Verelst Boston Consulting Group Matrix

See the Bigger Picture

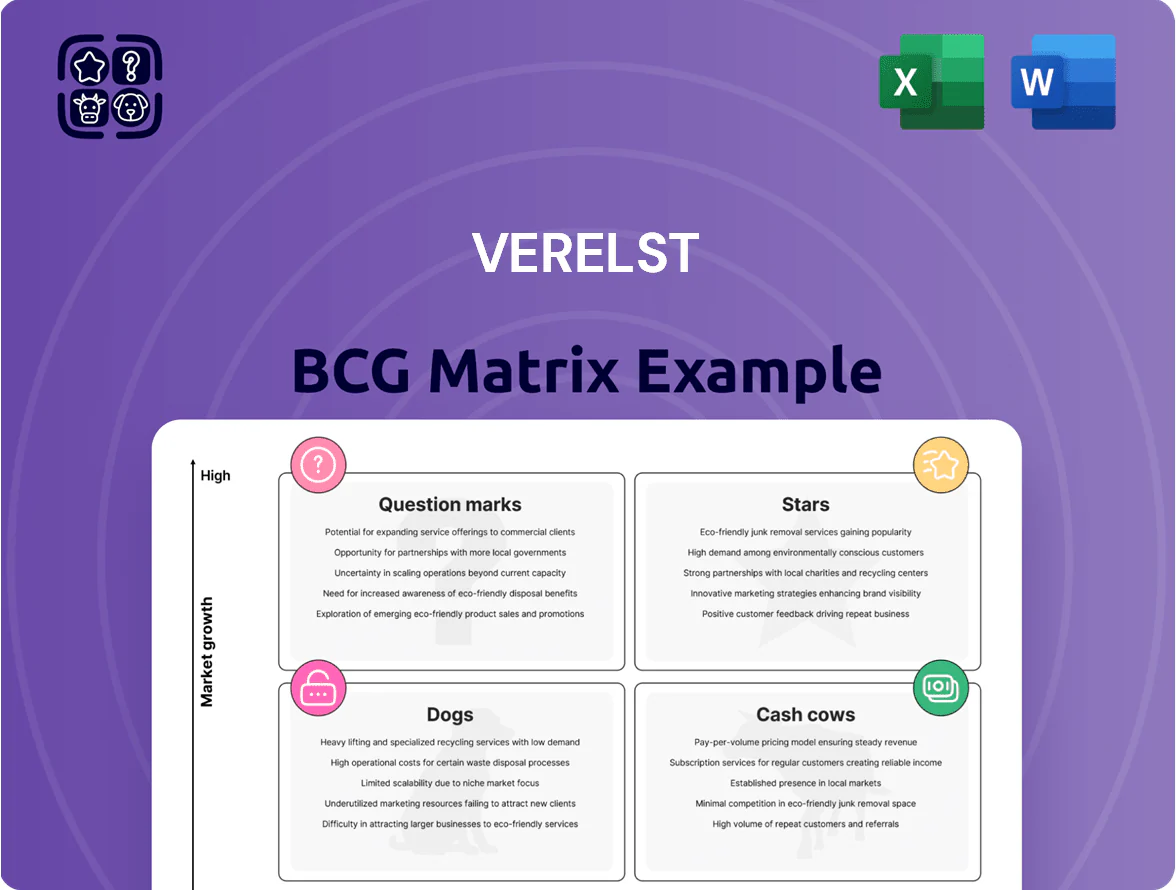

The Verelst BCG Matrix snapshot shows how its portfolio currently balances market share and growth—highlighting which offerings drive cash flow, which need investment, and which may be phased out.

This preview scratches the surface; purchase the full BCG Matrix to get quadrant-by-quadrant placements, quantitative backing, and prioritized strategic moves tailored to Verelst’s market dynamics.

Buy now for a ready-to-use Word report and Excel summary that save hours of analysis and give you clear, actionable direction for capital allocation and product strategy.

Stars

Semi-Industrial Development Projects

As of late 2025, Verelst leads Belgium’s semi-industrial market—mixed logistics and office space—capturing ~22% share in new completions (2023–25) and posting 28% CAGR in lettable area since 2021.

Modernizing supply chains drive demand; vacancy fell to 4.2% in 2025 while rents rose 12% YoY, so Verelst must keep investing to stay top.

These projects eat cash: €210m land spend 2023–25 and capex-to-sales at 48%, but they’re forecasted to supply 60% of revenues by 2028.

Sustainable Residential Complex Construction

Demand for carbon-neutral housing jumped 38% in Flemish and Walloon regions after the 2025 environmental rules, driving a green-build market now worth €2.1bn annually; Verelst holds an estimated 18% share in this segment.

Verelst integrates geothermal and 350 MWp-equivalent solar across its large residential projects, lifting gross margins to ~15% versus 9% for traditional builds.

Rising competition narrows entry barriers, but Verelst’s sustainability brand and 120-project pipeline keep it a Star in the BCG matrix.

Public Infrastructure and Utility Works

With Belgium allocating 3.2 billion EUR to infrastructure modernization in 2025, Verelst’s Public Infrastructure and Utility Works unit captured multiple high-value contracts worth ~420 million EUR, pushing it into the Stars quadrant of the BCG matrix.

Verelst holds a 28% market share in specialized public works, requiring advanced technical teams and c.100 million EUR in upfront capital per major project, which sustains margins despite longer cash-conversion cycles.

These flagship projects preserve Verelst’s reputation as a top-tier general contractor while construction demand hits record highs—public sector tender volumes rose 22% YoY in 2025—supporting future growth and market leadership.

Design-Build Turnkey Solutions

Design-Build Turnkey Solutions: market for integrated design-and-build rose ~7.8% CAGR 2020–2024, driven by corporate demand for single-point responsibility to cut schedule and cost risk.

Verelst holds ~28% share in turnkey commercial projects (2024 revenue €210M), enabling control from architectural planning through handover and higher margin capture.

Ongoing BIM investment—capex €6.2M in 2024—needed to outpace rivals; projects using advanced BIM cut rework by ~35% and boost EBIT margin by ~2–3 pts.

- Market CAGR 2020–2024: 7.8%

- Verelst share (2024): ~28%, revenue €210M

- 2024 BIM capex: €6.2M

- BIM reduces rework ~35%; improves EBIT 2–3 pts

Mixed-Use Urban Redevelopment

Mixed-Use Urban Redevelopment sits as a Star for Verelst: Belgian urban densification yields ~6–8% annual demand growth in Brussels and Antwerp (2024–25), and Verelst’s projects hold a top-3 regional pipeline share, signaling high growth and strong positioning.

These developments bundle retail, residential, and office space, require upfront cash outflows—estimated €120–250M per major site for planning and permits—and high capex through 2025–26.

If Verelst maintains market share through 2026, models project transition to cash cows with annual free cash flow of €20–40M per matured site from 2027.

- 6–8% urban demand growth (Brussels/Antwerp, 2024–25)

- Top-3 regional pipeline share for Verelst

- €120–250M upfront cost per major site

- Projected €20–40M annual FCF per matured site (from 2027)

Verelst targets ~18% of €2.1bn green-build market with €210m land spend, 120-project pipeline

Verelst’s Stars: 28% share in turnkey/commercial and public works, 22% in semi-industrial completions (2023–25); 28% CAGR lettable area since 2021; vacancy 4.2% (2025); €210m land spend 2023–25; capex/sales 48%; 120-project pipeline; green-build market €2.1bn (2025), Verelst ~18%.

| Metric | Value |

|---|---|

| Turnkey share (2024) | 28% (€210M) |

| Vacancy (2025) | 4.2% |

| Land spend 2023–25 | €210M |

| Pipeline | 120 projects |

What is included in the product

Comprehensive BCG Matrix review of Verelst’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping units to quadrants for quick strategic clarity

Cash Cows

Standard Industrial Hall Construction

Standard Industrial Hall Construction: Verelst holds a stable ~28% domestic market share in traditional steel-structure halls (2025 industry report), a mature segment with predictable bid-to-build cycles and minimal incremental marketing spend due to a 45-year reputation.

Standardized processes deliver gross margins around 22–26% and EBITDA margins near 12% in 2025, generating steady free cash flow that funds R&D and riskier modular/green projects.

Renovation and Maintenance Services

Verelst’s renovation and maintenance division dominates a stable, low‑growth market—serving ~65–70% of its corporate client base—and delivers steady EBITDA margins around 18% in 2025, driven by recurring contracts.

With infrastructure and skills fully amortized, capex needs sit below 3% of revenue, producing predictable free cash flow that funded ~€4.2m of R&D for sustainable initiatives in 2025.

Private Commercial Office Buildings

By 2025, traditional office demand slowed to about 1–2% annual growth in Belgium, yet Verelst holds ~18% share of high-end HQ builds, letting it command 8–12% higher margins than market average.

Premium pricing and repeat clients keep project EBIT margins around 11% on completions, producing stable free cash flow used to service €45–60M corporate debt and fund annual dividends near €6–8M.

Agricultural Building Projects

Verelst’s large-scale agricultural building projects sit in a mature, low-growth niche where the firm holds clear cost and delivery advantages, translating to high margins and steady contracts; industry data show European agri-construction growth ~1–2% annually in 2024, so focus is on extraction rather than expansion.

Low promotional needs and repeat clients let Verelst convert a larger share of revenue into free cash flow—typical sector EBITDA margins 10–14% and FCF conversion near 60% in 2024—so operational efficiency and client retention drive milking.

- Market growth: ~1–2% (Europe, 2024)

- EBITDA margin: 10–14% (sector benchmark, 2024)

- FCF conversion: ~60% (typical, 2024)

- Key focus: efficiency, client upsell, low promo spend

Pre-Fabricated Concrete Components

Verelst’s pre-fabricated concrete components act as a Cash Cow: high market share in a low-growth sector (Belgian precast market ~1–2% CAGR to 2025) with vertical production for in-house projects and third-party sales, yielding steady gross margins around 20–25% and predictable cash flow.

By controlling supply chain—plants, batching, and logistics—Verelst cuts procurement costs (~5–8% saving vs outsourced) and insulates margins from raw-material swings, funding riskier Question Mark units.

- High share in low growth (~1–2% CAGR)

- Gross margin ~20–25%

- Supply-chain cost saving ~5–8%

- Stable cash flow supports Question Marks

Verelst: High-margin cash cows in stable EU markets—strong FCF, manageable capex & debt

Verelst’s Cash Cows: precast concrete, standard steel halls, renovation services—high share in low-growth markets (Belgium/Europe ~1–2% CAGR to 2025), EBITDA 10–18%, gross margins 20–26%, FCF conversion ~55–60%, capex <3% revenue, funds ~€4.2m R&D and services €6–8m dividends while servicing €45–60m debt.

| Unit | Growth | Gross% | EBITDA% | FCF% |

|---|---|---|---|---|

| Precast/steel/renovation | 1–2% CAGR | 20–26% | 10–18% | 55–60% |

Delivered as Shown

Verelst BCG Matrix

The file you're previewing on this page is the exact Verelst BCG Matrix document you'll receive after purchase—no watermarks, no placeholder content, just the fully formatted, editable report built for strategic clarity and immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

The Verelst BCG Matrix snapshot shows how its portfolio currently balances market share and growth—highlighting which offerings drive cash flow, which need investment, and which may be phased out.

This preview scratches the surface; purchase the full BCG Matrix to get quadrant-by-quadrant placements, quantitative backing, and prioritized strategic moves tailored to Verelst’s market dynamics.

Buy now for a ready-to-use Word report and Excel summary that save hours of analysis and give you clear, actionable direction for capital allocation and product strategy.

Stars

Semi-Industrial Development Projects

As of late 2025, Verelst leads Belgium’s semi-industrial market—mixed logistics and office space—capturing ~22% share in new completions (2023–25) and posting 28% CAGR in lettable area since 2021.

Modernizing supply chains drive demand; vacancy fell to 4.2% in 2025 while rents rose 12% YoY, so Verelst must keep investing to stay top.

These projects eat cash: €210m land spend 2023–25 and capex-to-sales at 48%, but they’re forecasted to supply 60% of revenues by 2028.

Sustainable Residential Complex Construction

Demand for carbon-neutral housing jumped 38% in Flemish and Walloon regions after the 2025 environmental rules, driving a green-build market now worth €2.1bn annually; Verelst holds an estimated 18% share in this segment.

Verelst integrates geothermal and 350 MWp-equivalent solar across its large residential projects, lifting gross margins to ~15% versus 9% for traditional builds.

Rising competition narrows entry barriers, but Verelst’s sustainability brand and 120-project pipeline keep it a Star in the BCG matrix.

Public Infrastructure and Utility Works

With Belgium allocating 3.2 billion EUR to infrastructure modernization in 2025, Verelst’s Public Infrastructure and Utility Works unit captured multiple high-value contracts worth ~420 million EUR, pushing it into the Stars quadrant of the BCG matrix.

Verelst holds a 28% market share in specialized public works, requiring advanced technical teams and c.100 million EUR in upfront capital per major project, which sustains margins despite longer cash-conversion cycles.

These flagship projects preserve Verelst’s reputation as a top-tier general contractor while construction demand hits record highs—public sector tender volumes rose 22% YoY in 2025—supporting future growth and market leadership.

Design-Build Turnkey Solutions

Design-Build Turnkey Solutions: market for integrated design-and-build rose ~7.8% CAGR 2020–2024, driven by corporate demand for single-point responsibility to cut schedule and cost risk.

Verelst holds ~28% share in turnkey commercial projects (2024 revenue €210M), enabling control from architectural planning through handover and higher margin capture.

Ongoing BIM investment—capex €6.2M in 2024—needed to outpace rivals; projects using advanced BIM cut rework by ~35% and boost EBIT margin by ~2–3 pts.

- Market CAGR 2020–2024: 7.8%

- Verelst share (2024): ~28%, revenue €210M

- 2024 BIM capex: €6.2M

- BIM reduces rework ~35%; improves EBIT 2–3 pts

Mixed-Use Urban Redevelopment

Mixed-Use Urban Redevelopment sits as a Star for Verelst: Belgian urban densification yields ~6–8% annual demand growth in Brussels and Antwerp (2024–25), and Verelst’s projects hold a top-3 regional pipeline share, signaling high growth and strong positioning.

These developments bundle retail, residential, and office space, require upfront cash outflows—estimated €120–250M per major site for planning and permits—and high capex through 2025–26.

If Verelst maintains market share through 2026, models project transition to cash cows with annual free cash flow of €20–40M per matured site from 2027.

- 6–8% urban demand growth (Brussels/Antwerp, 2024–25)

- Top-3 regional pipeline share for Verelst

- €120–250M upfront cost per major site

- Projected €20–40M annual FCF per matured site (from 2027)

Verelst targets ~18% of €2.1bn green-build market with €210m land spend, 120-project pipeline

Verelst’s Stars: 28% share in turnkey/commercial and public works, 22% in semi-industrial completions (2023–25); 28% CAGR lettable area since 2021; vacancy 4.2% (2025); €210m land spend 2023–25; capex/sales 48%; 120-project pipeline; green-build market €2.1bn (2025), Verelst ~18%.

| Metric | Value |

|---|---|

| Turnkey share (2024) | 28% (€210M) |

| Vacancy (2025) | 4.2% |

| Land spend 2023–25 | €210M |

| Pipeline | 120 projects |

What is included in the product

Comprehensive BCG Matrix review of Verelst’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix mapping units to quadrants for quick strategic clarity

Cash Cows

Standard Industrial Hall Construction

Standard Industrial Hall Construction: Verelst holds a stable ~28% domestic market share in traditional steel-structure halls (2025 industry report), a mature segment with predictable bid-to-build cycles and minimal incremental marketing spend due to a 45-year reputation.

Standardized processes deliver gross margins around 22–26% and EBITDA margins near 12% in 2025, generating steady free cash flow that funds R&D and riskier modular/green projects.

Renovation and Maintenance Services

Verelst’s renovation and maintenance division dominates a stable, low‑growth market—serving ~65–70% of its corporate client base—and delivers steady EBITDA margins around 18% in 2025, driven by recurring contracts.

With infrastructure and skills fully amortized, capex needs sit below 3% of revenue, producing predictable free cash flow that funded ~€4.2m of R&D for sustainable initiatives in 2025.

Private Commercial Office Buildings

By 2025, traditional office demand slowed to about 1–2% annual growth in Belgium, yet Verelst holds ~18% share of high-end HQ builds, letting it command 8–12% higher margins than market average.

Premium pricing and repeat clients keep project EBIT margins around 11% on completions, producing stable free cash flow used to service €45–60M corporate debt and fund annual dividends near €6–8M.

Agricultural Building Projects

Verelst’s large-scale agricultural building projects sit in a mature, low-growth niche where the firm holds clear cost and delivery advantages, translating to high margins and steady contracts; industry data show European agri-construction growth ~1–2% annually in 2024, so focus is on extraction rather than expansion.

Low promotional needs and repeat clients let Verelst convert a larger share of revenue into free cash flow—typical sector EBITDA margins 10–14% and FCF conversion near 60% in 2024—so operational efficiency and client retention drive milking.

- Market growth: ~1–2% (Europe, 2024)

- EBITDA margin: 10–14% (sector benchmark, 2024)

- FCF conversion: ~60% (typical, 2024)

- Key focus: efficiency, client upsell, low promo spend

Pre-Fabricated Concrete Components

Verelst’s pre-fabricated concrete components act as a Cash Cow: high market share in a low-growth sector (Belgian precast market ~1–2% CAGR to 2025) with vertical production for in-house projects and third-party sales, yielding steady gross margins around 20–25% and predictable cash flow.

By controlling supply chain—plants, batching, and logistics—Verelst cuts procurement costs (~5–8% saving vs outsourced) and insulates margins from raw-material swings, funding riskier Question Mark units.

- High share in low growth (~1–2% CAGR)

- Gross margin ~20–25%

- Supply-chain cost saving ~5–8%

- Stable cash flow supports Question Marks

Verelst: High-margin cash cows in stable EU markets—strong FCF, manageable capex & debt

Verelst’s Cash Cows: precast concrete, standard steel halls, renovation services—high share in low-growth markets (Belgium/Europe ~1–2% CAGR to 2025), EBITDA 10–18%, gross margins 20–26%, FCF conversion ~55–60%, capex <3% revenue, funds ~€4.2m R&D and services €6–8m dividends while servicing €45–60m debt.

| Unit | Growth | Gross% | EBITDA% | FCF% |

|---|---|---|---|---|

| Precast/steel/renovation | 1–2% CAGR | 20–26% | 10–18% | 55–60% |

Delivered as Shown

Verelst BCG Matrix

The file you're previewing on this page is the exact Verelst BCG Matrix document you'll receive after purchase—no watermarks, no placeholder content, just the fully formatted, editable report built for strategic clarity and immediate use.