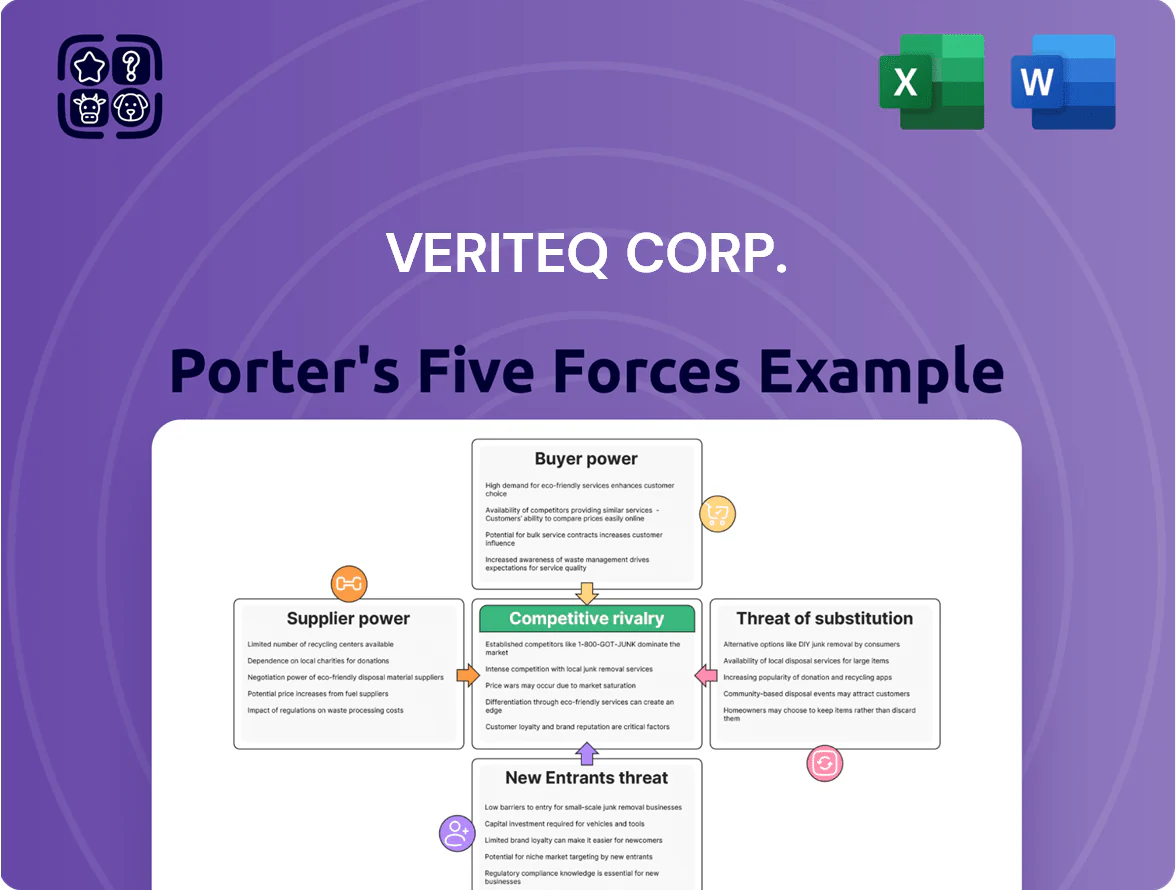

VeriTeQ Corp. Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

VeriTeQ faces moderate buyer power and growing substitute threats as remote monitoring and low-cost wearables expand, while suppliers hold limited leverage due to component commoditization; regulatory barriers and IP create a meaningful moat but also raise compliance costs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VeriTeQ Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Clinical Labor and Physician Talent

The supply of board-certified specialists and skilled nursing staff is highly constrained in 2025, with US physician vacancy rates near 7% and nursing shortages projecting 1.2 million RNs by 2026; demand for multi-specialty care is rising. Because Consensus Health is physician-owned and managed, individual clinicians wield strong leverage over pay and operational autonomy, pushing up compensation benchmarks by ~8–12% year-over-year. This supplier power forces VeriTeQ to spend aggressively on recruitment, sign-on bonuses, and retention—adding ~2–4% to operating costs. If providers are dissatisfied, attrition risk rises, with moves to larger hospital systems or private-equity-backed competitors already accounting for ~15% of departures in 2024.

Pharmaceutical and Biotechnology Manufacturers

Consensus Health depends on steady supplies of specialty meds and biologics; top pharma firms hold strong bargaining power via patents and limited substitutes, with the global biologics market at $344B in 2024 reinforcing supplier leverage. Price swings—some oncology drugs rose 12–18% in 2023—can squeeze margins if payer reimbursements lag. To counter this, Consensus joins group purchasing organizations, which can cut acquisition costs 5–15% and improve negotiating clout.

Electronic Medical Record and Health IT Providers

EMR and health IT vendors wield strong supplier power as advanced digital ecosystems grow; Gartner estimated 2024 global healthcare IT spend at $240B, concentrating buying with a few major EMR players. Switching costs are high—data migration and retraining can exceed $1M for mid-sized systems—so vendors lock clients into multi-year contracts. Subscription pricing and mandatory updates directly affect Consensus Health’s operating margins and capex planning, reducing vendor flexibility.

Medical Equipment and Device Vendors

High-end diagnostic and surgical kit like MRI and robotic systems are sold by a few global firms (GE Healthcare, Siemens Healthineers, Philips), letting them set prices and maintenance fees; MRI purchase cost ranges $1–3M and annual service can be 8–12% of purchase price (2024–25 data), raising supplier power.

Rapid tech change to 2026 forces frequent upgrades, keeping vendors in control and causing capital-intensive refresh cycles Consensus Health must fund to stay competitive.

- Concentrated suppliers: 3–4 majors dominate global market

- MRI capex $1–3M; service 8–12%/yr (2024–25)

- Upgrades every 5–7 years keeps vendor leverage

- Maintenance/contracts drive predictable Opex pressure

Professional Liability and Malpractice Insurers

The specialized nature of multi-specialty medical groups makes professional liability insurance essential and non-negotiable; only about 10–15 US carriers underwrite high-risk surgical portfolios as of 2025, concentrating supplier power.

These insurers can hike premiums 15–40% in volatile markets or litigious states (eg, Florida, Texas), directly cutting margins for practices and for VeriTeQ.

That dependency forces VeriTeQ to enforce strict risk-management protocols—credentialing, proctoring, and incident reporting—to hold renewal increases nearer to industry average (~8% in 2024).

- 10–15 carriers dominate high-risk coverage

- Premium swings: 15–40% by region/volatility

- VeriTeQ targets ~8% renewal rise via controls

- Strict protocols reduce insurer leverage

Supplier power soars: staffing, pharma, IT, imaging & malpractice drive costs up

Suppliers hold high power: clinician shortages (physician vacancy ~7% in 2025; RN gap ~1.2M by 2026) push wages +8–12% YoY, adding ~2–4% to VeriTeQ Opex; pharma/biologics market $344B (2024) and EMR concentration (2024 healthcare IT spend $240B) raise costs; MRI capex $1–3M, service 8–12%/yr; 10–15 carriers dominate high-risk malpractice, premiums swing 15–40%.

| Supplier | Key stat |

|---|---|

| Clinicians | Physician vacancy 7%; RN gap 1.2M |

| Pharma | Biologics market $344B (2024) |

| Health IT | IT spend $240B (2024) |

| Imaging | MRI $1–3M; svc 8–12%/yr |

| Malpractice | 10–15 carriers; premiums ±15–40% |

What is included in the product

Tailored Porter's Five Forces analysis for VeriTeQ Corp. uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive risks—supported by industry insights to inform strategic positioning, pricing leverage, and defensive barriers.

A concise Porter's Five Forces one-sheet for VeriTeQ that highlights competitive pressures and relief strategies—ideal for rapid decision-making and slide-ready presentation.

Customers Bargaining Power

Large Managed Care and Private Insurance Payers

In 2025 commercial insurers remain the dominant customer for Consensus Health, with the top five payers covering roughly 70% of US lives and setting reimbursement rates and medical-necessity rules that drive medical-group revenue.

National payer consolidation cut the number of contracting alternatives by over 40% since 2015, shrinking negotiating leverage for practices and compressing margins.

Loss of in-network status with a major insurer typically reduces practice patient volume by 25–45% and can trigger acute financial stress within 6–12 months.

Government Payers and Regulatory Agencies

Medicare and Medicaid cover ~38% of US hospital discharges in 2024 and will grow with aging through 2026, giving these payers absolute bargaining power via non-negotiable fee schedules and quality-based payment metrics.

VeriTeQ’s customer Consensus Health must follow federal rules to keep participation and avoid penalties; value-based care shifts let agencies demand better outcomes at lower cost, affecting reimbursement and contract terms.

Patient Consumerism and Digital Choice

Patients now act like consumers, using online reviews and price tools; 72% of US adults consulted online reviews for health decisions in 2023, raising individual bargaining power versus prior decades.

This ease of switching to competitors with better reputation or lower out-of-pocket costs forces VeriTeQ/Consensus Health to boost patient experience and brand management or face churn.

With 45% of covered workers in 2024 enrolled in high-deductible health plans, price sensitivity rises and patients increasingly shop for perceived value.

Corporate and Employer-Led Health Coalitions

This forces Consensus to demonstrate outcomes—reduced ER visits, HbA1c drops, or per-member-per-month (PMPM) savings—to justify discounted rates.

- Scale: employers control 5k–50k lives

- Price pressure: 10–30% discounts

- Expected ROI: 5–10% cost cut

- Value proof: ER visits, HbA1c, PMPM

Referral Networks and Primary Care Gatekeepers

Referral networks give primary care gatekeepers strong leverage over Consensus Health because they direct specialist and surgical volume; roughly 60% of specialty visits originate from PCP referrals in US multispecialty systems (2024 Medicare data).

If local practices are acquired by competing systems, Consensus could lose 15–30% of referral volume within 12–24 months, cutting revenue tied to procedures and diagnostics.

Maintaining tight professional ties, sharing 12‑month outcomes data (readmission rates, infection rates) and joint care pathways is vital to preserve referrals.

- ~60% specialty visits from PCPs (2024)

- Risk: 15–30% referral loss if PCPs acquired

- Counter: publish outcomes, build joint pathways

Buyers Dictate Terms: Top Payers & Employers Force Cuts, Outcomes, and Switching

Buyers—commercial insurers, Medicare/Medicaid, large employers, and price-sensitive patients—hold strong bargaining power, driving reimbursement cuts, outcomes-based terms, and switching; top five payers cover ~70% of US lives (2025) and employer coalitions demand 10–30% discounts. Loss of in-network status cuts volume 25–45%; Medicare/Medicaid account for ~38% of discharges (2024). VeriTeQ/Consensus must prove PMPM savings and clinical outcomes to retain contracts.

| Buyer | Key stat | Impact |

|---|---|---|

| Top 5 payers | ~70% US lives (2025) | Sets rates, high leverage |

| Medicare/Medicaid | ~38% discharges (2024) | Non-negotiable fees, mandates |

| Large employers | 5k–50k lives; 10–30% discounts | Demands ROI, price pressure |

| Patients | 45% HDHP; 72% use reviews | Higher switching, price sensitivity |

Same Document Delivered

VeriTeQ Corp. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of VeriTeQ Corp. you'll receive immediately after purchase—no surprises, no placeholders. It assesses supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with supporting data and implications for strategy. The document is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

VeriTeQ faces moderate buyer power and growing substitute threats as remote monitoring and low-cost wearables expand, while suppliers hold limited leverage due to component commoditization; regulatory barriers and IP create a meaningful moat but also raise compliance costs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VeriTeQ Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Clinical Labor and Physician Talent

The supply of board-certified specialists and skilled nursing staff is highly constrained in 2025, with US physician vacancy rates near 7% and nursing shortages projecting 1.2 million RNs by 2026; demand for multi-specialty care is rising. Because Consensus Health is physician-owned and managed, individual clinicians wield strong leverage over pay and operational autonomy, pushing up compensation benchmarks by ~8–12% year-over-year. This supplier power forces VeriTeQ to spend aggressively on recruitment, sign-on bonuses, and retention—adding ~2–4% to operating costs. If providers are dissatisfied, attrition risk rises, with moves to larger hospital systems or private-equity-backed competitors already accounting for ~15% of departures in 2024.

Pharmaceutical and Biotechnology Manufacturers

Consensus Health depends on steady supplies of specialty meds and biologics; top pharma firms hold strong bargaining power via patents and limited substitutes, with the global biologics market at $344B in 2024 reinforcing supplier leverage. Price swings—some oncology drugs rose 12–18% in 2023—can squeeze margins if payer reimbursements lag. To counter this, Consensus joins group purchasing organizations, which can cut acquisition costs 5–15% and improve negotiating clout.

Electronic Medical Record and Health IT Providers

EMR and health IT vendors wield strong supplier power as advanced digital ecosystems grow; Gartner estimated 2024 global healthcare IT spend at $240B, concentrating buying with a few major EMR players. Switching costs are high—data migration and retraining can exceed $1M for mid-sized systems—so vendors lock clients into multi-year contracts. Subscription pricing and mandatory updates directly affect Consensus Health’s operating margins and capex planning, reducing vendor flexibility.

Medical Equipment and Device Vendors

High-end diagnostic and surgical kit like MRI and robotic systems are sold by a few global firms (GE Healthcare, Siemens Healthineers, Philips), letting them set prices and maintenance fees; MRI purchase cost ranges $1–3M and annual service can be 8–12% of purchase price (2024–25 data), raising supplier power.

Rapid tech change to 2026 forces frequent upgrades, keeping vendors in control and causing capital-intensive refresh cycles Consensus Health must fund to stay competitive.

- Concentrated suppliers: 3–4 majors dominate global market

- MRI capex $1–3M; service 8–12%/yr (2024–25)

- Upgrades every 5–7 years keeps vendor leverage

- Maintenance/contracts drive predictable Opex pressure

Professional Liability and Malpractice Insurers

The specialized nature of multi-specialty medical groups makes professional liability insurance essential and non-negotiable; only about 10–15 US carriers underwrite high-risk surgical portfolios as of 2025, concentrating supplier power.

These insurers can hike premiums 15–40% in volatile markets or litigious states (eg, Florida, Texas), directly cutting margins for practices and for VeriTeQ.

That dependency forces VeriTeQ to enforce strict risk-management protocols—credentialing, proctoring, and incident reporting—to hold renewal increases nearer to industry average (~8% in 2024).

- 10–15 carriers dominate high-risk coverage

- Premium swings: 15–40% by region/volatility

- VeriTeQ targets ~8% renewal rise via controls

- Strict protocols reduce insurer leverage

Supplier power soars: staffing, pharma, IT, imaging & malpractice drive costs up

Suppliers hold high power: clinician shortages (physician vacancy ~7% in 2025; RN gap ~1.2M by 2026) push wages +8–12% YoY, adding ~2–4% to VeriTeQ Opex; pharma/biologics market $344B (2024) and EMR concentration (2024 healthcare IT spend $240B) raise costs; MRI capex $1–3M, service 8–12%/yr; 10–15 carriers dominate high-risk malpractice, premiums swing 15–40%.

| Supplier | Key stat |

|---|---|

| Clinicians | Physician vacancy 7%; RN gap 1.2M |

| Pharma | Biologics market $344B (2024) |

| Health IT | IT spend $240B (2024) |

| Imaging | MRI $1–3M; svc 8–12%/yr |

| Malpractice | 10–15 carriers; premiums ±15–40% |

What is included in the product

Tailored Porter's Five Forces analysis for VeriTeQ Corp. uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive risks—supported by industry insights to inform strategic positioning, pricing leverage, and defensive barriers.

A concise Porter's Five Forces one-sheet for VeriTeQ that highlights competitive pressures and relief strategies—ideal for rapid decision-making and slide-ready presentation.

Customers Bargaining Power

Large Managed Care and Private Insurance Payers

In 2025 commercial insurers remain the dominant customer for Consensus Health, with the top five payers covering roughly 70% of US lives and setting reimbursement rates and medical-necessity rules that drive medical-group revenue.

National payer consolidation cut the number of contracting alternatives by over 40% since 2015, shrinking negotiating leverage for practices and compressing margins.

Loss of in-network status with a major insurer typically reduces practice patient volume by 25–45% and can trigger acute financial stress within 6–12 months.

Government Payers and Regulatory Agencies

Medicare and Medicaid cover ~38% of US hospital discharges in 2024 and will grow with aging through 2026, giving these payers absolute bargaining power via non-negotiable fee schedules and quality-based payment metrics.

VeriTeQ’s customer Consensus Health must follow federal rules to keep participation and avoid penalties; value-based care shifts let agencies demand better outcomes at lower cost, affecting reimbursement and contract terms.

Patient Consumerism and Digital Choice

Patients now act like consumers, using online reviews and price tools; 72% of US adults consulted online reviews for health decisions in 2023, raising individual bargaining power versus prior decades.

This ease of switching to competitors with better reputation or lower out-of-pocket costs forces VeriTeQ/Consensus Health to boost patient experience and brand management or face churn.

With 45% of covered workers in 2024 enrolled in high-deductible health plans, price sensitivity rises and patients increasingly shop for perceived value.

Corporate and Employer-Led Health Coalitions

This forces Consensus to demonstrate outcomes—reduced ER visits, HbA1c drops, or per-member-per-month (PMPM) savings—to justify discounted rates.

- Scale: employers control 5k–50k lives

- Price pressure: 10–30% discounts

- Expected ROI: 5–10% cost cut

- Value proof: ER visits, HbA1c, PMPM

Referral Networks and Primary Care Gatekeepers

Referral networks give primary care gatekeepers strong leverage over Consensus Health because they direct specialist and surgical volume; roughly 60% of specialty visits originate from PCP referrals in US multispecialty systems (2024 Medicare data).

If local practices are acquired by competing systems, Consensus could lose 15–30% of referral volume within 12–24 months, cutting revenue tied to procedures and diagnostics.

Maintaining tight professional ties, sharing 12‑month outcomes data (readmission rates, infection rates) and joint care pathways is vital to preserve referrals.

- ~60% specialty visits from PCPs (2024)

- Risk: 15–30% referral loss if PCPs acquired

- Counter: publish outcomes, build joint pathways

Buyers Dictate Terms: Top Payers & Employers Force Cuts, Outcomes, and Switching

Buyers—commercial insurers, Medicare/Medicaid, large employers, and price-sensitive patients—hold strong bargaining power, driving reimbursement cuts, outcomes-based terms, and switching; top five payers cover ~70% of US lives (2025) and employer coalitions demand 10–30% discounts. Loss of in-network status cuts volume 25–45%; Medicare/Medicaid account for ~38% of discharges (2024). VeriTeQ/Consensus must prove PMPM savings and clinical outcomes to retain contracts.

| Buyer | Key stat | Impact |

|---|---|---|

| Top 5 payers | ~70% US lives (2025) | Sets rates, high leverage |

| Medicare/Medicaid | ~38% discharges (2024) | Non-negotiable fees, mandates |

| Large employers | 5k–50k lives; 10–30% discounts | Demands ROI, price pressure |

| Patients | 45% HDHP; 72% use reviews | Higher switching, price sensitivity |

Same Document Delivered

VeriTeQ Corp. Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of VeriTeQ Corp. you'll receive immediately after purchase—no surprises, no placeholders. It assesses supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with supporting data and implications for strategy. The document is fully formatted and ready for download and use the moment you buy. You're viewing the final deliverable.