD 322m |

| Smart‑meter vendor concentration (2025) | ~70% |

| Copper price change (2024) | +35% |

| Electrification demand (2025) | +18% |

| Estimated capex pressure | +12% YoY |

| Contractor rate rise | +18% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Vector, revealing competitive intensity, buyer and supplier power, entry barriers, substitute threats, and strategic levers to strengthen market position and profitability.

Concise five-forces summary that highlights competitive pressures at a glance—ideal for fast strategic decisions and investor briefings.

Customers Bargaining Power

Regulatory Oversight as a Buyer Proxy

In NZ’s regulated electricity and gas distribution, the Commerce Commission sets price-quality paths and acts as a buyer proxy, capping Vector’s price-setting freedom and boosting customers’ collective bargaining power via regulation.

Regulatory limits mean Vector cannot unilaterally raise prices; the 2023–28 Default Price-Quality Path constrained allowed revenue growth to about CPI+1.0% annually, tying increases to service outcomes.

By 2025, stricter transparency rules require detailed cost-justifications and performance metrics; any price adjustments face public consultation and Commission scrutiny, reducing pricing leeway.

Concentration of Energy Retailers

Vector’s direct customers are a few large energy retailers who bundle distribution for end-users; Mercury NZ and Genesis Energy together accounted for roughly 40–50% of retail market volumes in 2024, concentrating bargaining power.

Those dominant retailers can press for tighter service-levels and lower operational charges; in 2024 retailer-led negotiations influenced Vector’s proposed price paths in the Commerce Commission review.

Retailers’ analytics teams routinely push back on Vector’s cost allocations and seek favorable terms, raising regulatory risk and margin pressure on Vector’s distribution revenues.

Price Sensitivity of Industrial Consumers

Large industrial customers in Auckland—many drawing 10–50 MW and representing ~25–30% of Vector Limited’s (NZX: VCT) distribution revenue—can switch to behind-the-meter generation or third-party suppliers if Vector raises transmission charges, so they wield strong price sensitivity and exit threats.

Low Switching Costs in Fiber Services

Unlike the physical electricity monopoly, Vector’s fiber customers face low switching costs and can choose among multiple Auckland broadband providers, reducing customer lock-in.

In 2025 Auckland market data shows ~4 national and 20+ regional retail ISPs; retailers can shift to alternative wholesalers if Vector’s pricing or reliability lags, pressuring margins.

This forces Vector to keep high uptime (target ≥99.95% SLA), competitive wholesale MRCs and product innovation to retain wholesale clients and limit churn.

- Multiple ISPs: ~24 in Auckland (2025)

- Required SLA: ≥99.95% uptime

- Wholesale margin pressure if prices not competitive

- Retention via product innovation and reliability

Growing Consumer Demand for Transparency

Modern residential customers use smart meters and apps to track energy in real time; 65% of UK households had smart meters by end-2024, raising service expectations for Vector.

They demand proactive outage alerts and network transparency; missed SLAs increase complaints and can shift regulators—Ofgem fines reached £64m in 2023 across utilities, showing political risk.

Vector must invest in customer tech and communications; a circa £20–50m program (example capex range for medium network upgrades) would cut churn and regulatory exposure.

- 65% smart-meter adoption (UK, 2024)

- Ofgem fines £64m (2023)

- Estimated upgrade capex £20–50m

Regulation caps Vector growth; concentrated buyers and low-switching fiber force tight SLAs

Regulation (Commerce Commission DPP 2023–28) caps Vector’s allowed revenue to ~CPI+1.0% pa, cutting unilateral pricing power; large retailers (Mercury, Genesis ~40–50% retail volumes in 2024) and Auckland industrials (~25–30% of VCT distribution revenue) concentrate bargaining leverage; fiber customers face low switching costs (~24 ISPs in Auckland, 2025) forcing uptime targets ≥99.95% and product/price competitiveness.

| Metric | Value |

|---|---|

| DPP allowed revenue growth | CPI+1.0% pa (2023–28) |

| Retailer concentration | Mercury+Genesis ~40–50% (2024) |

| Industrial revenue share | ~25–30% of VCT distribution rev (2024) |

| ISPs in Auckland | ~24 (2025) |

| Uptime SLA | ≥99.95% |

Full Version Awaits

Vector Porter's Five Forces Analysis

This preview shows the exact Vector Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.