Verizon Communications PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

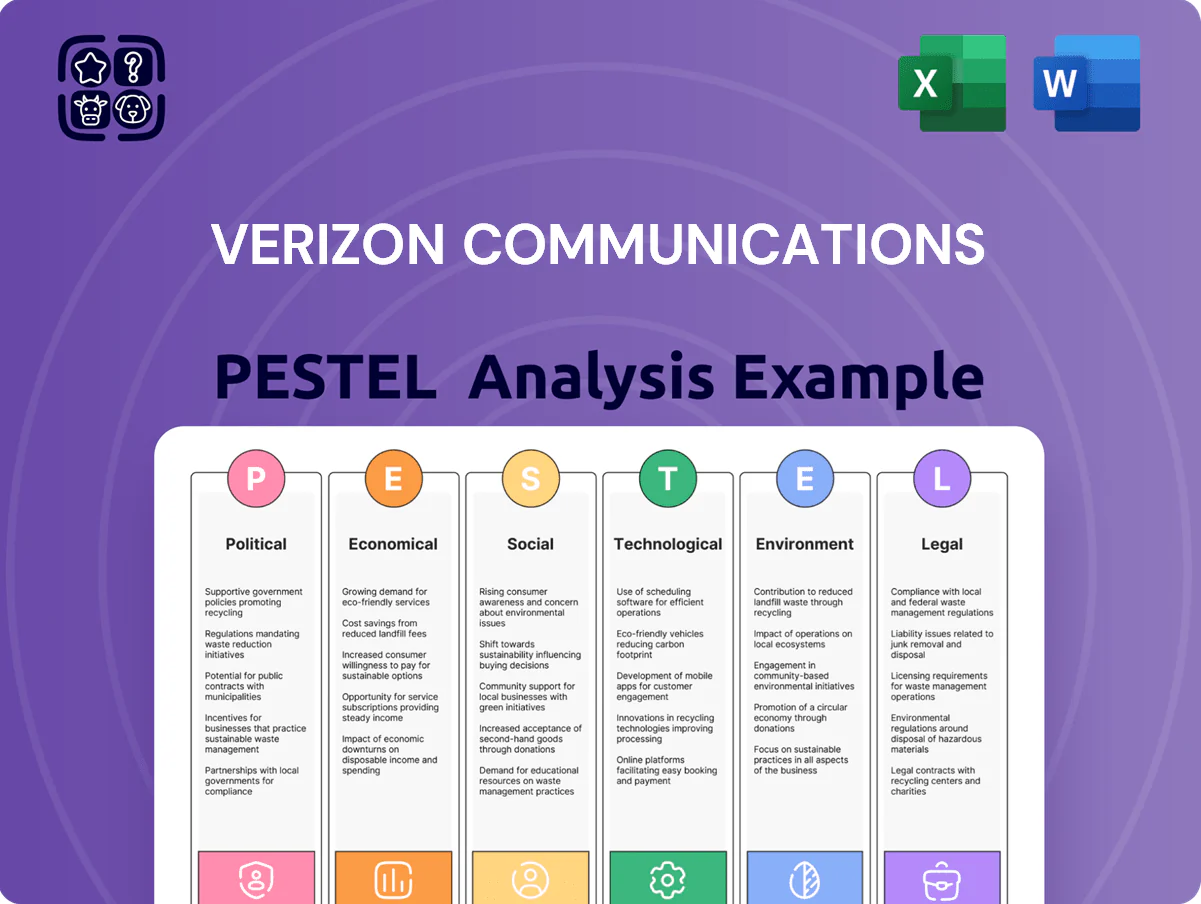

Explore how regulatory shifts, economic cycles, and rapid tech innovation are reshaping Verizon Communications’ competitive landscape—our concise PESTLE highlights key risks and opportunities to inform smarter decisions.

Political factors

FCC Spectrum Allocation Policies

The Federal Communications Commission controls spectrum availability and pricing; Verizon spent about $45.5 billion on spectrum auctions from 2017–2021 and continues to bid heavily to sustain 5G capacity and market position.

Federal Infrastructure Funding and Subsidies

The BEAD program allocates about $42.45 billion nationwide; securing these funds is critical as Verizon competes for grants to extend fiber and fixed wireless into underserved areas, affecting its rural rollout pace.

Meeting federal grant requirements—service milestones, reporting, and matching funds—shapes Verizon’s project timelines and capital allocation, with successful captures improving capex efficiency per subscriber.

Geopolitical Trade Restrictions on Hardware

Ongoing U.S.-China tech tensions—including 2024 export controls that affected suppliers responsible for roughly 30% of global 5G radio equipment—risk disrupting Verizon’s supply chain for critical networking hardware. Political mandates banning certain foreign-made components force Verizon to diversify vendors, raising procurement costs; analysts estimate supplier-switching could add 3–6% to capex. These dynamics require continuous monitoring to ensure network security and compliance with U.S. national security directives.

Net Neutrality and Regulatory Oversight

Shifts in Washington on net neutrality affect how Verizon manages traffic; a 2023 FCC rollback of strict rules and ongoing state-level actions create uncertainty for ISP business models.

Stricter enforcement could curb Verizon’s ability to sell tiered or prioritized services, potentially impacting revenue from Verizon Consumer and Business segments (2024 revenue: $133.6B consolidated).

Verizon invests in lobbying—spending $20.6M in 2023—and maintains legal teams to adapt to changing regulation.

- Regulatory uncertainty: federal vs. state rules

- Potential cap on tiered/prioritized services

- 2023 lobbying spend $20.6M

- 2024 consolidated revenue $133.6B

Cybersecurity and National Security Mandates

The U.S. treats telecom as critical infrastructure, driving mandates that force carriers like Verizon to meet stricter cybersecurity and reporting rules; FCC and CISA guidance increased incident reporting, with the sector seeing a 20% rise in reported breaches in 2024, raising regulatory scrutiny.

Meeting mandates requires heavy CAPEX and OPEX: Verizon disclosed roughly $2.2 billion in network security and infrastructure investments in 2024, and ongoing coordination with federal agencies (DHS, NSA) for threat intel sharing is mandatory.

- 20% rise in sector breach reports in 2024

- Verizon security/infrastructure spend ≈ $2.2B in 2024

- Mandatory incident reporting to FCC/CISA and interagency coordination

Verizon: $45.5B spectrum, BEAD $42.45B, rising capex & compliance costs reshape 5G

Federal spectrum auctions cost Verizon ~$45.5B (2017–2021) and ongoing bids sustain 5G capacity; BEAD grants (~$42.45B nationwide) affect rural rollout timing and grant competition. U.S.-China export controls raised supplier-switch costs (~3–6% capex), while net neutrality shifts and stricter cybersecurity rules (20% rise in breach reports 2024) drive compliance spend (~$2.2B in 2024); lobbying was $20.6M (2023).

| Metric | Value |

|---|---|

| Spectrum spend (2017–21) | $45.5B |

| BEAD program (nat.) | $42.45B |

| Supply-switch capex impact | +3–6% |

| Breach reports rise (2024) | +20% |

| Security spend (2024) | $2.2B |

| Lobbying (2023) | $20.6M |

What is included in the product

Explores how macro-environmental factors uniquely affect Verizon Communications across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists on threats, opportunities, and scenario planning.

A concise, PESTLE-organized summary of Verizon Communications that’s presentation-ready and easily shareable, enabling quick alignment across teams and supporting risk and market-position discussions during planning sessions.

Economic factors

Interest Rate Volatility and Debt Management

Verizon carried about $116 billion of long-term debt at end-2024; interest rate swings in 2025 materially affect refinancing costs for spectrum and 5G capex, with Fed policy pushing benchmark yields up ~80 bps in H1 2025 increasing interest expense projections.

Higher rates compress valuation multiples and raise weighted average cost of capital, forcing stricter capital allocation between network investment, M&A and shareholder returns.

Persistent rate strength could constrain Verizon’s ability to sustain its $2.61 annual dividend per share (2024 payout) without cutting investments or borrowing more expensively.

Inflationary Pressure on Operating Costs

Persistent U.S. inflation — CPI running near 3.4% in 2024 vs 6.5% in 2022 — raises Verizon’s labor, materials and energy costs for its 5G fiber network; Verizon reported network opex rising 4.8% y/y in 2024, pressuring margins.

Rising unit costs force Verizon to weigh price increases against competitive pressure from T-Mobile and Dish; postpaid ARPU grew 2.1% y/y in 2024, limiting room for large hikes.

Verizon’s ability to pass costs through without spiking churn (churn ~0.82% postpaid in 2024) is a key economic risk impacting EBITDA and capex funding.

5G Monetization and Return on Investment

After years of heavy 5G capex—Verizon spent about $39.6 billion on network investment in 2019–2023—economic focus now targets sustainable ROI from that infrastructure.

Verizon is monetizing through private 5G for enterprises and advanced IoT; its Verizon Business segment revenue rose 8% in 2024, reflecting early traction.

The long-term success depends on enterprise adoption rates of premium services; industry forecasts expect private 5G market to reach $17–20 billion in the US by 2028, shaping Verizon’s revenue upside.

Consumer Purchasing Power and Economic Cycles

The demand for premium plans and flagship devices is cyclical and tied to U.S. GDP and consumer confidence; in 2023 U.S. real GDP grew 2.5% and consumer confidence averaged 101, supporting higher ARPU, but a 2024 Q3 slowdown saw device upgrade rates fall ~6% YoY, pressuring Verizon’s equipment revenue (~$24.5B in 2023). Monitoring indicators like CPI, unemployment (3.9% in 2024) lets Verizon tailor promotions and prepaid offerings to protect margins.

- Premium plan demand correlates with GDP and consumer confidence

- Device upgrades fell ~6% YoY in 2024 Q3, impacting equipment revenue

- Verizon equipment revenue ~$24.5B in 2023; ARPU sensitive to macro swings

- Monitor CPI, unemployment (3.9% 2024) to adjust bundles and promotions

Labor Market Dynamics and Talent Retention

The telecom sector needs skilled engineers to manage 5G, edge computing and software-defined networks; Verizon reported 133,400 employees in 2024 and spent $1.9 billion on employee benefits in 2023, reflecting high labor costs.

Intense competition for technical talent pushes wages up—median tech salaries rose ~6% in 2024—forcing Verizon to increase training and retention investments to protect service quality and innovation.

Labor market shifts, including lower unemployment in tech hubs, risk operational efficiency and could delay network upgrades if talent shortages persist.

- Verizon workforce 2024: 133,400; benefits expense 2023: $1.9B

- Tech median salaries up ~6% in 2024, raising hiring costs

- Training/retention spend critical to support 5G and software-defined transitions

Rising Rates Strain Verizon: $116B Debt, Tight FCF & Dividend Pressure

Rising rates (Fed-driven ~+80bps H1 2025) lift Verizon’s interest costs on ~$116B debt, pressuring free cash flow and dividend sustainability; network opex rose 4.8% y/y in 2024 while postpaid ARPU grew 2.1% and churn ~0.82%, limiting pricing power; Verizon Business revenue +8% in 2024 supports 5G monetization while device revenue weakness (equipment ~$24.5B in 2023) ties to GDP/consumer confidence.

| Metric | Value |

|---|---|

| Long-term debt | $116B (2024) |

| Network opex growth | +4.8% (2024) |

| Postpaid ARPU | +2.1% (2024) |

| Churn | 0.82% (2024) |

| Verizon Business rev | +8% (2024) |

Preview Before You Purchase

Verizon Communications PESTLE Analysis

The preview shown here is the exact Verizon Communications PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, economic cycles, and rapid tech innovation are reshaping Verizon Communications’ competitive landscape—our concise PESTLE highlights key risks and opportunities to inform smarter decisions.

Political factors

FCC Spectrum Allocation Policies

The Federal Communications Commission controls spectrum availability and pricing; Verizon spent about $45.5 billion on spectrum auctions from 2017–2021 and continues to bid heavily to sustain 5G capacity and market position.

Federal Infrastructure Funding and Subsidies

The BEAD program allocates about $42.45 billion nationwide; securing these funds is critical as Verizon competes for grants to extend fiber and fixed wireless into underserved areas, affecting its rural rollout pace.

Meeting federal grant requirements—service milestones, reporting, and matching funds—shapes Verizon’s project timelines and capital allocation, with successful captures improving capex efficiency per subscriber.

Geopolitical Trade Restrictions on Hardware

Ongoing U.S.-China tech tensions—including 2024 export controls that affected suppliers responsible for roughly 30% of global 5G radio equipment—risk disrupting Verizon’s supply chain for critical networking hardware. Political mandates banning certain foreign-made components force Verizon to diversify vendors, raising procurement costs; analysts estimate supplier-switching could add 3–6% to capex. These dynamics require continuous monitoring to ensure network security and compliance with U.S. national security directives.

Net Neutrality and Regulatory Oversight

Shifts in Washington on net neutrality affect how Verizon manages traffic; a 2023 FCC rollback of strict rules and ongoing state-level actions create uncertainty for ISP business models.

Stricter enforcement could curb Verizon’s ability to sell tiered or prioritized services, potentially impacting revenue from Verizon Consumer and Business segments (2024 revenue: $133.6B consolidated).

Verizon invests in lobbying—spending $20.6M in 2023—and maintains legal teams to adapt to changing regulation.

- Regulatory uncertainty: federal vs. state rules

- Potential cap on tiered/prioritized services

- 2023 lobbying spend $20.6M

- 2024 consolidated revenue $133.6B

Cybersecurity and National Security Mandates

The U.S. treats telecom as critical infrastructure, driving mandates that force carriers like Verizon to meet stricter cybersecurity and reporting rules; FCC and CISA guidance increased incident reporting, with the sector seeing a 20% rise in reported breaches in 2024, raising regulatory scrutiny.

Meeting mandates requires heavy CAPEX and OPEX: Verizon disclosed roughly $2.2 billion in network security and infrastructure investments in 2024, and ongoing coordination with federal agencies (DHS, NSA) for threat intel sharing is mandatory.

- 20% rise in sector breach reports in 2024

- Verizon security/infrastructure spend ≈ $2.2B in 2024

- Mandatory incident reporting to FCC/CISA and interagency coordination

Verizon: $45.5B spectrum, BEAD $42.45B, rising capex & compliance costs reshape 5G

Federal spectrum auctions cost Verizon ~$45.5B (2017–2021) and ongoing bids sustain 5G capacity; BEAD grants (~$42.45B nationwide) affect rural rollout timing and grant competition. U.S.-China export controls raised supplier-switch costs (~3–6% capex), while net neutrality shifts and stricter cybersecurity rules (20% rise in breach reports 2024) drive compliance spend (~$2.2B in 2024); lobbying was $20.6M (2023).

| Metric | Value |

|---|---|

| Spectrum spend (2017–21) | $45.5B |

| BEAD program (nat.) | $42.45B |

| Supply-switch capex impact | +3–6% |

| Breach reports rise (2024) | +20% |

| Security spend (2024) | $2.2B |

| Lobbying (2023) | $20.6M |

What is included in the product

Explores how macro-environmental factors uniquely affect Verizon Communications across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, investors, and strategists on threats, opportunities, and scenario planning.

A concise, PESTLE-organized summary of Verizon Communications that’s presentation-ready and easily shareable, enabling quick alignment across teams and supporting risk and market-position discussions during planning sessions.

Economic factors

Interest Rate Volatility and Debt Management

Verizon carried about $116 billion of long-term debt at end-2024; interest rate swings in 2025 materially affect refinancing costs for spectrum and 5G capex, with Fed policy pushing benchmark yields up ~80 bps in H1 2025 increasing interest expense projections.

Higher rates compress valuation multiples and raise weighted average cost of capital, forcing stricter capital allocation between network investment, M&A and shareholder returns.

Persistent rate strength could constrain Verizon’s ability to sustain its $2.61 annual dividend per share (2024 payout) without cutting investments or borrowing more expensively.

Inflationary Pressure on Operating Costs

Persistent U.S. inflation — CPI running near 3.4% in 2024 vs 6.5% in 2022 — raises Verizon’s labor, materials and energy costs for its 5G fiber network; Verizon reported network opex rising 4.8% y/y in 2024, pressuring margins.

Rising unit costs force Verizon to weigh price increases against competitive pressure from T-Mobile and Dish; postpaid ARPU grew 2.1% y/y in 2024, limiting room for large hikes.

Verizon’s ability to pass costs through without spiking churn (churn ~0.82% postpaid in 2024) is a key economic risk impacting EBITDA and capex funding.

5G Monetization and Return on Investment

After years of heavy 5G capex—Verizon spent about $39.6 billion on network investment in 2019–2023—economic focus now targets sustainable ROI from that infrastructure.

Verizon is monetizing through private 5G for enterprises and advanced IoT; its Verizon Business segment revenue rose 8% in 2024, reflecting early traction.

The long-term success depends on enterprise adoption rates of premium services; industry forecasts expect private 5G market to reach $17–20 billion in the US by 2028, shaping Verizon’s revenue upside.

Consumer Purchasing Power and Economic Cycles

The demand for premium plans and flagship devices is cyclical and tied to U.S. GDP and consumer confidence; in 2023 U.S. real GDP grew 2.5% and consumer confidence averaged 101, supporting higher ARPU, but a 2024 Q3 slowdown saw device upgrade rates fall ~6% YoY, pressuring Verizon’s equipment revenue (~$24.5B in 2023). Monitoring indicators like CPI, unemployment (3.9% in 2024) lets Verizon tailor promotions and prepaid offerings to protect margins.

- Premium plan demand correlates with GDP and consumer confidence

- Device upgrades fell ~6% YoY in 2024 Q3, impacting equipment revenue

- Verizon equipment revenue ~$24.5B in 2023; ARPU sensitive to macro swings

- Monitor CPI, unemployment (3.9% 2024) to adjust bundles and promotions

Labor Market Dynamics and Talent Retention

The telecom sector needs skilled engineers to manage 5G, edge computing and software-defined networks; Verizon reported 133,400 employees in 2024 and spent $1.9 billion on employee benefits in 2023, reflecting high labor costs.

Intense competition for technical talent pushes wages up—median tech salaries rose ~6% in 2024—forcing Verizon to increase training and retention investments to protect service quality and innovation.

Labor market shifts, including lower unemployment in tech hubs, risk operational efficiency and could delay network upgrades if talent shortages persist.

- Verizon workforce 2024: 133,400; benefits expense 2023: $1.9B

- Tech median salaries up ~6% in 2024, raising hiring costs

- Training/retention spend critical to support 5G and software-defined transitions

Rising Rates Strain Verizon: $116B Debt, Tight FCF & Dividend Pressure

Rising rates (Fed-driven ~+80bps H1 2025) lift Verizon’s interest costs on ~$116B debt, pressuring free cash flow and dividend sustainability; network opex rose 4.8% y/y in 2024 while postpaid ARPU grew 2.1% and churn ~0.82%, limiting pricing power; Verizon Business revenue +8% in 2024 supports 5G monetization while device revenue weakness (equipment ~$24.5B in 2023) ties to GDP/consumer confidence.

| Metric | Value |

|---|---|

| Long-term debt | $116B (2024) |

| Network opex growth | +4.8% (2024) |

| Postpaid ARPU | +2.1% (2024) |

| Churn | 0.82% (2024) |

| Verizon Business rev | +8% (2024) |

Preview Before You Purchase

Verizon Communications PESTLE Analysis

The preview shown here is the exact Verizon Communications PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.