Vestas Wind Systems Boston Consulting Group Matrix

Unlock Strategic Clarity

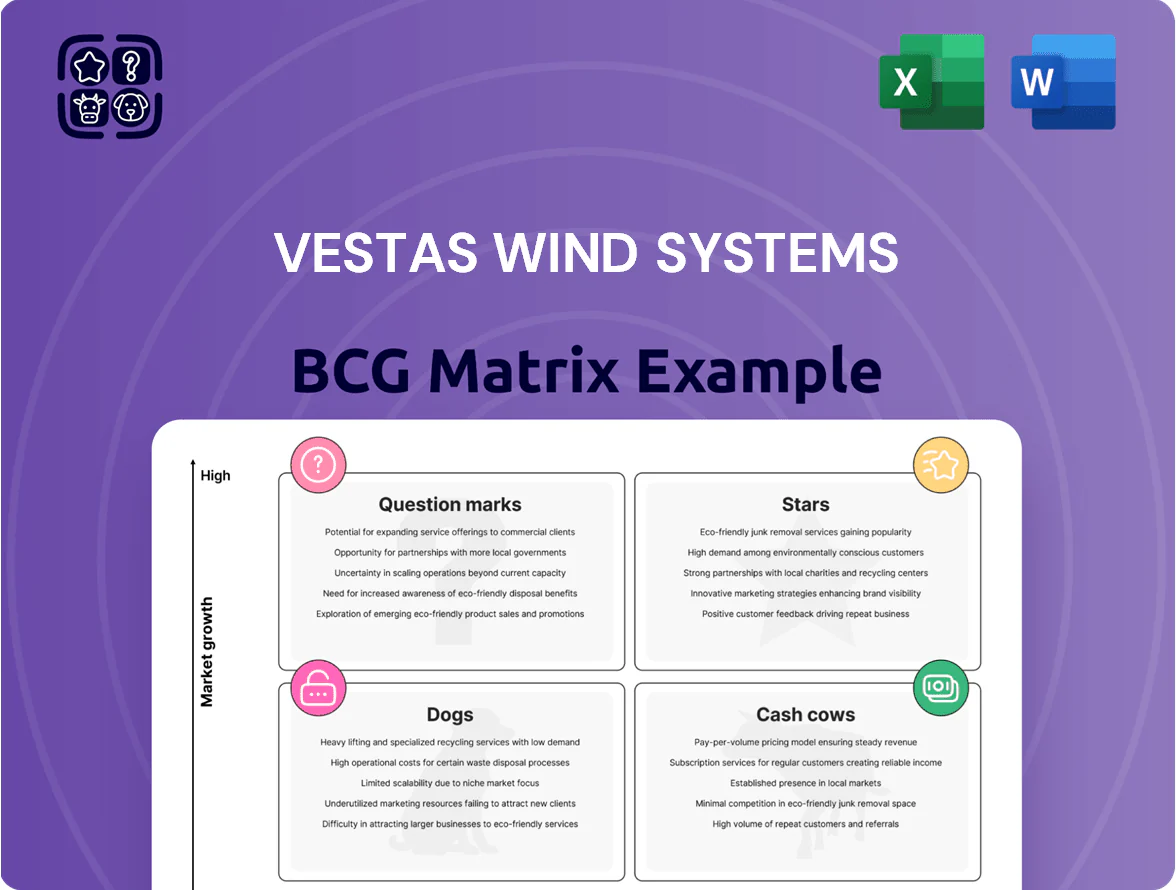

Vestas Wind Systems sits at a pivotal crossroads between rapid-growth turbine segments and mature service revenues; our BCG Matrix preview highlights which offerings are Stars driving future scale and which legacy lines risk becoming Cash Cows or Dogs. This snapshot teases product-level market share and growth dynamics—purchase the full BCG Matrix for complete quadrant placements, actionable reallocations, and a downloadable Word + Excel package to guide capital deployment and strategic priorities.

Stars

V236-15.0 MW Offshore Turbine

The V236-15.0 MW is a Star for Vestas, grabbing major share in offshore wind as the sector is forecast to grow at a CAGR >18% through 2035; its size and efficiency anchor Vestas’ market leadership.

By end-2025 Vestas reported an offshore order backlog of €10.1bn, led by the 5.2 GW North Sea contract, with the V236 central to revenue projections.

These turbines drive strong top-line growth but demand heavy cash: Vestas is expanding factories in Poland and Denmark, requiring multihundred‑million euro capex and working capital during ramp-up.

Onshore Wind Turbines outside China

Vestas holds a 30% share of the onshore wind market outside China, marking this segment as a Star that drives the sector transition as demand shifts to renewables.

In 2025 Vestas delivered over 12.5 GW of onshore capacity, with strong wins in Germany, Brazil and the UK, supporting revenue and order intake growth.

High share requires steady R&D spend—product, turbine scaling and grid services—to fend off emerging Chinese OEMs and meet evolving US regulatory and permitting rules.

EnVentus Onshore Platform

The EnVentus onshore platform, Vestas Wind Systems' next-gen modular, high-efficiency turbine, captured roughly 28% of Vestas' 2024–25 new onshore orders, driven by large projects in Australia (300 MW+ portfolio) and Europe (~1.2 GW pipeline).

Digital Wind Farm Solutions

Vestas Digital Wind Farm Solutions—SCADA and AI-driven upgrades like PowerPlus—are Stars in Vestas's BCG matrix: market share rising fast in a high-growth segment, serving a global 150+ GW installed base and supporting grid integration needs.

These software products posted double-digit growth in 2024 (Vestas reported digital revenue growth ~25% YoY), boost turbine availability by 1–3% (here’s the quick math: 1% on 150 GW ≈ 1.5 GW incremental output), and need heavy upfront spend on R&D and data ops.

They’re strategic: essential for operators squeezing extra MWh from existing assets and for meeting grid codes; continued investment keeps Vestas competitive as markets digitalize.

- Market: high-growth, global 150+ GW base

- Growth: ~25% digital revenue YoY (2024)

- Impact: +1–3% availability (~1.5 GW potential)

- Cost: high R&D/data analytics investment

Strategic Partnerships in Emerging Markets

Vestas is treating strategic joint ventures and local factories in Vietnam, South Korea, and Japan as Stars—markets forecast to grow ~15% annually, needing heavy capex to build supply chains and meet 2030 demand peaks.

By committing ~€500m in regional investments and first-mover local content deals, Vestas aims to convert early share into long-term cash flows as turbines and services scale.

- Targets: Vietnam, South Korea, Japan

- Growth: ~15% annual market CAGR

- Investment: ~€500m regional capex

- Strategy: JVs + local manufacturing

Vestas’ V236 & EnVentus Propel €10.1bn Offshore Backlog, 12.5GW Onshore & 25% Digital Growth

Vestas’ Stars: V236-15.0 MW offshore and EnVentus onshore drive share and revenues—offshore backlog €10.1bn (end‑2025), onshore deliveries 12.5 GW (2025); digital solutions grew ~25% YoY (2024) boosting availability +1–3% (~1.5 GW). Regional JVs (Vietnam/Korea/Japan) backed by ~€500m capex target 15% CAGR markets.

| Asset | Key 2024–25 Data | Capex / Notes |

|---|---|---|

| V236‑15.0 MW | Backlog €10.1bn; central to 5.2 GW North Sea | High factory capex |

| EnVentus | ~28% of new onshore orders; 12.5 GW delivered (2025) | R&D heavy |

| Digital | +25% rev YoY; +1–3% avail (~1.5 GW) | Data ops spend |

| Regional JVs | Targets: 15% CAGR markets | ~€500m regional capex |

What is included in the product

In-depth BCG overview of Vestas’ units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs amid macro/micro trends.

One-page Vestas BCG Matrix placing turbine, service and digital units in clear quadrants for fast strategic decisions.

Cash Cows

Global Service and Maintenance Business

With over 161 GW of wind turbines under service contracts and a backlog of EUR 38.7 billion at end-2025, Vestas’s Global Service and Maintenance is its most reliable Cash Cow.

The Service segment consistently posts EBIT margins above 25%, generating steady free cash flow that funds R&D for offshore Stars and new Question Marks.

Long-term service agreements, typically 20–25 years, deliver predictable recurring revenue and require minimal incremental capital expenditure.

Mature V117 and V150 Turbine Models

Legacy onshore models V117-4.2 MW and V150-4.5 MW act as Cash Cows for Vestas, delivering stable margins after >5 GW installed in Europe by 2024 and unit manufacturing costs ~15% below newer platforms due to scale.

They’re milked in Italy and Spain—~1.2 GW annual retrofit demand in 2024—mostly for simple capacity additions or replacements, yielding predictable free cash flow and >20% operating margin in renewables O&M pockets.

Proven tech and a mature supply chain cut marketing spend by an estimated 40% versus new models, letting Vestas allocate R&D and capex to growth turbines while extracting steady profits.

Repowering Solutions

As thousands of turbines hit 20-year life, Vestas’s repowering unit is a high-margin Cash Cow, upgrading sites with modern rotors and controls to extend output and boost margins—Vestas reported repowering and servicing revenue of EUR 4.1bn in 2024, with gross margins ~22% vs new-build ~12%.

Repowering leverages Vestas’s 145 GW installed base (end-2024), cutting customer acquisition costs and logistics; retrofit projects often deliver ROIC >15% and faster cash conversion than greenfield builds.

In 2025 Spain alone saw a repowering order uptick—announced projects worth ~EUR 600m—helping deliver steady high-margin cash flows that underpin Vestas’s broader financial stability.

Refurbished Turbine Sales

Vestas Refurbished Turbine sales target price-sensitive markets by selling certified, pre-owned legacy turbines, converting decommissioned assets into cash with minimal new R&D and high margin; in 2024 Vestas reported reused/repowered activity contributing an estimated EUR 150–220m revenue run-rate across service and refurbishment channels.

The unit sits in a mature niche with high market share, extending older models’ lifecycles, lowering levelized cost of energy for buyers, and advancing Vestas’ zero-waste turbine by 2040 sustainability goal.

- Targets price-sensitive markets

- Certified, pre-owned legacy tech

- High margin, low R&D

- Estimated EUR 150–220m run-rate (2024)

- Supports zero-waste by 2040

Standard Spare Parts Distribution

Standard Spare Parts Distribution is a Cash Cow: Vestas’s 189 GW installed base (2025) gives it dominant share in legacy parts for older turbines, so market growth is low but margins are high and predictable.

Proprietary components create near-monopoly pricing power, driving operating cash that funds debt service and dividends; parts & service gross margins often exceed 40% in industry reports (2024–25).

- 189 GW global installed base (Vestas, 2025)

- High-margin, low-growth segment; parts margins ~40%+

- Minimal marketing; steady cash flow for debt and dividends

Vestas’ 161GW Service Cash Cow: €38.7bn backlog, >25% EBIT funds offshore R&D

Vestas’s Service & legacy onshore turbines are Cash Cows: 161 GW under service (end-2025), EUR 38.7bn backlog, Service EBIT >25%, repowering/service revenue EUR 4.1bn (2024), parts margins ~40%, refurbished run-rate EUR 150–220m (2024); these units fund R&D and offshore growth with ROIC >15% on retrofit projects.

| Metric | Value |

|---|---|

| Installed under service | 161 GW (end-2025) |

| Backlog | EUR 38.7bn (end-2025) |

| Service EBIT | >25% |

| Repowering/service rev | EUR 4.1bn (2024) |

| Parts margin | ~40% |

| Refurb run-rate | EUR 150–220m (2024) |

Delivered as Shown

Vestas Wind Systems BCG Matrix

The Vestas Wind Systems BCG Matrix you're previewing on this page is the exact, final file you'll receive after purchase—no watermarks, no placeholder content, just a fully formatted strategic analysis ready for use.

This preview mirrors the downloadable report in full: market-backed positioning, clear quadrant placement, and actionable insights crafted by strategy experts.

Upon purchase you’ll instantly get the same editable document for presenting, printing, or integrating into business plans or investor decks.

No surprises—what you see is the professional BCG Matrix report that becomes yours with a one-time purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Vestas Wind Systems sits at a pivotal crossroads between rapid-growth turbine segments and mature service revenues; our BCG Matrix preview highlights which offerings are Stars driving future scale and which legacy lines risk becoming Cash Cows or Dogs. This snapshot teases product-level market share and growth dynamics—purchase the full BCG Matrix for complete quadrant placements, actionable reallocations, and a downloadable Word + Excel package to guide capital deployment and strategic priorities.

Stars

V236-15.0 MW Offshore Turbine

The V236-15.0 MW is a Star for Vestas, grabbing major share in offshore wind as the sector is forecast to grow at a CAGR >18% through 2035; its size and efficiency anchor Vestas’ market leadership.

By end-2025 Vestas reported an offshore order backlog of €10.1bn, led by the 5.2 GW North Sea contract, with the V236 central to revenue projections.

These turbines drive strong top-line growth but demand heavy cash: Vestas is expanding factories in Poland and Denmark, requiring multihundred‑million euro capex and working capital during ramp-up.

Onshore Wind Turbines outside China

Vestas holds a 30% share of the onshore wind market outside China, marking this segment as a Star that drives the sector transition as demand shifts to renewables.

In 2025 Vestas delivered over 12.5 GW of onshore capacity, with strong wins in Germany, Brazil and the UK, supporting revenue and order intake growth.

High share requires steady R&D spend—product, turbine scaling and grid services—to fend off emerging Chinese OEMs and meet evolving US regulatory and permitting rules.

EnVentus Onshore Platform

The EnVentus onshore platform, Vestas Wind Systems' next-gen modular, high-efficiency turbine, captured roughly 28% of Vestas' 2024–25 new onshore orders, driven by large projects in Australia (300 MW+ portfolio) and Europe (~1.2 GW pipeline).

Digital Wind Farm Solutions

Vestas Digital Wind Farm Solutions—SCADA and AI-driven upgrades like PowerPlus—are Stars in Vestas's BCG matrix: market share rising fast in a high-growth segment, serving a global 150+ GW installed base and supporting grid integration needs.

These software products posted double-digit growth in 2024 (Vestas reported digital revenue growth ~25% YoY), boost turbine availability by 1–3% (here’s the quick math: 1% on 150 GW ≈ 1.5 GW incremental output), and need heavy upfront spend on R&D and data ops.

They’re strategic: essential for operators squeezing extra MWh from existing assets and for meeting grid codes; continued investment keeps Vestas competitive as markets digitalize.

- Market: high-growth, global 150+ GW base

- Growth: ~25% digital revenue YoY (2024)

- Impact: +1–3% availability (~1.5 GW potential)

- Cost: high R&D/data analytics investment

Strategic Partnerships in Emerging Markets

Vestas is treating strategic joint ventures and local factories in Vietnam, South Korea, and Japan as Stars—markets forecast to grow ~15% annually, needing heavy capex to build supply chains and meet 2030 demand peaks.

By committing ~€500m in regional investments and first-mover local content deals, Vestas aims to convert early share into long-term cash flows as turbines and services scale.

- Targets: Vietnam, South Korea, Japan

- Growth: ~15% annual market CAGR

- Investment: ~€500m regional capex

- Strategy: JVs + local manufacturing

Vestas’ V236 & EnVentus Propel €10.1bn Offshore Backlog, 12.5GW Onshore & 25% Digital Growth

Vestas’ Stars: V236-15.0 MW offshore and EnVentus onshore drive share and revenues—offshore backlog €10.1bn (end‑2025), onshore deliveries 12.5 GW (2025); digital solutions grew ~25% YoY (2024) boosting availability +1–3% (~1.5 GW). Regional JVs (Vietnam/Korea/Japan) backed by ~€500m capex target 15% CAGR markets.

| Asset | Key 2024–25 Data | Capex / Notes |

|---|---|---|

| V236‑15.0 MW | Backlog €10.1bn; central to 5.2 GW North Sea | High factory capex |

| EnVentus | ~28% of new onshore orders; 12.5 GW delivered (2025) | R&D heavy |

| Digital | +25% rev YoY; +1–3% avail (~1.5 GW) | Data ops spend |

| Regional JVs | Targets: 15% CAGR markets | ~€500m regional capex |

What is included in the product

In-depth BCG overview of Vestas’ units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs amid macro/micro trends.

One-page Vestas BCG Matrix placing turbine, service and digital units in clear quadrants for fast strategic decisions.

Cash Cows

Global Service and Maintenance Business

With over 161 GW of wind turbines under service contracts and a backlog of EUR 38.7 billion at end-2025, Vestas’s Global Service and Maintenance is its most reliable Cash Cow.

The Service segment consistently posts EBIT margins above 25%, generating steady free cash flow that funds R&D for offshore Stars and new Question Marks.

Long-term service agreements, typically 20–25 years, deliver predictable recurring revenue and require minimal incremental capital expenditure.

Mature V117 and V150 Turbine Models

Legacy onshore models V117-4.2 MW and V150-4.5 MW act as Cash Cows for Vestas, delivering stable margins after >5 GW installed in Europe by 2024 and unit manufacturing costs ~15% below newer platforms due to scale.

They’re milked in Italy and Spain—~1.2 GW annual retrofit demand in 2024—mostly for simple capacity additions or replacements, yielding predictable free cash flow and >20% operating margin in renewables O&M pockets.

Proven tech and a mature supply chain cut marketing spend by an estimated 40% versus new models, letting Vestas allocate R&D and capex to growth turbines while extracting steady profits.

Repowering Solutions

As thousands of turbines hit 20-year life, Vestas’s repowering unit is a high-margin Cash Cow, upgrading sites with modern rotors and controls to extend output and boost margins—Vestas reported repowering and servicing revenue of EUR 4.1bn in 2024, with gross margins ~22% vs new-build ~12%.

Repowering leverages Vestas’s 145 GW installed base (end-2024), cutting customer acquisition costs and logistics; retrofit projects often deliver ROIC >15% and faster cash conversion than greenfield builds.

In 2025 Spain alone saw a repowering order uptick—announced projects worth ~EUR 600m—helping deliver steady high-margin cash flows that underpin Vestas’s broader financial stability.

Refurbished Turbine Sales

Vestas Refurbished Turbine sales target price-sensitive markets by selling certified, pre-owned legacy turbines, converting decommissioned assets into cash with minimal new R&D and high margin; in 2024 Vestas reported reused/repowered activity contributing an estimated EUR 150–220m revenue run-rate across service and refurbishment channels.

The unit sits in a mature niche with high market share, extending older models’ lifecycles, lowering levelized cost of energy for buyers, and advancing Vestas’ zero-waste turbine by 2040 sustainability goal.

- Targets price-sensitive markets

- Certified, pre-owned legacy tech

- High margin, low R&D

- Estimated EUR 150–220m run-rate (2024)

- Supports zero-waste by 2040

Standard Spare Parts Distribution

Standard Spare Parts Distribution is a Cash Cow: Vestas’s 189 GW installed base (2025) gives it dominant share in legacy parts for older turbines, so market growth is low but margins are high and predictable.

Proprietary components create near-monopoly pricing power, driving operating cash that funds debt service and dividends; parts & service gross margins often exceed 40% in industry reports (2024–25).

- 189 GW global installed base (Vestas, 2025)

- High-margin, low-growth segment; parts margins ~40%+

- Minimal marketing; steady cash flow for debt and dividends

Vestas’ 161GW Service Cash Cow: €38.7bn backlog, >25% EBIT funds offshore R&D

Vestas’s Service & legacy onshore turbines are Cash Cows: 161 GW under service (end-2025), EUR 38.7bn backlog, Service EBIT >25%, repowering/service revenue EUR 4.1bn (2024), parts margins ~40%, refurbished run-rate EUR 150–220m (2024); these units fund R&D and offshore growth with ROIC >15% on retrofit projects.

| Metric | Value |

|---|---|

| Installed under service | 161 GW (end-2025) |

| Backlog | EUR 38.7bn (end-2025) |

| Service EBIT | >25% |

| Repowering/service rev | EUR 4.1bn (2024) |

| Parts margin | ~40% |

| Refurb run-rate | EUR 150–220m (2024) |

Delivered as Shown

Vestas Wind Systems BCG Matrix

The Vestas Wind Systems BCG Matrix you're previewing on this page is the exact, final file you'll receive after purchase—no watermarks, no placeholder content, just a fully formatted strategic analysis ready for use.

This preview mirrors the downloadable report in full: market-backed positioning, clear quadrant placement, and actionable insights crafted by strategy experts.

Upon purchase you’ll instantly get the same editable document for presenting, printing, or integrating into business plans or investor decks.

No surprises—what you see is the professional BCG Matrix report that becomes yours with a one-time purchase.