Veritex Community Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

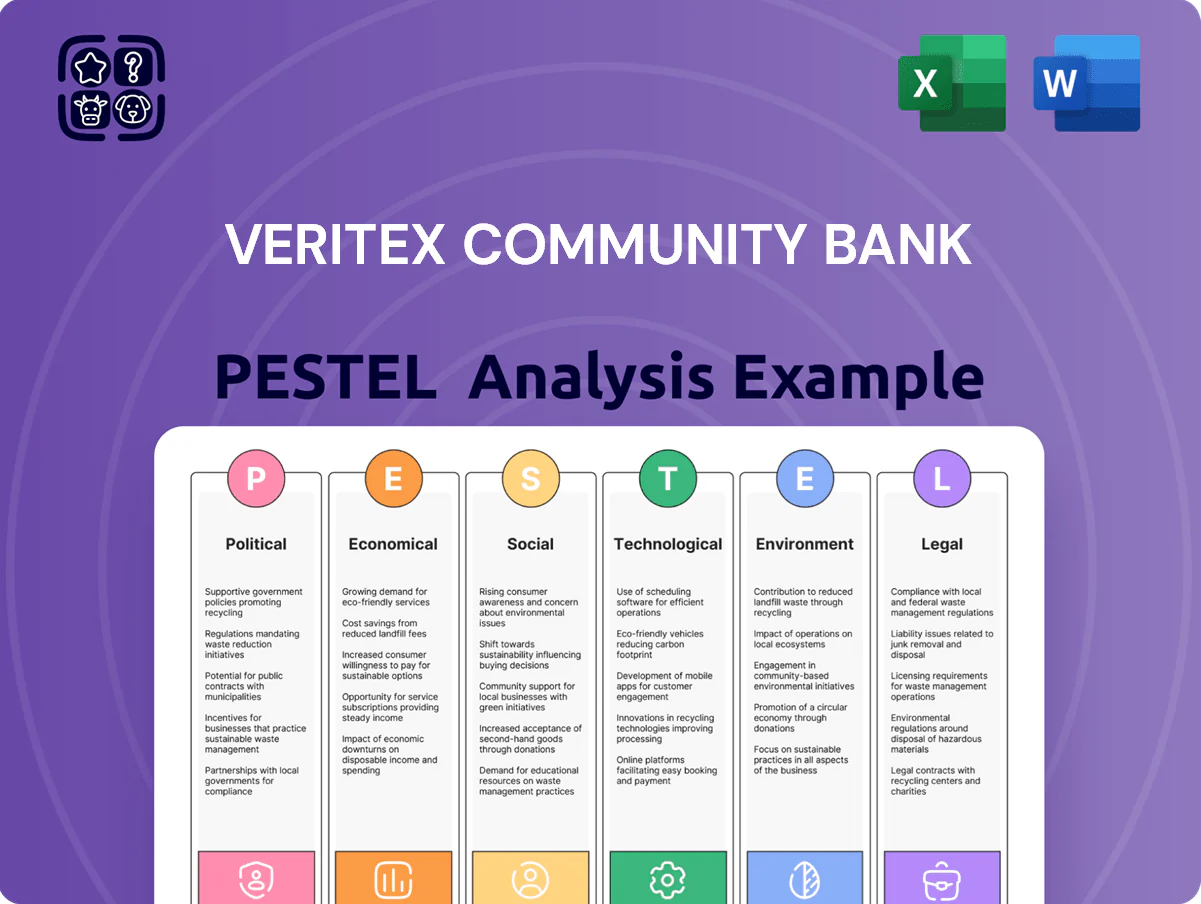

Gain a competitive edge with our PESTLE Analysis of Veritex Community Bank—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental factors shape strategy and risk. This concise, actionable report is perfect for investors, advisors, and executives seeking quick, evidence-based insights. Purchase the full analysis now for the complete, editable breakdown and strengthen your decisions instantly.

Political factors

Post-election regulatory landscape

Post-election regulatory shifts after the 2024 U.S. presidential result have driven federal policy toward banking deregulation by late 2025, including proposals to ease Dodd-Frank capital and stress-test requirements; for Veritex this could cut compliance costs—CET1 capital buffer relief and lower reporting burdens—freeing capital for lending as Veritex reported $14.8bn assets (2024) and could redeploy a portion of reduced compliance expenses into community loan growth.

Texas state fiscal policy

The Texas pro-business stance—no state income tax and $10.8 billion in 2024 corporate incentives—boosts inbound firms and HNW individuals, expanding Veritex Community Bank’s Dallas–Fort Worth and Houston deposit and lending bases.

Net migration added ~1.1 million residents to Texas in 2020–2023, supporting commercial real estate demand and underwriting for Veritex’s CRE portfolio.

State-level political stability yields predictable regulatory and tax outlooks, reducing credit-risk volatility for Veritex’s long-term business and commercial real estate loans.

Geopolitical influence on local energy

Political tensions in major energy regions — notably the Middle East and Russia — have pushed Brent and WTI price volatility; WTI averaged 77.3 USD/bbl in 2024, reinforcing Texas production policy shifts that affect Veritex's local markets.

Veritex, with concentrated Texas exposure, must track federal mandates such as 2024 EPA rules and DOI leasing changes that impact its oil and gas clients and collateral valuations.

U.S. moves toward energy independence and the 2024 surge in shale output (U.S. crude production ~13.3 mbpd) can compress margins, raising probability of credit deterioration in Veritex’s energy portfolio.

Federal Reserve independence and pressure

By late 2025 political debate over Federal Reserve independence has intensified, shifting market-implied odds for rate cuts/ hikes; fed funds futures implied a 40% chance of a cut by Dec 2025 and a 20% chance of hikes, altering yield curve expectations that affect bank funding costs.

Veritex must balance pressure for lower rates to spur lending against inflation control, as a 25–75 bps swing in short-term rates can compress or expand net interest margin (NIM) materially given the bank's sensitivity to repricing.

These dynamics directly influence loan pricing and deposit spreads: Veritex's NIM reported 3.45% in 2024 and could move +/-20–30 bps under differing Fed scenarios, impacting net interest income and loan origination strategy.

- Fed futures: ~40% cut probability by Dec 2025

- Veritex NIM 2024: 3.45%

- Potential NIM swing: +/-20–30 bps from rate shifts

Infrastructure and housing initiatives

Federal and state emphasis on affordable housing and infrastructure—highlighted by the 2024 $65 billion CHIPS+ and 2025 state housing bonds—creates targeted lending opportunities for Veritex Community Bank to grow mortgage and construction loan portfolios.

Leveraging FHA, USDA, and HUD programs plus public-private partnerships can boost originations while helping meet CRA obligations; in 2024 community banks saw a 12% YoY rise in construction lending.

- Aligns with government-backed programs (FHA/USDA/HUD)

- Opportunity to expand mortgage/construction loans amid 12% sector growth

- Supports CRA compliance through community-focused lending

Veritex: Deregulation, Texas growth boost balance sheet as energy and Fed risks pressure NIM

Post-2024 deregulatory proposals could lower Veritex compliance costs, freeing capital against $14.8bn assets (2024); Texas population growth (~+1.1M, 2020–23) and pro-business policy expand deposit/lending bases; energy price volatility (WTI avg $77.3/bbl, 2024) and US crude ~13.3 mbpd raise energy credit risk; Fed cut odds (~40% Dec 2025) threaten NIM (3.45% in 2024; ±20–30bps).

| Metric | Value |

|---|---|

| Total assets (2024) | $14.8bn |

| Veritex NIM (2024) | 3.45% |

| WTI (2024 avg) | $77.3/bbl |

| US crude prod (2024) | ~13.3 mbpd |

| TX net migration (2020–23) | ~1.1M |

| Fed cut odds (Dec 2025) | ~40% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Veritex Community Bank, with data-backed trends and region-specific examples to reveal risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Veritex Community Bank that streamlines external risk discussion, is easily dropped into presentations or strategy packs, and editable for regional or business-line notes to speed alignment across teams.

Economic factors

Texas-specific economic resilience

Texas GDP grew 3.8% in 2024 and job creation averaged 2.9% y/y through Q3 2025, outpacing the U.S. (≈1.8% GDP, 1.5% jobs); Veritex’s Texas-focused footprint positions it to capture deposits and commercial lending from corporate migration to the Silicon Prairie and Texas Medical Center, where employment expanded ~4% in 2024, bolstering loan demand and providing localized resilience that supports asset quality and keeps nonperforming loans below peer averages.

Interest rate cycle stabilization

Commercial real estate market correction

The commercial real estate market correction, driven by a 20-30% office valuation decline nationally and about 25% in major Texas metros through 2024, continues to pressure bank balance sheets; Veritex’s Texas-heavy loan book sees differentiated risk as multi-family fundamentals remain stronger with <5% vacancy while traditional office vacancies exceed 20% in Dallas and Houston. Veritex’s Q4 2024 allowance for credit losses and non-performing assets management will be pivotal to sustain CET1 ratios above regulatory minima.

Inflationary impact on operational costs

Persistent but moderating U.S. inflation (3.4% YoY Jan 2025) has raised Veritex’s talent and operating costs, with Texas private-sector wage growth near 4.0% in 2024 pressuring compensation for relationship managers.

Higher overhead risks widening Veritex’s reported efficiency ratio (peer median ~58% in 2024); careful wage management and productivity gains are required to protect 2025 net interest margin and ROA targets.

- Inflation: 3.4% YoY (Jan 2025)

- Texas wage growth: ~4.0% (2024)

- Peer efficiency ratio: ~58% (2024)

Small business credit demand

Entrepreneurial activity in Texas remains robust, with 2024 new business formations up ~5.2% year-over-year, supporting higher demand for SBA loans and commercial lines of credit that benefit Veritex’s SMB focus.

Veritex’s SMB specialization enables personalized lending solutions and cross-sell; SMB loans comprised roughly 38% of commercial loan growth in 2024 for regional banks.

To avoid elevated losses in a maturing cycle, Veritex must keep disciplined underwriting—maintain coverage ratios and limit concentration risk as delinquencies ticked slightly higher to ~1.2% in late 2024.

- Texas new business formations +5.2% (2024)

- SMB lending ~38% of regional commercial loan growth (2024)

- Delinquencies ~1.2% (late 2024) — underwrite tightly

Texas: Strong growth, tight labor, CRE pressure — funding stable, deposit beta risk

Texas GDP +3.8% (2024); job growth 2.9% y/y through Q3 2025 fuels deposit and loan demand; federal funds ~5.25% (late 2025) stabilizes funding costs but deposit beta risk remains 40–60bp per 100bp; CRE office valuations down ~25% in Texas, multifamily vacancy <5% supporting asset quality; inflation 3.4% (Jan 2025) and Texas wage growth ~4.0% press operating costs.

| Metric | Value |

|---|---|

| Texas GDP (2024) | +3.8% |

| Job growth (through Q3 2025) | +2.9% y/y |

| Fed funds (late 2025) | ~5.25% |

| Deposit beta | 40–60bp per 100bp |

| Texas office valuations change | ≈-25% |

| Multifamily vacancy (TX) | <5% |

| Inflation (Jan 2025) | 3.4% YoY |

| Texas wage growth (2024) | ~4.0% |

What You See Is What You Get

Veritex Community Bank PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Veritex Community Bank you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Veritex Community Bank—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental factors shape strategy and risk. This concise, actionable report is perfect for investors, advisors, and executives seeking quick, evidence-based insights. Purchase the full analysis now for the complete, editable breakdown and strengthen your decisions instantly.

Political factors

Post-election regulatory landscape

Post-election regulatory shifts after the 2024 U.S. presidential result have driven federal policy toward banking deregulation by late 2025, including proposals to ease Dodd-Frank capital and stress-test requirements; for Veritex this could cut compliance costs—CET1 capital buffer relief and lower reporting burdens—freeing capital for lending as Veritex reported $14.8bn assets (2024) and could redeploy a portion of reduced compliance expenses into community loan growth.

Texas state fiscal policy

The Texas pro-business stance—no state income tax and $10.8 billion in 2024 corporate incentives—boosts inbound firms and HNW individuals, expanding Veritex Community Bank’s Dallas–Fort Worth and Houston deposit and lending bases.

Net migration added ~1.1 million residents to Texas in 2020–2023, supporting commercial real estate demand and underwriting for Veritex’s CRE portfolio.

State-level political stability yields predictable regulatory and tax outlooks, reducing credit-risk volatility for Veritex’s long-term business and commercial real estate loans.

Geopolitical influence on local energy

Political tensions in major energy regions — notably the Middle East and Russia — have pushed Brent and WTI price volatility; WTI averaged 77.3 USD/bbl in 2024, reinforcing Texas production policy shifts that affect Veritex's local markets.

Veritex, with concentrated Texas exposure, must track federal mandates such as 2024 EPA rules and DOI leasing changes that impact its oil and gas clients and collateral valuations.

U.S. moves toward energy independence and the 2024 surge in shale output (U.S. crude production ~13.3 mbpd) can compress margins, raising probability of credit deterioration in Veritex’s energy portfolio.

Federal Reserve independence and pressure

By late 2025 political debate over Federal Reserve independence has intensified, shifting market-implied odds for rate cuts/ hikes; fed funds futures implied a 40% chance of a cut by Dec 2025 and a 20% chance of hikes, altering yield curve expectations that affect bank funding costs.

Veritex must balance pressure for lower rates to spur lending against inflation control, as a 25–75 bps swing in short-term rates can compress or expand net interest margin (NIM) materially given the bank's sensitivity to repricing.

These dynamics directly influence loan pricing and deposit spreads: Veritex's NIM reported 3.45% in 2024 and could move +/-20–30 bps under differing Fed scenarios, impacting net interest income and loan origination strategy.

- Fed futures: ~40% cut probability by Dec 2025

- Veritex NIM 2024: 3.45%

- Potential NIM swing: +/-20–30 bps from rate shifts

Infrastructure and housing initiatives

Federal and state emphasis on affordable housing and infrastructure—highlighted by the 2024 $65 billion CHIPS+ and 2025 state housing bonds—creates targeted lending opportunities for Veritex Community Bank to grow mortgage and construction loan portfolios.

Leveraging FHA, USDA, and HUD programs plus public-private partnerships can boost originations while helping meet CRA obligations; in 2024 community banks saw a 12% YoY rise in construction lending.

- Aligns with government-backed programs (FHA/USDA/HUD)

- Opportunity to expand mortgage/construction loans amid 12% sector growth

- Supports CRA compliance through community-focused lending

Veritex: Deregulation, Texas growth boost balance sheet as energy and Fed risks pressure NIM

Post-2024 deregulatory proposals could lower Veritex compliance costs, freeing capital against $14.8bn assets (2024); Texas population growth (~+1.1M, 2020–23) and pro-business policy expand deposit/lending bases; energy price volatility (WTI avg $77.3/bbl, 2024) and US crude ~13.3 mbpd raise energy credit risk; Fed cut odds (~40% Dec 2025) threaten NIM (3.45% in 2024; ±20–30bps).

| Metric | Value |

|---|---|

| Total assets (2024) | $14.8bn |

| Veritex NIM (2024) | 3.45% |

| WTI (2024 avg) | $77.3/bbl |

| US crude prod (2024) | ~13.3 mbpd |

| TX net migration (2020–23) | ~1.1M |

| Fed cut odds (Dec 2025) | ~40% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Veritex Community Bank, with data-backed trends and region-specific examples to reveal risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Veritex Community Bank that streamlines external risk discussion, is easily dropped into presentations or strategy packs, and editable for regional or business-line notes to speed alignment across teams.

Economic factors

Texas-specific economic resilience

Texas GDP grew 3.8% in 2024 and job creation averaged 2.9% y/y through Q3 2025, outpacing the U.S. (≈1.8% GDP, 1.5% jobs); Veritex’s Texas-focused footprint positions it to capture deposits and commercial lending from corporate migration to the Silicon Prairie and Texas Medical Center, where employment expanded ~4% in 2024, bolstering loan demand and providing localized resilience that supports asset quality and keeps nonperforming loans below peer averages.

Interest rate cycle stabilization

Commercial real estate market correction

The commercial real estate market correction, driven by a 20-30% office valuation decline nationally and about 25% in major Texas metros through 2024, continues to pressure bank balance sheets; Veritex’s Texas-heavy loan book sees differentiated risk as multi-family fundamentals remain stronger with <5% vacancy while traditional office vacancies exceed 20% in Dallas and Houston. Veritex’s Q4 2024 allowance for credit losses and non-performing assets management will be pivotal to sustain CET1 ratios above regulatory minima.

Inflationary impact on operational costs

Persistent but moderating U.S. inflation (3.4% YoY Jan 2025) has raised Veritex’s talent and operating costs, with Texas private-sector wage growth near 4.0% in 2024 pressuring compensation for relationship managers.

Higher overhead risks widening Veritex’s reported efficiency ratio (peer median ~58% in 2024); careful wage management and productivity gains are required to protect 2025 net interest margin and ROA targets.

- Inflation: 3.4% YoY (Jan 2025)

- Texas wage growth: ~4.0% (2024)

- Peer efficiency ratio: ~58% (2024)

Small business credit demand

Entrepreneurial activity in Texas remains robust, with 2024 new business formations up ~5.2% year-over-year, supporting higher demand for SBA loans and commercial lines of credit that benefit Veritex’s SMB focus.

Veritex’s SMB specialization enables personalized lending solutions and cross-sell; SMB loans comprised roughly 38% of commercial loan growth in 2024 for regional banks.

To avoid elevated losses in a maturing cycle, Veritex must keep disciplined underwriting—maintain coverage ratios and limit concentration risk as delinquencies ticked slightly higher to ~1.2% in late 2024.

- Texas new business formations +5.2% (2024)

- SMB lending ~38% of regional commercial loan growth (2024)

- Delinquencies ~1.2% (late 2024) — underwrite tightly

Texas: Strong growth, tight labor, CRE pressure — funding stable, deposit beta risk

Texas GDP +3.8% (2024); job growth 2.9% y/y through Q3 2025 fuels deposit and loan demand; federal funds ~5.25% (late 2025) stabilizes funding costs but deposit beta risk remains 40–60bp per 100bp; CRE office valuations down ~25% in Texas, multifamily vacancy <5% supporting asset quality; inflation 3.4% (Jan 2025) and Texas wage growth ~4.0% press operating costs.

| Metric | Value |

|---|---|

| Texas GDP (2024) | +3.8% |

| Job growth (through Q3 2025) | +2.9% y/y |

| Fed funds (late 2025) | ~5.25% |

| Deposit beta | 40–60bp per 100bp |

| Texas office valuations change | ≈-25% |

| Multifamily vacancy (TX) | <5% |

| Inflation (Jan 2025) | 3.4% YoY |

| Texas wage growth (2024) | ~4.0% |

What You See Is What You Get

Veritex Community Bank PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Veritex Community Bank you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.