Veritone Porter's Five Forces Analysis

From Overview to Strategy Blueprint

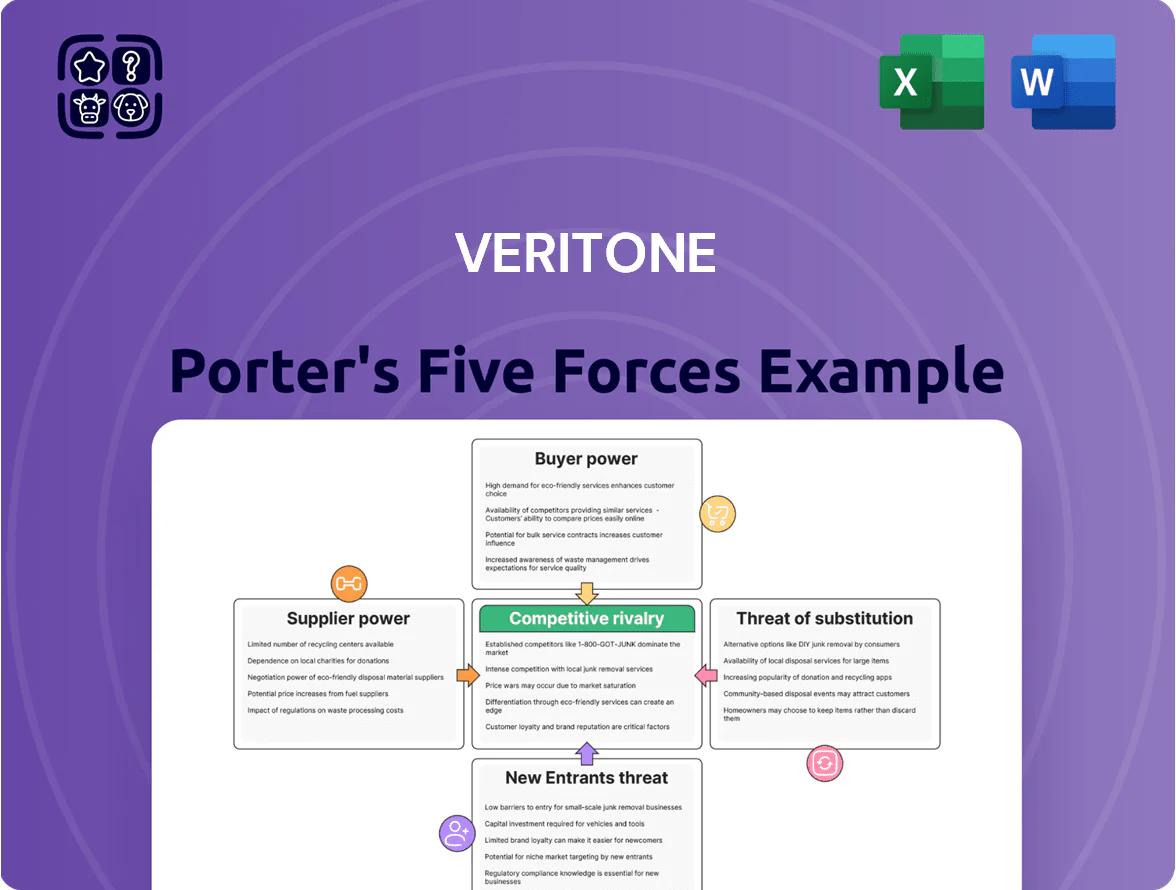

Veritone faces moderate rivalry from specialized AI firms and cloud incumbents, while supplier leverage is mitigated by scalable cloud infrastructure and diverse data partnerships; customer bargaining varies across enterprise and media segments, and the threat of entrants is tempered by AI IP and regulatory hurdles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Veritone’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hyperscale Cloud Infrastructure

Veritone depends on AWS and Microsoft Azure to host its aiWARE platform, giving those hyperscalers strong supplier power because moving clouds is technically hard and can cause weeks of downtime; by end-2025 AWS and Azure held roughly 60% of global cloud IaaS/PaaS market share, keeping pricing power high for GPU/TPU compute needed for AI, where spot and instance costs rose ~15–30% YoY in 2024–2025, squeezing Veritone’s margins.

Access to Third-Party Cognitive Engines

The aiWARE ecosystem integrates 300+ third-party AI models and cognitive engines, giving Veritone wide analytical coverage but making it dependent on external partners.

Veritone’s own models help, yet the platform’s value hinges on keeping positive developer ties; loss of key engines would cut features and hurt customer retention.

If major providers raise licensing by 20–40% or consolidate—like recent M&A trends in 2024—Veritone could see margin pressure and slower product roadmap delivery.

Scarcity of Specialized AI Engineering Talent

Through 2025 the market for senior ML engineers and data scientists stayed intense: US median salary for ML engineers hit about $160,000 in 2024 and top hires command >$250,000 plus equity, so labor suppliers hold strong bargaining power on pay and remote/flexible terms. Veritone must keep investing in hiring, training, and retention—R&D spend was $53.6M in FY2024—otherwise larger tech rivals with deeper pockets will outpace its aiOS innovation.

Reliance on Specialized Hardware Manufacturers

The processing of unstructured data at scale demands high-performance GPUs and AI chips made mainly by Nvidia, AMD, and Taiwan Semiconductor Manufacturing Company (TSMC); Nvidia held ~80% of the discrete AI GPU market in 2024. Supply chain shocks or US-China tensions raised GPU prices ~20–30% in 2022–24, raising Veritone’s cloud costs and capacity risk. That concentration lets suppliers limit allocations or hike prices, creating a clear bottleneck.

- Key suppliers: Nvidia, AMD, TSMC

- Nvidia ~80% AI GPU share (2024)

- GPU price swings ~20–30% (2022–24)

- Supply limits → allocation risk, higher cloud costs

Data Acquisition and Licensing Sources

Veritone depends on vast, industry-specific datasets to train AI models, and owners of media archives and public records can demand steep licensing fees, raising supplier power.

With stricter 2025 data privacy rules, compliant data sourcing costs rose—industry estimates show a 12–18% increase in acquisition and legal compliance expenses for AI vendors in 2024–25.

Higher fees and limited exclusivity deals force Veritone to pay more or seek synthetic/partnership alternatives, compressing margins unless offset by higher output prices or efficiency gains.

- Data owners: high pricing leverage

- 2024–25 compliance cost rise: ~12–18%

- Media/public records critical, scarce

- Synthetic data and partnerships as mitigants

Suppliers (AWS/Nvidia/talent/data) Squeeze Veritone: Rising costs, scarce capacity

Suppliers (hyperscalers, GPU makers, data owners, talent) hold strong bargaining power vs Veritone: AWS/Azure ~60% IaaS/PaaS (end-2025), Nvidia ~80% AI GPU share (2024), ML median pay ~$160k (2024), compliance costs +12–18% (2024–25); price/availability shocks and license fees squeeze margins and risk feature loss.

| Supplier | Key metric | Impact |

|---|---|---|

| Hyperscalers | AWS/Azure ~60% (end-2025) | Pricing power, migration risk |

| GPUs | Nvidia ~80% (2024) | Allocation, price volatility |

| Talent | ML median $160k (2024) | Higher R&D cost |

| Data owners | Compliance +12–18% (2024–25) | Licensing cost rise |

What is included in the product

Tailored exclusively for Veritone, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, potential new-entrant and substitute threats, and strategic barriers that shape its market positioning and profitability.

Instantly visualize Veritone's competitive pressures with a concise Porter's Five Forces one-sheet—easy to drop into decks, tweak force levels for scenario analysis, and share with nontechnical stakeholders.

Customers Bargaining Power

Concentration of Large Enterprise and Government Clients

A significant share of Veritone’s revenue comes from large government, legal, and media contracts—about 35% of FY2024 revenue per the 2024 10-K—so these customers can demand custom integrations and volume discounts that compress margins. Large clients’ bargaining power forces longer sales cycles and tailored SLAs, increasing implementation costs and pricing pressure. Losing one major agency or media conglomerate (each can represent 5–12% of revenue) would materially hurt cash flow and growth forecasts.

Moderate Switching Costs for aiWARE Users

Once clients integrate Veritone aiWARE into workflows, migration costs—retraining, API rewrites, and data transfer—can exceed $200k for enterprise deployments, creating technical lock-in that reduces churn in data-critical sectors like legal and law enforcement where chain-of-custody matters.

That lock-in gives Veritone moderate customer power, but by 2025 rising standards such as OpenAI API common formats and interoperable model hubs are lowering switching costs, modestly increasing buyer mobility.

Availability of Alternative Niche AI Solutions

Customers can choose many niche AI tools focused on specific tasks instead of a full platform; a 2024 McKinsey survey found 58% of firms used at least one specialized AI point solution. If a buyer needs only narrow features, point solutions can be 30–60% cheaper upfront than integrated suites, pushing Veritone to prove higher lifetime ROI. Veritone must show its ecosystem boosts productivity and reduces total cost of ownership to stop customers unbundling AI spend.

Price Sensitivity in the Media and Entertainment Sector

The media and entertainment sector, a core market for Veritone, is highly price sensitive as 2024 industry reports show media tech procurement budgets fell about 6% year-over-year, pushing buyers toward cost-effective AI solutions.

Buyers run competitive RFPs and price benchmarking—large broadcasters cut vendor lists by 30%—so Veritone must match aggressive pricing while protecting margins amid rising R&D and cloud costs.

- 2024: media tech budgets down ~6%

- Broadcasters trimming vendors ~30%

- Pressure: lower prices vs. higher R&D/cloud spend

High Information Transparency and Market Knowledge

In 2025, buyers access benchmarking datasets showing AI model accuracy and pricing spreads—industry reports cite median model performance variance of ±6% and SaaS price per API call ranging $0.001–$0.03, letting customers precisely compare Veritone versus rivals.

That visibility strengthens negotiation: procurement teams push for tighter SLAs and transparent tiered pricing; 48% of enterprise buyers (2024 survey) demand usage-based billing over flat fees.

- Median model variance ±6%

- API price range $0.001–$0.03

- 48% prefer usage billing

Concentrated Clients Boost Bargaining Power, Lower Margins as Switching Costs Fall

Large government, legal, and media clients (≈35% of FY2024 revenue) exert strong bargaining power—demanding custom SLAs, longer sales cycles, and volume discounts that compress margins; losing one major client (5–12% revenue) would be material. Technical lock-in (enterprise migration >$200k) reduces churn, but rising interoperable standards and point solutions (58% firms use niche AI; media tech budgets down ~6% in 2024) lower switching costs and increase buyer leverage.

| Metric | Value |

|---|---|

| FY2024 revenue from large clients | ≈35% |

| Major client revenue share | 5–12% |

| Enterprise migration cost | >$200,000 |

| Firms using niche AI (2024) | 58% |

| Media tech budgets YoY (2024) | −6% |

Same Document Delivered

Veritone Porter's Five Forces Analysis

This preview shows the exact Veritone Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Veritone faces moderate rivalry from specialized AI firms and cloud incumbents, while supplier leverage is mitigated by scalable cloud infrastructure and diverse data partnerships; customer bargaining varies across enterprise and media segments, and the threat of entrants is tempered by AI IP and regulatory hurdles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Veritone’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Hyperscale Cloud Infrastructure

Veritone depends on AWS and Microsoft Azure to host its aiWARE platform, giving those hyperscalers strong supplier power because moving clouds is technically hard and can cause weeks of downtime; by end-2025 AWS and Azure held roughly 60% of global cloud IaaS/PaaS market share, keeping pricing power high for GPU/TPU compute needed for AI, where spot and instance costs rose ~15–30% YoY in 2024–2025, squeezing Veritone’s margins.

Access to Third-Party Cognitive Engines

The aiWARE ecosystem integrates 300+ third-party AI models and cognitive engines, giving Veritone wide analytical coverage but making it dependent on external partners.

Veritone’s own models help, yet the platform’s value hinges on keeping positive developer ties; loss of key engines would cut features and hurt customer retention.

If major providers raise licensing by 20–40% or consolidate—like recent M&A trends in 2024—Veritone could see margin pressure and slower product roadmap delivery.

Scarcity of Specialized AI Engineering Talent

Through 2025 the market for senior ML engineers and data scientists stayed intense: US median salary for ML engineers hit about $160,000 in 2024 and top hires command >$250,000 plus equity, so labor suppliers hold strong bargaining power on pay and remote/flexible terms. Veritone must keep investing in hiring, training, and retention—R&D spend was $53.6M in FY2024—otherwise larger tech rivals with deeper pockets will outpace its aiOS innovation.

Reliance on Specialized Hardware Manufacturers

The processing of unstructured data at scale demands high-performance GPUs and AI chips made mainly by Nvidia, AMD, and Taiwan Semiconductor Manufacturing Company (TSMC); Nvidia held ~80% of the discrete AI GPU market in 2024. Supply chain shocks or US-China tensions raised GPU prices ~20–30% in 2022–24, raising Veritone’s cloud costs and capacity risk. That concentration lets suppliers limit allocations or hike prices, creating a clear bottleneck.

- Key suppliers: Nvidia, AMD, TSMC

- Nvidia ~80% AI GPU share (2024)

- GPU price swings ~20–30% (2022–24)

- Supply limits → allocation risk, higher cloud costs

Data Acquisition and Licensing Sources

Veritone depends on vast, industry-specific datasets to train AI models, and owners of media archives and public records can demand steep licensing fees, raising supplier power.

With stricter 2025 data privacy rules, compliant data sourcing costs rose—industry estimates show a 12–18% increase in acquisition and legal compliance expenses for AI vendors in 2024–25.

Higher fees and limited exclusivity deals force Veritone to pay more or seek synthetic/partnership alternatives, compressing margins unless offset by higher output prices or efficiency gains.

- Data owners: high pricing leverage

- 2024–25 compliance cost rise: ~12–18%

- Media/public records critical, scarce

- Synthetic data and partnerships as mitigants

Suppliers (AWS/Nvidia/talent/data) Squeeze Veritone: Rising costs, scarce capacity

Suppliers (hyperscalers, GPU makers, data owners, talent) hold strong bargaining power vs Veritone: AWS/Azure ~60% IaaS/PaaS (end-2025), Nvidia ~80% AI GPU share (2024), ML median pay ~$160k (2024), compliance costs +12–18% (2024–25); price/availability shocks and license fees squeeze margins and risk feature loss.

| Supplier | Key metric | Impact |

|---|---|---|

| Hyperscalers | AWS/Azure ~60% (end-2025) | Pricing power, migration risk |

| GPUs | Nvidia ~80% (2024) | Allocation, price volatility |

| Talent | ML median $160k (2024) | Higher R&D cost |

| Data owners | Compliance +12–18% (2024–25) | Licensing cost rise |

What is included in the product

Tailored exclusively for Veritone, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, potential new-entrant and substitute threats, and strategic barriers that shape its market positioning and profitability.

Instantly visualize Veritone's competitive pressures with a concise Porter's Five Forces one-sheet—easy to drop into decks, tweak force levels for scenario analysis, and share with nontechnical stakeholders.

Customers Bargaining Power

Concentration of Large Enterprise and Government Clients

A significant share of Veritone’s revenue comes from large government, legal, and media contracts—about 35% of FY2024 revenue per the 2024 10-K—so these customers can demand custom integrations and volume discounts that compress margins. Large clients’ bargaining power forces longer sales cycles and tailored SLAs, increasing implementation costs and pricing pressure. Losing one major agency or media conglomerate (each can represent 5–12% of revenue) would materially hurt cash flow and growth forecasts.

Moderate Switching Costs for aiWARE Users

Once clients integrate Veritone aiWARE into workflows, migration costs—retraining, API rewrites, and data transfer—can exceed $200k for enterprise deployments, creating technical lock-in that reduces churn in data-critical sectors like legal and law enforcement where chain-of-custody matters.

That lock-in gives Veritone moderate customer power, but by 2025 rising standards such as OpenAI API common formats and interoperable model hubs are lowering switching costs, modestly increasing buyer mobility.

Availability of Alternative Niche AI Solutions

Customers can choose many niche AI tools focused on specific tasks instead of a full platform; a 2024 McKinsey survey found 58% of firms used at least one specialized AI point solution. If a buyer needs only narrow features, point solutions can be 30–60% cheaper upfront than integrated suites, pushing Veritone to prove higher lifetime ROI. Veritone must show its ecosystem boosts productivity and reduces total cost of ownership to stop customers unbundling AI spend.

Price Sensitivity in the Media and Entertainment Sector

The media and entertainment sector, a core market for Veritone, is highly price sensitive as 2024 industry reports show media tech procurement budgets fell about 6% year-over-year, pushing buyers toward cost-effective AI solutions.

Buyers run competitive RFPs and price benchmarking—large broadcasters cut vendor lists by 30%—so Veritone must match aggressive pricing while protecting margins amid rising R&D and cloud costs.

- 2024: media tech budgets down ~6%

- Broadcasters trimming vendors ~30%

- Pressure: lower prices vs. higher R&D/cloud spend

High Information Transparency and Market Knowledge

In 2025, buyers access benchmarking datasets showing AI model accuracy and pricing spreads—industry reports cite median model performance variance of ±6% and SaaS price per API call ranging $0.001–$0.03, letting customers precisely compare Veritone versus rivals.

That visibility strengthens negotiation: procurement teams push for tighter SLAs and transparent tiered pricing; 48% of enterprise buyers (2024 survey) demand usage-based billing over flat fees.

- Median model variance ±6%

- API price range $0.001–$0.03

- 48% prefer usage billing

Concentrated Clients Boost Bargaining Power, Lower Margins as Switching Costs Fall

Large government, legal, and media clients (≈35% of FY2024 revenue) exert strong bargaining power—demanding custom SLAs, longer sales cycles, and volume discounts that compress margins; losing one major client (5–12% revenue) would be material. Technical lock-in (enterprise migration >$200k) reduces churn, but rising interoperable standards and point solutions (58% firms use niche AI; media tech budgets down ~6% in 2024) lower switching costs and increase buyer leverage.

| Metric | Value |

|---|---|

| FY2024 revenue from large clients | ≈35% |

| Major client revenue share | 5–12% |

| Enterprise migration cost | >$200,000 |

| Firms using niche AI (2024) | 58% |

| Media tech budgets YoY (2024) | −6% |

Same Document Delivered

Veritone Porter's Five Forces Analysis

This preview shows the exact Veritone Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.