Viant Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

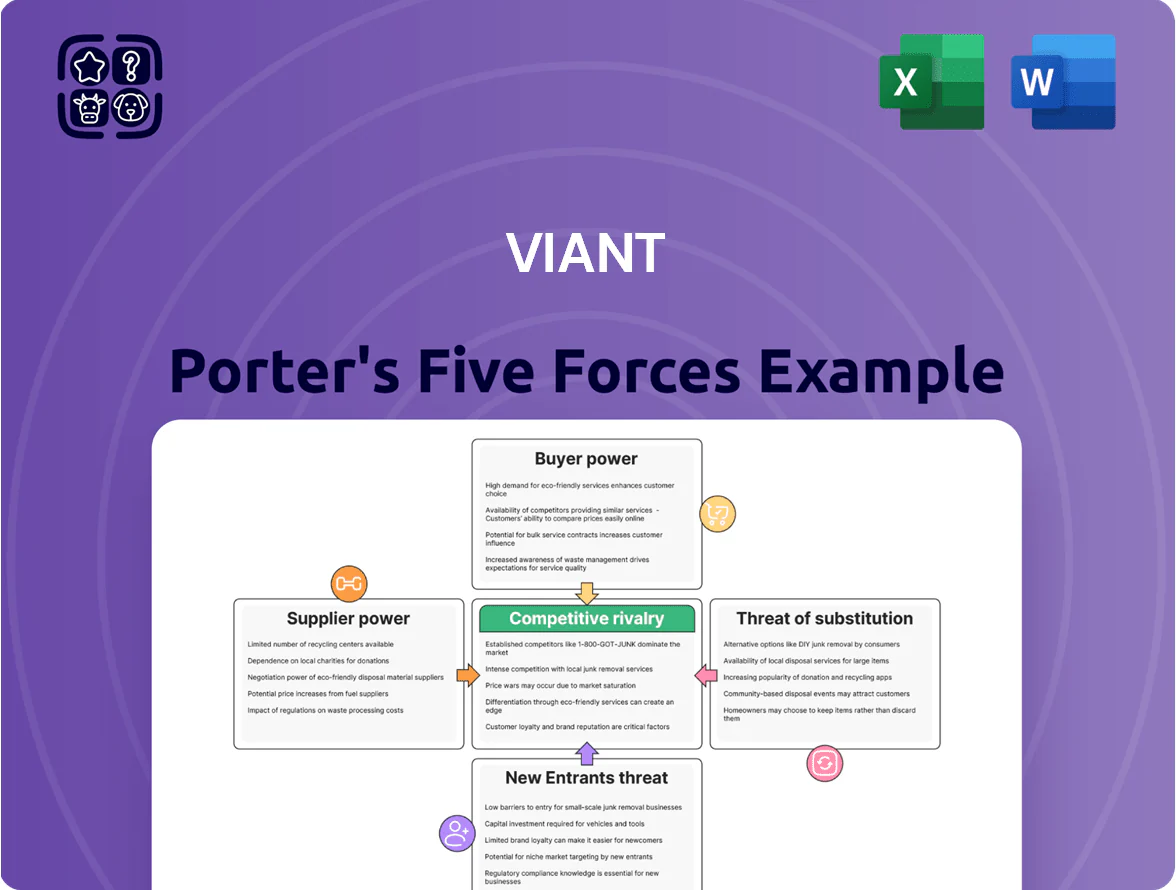

Viant faces intense rivalry from ad-tech incumbents and rising programmatic platforms, while buyers wield strong leverage through scale and data demands; suppliers exert moderate influence but data privacy shifts heighten compliance costs and operational complexity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Viant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Premium CTV Inventory

Publishers of premium Connected TV (CTV) inventory hold strong leverage because premium ad slots are scarce while advertiser spend on CTV rose 28% in 2024 to $19.3B, keeping supply tight.

Viant’s Adelphic depends on top-tier media partners, letting large owners push higher CPMs or favor direct deals over programmatic; reported CTV CPMs climbed 22% in 2025 YTD.

This dependency deepens as streaming viewership hit 85% of US households by Q3 2025, concentrating pricing power with a few high-demand publishers.

Cloud Infrastructure Dependencies

Viant runs on cloud infrastructure, so AWS and Google Cloud hold high supplier power; switching costs for 2025-scale adtech workloads (petabytes, thousands of VMs) exceed tens of millions of dollars and months of engineering work.

Price hikes or SLAs changes by these providers directly squeeze Viant’s margins—cloud IaaS rose ~12% YoY in spot markets in 2024, so a 5–10% rate increase would cut operating margin materially.

Data Provider Concentration

Viant’s Household ID relies on high-quality third-party feeds; about 4-6 specialist vendors supply the most accurate demographic and behavioral datasets, concentrating leverage in the supplier base.

Those vendors can raise licensing fees or limit access—industry reports show data licensing price indices rose ~12% from 2022–2024, squeezing margins for DSPs and identity platforms.

Tighter privacy rules expected by end-2025 (e.g., updated US state laws and EU adequacy talks) increase demand for compliant, high-fidelity sources, strengthening supplier bargaining power and raising switch costs for Viant.

Supply Path Optimization Trends

Supply Path Optimization (SPO) lets advertisers cut intermediaries, reducing fees—SPO adoption rose to ~45% of programmatic spend in 2024, pressuring margins.

Consolidated major SSPs can favor select DSPs, so Viant needs tight tech integrations and competitive fee/share terms to keep client access to premium inventory.

This forces Viant to prove clear ROI and unique data-driven value or risk exclusion from top buying paths.

- ~45% programmatic spend via SPO (2024)

- Major SSP consolidation increases gatekeeping risk

- Must maintain integrations, favorable terms

- Continuous ROI proof needed to avoid exclusion

Regulatory Compliance Services

Viant must embed these services to keep omnichannel campaigns lawful across regions; loss of compliance can cost fines like GDPR penalties up to €20m or 4% of revenue, so vendors hold steady bargaining power.

- 140+ jurisdictions with data rules (2025)

- GDPR max fine: €20m/4% revenue

- Specialized tech → few alternatives

- Integration necessary to avoid legal risk

Suppliers Hold the Cards: Scarce CTV, Costly Cloud, Data & Compliance Drive Power

Suppliers—premium CTV publishers, cloud IaaS (AWS/GCP), data vendors, SSPs, and compliance-tool providers—hold high bargaining power due to scarce premium inventory, concentrated data sources, cloud switching costs (tens of millions), SPO pressure (~45% programmatic spend in 2024), and 140+ jurisdictions with modern privacy laws by 2025.

| Supplier | Key stat | Impact |

|---|---|---|

| CTV publishers | CTV ad spend $19.3B (2024) | High CPMs, scarcity |

| Cloud IaaS | Spot +12% YoY (2024) | High switch cost |

| Data vendors | Licensing +12% (2022–24) | Margin pressure |

| SPO/SSPs | 45% programmatic (2024) | Access gatekeeping |

| Compliance tools | 140+ jurisdictions (2025) | Mandatory integration |

What is included in the product

Tailored Porter's Five Forces analysis for Viant that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to inform strategy and valuation.

Interactive Porter's Five Forces for Viant—one-sheet clarity that maps competitive pressure and suggests targeted mitigation actions for faster strategic decisions.

Customers Bargaining Power

Low Switching Costs for Agencies

Advertising agencies run multiple demand-side platforms (DSPs) and can reallocate budgets quickly, so Viant faces constant churn risk unless it proves superior ROI; in 2024, programmatic spend shifts saw 28% of agency budgets move quarterly between DSPs.

Low switching costs mean agencies will shift to competitors like The Trade Desk or Google if performance lags; Viant reported $123.2M revenue in Q3 2024, so even small market-share loss can cut growth sharply.

Demand for Pricing Transparency

By late 2025, 68% of large advertisers demand full take-rate transparency across DSPs and SSPs, pressuring buyers to negotiate lower margins or flat fees as they understand ad-tech cost stacks.

Customers can force Viant to cut fees—median programmatic take rates fell from 19% in 2022 to 14% in 2024—so Viant must offer granular, auditable reporting tying fees to measurable outcomes.

In-Housing of Ad Tech

In-housing of ad tech is rising: by 2024 about 38% of global ad spend from top 200 brands was managed in-house, so Viant faces customers with deep first-party data and tech skills who push for custom features and volume pricing; these direct-to-brand buyers can cut agency fees (US advertisers saved an estimated $4.3B in 2023) and force Viant to split sales motions between agencies and internal brand teams, redesigning product demos, SLAs, and pricing tiers.

Consolidation of Ad Budgets

Large advertisers have moved budgets to fewer platforms: the top 10 global advertisers now allocate ~45% of digital ad spend to preferred stacks, pressuring Viant to win RFP slots or lose full budgets.

Being excluded from a consolidated tech stack means total revenue loss per client, so buyers push harder on SLAs, pricing, and integrations, lowering Viant’s bargaining power.

Competition from DSPs and walled gardens (Google, Meta, The Trade Desk) amplifies buyer leverage during negotiations.

- Top 10 advertisers: ~45% spend concentration

- Missing RFP slot = full budget loss

- Buyers demand tougher SLAs, lower fees

Requirement for Unified Measurement

Customers now demand cross-channel measurement that ties CTV views to sales or store visits; industry studies show 62% of marketers in 2024 prioritized unified attribution across TV and digital for budget allocation decisions.

If Viant’s Household ID fails to match or outperform rivals’ models, clients will shift spend—programmatic budgets moved 14% toward platforms with superior attribution in 2023–24.

Buyers use measurement accuracy to enforce ROI: advertisers expect campaign-level ROAS proof and can withhold renewal if lift tests or foot-traffic linking miss targets.

- 62% of marketers prioritize cross-channel attribution (2024)

- 14% programmatic budget reallocation to better-attributing platforms (2023–24)

- Clients demand campaign-level ROAS and foot-traffic linkage

Advertisers Seize Power: In‑housing, DSP Shifts Drive Fee Cuts & Demand Unified Attribution

Buyers hold strong leverage: low switching costs, agency reallocation (28% quarterly DSP shifts in 2024), in-housing (38% of top-200 brand spend in-house, 2024), and top-10 advertisers concentrating ~45% of spend force Viant to cut fees and meet strict SLAs; median take-rates fell 19%→14% (2022–24), and 62% of marketers demand unified attribution (2024).

| Metric | Value |

|---|---|

| Quarterly DSP reallocation | 28% |

| In-housed top-200 spend (2024) | 38% |

| Top-10 advertiser spend share | ~45% |

| Take-rate median (2022→2024) | 19%→14% |

| Marketers prioritizing unified attribution (2024) | 62% |

Preview the Actual Deliverable

Viant Porter's Five Forces Analysis

This preview shows the exact Viant Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted, ready to download, and usable the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Viant faces intense rivalry from ad-tech incumbents and rising programmatic platforms, while buyers wield strong leverage through scale and data demands; suppliers exert moderate influence but data privacy shifts heighten compliance costs and operational complexity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Viant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Premium CTV Inventory

Publishers of premium Connected TV (CTV) inventory hold strong leverage because premium ad slots are scarce while advertiser spend on CTV rose 28% in 2024 to $19.3B, keeping supply tight.

Viant’s Adelphic depends on top-tier media partners, letting large owners push higher CPMs or favor direct deals over programmatic; reported CTV CPMs climbed 22% in 2025 YTD.

This dependency deepens as streaming viewership hit 85% of US households by Q3 2025, concentrating pricing power with a few high-demand publishers.

Cloud Infrastructure Dependencies

Viant runs on cloud infrastructure, so AWS and Google Cloud hold high supplier power; switching costs for 2025-scale adtech workloads (petabytes, thousands of VMs) exceed tens of millions of dollars and months of engineering work.

Price hikes or SLAs changes by these providers directly squeeze Viant’s margins—cloud IaaS rose ~12% YoY in spot markets in 2024, so a 5–10% rate increase would cut operating margin materially.

Data Provider Concentration

Viant’s Household ID relies on high-quality third-party feeds; about 4-6 specialist vendors supply the most accurate demographic and behavioral datasets, concentrating leverage in the supplier base.

Those vendors can raise licensing fees or limit access—industry reports show data licensing price indices rose ~12% from 2022–2024, squeezing margins for DSPs and identity platforms.

Tighter privacy rules expected by end-2025 (e.g., updated US state laws and EU adequacy talks) increase demand for compliant, high-fidelity sources, strengthening supplier bargaining power and raising switch costs for Viant.

Supply Path Optimization Trends

Supply Path Optimization (SPO) lets advertisers cut intermediaries, reducing fees—SPO adoption rose to ~45% of programmatic spend in 2024, pressuring margins.

Consolidated major SSPs can favor select DSPs, so Viant needs tight tech integrations and competitive fee/share terms to keep client access to premium inventory.

This forces Viant to prove clear ROI and unique data-driven value or risk exclusion from top buying paths.

- ~45% programmatic spend via SPO (2024)

- Major SSP consolidation increases gatekeeping risk

- Must maintain integrations, favorable terms

- Continuous ROI proof needed to avoid exclusion

Regulatory Compliance Services

Viant must embed these services to keep omnichannel campaigns lawful across regions; loss of compliance can cost fines like GDPR penalties up to €20m or 4% of revenue, so vendors hold steady bargaining power.

- 140+ jurisdictions with data rules (2025)

- GDPR max fine: €20m/4% revenue

- Specialized tech → few alternatives

- Integration necessary to avoid legal risk

Suppliers Hold the Cards: Scarce CTV, Costly Cloud, Data & Compliance Drive Power

Suppliers—premium CTV publishers, cloud IaaS (AWS/GCP), data vendors, SSPs, and compliance-tool providers—hold high bargaining power due to scarce premium inventory, concentrated data sources, cloud switching costs (tens of millions), SPO pressure (~45% programmatic spend in 2024), and 140+ jurisdictions with modern privacy laws by 2025.

| Supplier | Key stat | Impact |

|---|---|---|

| CTV publishers | CTV ad spend $19.3B (2024) | High CPMs, scarcity |

| Cloud IaaS | Spot +12% YoY (2024) | High switch cost |

| Data vendors | Licensing +12% (2022–24) | Margin pressure |

| SPO/SSPs | 45% programmatic (2024) | Access gatekeeping |

| Compliance tools | 140+ jurisdictions (2025) | Mandatory integration |

What is included in the product

Tailored Porter's Five Forces analysis for Viant that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to inform strategy and valuation.

Interactive Porter's Five Forces for Viant—one-sheet clarity that maps competitive pressure and suggests targeted mitigation actions for faster strategic decisions.

Customers Bargaining Power

Low Switching Costs for Agencies

Advertising agencies run multiple demand-side platforms (DSPs) and can reallocate budgets quickly, so Viant faces constant churn risk unless it proves superior ROI; in 2024, programmatic spend shifts saw 28% of agency budgets move quarterly between DSPs.

Low switching costs mean agencies will shift to competitors like The Trade Desk or Google if performance lags; Viant reported $123.2M revenue in Q3 2024, so even small market-share loss can cut growth sharply.

Demand for Pricing Transparency

By late 2025, 68% of large advertisers demand full take-rate transparency across DSPs and SSPs, pressuring buyers to negotiate lower margins or flat fees as they understand ad-tech cost stacks.

Customers can force Viant to cut fees—median programmatic take rates fell from 19% in 2022 to 14% in 2024—so Viant must offer granular, auditable reporting tying fees to measurable outcomes.

In-Housing of Ad Tech

In-housing of ad tech is rising: by 2024 about 38% of global ad spend from top 200 brands was managed in-house, so Viant faces customers with deep first-party data and tech skills who push for custom features and volume pricing; these direct-to-brand buyers can cut agency fees (US advertisers saved an estimated $4.3B in 2023) and force Viant to split sales motions between agencies and internal brand teams, redesigning product demos, SLAs, and pricing tiers.

Consolidation of Ad Budgets

Large advertisers have moved budgets to fewer platforms: the top 10 global advertisers now allocate ~45% of digital ad spend to preferred stacks, pressuring Viant to win RFP slots or lose full budgets.

Being excluded from a consolidated tech stack means total revenue loss per client, so buyers push harder on SLAs, pricing, and integrations, lowering Viant’s bargaining power.

Competition from DSPs and walled gardens (Google, Meta, The Trade Desk) amplifies buyer leverage during negotiations.

- Top 10 advertisers: ~45% spend concentration

- Missing RFP slot = full budget loss

- Buyers demand tougher SLAs, lower fees

Requirement for Unified Measurement

Customers now demand cross-channel measurement that ties CTV views to sales or store visits; industry studies show 62% of marketers in 2024 prioritized unified attribution across TV and digital for budget allocation decisions.

If Viant’s Household ID fails to match or outperform rivals’ models, clients will shift spend—programmatic budgets moved 14% toward platforms with superior attribution in 2023–24.

Buyers use measurement accuracy to enforce ROI: advertisers expect campaign-level ROAS proof and can withhold renewal if lift tests or foot-traffic linking miss targets.

- 62% of marketers prioritize cross-channel attribution (2024)

- 14% programmatic budget reallocation to better-attributing platforms (2023–24)

- Clients demand campaign-level ROAS and foot-traffic linkage

Advertisers Seize Power: In‑housing, DSP Shifts Drive Fee Cuts & Demand Unified Attribution

Buyers hold strong leverage: low switching costs, agency reallocation (28% quarterly DSP shifts in 2024), in-housing (38% of top-200 brand spend in-house, 2024), and top-10 advertisers concentrating ~45% of spend force Viant to cut fees and meet strict SLAs; median take-rates fell 19%→14% (2022–24), and 62% of marketers demand unified attribution (2024).

| Metric | Value |

|---|---|

| Quarterly DSP reallocation | 28% |

| In-housed top-200 spend (2024) | 38% |

| Top-10 advertiser spend share | ~45% |

| Take-rate median (2022→2024) | 19%→14% |

| Marketers prioritizing unified attribution (2024) | 62% |

Preview the Actual Deliverable

Viant Porter's Five Forces Analysis

This preview shows the exact Viant Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted, ready to download, and usable the moment you buy.