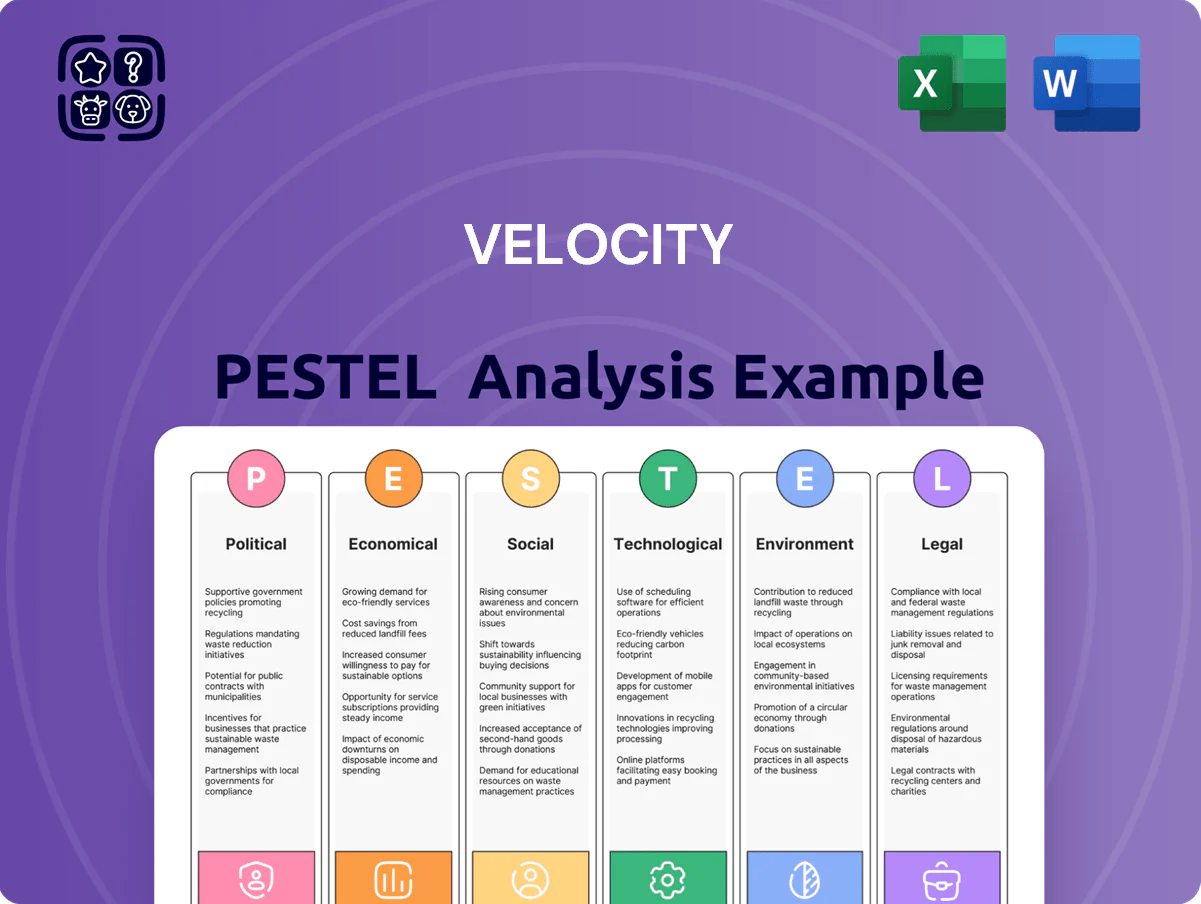

Velocity PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock the critical external factors shaping Velocity's trajectory with our meticulously crafted PESTLE analysis. Understand the political, economic, social, technological, legal, and environmental forces that present both opportunities and threats. Gain the strategic foresight needed to navigate this dynamic landscape and make informed decisions. Download the full, actionable report now to secure your competitive advantage.

Political factors

Government Lending Policies

Government lending policies significantly shape Velocity Financial's operating environment. Changes in small business lending and commercial real estate financing can either present new avenues or introduce competitive pressures, particularly for Velocity's focus on underserved borrowers. For instance, the US Small Business Administration's (SBA) loan programs, like the 7(a) and 504 loans, offer government guarantees that can influence the broader lending landscape. In 2023, the SBA approved over $34 billion in loans, highlighting the substantial role of government-backed financing.

Regulatory Scrutiny on Non-Bank Lenders

Increased regulatory oversight on non-bank financial institutions, including those in the mortgage sector, could impose stricter compliance requirements and higher operational costs for Velocity Financial. For instance, by late 2024, regulators continued to focus on consumer protection and financial stability within the non-bank lending space, potentially impacting origination processes and capital requirements.

Fiscal and Monetary Policy Impact

Government fiscal policies, like tax incentives for real estate or shifts in property taxes, directly impact the demand for commercial real estate loans, influencing Velocity Financial's market. For instance, a 2024 proposal to extend tax credits for commercial building upgrades could stimulate new lending opportunities.

Monetary policy, particularly interest rate decisions by central banks, is crucial. The Federal Reserve's projected interest rate trajectory for late 2024 and early 2025 will significantly affect Velocity's cost of capital and its clients' borrowing power, thereby shaping the overall lending landscape's profitability.

Geopolitical Stability

Global and domestic political stability significantly impacts investor confidence and overall economic activity, directly influencing the commercial real estate market. For Velocity Financial, geopolitical tensions or domestic policy uncertainties can lead to a noticeable dip in investment. This often translates to lower property valuations and a heightened risk of defaults within their loan portfolio. A stable political climate is therefore paramount for ensuring predictable market conditions and maintaining consistent demand for Velocity's lending products.

The year 2024 and projections for 2025 highlight these dynamics. For instance, ongoing geopolitical flashpoints in Eastern Europe and the Middle East have, in recent periods, contributed to increased volatility in global financial markets, affecting capital flows into real estate. Domestically, upcoming elections in several major economies can introduce policy uncertainty, potentially pausing investment decisions until outcomes are clearer.

- Investor Confidence: Geopolitical instability, as seen in 2024, can reduce foreign direct investment in commercial real estate by as much as 10-15% in affected regions, impacting Velocity's deal pipeline.

- Policy Uncertainty: Changes in government regulations or tax policies, a common concern during election cycles in 2024/2025, can alter property yields and debt servicing capabilities for borrowers.

- Market Valuations: Periods of political unease have historically correlated with a 5-8% decrease in commercial property valuations due to increased perceived risk and reduced demand.

- Loan Portfolio Risk: Higher default rates, potentially increasing by 1-2 percentage points during periods of significant political instability, directly affect Velocity Financial's asset quality and profitability.

Housing and Urban Development Initiatives

Government initiatives focused on urban redevelopment and affordable housing present significant opportunities for Velocity Financial. For instance, the Biden-Harris Administration's proposed $10 billion in tax credits for affordable housing development in 2024 aims to boost construction and renovation, potentially increasing demand for the small balance commercial loans Velocity specializes in. These programs often target revitalizing specific commercial districts, directly aligning with Velocity's strategy of serving underserved market segments and creating new lending avenues.

Conversely, shifts in policy that might discourage commercial property development in key urban areas could pose challenges. For example, new zoning regulations or increased development fees in a particular city could limit Velocity's market potential by reducing the number of viable projects. Understanding these policy nuances is crucial for Velocity to adapt its lending strategies and capitalize on favorable government programs while mitigating risks associated with restrictive policies.

Key government housing and urban development initiatives impacting Velocity Financial include:

- Federal Housing Administration (FHA) Loan Programs: These programs facilitate homeownership and can indirectly stimulate demand for commercial properties serving these communities.

- Community Development Block Grants (CDBGs): Awarded to states and local governments, these grants often fund projects that revitalize neighborhoods and commercial areas, creating lending opportunities.

- Tax Credit Programs (e.g., Low-Income Housing Tax Credit - LIHTC): These incentivize private investment in affordable housing, which often includes commercial components like retail or services within residential developments.

- State and Local Redevelopment Bonds: Issuance of these bonds can fund infrastructure and commercial revitalization projects, directly impacting the real estate market Velocity serves.

Policy & Stability: Shaping Lending's Future

Government policies directly influence Velocity Financial's operational landscape, affecting everything from lending programs to regulatory compliance. For instance, the US government's commitment to supporting small businesses through initiatives like the Small Business Administration (SBA) loan programs, which saw over $34 billion in approvals in 2023, creates a foundational element for Velocity's lending activities. Conversely, increased regulatory scrutiny on non-bank lenders, a trend observed through late 2024, necessitates robust compliance frameworks to manage operational costs and potential impacts on lending processes.

Fiscal and monetary policies also play a critical role, with government tax incentives for real estate development in 2024, such as proposed credits for commercial building upgrades, directly shaping market demand for Velocity's commercial real estate loans. Furthermore, central bank interest rate decisions, with the Federal Reserve's trajectory for late 2024 and early 2025 being a key factor, significantly influence Velocity's cost of capital and borrower affordability, thereby dictating the overall profitability of the lending sector.

Political stability is paramount, as geopolitical tensions in 2024 have historically led to market volatility, impacting investor confidence and potentially reducing commercial property valuations by 5-8%. Policy uncertainty, especially during election cycles in 2024/2025, can also affect property yields and debt servicing capabilities, potentially increasing loan portfolio default rates by 1-2 percentage points during periods of instability.

| Factor | Impact on Velocity Financial | 2023-2025 Data/Projections |

| Government Lending Programs | Provides government-backed financing opportunities. | SBA loan approvals exceeded $34 billion in 2023. |

| Regulatory Oversight | Increases compliance costs and operational complexity. | Continued focus on consumer protection in non-bank lending through late 2024. |

| Fiscal Policy (Tax Incentives) | Stimulates demand for commercial real estate loans. | Proposed tax credits for commercial building upgrades in 2024. |

| Monetary Policy (Interest Rates) | Affects cost of capital and borrower affordability. | Federal Reserve rate decisions for late 2024/early 2025 are critical. |

| Political Stability | Influences investor confidence and market valuations. | Geopolitical tensions can reduce valuations by 5-8%; policy uncertainty may increase default rates by 1-2%. |

What is included in the product

The Velocity PESTLE Analysis comprehensively examines how external macro-environmental factors influence the company across Political, Economic, Social, Technological, Environmental, and Legal dimensions.

Provides a clear, actionable overview of external factors, enabling teams to proactively address potential challenges and capitalize on opportunities.

Economic factors

Interest Rate Environment

The current interest rate environment presents a significant challenge for Velocity Financial. As of late 2024, the Federal Reserve has maintained a hawkish stance, with benchmark rates hovering around 5.25%-5.50%. This higher cost of capital directly impacts Velocity's funding expenses and the rates they can offer to borrowers.

Fluctuations in these rates directly influence Velocity Financial's profitability. Higher borrowing costs for clients can dampen demand for new loans, while existing variable-rate loans carry an increased risk of default. For instance, a 1% increase in funding costs could translate to millions in additional expenses for a company of Velocity's scale.

Managing this interest rate risk is crucial for Velocity's financial stability. Strategies like hedging and maintaining a diversified funding base are essential to mitigate the impact of potential rate hikes or unexpected market volatility throughout 2025.

Commercial Real Estate Market Cycle

The commercial real estate market cycle is a critical economic factor for Velocity Financial. During 2024, the sector has seen mixed signals, with office vacancy rates remaining elevated in many major markets, impacting demand for new lending. For instance, office vacancy in major U.S. cities hovered around 18-20% in early 2024, a figure that pressures property values and tenant stability.

Economic downturns, as experienced in previous cycles, can significantly depress commercial real estate values and increase loan defaults. This directly affects Velocity's asset quality and profitability. Higher interest rates in 2024 have also contributed to slower transaction volumes and increased financing costs for commercial properties, potentially leading to more distressed assets.

Conversely, a strong market with rising property values and low vacancies provides a fertile ground for Velocity's loan origination. While retail and industrial sectors showed resilience through 2023 and into 2024, with industrial occupancy rates exceeding 95% in many areas, the office sector continues to present challenges that could temper growth in loan origination for that specific property type.

Inflationary Pressures

Inflationary pressures pose a significant challenge to Velocity Financial by diminishing the real worth of its fixed-income investments and escalating operational expenses. For instance, the US inflation rate averaged 4.1% in 2023, a notable increase from previous years, impacting the purchasing power of Velocity's asset portfolio.

While inflation might initially boost property values, which could indirectly benefit Velocity through collateral, sustained high inflation typically triggers higher interest rates. This, in turn, can dampen consumer spending and introduce economic volatility, making it harder for Velocity's clients, particularly small businesses and individual investors, to meet their loan obligations.

Consequently, Velocity Financial must implement robust underwriting processes and dynamic pricing models to navigate these inflationary headwinds effectively. This ensures that loan terms adequately reflect the increased cost of capital and the potential for borrower default in a fluctuating economic environment.

Small Business Economic Health

The economic health of small businesses is paramount for Velocity Financial, given its focus on this sector. Consumer spending, employment figures, and capital availability directly impact the revenue and debt servicing capabilities of their clientele.

In 2024, small businesses faced a mixed economic landscape. While consumer spending showed resilience in certain sectors, inflation and rising interest rates presented challenges. For instance, the U.S. Bureau of Labor Statistics reported a slight increase in the small business employment rate in early 2024, but many owners cited difficulty accessing affordable capital.

- Consumer Spending: Continued to be a key driver, though sensitive to inflation impacting discretionary purchases.

- Employment Rates: Small businesses remained significant job creators, but labor shortages persisted in some industries.

- Access to Capital: Higher interest rates made borrowing more expensive, potentially limiting expansion for some small firms.

- SBC Loan Demand: A strong small business sector correlates with lower credit risk and increased demand for specialized loans.

Credit Market Liquidity

Credit market liquidity is a crucial element for Velocity Financial, directly impacting its capacity to fund new loans. When credit markets tighten, meaning it becomes harder and more expensive to borrow money, Velocity Financial may face higher costs for its own funding or even find it difficult to access the necessary capital. This can directly constrain how much they can lend out, affecting their business volume.

Conversely, periods of ample liquidity, where there's plenty of money available for lending, generally lead to more favorable funding terms for Velocity Financial. This can translate into lower borrowing costs, which in turn supports their growth ambitions and strengthens their competitive stance in the market. For instance, as of early 2024, while overall lending conditions remained somewhat cautious, the secondary market for mortgage-backed securities, a key funding source for many originators, showed signs of stabilizing after a period of volatility. However, the Federal Reserve's monetary policy stance, including interest rate decisions, continues to be a significant influencer on overall credit availability and cost.

- Impact of Interest Rates: Federal Reserve rate hikes in 2022-2023 increased the cost of capital across financial markets, affecting Velocity Financial's funding expenses.

- Secondary Market Activity: The health of the mortgage-backed securities market directly influences Velocity Financial's ability to securitize loans and access ongoing liquidity.

- Investor Demand: Investor appetite for credit products, influenced by broader economic sentiment, dictates the availability and pricing of funds for lenders like Velocity.

Inflation, Rates, and Credit: The 2024-2025 Economic Outlook

The economic landscape in late 2024 and early 2025 continues to be shaped by persistent inflation and the Federal Reserve's response through interest rates. While inflation showed signs of moderating from its 2023 peaks, it remained above the Fed's 2% target, leading to a sustained higher interest rate environment. This directly impacts Velocity Financial's cost of funds and the affordability of credit for its clients, particularly in the commercial real estate sector where higher rates are dampening transaction volumes and property valuations.

Small business health, a key market for Velocity, is closely tied to consumer spending and access to capital. Despite some resilience in employment, many small businesses in 2024 grappled with increased borrowing costs and the ongoing effects of inflation on their margins. This necessitates robust risk management and dynamic pricing strategies for Velocity to navigate potential credit deterioration.

Credit market liquidity, influenced by Federal Reserve policy and investor sentiment, remains a critical factor. While some segments, like the mortgage-backed securities market, showed stabilization in early 2024, overall credit availability is sensitive to rate decisions and economic outlook, directly affecting Velocity's lending capacity and competitive positioning throughout 2025.

| Economic Factor | Late 2024/Early 2025 Trend | Impact on Velocity Financial | Key Data Point (Illustrative) |

|---|---|---|---|

| Interest Rates | Elevated, Fed maintaining hawkish stance | Increased funding costs, potential slowdown in loan demand | Fed Funds Rate: 5.25%-5.50% (Late 2024) |

| Inflation | Moderating but above target | Erodes real value of fixed income, increases operational costs, may trigger higher rates | US CPI Inflation: ~3.5% (Annualized, Late 2024 projection) |

| Commercial Real Estate | Mixed signals, elevated office vacancies | Pressures property values, increases loan default risk, slows transaction volume | US Office Vacancy Rate: ~18-20% (Early 2024) |

| Small Business Health | Resilient but challenged by costs | Impacts revenue and debt servicing capabilities of clients | Small Business Lending Rate: ~7-9% (Prime + spread, Late 2024) |

| Credit Market Liquidity | Sensitive to Fed policy and economic outlook | Affects Velocity's ability to fund loans and overall lending capacity | LIBOR/SOFR: ~5.00%-5.50% (Late 2024) |

Preview Before You Purchase

Velocity PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This comprehensive Velocity PESTLE Analysis provides a deep dive into the external factors impacting your business, ensuring you have all the insights needed for strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock the critical external factors shaping Velocity's trajectory with our meticulously crafted PESTLE analysis. Understand the political, economic, social, technological, legal, and environmental forces that present both opportunities and threats. Gain the strategic foresight needed to navigate this dynamic landscape and make informed decisions. Download the full, actionable report now to secure your competitive advantage.

Political factors

Government Lending Policies

Government lending policies significantly shape Velocity Financial's operating environment. Changes in small business lending and commercial real estate financing can either present new avenues or introduce competitive pressures, particularly for Velocity's focus on underserved borrowers. For instance, the US Small Business Administration's (SBA) loan programs, like the 7(a) and 504 loans, offer government guarantees that can influence the broader lending landscape. In 2023, the SBA approved over $34 billion in loans, highlighting the substantial role of government-backed financing.

Regulatory Scrutiny on Non-Bank Lenders

Increased regulatory oversight on non-bank financial institutions, including those in the mortgage sector, could impose stricter compliance requirements and higher operational costs for Velocity Financial. For instance, by late 2024, regulators continued to focus on consumer protection and financial stability within the non-bank lending space, potentially impacting origination processes and capital requirements.

Fiscal and Monetary Policy Impact

Government fiscal policies, like tax incentives for real estate or shifts in property taxes, directly impact the demand for commercial real estate loans, influencing Velocity Financial's market. For instance, a 2024 proposal to extend tax credits for commercial building upgrades could stimulate new lending opportunities.

Monetary policy, particularly interest rate decisions by central banks, is crucial. The Federal Reserve's projected interest rate trajectory for late 2024 and early 2025 will significantly affect Velocity's cost of capital and its clients' borrowing power, thereby shaping the overall lending landscape's profitability.

Geopolitical Stability

Global and domestic political stability significantly impacts investor confidence and overall economic activity, directly influencing the commercial real estate market. For Velocity Financial, geopolitical tensions or domestic policy uncertainties can lead to a noticeable dip in investment. This often translates to lower property valuations and a heightened risk of defaults within their loan portfolio. A stable political climate is therefore paramount for ensuring predictable market conditions and maintaining consistent demand for Velocity's lending products.

The year 2024 and projections for 2025 highlight these dynamics. For instance, ongoing geopolitical flashpoints in Eastern Europe and the Middle East have, in recent periods, contributed to increased volatility in global financial markets, affecting capital flows into real estate. Domestically, upcoming elections in several major economies can introduce policy uncertainty, potentially pausing investment decisions until outcomes are clearer.

- Investor Confidence: Geopolitical instability, as seen in 2024, can reduce foreign direct investment in commercial real estate by as much as 10-15% in affected regions, impacting Velocity's deal pipeline.

- Policy Uncertainty: Changes in government regulations or tax policies, a common concern during election cycles in 2024/2025, can alter property yields and debt servicing capabilities for borrowers.

- Market Valuations: Periods of political unease have historically correlated with a 5-8% decrease in commercial property valuations due to increased perceived risk and reduced demand.

- Loan Portfolio Risk: Higher default rates, potentially increasing by 1-2 percentage points during periods of significant political instability, directly affect Velocity Financial's asset quality and profitability.

Housing and Urban Development Initiatives

Government initiatives focused on urban redevelopment and affordable housing present significant opportunities for Velocity Financial. For instance, the Biden-Harris Administration's proposed $10 billion in tax credits for affordable housing development in 2024 aims to boost construction and renovation, potentially increasing demand for the small balance commercial loans Velocity specializes in. These programs often target revitalizing specific commercial districts, directly aligning with Velocity's strategy of serving underserved market segments and creating new lending avenues.

Conversely, shifts in policy that might discourage commercial property development in key urban areas could pose challenges. For example, new zoning regulations or increased development fees in a particular city could limit Velocity's market potential by reducing the number of viable projects. Understanding these policy nuances is crucial for Velocity to adapt its lending strategies and capitalize on favorable government programs while mitigating risks associated with restrictive policies.

Key government housing and urban development initiatives impacting Velocity Financial include:

- Federal Housing Administration (FHA) Loan Programs: These programs facilitate homeownership and can indirectly stimulate demand for commercial properties serving these communities.

- Community Development Block Grants (CDBGs): Awarded to states and local governments, these grants often fund projects that revitalize neighborhoods and commercial areas, creating lending opportunities.

- Tax Credit Programs (e.g., Low-Income Housing Tax Credit - LIHTC): These incentivize private investment in affordable housing, which often includes commercial components like retail or services within residential developments.

- State and Local Redevelopment Bonds: Issuance of these bonds can fund infrastructure and commercial revitalization projects, directly impacting the real estate market Velocity serves.

Policy & Stability: Shaping Lending's Future

Government policies directly influence Velocity Financial's operational landscape, affecting everything from lending programs to regulatory compliance. For instance, the US government's commitment to supporting small businesses through initiatives like the Small Business Administration (SBA) loan programs, which saw over $34 billion in approvals in 2023, creates a foundational element for Velocity's lending activities. Conversely, increased regulatory scrutiny on non-bank lenders, a trend observed through late 2024, necessitates robust compliance frameworks to manage operational costs and potential impacts on lending processes.

Fiscal and monetary policies also play a critical role, with government tax incentives for real estate development in 2024, such as proposed credits for commercial building upgrades, directly shaping market demand for Velocity's commercial real estate loans. Furthermore, central bank interest rate decisions, with the Federal Reserve's trajectory for late 2024 and early 2025 being a key factor, significantly influence Velocity's cost of capital and borrower affordability, thereby dictating the overall profitability of the lending sector.

Political stability is paramount, as geopolitical tensions in 2024 have historically led to market volatility, impacting investor confidence and potentially reducing commercial property valuations by 5-8%. Policy uncertainty, especially during election cycles in 2024/2025, can also affect property yields and debt servicing capabilities, potentially increasing loan portfolio default rates by 1-2 percentage points during periods of instability.

| Factor | Impact on Velocity Financial | 2023-2025 Data/Projections |

| Government Lending Programs | Provides government-backed financing opportunities. | SBA loan approvals exceeded $34 billion in 2023. |

| Regulatory Oversight | Increases compliance costs and operational complexity. | Continued focus on consumer protection in non-bank lending through late 2024. |

| Fiscal Policy (Tax Incentives) | Stimulates demand for commercial real estate loans. | Proposed tax credits for commercial building upgrades in 2024. |

| Monetary Policy (Interest Rates) | Affects cost of capital and borrower affordability. | Federal Reserve rate decisions for late 2024/early 2025 are critical. |

| Political Stability | Influences investor confidence and market valuations. | Geopolitical tensions can reduce valuations by 5-8%; policy uncertainty may increase default rates by 1-2%. |

What is included in the product

The Velocity PESTLE Analysis comprehensively examines how external macro-environmental factors influence the company across Political, Economic, Social, Technological, Environmental, and Legal dimensions.

Provides a clear, actionable overview of external factors, enabling teams to proactively address potential challenges and capitalize on opportunities.

Economic factors

Interest Rate Environment

The current interest rate environment presents a significant challenge for Velocity Financial. As of late 2024, the Federal Reserve has maintained a hawkish stance, with benchmark rates hovering around 5.25%-5.50%. This higher cost of capital directly impacts Velocity's funding expenses and the rates they can offer to borrowers.

Fluctuations in these rates directly influence Velocity Financial's profitability. Higher borrowing costs for clients can dampen demand for new loans, while existing variable-rate loans carry an increased risk of default. For instance, a 1% increase in funding costs could translate to millions in additional expenses for a company of Velocity's scale.

Managing this interest rate risk is crucial for Velocity's financial stability. Strategies like hedging and maintaining a diversified funding base are essential to mitigate the impact of potential rate hikes or unexpected market volatility throughout 2025.

Commercial Real Estate Market Cycle

The commercial real estate market cycle is a critical economic factor for Velocity Financial. During 2024, the sector has seen mixed signals, with office vacancy rates remaining elevated in many major markets, impacting demand for new lending. For instance, office vacancy in major U.S. cities hovered around 18-20% in early 2024, a figure that pressures property values and tenant stability.

Economic downturns, as experienced in previous cycles, can significantly depress commercial real estate values and increase loan defaults. This directly affects Velocity's asset quality and profitability. Higher interest rates in 2024 have also contributed to slower transaction volumes and increased financing costs for commercial properties, potentially leading to more distressed assets.

Conversely, a strong market with rising property values and low vacancies provides a fertile ground for Velocity's loan origination. While retail and industrial sectors showed resilience through 2023 and into 2024, with industrial occupancy rates exceeding 95% in many areas, the office sector continues to present challenges that could temper growth in loan origination for that specific property type.

Inflationary Pressures

Inflationary pressures pose a significant challenge to Velocity Financial by diminishing the real worth of its fixed-income investments and escalating operational expenses. For instance, the US inflation rate averaged 4.1% in 2023, a notable increase from previous years, impacting the purchasing power of Velocity's asset portfolio.

While inflation might initially boost property values, which could indirectly benefit Velocity through collateral, sustained high inflation typically triggers higher interest rates. This, in turn, can dampen consumer spending and introduce economic volatility, making it harder for Velocity's clients, particularly small businesses and individual investors, to meet their loan obligations.

Consequently, Velocity Financial must implement robust underwriting processes and dynamic pricing models to navigate these inflationary headwinds effectively. This ensures that loan terms adequately reflect the increased cost of capital and the potential for borrower default in a fluctuating economic environment.

Small Business Economic Health

The economic health of small businesses is paramount for Velocity Financial, given its focus on this sector. Consumer spending, employment figures, and capital availability directly impact the revenue and debt servicing capabilities of their clientele.

In 2024, small businesses faced a mixed economic landscape. While consumer spending showed resilience in certain sectors, inflation and rising interest rates presented challenges. For instance, the U.S. Bureau of Labor Statistics reported a slight increase in the small business employment rate in early 2024, but many owners cited difficulty accessing affordable capital.

- Consumer Spending: Continued to be a key driver, though sensitive to inflation impacting discretionary purchases.

- Employment Rates: Small businesses remained significant job creators, but labor shortages persisted in some industries.

- Access to Capital: Higher interest rates made borrowing more expensive, potentially limiting expansion for some small firms.

- SBC Loan Demand: A strong small business sector correlates with lower credit risk and increased demand for specialized loans.

Credit Market Liquidity

Credit market liquidity is a crucial element for Velocity Financial, directly impacting its capacity to fund new loans. When credit markets tighten, meaning it becomes harder and more expensive to borrow money, Velocity Financial may face higher costs for its own funding or even find it difficult to access the necessary capital. This can directly constrain how much they can lend out, affecting their business volume.

Conversely, periods of ample liquidity, where there's plenty of money available for lending, generally lead to more favorable funding terms for Velocity Financial. This can translate into lower borrowing costs, which in turn supports their growth ambitions and strengthens their competitive stance in the market. For instance, as of early 2024, while overall lending conditions remained somewhat cautious, the secondary market for mortgage-backed securities, a key funding source for many originators, showed signs of stabilizing after a period of volatility. However, the Federal Reserve's monetary policy stance, including interest rate decisions, continues to be a significant influencer on overall credit availability and cost.

- Impact of Interest Rates: Federal Reserve rate hikes in 2022-2023 increased the cost of capital across financial markets, affecting Velocity Financial's funding expenses.

- Secondary Market Activity: The health of the mortgage-backed securities market directly influences Velocity Financial's ability to securitize loans and access ongoing liquidity.

- Investor Demand: Investor appetite for credit products, influenced by broader economic sentiment, dictates the availability and pricing of funds for lenders like Velocity.

Inflation, Rates, and Credit: The 2024-2025 Economic Outlook

The economic landscape in late 2024 and early 2025 continues to be shaped by persistent inflation and the Federal Reserve's response through interest rates. While inflation showed signs of moderating from its 2023 peaks, it remained above the Fed's 2% target, leading to a sustained higher interest rate environment. This directly impacts Velocity Financial's cost of funds and the affordability of credit for its clients, particularly in the commercial real estate sector where higher rates are dampening transaction volumes and property valuations.

Small business health, a key market for Velocity, is closely tied to consumer spending and access to capital. Despite some resilience in employment, many small businesses in 2024 grappled with increased borrowing costs and the ongoing effects of inflation on their margins. This necessitates robust risk management and dynamic pricing strategies for Velocity to navigate potential credit deterioration.

Credit market liquidity, influenced by Federal Reserve policy and investor sentiment, remains a critical factor. While some segments, like the mortgage-backed securities market, showed stabilization in early 2024, overall credit availability is sensitive to rate decisions and economic outlook, directly affecting Velocity's lending capacity and competitive positioning throughout 2025.

| Economic Factor | Late 2024/Early 2025 Trend | Impact on Velocity Financial | Key Data Point (Illustrative) |

|---|---|---|---|

| Interest Rates | Elevated, Fed maintaining hawkish stance | Increased funding costs, potential slowdown in loan demand | Fed Funds Rate: 5.25%-5.50% (Late 2024) |

| Inflation | Moderating but above target | Erodes real value of fixed income, increases operational costs, may trigger higher rates | US CPI Inflation: ~3.5% (Annualized, Late 2024 projection) |

| Commercial Real Estate | Mixed signals, elevated office vacancies | Pressures property values, increases loan default risk, slows transaction volume | US Office Vacancy Rate: ~18-20% (Early 2024) |

| Small Business Health | Resilient but challenged by costs | Impacts revenue and debt servicing capabilities of clients | Small Business Lending Rate: ~7-9% (Prime + spread, Late 2024) |

| Credit Market Liquidity | Sensitive to Fed policy and economic outlook | Affects Velocity's ability to fund loans and overall lending capacity | LIBOR/SOFR: ~5.00%-5.50% (Late 2024) |

Preview Before You Purchase

Velocity PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This comprehensive Velocity PESTLE Analysis provides a deep dive into the external factors impacting your business, ensuring you have all the insights needed for strategic planning.