Verelst PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE Analysis of Verelst—spot how regulatory shifts, economic trends, and tech adoption reshape its prospects and where competitive opportunities lie; buy the full report to access the complete, actionable breakdown and ready-to-use slides for immediate implementation.

Political factors

Belgian federal and regional housing policies

The Belgian government offers subsidies and tax incentives—including a 6% VAT on major renovation in some regions vs 21% for new builds—boosting residential construction and influencing Verelst’s 2024–25 pipeline where housing starts rose 4.2% in 2024 to ~65,000 units; these measures directly affect project margins and cashflow timing.

Public infrastructure investment mandates

Government budgetary allocations for public works directly affect Verelst’s pipeline; EU member states increased infrastructure budgets to an average of 3.4% of GDP in 2025, boosting available tenders.

By late 2025 a political push for modernized public facilities and transport—backed by €48bn in national and EU grants—generated steady long-term contract opportunities for firms like Verelst.

Shifts toward austerity could cut project volumes by 12–20% annually, while expansionary fiscal policy scenarios in 2025–26 project 8–15% growth in high-value public contracts.

Geopolitical stability and supply chain security

Political tensions in Europe and globally have pushed steel futures up about 18% in 2024 and timber prices by ~12%, raising Verelst’s input costs for industrial and commercial projects.

Trade policy shifts and potential EU/UK tariffs risk disrupting procurement, increasing lead times that already average 14–20 weeks for key materials.

Verelst is responding with strategic stockpiling (targeting 3–6 months of critical inventory) and diversifying suppliers across Eastern Europe and Southeast Asia to mitigate supply-chain shocks.

Urban planning and zoning regulations

- Local density vs. green-space rules limit project locations

- Betonstop drives compact/vertical and brownfield focus; 12% brownfield transaction rise (2023)

- Average permitting >14 months, raising holding costs

European Union construction standards

EU directives on building safety, energy efficiency and public procurement shape Belgian construction rules; contractors face penalties and loss of tender eligibility if non-compliant.

Verelst must align with the Energy Performance of Buildings Directive (EPBD); EU targets aim for all new buildings nearly zero-energy by 2030 and member states report median renovation rates around 1% annually.

EU sustainability policies push Verelst toward low-carbon materials and smart-building tech, affecting capital expenditure and supply chains; green public contracts rose to 32% of tenders in some member states in 2024.

- Must comply with EPBD nearly zero-energy standard by 2030

- Renovation rates ~1%/yr across EU

- Green tenders ~32% in 2024

Policy-led pipeline boosts starts to ~65k amid rising costs, long permits and green shift

Political support for renovation (6% VAT) and expanded infrastructure budgets (3.4% of GDP in 2025) boosted Verelst’s 2024–25 pipeline—housing starts +4.2% to ~65,000 units—while austerity scenarios could cut volumes 12–20% vs expansion +8–15% in 2025–26; input costs rose (steel +18%, timber +12% in 2024) and permitting >14 months; green tenders ~32% (2024) and EPBD nearly-zero target by 2030 force capex shifts.

| Metric | Value |

|---|---|

| Housing starts 2024 | ~65,000 (+4.2%) |

| Infra budgets 2025 | 3.4% GDP (avg) |

| Steel/timber 2024 | +18% / +12% |

| Permitting | >14 months |

| Green tenders 2024 | ~32% |

What is included in the product

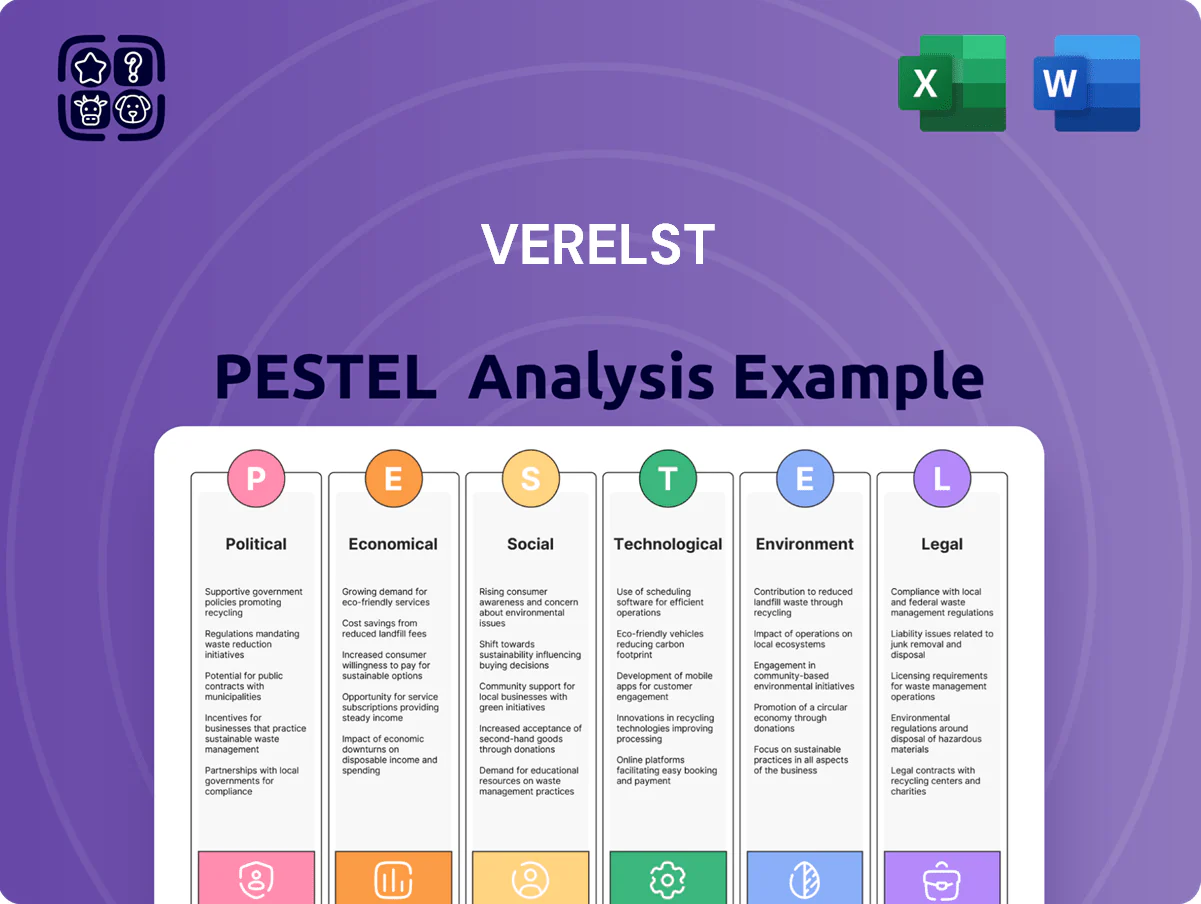

Explores how external macro-environmental factors uniquely affect the Verelst across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented Verelst PESTLE summary that can be dropped into presentations or shared across teams, enabling quick alignment on external risks and market positioning while allowing users to add context-specific notes for their region or business line.

Economic factors

Interest rate environment and financing costs

The ECB deposit rate rose to 4.00% in 2023–24 then eased to 3.25% by late 2025; this raised mortgage costs and pressured demand for Verelst’s residential projects, while pushing up industrial financing costs for expansions.

By 2025 mortgage rates in Belgium averaged ~3.8–4.5% depending on term, cooling new-build demand; easing rates toward 2026 improved affordability and investment appetite.

Verelst must optimize debt maturity, lock-in fixed-rate financing and use interest-rate hedges to control financing costs for large-scale developments.

Inflationary pressure on building materials

Fluctuations in energy, cement, steel and timber—steel up ~18% and cement up ~9% in EUQ4 2024 vs 2023—squeeze margins on fixed-price contracts for Verelst. The company uses indexation clauses and centralized procurement; group purchasing cut input cost volatility by ~6% in 2024. Eurozone inflation cooling to 2.4% in 2025 remains pivotal for accurate multi-year cost estimates.

Labor market shortages and wage indexation

Belgian construction faces a 20-25% shortfall in skilled technical labor, pushing Verelst to compete for talent and accept wage growth; construction wages rose about 6.2% y/y in 2024. Automatic wage indexation obliges regular payroll uplifts—Belgium's indexation added roughly 4–5% to labor costs in 2023–2024—eating into margins. Verelst must therefore scale internal training and invest in automation (robotics/ERP) to boost productivity and offset rising personnel expenses.

Commercial and industrial real estate demand

The Belgian corporate sector's health directly affects demand for offices and warehouses—Verelst's core markets; GDP grew 0.8% in 2024 Q3 year-on-year, supporting steady leasing activity.

Growth in e-commerce (Belgian online retail up ~9% in 2024) increases logistics-hub demand, while hybrid work trends trim traditional office absorption by an estimated 10–15% versus pre‑pandemic levels.

Verelst's diversified portfolio lets it reallocate capital between logistics and office assets to capture higher yields amid these shifts.

- Belgian GDP +0.8% (2024 Q3)

- E‑commerce +9% (2024)

- Office absorption down ~10–15%

- Portfolio diversification enables asset pivoting

Public sector debt and spending capacity

Belgium's public investment capacity depends on sovereign debt (~100.5% of GDP in 2024) and tax receipts; regions with constrained fiscal space may defer projects, reducing Verelst's public-sector backlog.

Recessions typically push non-essential works into postponement, while targeted stimulus—Belgium allocated €6.5bn in 2024–25 recovery/construction measures—can boost orders for contractors like Verelst.

- Belgian general government debt ~100.5% of GDP (2024)

- €6.5bn targeted recovery/construction measures (2024–25)

- Downturns risk postponement of non-essential public works, hurting order book

- Stimulus packages often prioritize construction to create jobs and upgrade infrastructure

Belgium 2024–25: Slower ECB, sticky costs, 0.8% GDP, €6.5bn stimulus

ECB rates peaked 4.00% (2023–24) easing to 3.25% by late‑2025, Belgian mortgages ~3.8–4.5% (2025); construction input prices rose steel +18%, cement +9% (EU Q4 2024), wages +6.2% y/y (2024); Belgian GDP +0.8% (2024 Q3), e‑commerce +9% (2024); sovereign debt ~100.5% of GDP (2024), €6.5bn stimulus (2024–25).

| Metric | Value |

|---|---|

| ECB rate | 3.25–4.00% |

| Mortgage | 3.8–4.5% |

| Steel / Cement | +18% / +9% |

| Wage growth | +6.2% |

| GDP (Q3 2024) | +0.8% |

| E‑commerce 2024 | +9% |

| Govt debt | ~100.5% GDP |

| Stimulus | €6.5bn |

What You See Is What You Get

Verelst PESTLE Analysis

The preview shown here is the exact Verelst PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and structure visible in this screenshot are the same document you’ll download immediately after payment, with no placeholders or surprises. Everything displayed is part of the final product, so you can proceed with confidence.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE Analysis of Verelst—spot how regulatory shifts, economic trends, and tech adoption reshape its prospects and where competitive opportunities lie; buy the full report to access the complete, actionable breakdown and ready-to-use slides for immediate implementation.

Political factors

Belgian federal and regional housing policies

The Belgian government offers subsidies and tax incentives—including a 6% VAT on major renovation in some regions vs 21% for new builds—boosting residential construction and influencing Verelst’s 2024–25 pipeline where housing starts rose 4.2% in 2024 to ~65,000 units; these measures directly affect project margins and cashflow timing.

Public infrastructure investment mandates

Government budgetary allocations for public works directly affect Verelst’s pipeline; EU member states increased infrastructure budgets to an average of 3.4% of GDP in 2025, boosting available tenders.

By late 2025 a political push for modernized public facilities and transport—backed by €48bn in national and EU grants—generated steady long-term contract opportunities for firms like Verelst.

Shifts toward austerity could cut project volumes by 12–20% annually, while expansionary fiscal policy scenarios in 2025–26 project 8–15% growth in high-value public contracts.

Geopolitical stability and supply chain security

Political tensions in Europe and globally have pushed steel futures up about 18% in 2024 and timber prices by ~12%, raising Verelst’s input costs for industrial and commercial projects.

Trade policy shifts and potential EU/UK tariffs risk disrupting procurement, increasing lead times that already average 14–20 weeks for key materials.

Verelst is responding with strategic stockpiling (targeting 3–6 months of critical inventory) and diversifying suppliers across Eastern Europe and Southeast Asia to mitigate supply-chain shocks.

Urban planning and zoning regulations

- Local density vs. green-space rules limit project locations

- Betonstop drives compact/vertical and brownfield focus; 12% brownfield transaction rise (2023)

- Average permitting >14 months, raising holding costs

European Union construction standards

EU directives on building safety, energy efficiency and public procurement shape Belgian construction rules; contractors face penalties and loss of tender eligibility if non-compliant.

Verelst must align with the Energy Performance of Buildings Directive (EPBD); EU targets aim for all new buildings nearly zero-energy by 2030 and member states report median renovation rates around 1% annually.

EU sustainability policies push Verelst toward low-carbon materials and smart-building tech, affecting capital expenditure and supply chains; green public contracts rose to 32% of tenders in some member states in 2024.

- Must comply with EPBD nearly zero-energy standard by 2030

- Renovation rates ~1%/yr across EU

- Green tenders ~32% in 2024

Policy-led pipeline boosts starts to ~65k amid rising costs, long permits and green shift

Political support for renovation (6% VAT) and expanded infrastructure budgets (3.4% of GDP in 2025) boosted Verelst’s 2024–25 pipeline—housing starts +4.2% to ~65,000 units—while austerity scenarios could cut volumes 12–20% vs expansion +8–15% in 2025–26; input costs rose (steel +18%, timber +12% in 2024) and permitting >14 months; green tenders ~32% (2024) and EPBD nearly-zero target by 2030 force capex shifts.

| Metric | Value |

|---|---|

| Housing starts 2024 | ~65,000 (+4.2%) |

| Infra budgets 2025 | 3.4% GDP (avg) |

| Steel/timber 2024 | +18% / +12% |

| Permitting | >14 months |

| Green tenders 2024 | ~32% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Verelst across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented Verelst PESTLE summary that can be dropped into presentations or shared across teams, enabling quick alignment on external risks and market positioning while allowing users to add context-specific notes for their region or business line.

Economic factors

Interest rate environment and financing costs

The ECB deposit rate rose to 4.00% in 2023–24 then eased to 3.25% by late 2025; this raised mortgage costs and pressured demand for Verelst’s residential projects, while pushing up industrial financing costs for expansions.

By 2025 mortgage rates in Belgium averaged ~3.8–4.5% depending on term, cooling new-build demand; easing rates toward 2026 improved affordability and investment appetite.

Verelst must optimize debt maturity, lock-in fixed-rate financing and use interest-rate hedges to control financing costs for large-scale developments.

Inflationary pressure on building materials

Fluctuations in energy, cement, steel and timber—steel up ~18% and cement up ~9% in EUQ4 2024 vs 2023—squeeze margins on fixed-price contracts for Verelst. The company uses indexation clauses and centralized procurement; group purchasing cut input cost volatility by ~6% in 2024. Eurozone inflation cooling to 2.4% in 2025 remains pivotal for accurate multi-year cost estimates.

Labor market shortages and wage indexation

Belgian construction faces a 20-25% shortfall in skilled technical labor, pushing Verelst to compete for talent and accept wage growth; construction wages rose about 6.2% y/y in 2024. Automatic wage indexation obliges regular payroll uplifts—Belgium's indexation added roughly 4–5% to labor costs in 2023–2024—eating into margins. Verelst must therefore scale internal training and invest in automation (robotics/ERP) to boost productivity and offset rising personnel expenses.

Commercial and industrial real estate demand

The Belgian corporate sector's health directly affects demand for offices and warehouses—Verelst's core markets; GDP grew 0.8% in 2024 Q3 year-on-year, supporting steady leasing activity.

Growth in e-commerce (Belgian online retail up ~9% in 2024) increases logistics-hub demand, while hybrid work trends trim traditional office absorption by an estimated 10–15% versus pre‑pandemic levels.

Verelst's diversified portfolio lets it reallocate capital between logistics and office assets to capture higher yields amid these shifts.

- Belgian GDP +0.8% (2024 Q3)

- E‑commerce +9% (2024)

- Office absorption down ~10–15%

- Portfolio diversification enables asset pivoting

Public sector debt and spending capacity

Belgium's public investment capacity depends on sovereign debt (~100.5% of GDP in 2024) and tax receipts; regions with constrained fiscal space may defer projects, reducing Verelst's public-sector backlog.

Recessions typically push non-essential works into postponement, while targeted stimulus—Belgium allocated €6.5bn in 2024–25 recovery/construction measures—can boost orders for contractors like Verelst.

- Belgian general government debt ~100.5% of GDP (2024)

- €6.5bn targeted recovery/construction measures (2024–25)

- Downturns risk postponement of non-essential public works, hurting order book

- Stimulus packages often prioritize construction to create jobs and upgrade infrastructure

Belgium 2024–25: Slower ECB, sticky costs, 0.8% GDP, €6.5bn stimulus

ECB rates peaked 4.00% (2023–24) easing to 3.25% by late‑2025, Belgian mortgages ~3.8–4.5% (2025); construction input prices rose steel +18%, cement +9% (EU Q4 2024), wages +6.2% y/y (2024); Belgian GDP +0.8% (2024 Q3), e‑commerce +9% (2024); sovereign debt ~100.5% of GDP (2024), €6.5bn stimulus (2024–25).

| Metric | Value |

|---|---|

| ECB rate | 3.25–4.00% |

| Mortgage | 3.8–4.5% |

| Steel / Cement | +18% / +9% |

| Wage growth | +6.2% |

| GDP (Q3 2024) | +0.8% |

| E‑commerce 2024 | +9% |

| Govt debt | ~100.5% GDP |

| Stimulus | €6.5bn |

What You See Is What You Get

Verelst PESTLE Analysis

The preview shown here is the exact Verelst PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The layout, content, and structure visible in this screenshot are the same document you’ll download immediately after payment, with no placeholders or surprises. Everything displayed is part of the final product, so you can proceed with confidence.