VIA Technologies Porter's Five Forces Analysis

Don't Miss the Bigger Picture

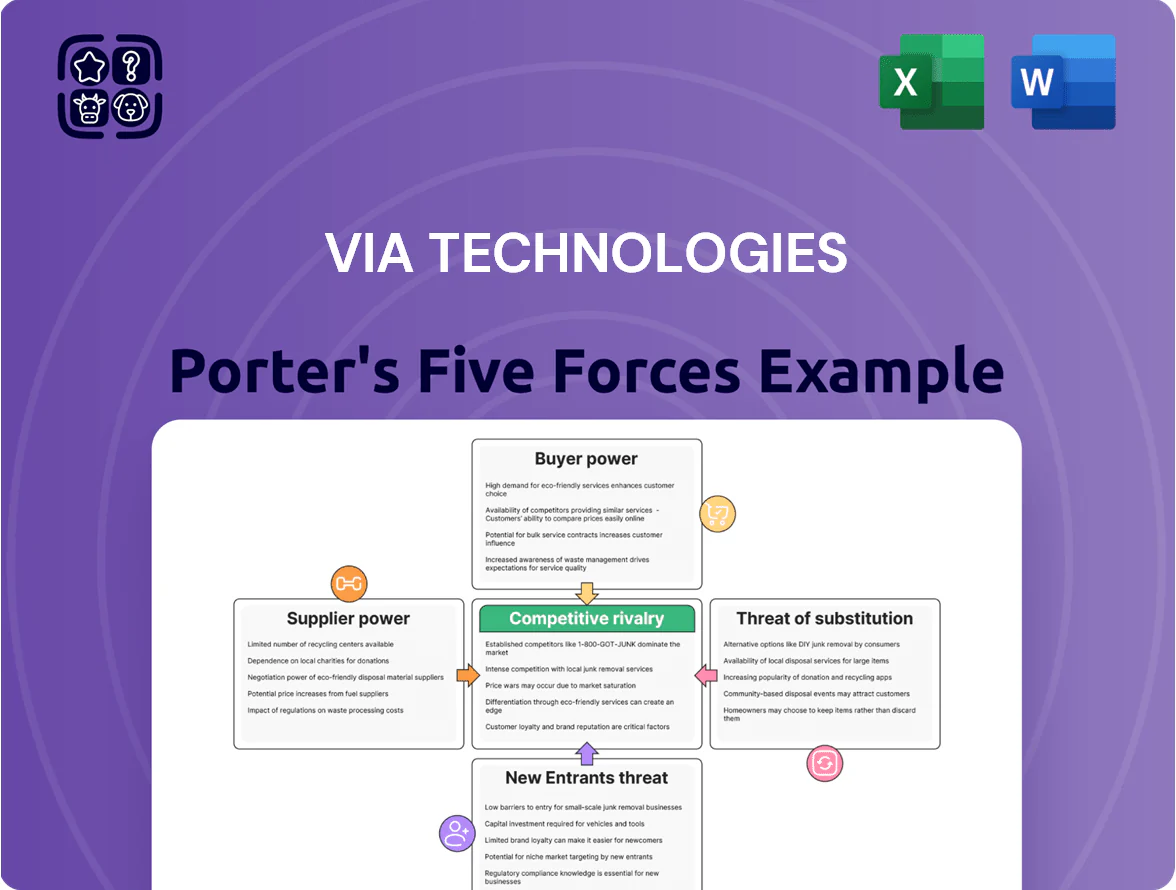

VIA Technologies faces moderate buyer power and intense rivalry from larger chipmakers, while supplier leverage and capital barriers temper new entrants; substitutes and regulator shifts add asymmetric risks that shape strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VIA Technologies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on Tier-One Foundries

As a fabless company VIA Technologies depends on Tier-One foundries like TSMC and UMC for chip fabrication; TSMC alone held ~56% of global foundry revenue in 2024, giving it leverage over pricing and allocation.

Advanced nodes are capacity-constrained—TSMC’s 5nm/3nm lines ran near full utilization in 2024—so any price hikes or priority shifts for high-demand customers can raise VIA’s COGS and delay shipments.

Dominance of EDA Tool Providers

The IC design relies on a few EDA vendors—Cadence Design Systems and Synopsys dominate ~70–80% of the global market (2024 revenue: Synopsys $5.6B, Cadence $4.6B), giving them high supplier power; their tools are essential and switching costs (retraining, IP migration) are large, so VIA must keep strong vendor ties for latest methodologies and priority support to avoid design delays and extra costs.

Intellectual Property Licensing Constraints

VIA relies on third-party IP cores such as ARM, where typical licensing can demand upfront fees plus per-unit royalties of $0.50–$2.00, squeezing gross margins; ARM reported licensing revenue of $1.9bn in FY2024, underscoring supplier leverage.

Because ARM and similar providers control industry-standard ISAs, VIA cannot easily cut costs without building proprietary CPU designs—a path requiring multi-year R&D and hundreds of millions in capex—or shifting to open ISAs like RISC-V, which still lack equivalent ecosystem maturity.

Specialized Component Shortages

The embedded-systems supply chain relies on substrates and high-grade silicon wafers; in 2024 global wafer shortages pushed foundry lead times to 20–28 weeks, giving niche suppliers short-term pricing power and causing component price jumps of 8–15% in some segments.

VIA must hedge via multi-sourcing, inventory buffers (6–12 weeks), and long-term purchase agreements to protect industrial and automotive lines from production delays and margin erosion.

- Wafers: 20–28 week lead times (2024)

- Price spikes: 8–15% in niche components

- Recommended buffer: 6–12 weeks inventory

- Mitigation: multi-source + long-term contracts

Geographic Concentration of Supply

- 65–75% suppliers in Taiwan/mainland China

- 28% shipping delay spike seen in 2022

- $486M VIA revenue FY2024

- Mitigations: sourcing diversification, buffers

High supplier power: TSMC dominance, capacity crunch, Taiwan concentration risk

Supplier power is high: TSMC/UMC dominance (TSMC ~56% foundry revenue 2024) and constrained advanced-node capacity (5nm/3nm near-full in 2024) raise VIA’s COGS and delay risk; EDA/IP vendors (Synopsys $5.6B, Cadence $4.6B 2024; ARM licensing $1.9B FY2024) add switching costs and royalties; 65–75% suppliers in Taiwan/China concentrate logistics risk; mitigate via multi-sourcing, 6–12 week buffers, LTAs.

| Metric | Value |

|---|---|

| TSMC market share (2024) | ~56% |

| Foundry lead times (2024) | 20–28 weeks |

| EDA revenues (2024) | Synopsys $5.6B; Cadence $4.6B |

| ARM licensing (FY2024) | $1.9B |

| Supplier regional concentration (2025) | 65–75% Taiwan/China |

| VIA revenue (FY2024) | $486M |

What is included in the product

Tailored Porter's Five Forces analysis for VIA Technologies, uncovering competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for VIA Technologies—quickly reveal supplier/customer leverage, competitive rivalry, threat of entrants/substitutes, and strategic choke points to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Industrial Clients

VIA’s focus on industrial automation and transportation means a large share of revenue comes from a few high-volume enterprise clients, with top 5 customers historically representing roughly 45–60% of embedded systems sales in comparable firms (2024 industry median). These large organizations wield strong bargaining power, demanding custom features, longer payment terms, and aggressive price discounts often cutting margins by 5–10 percentage points. Losing a single major contract could swing VIA’s embedded-segment revenue by 15–30% and materially hurt quarterly EBITDA. That concentration raises client-driven execution and cash-flow risk for VIA.

Availability of Alternative Architectures

Customers in IoT and embedded markets choose among x86, ARM, and fast-growing RISC-V options, giving buyers strong leverage; IDC reported ARM/RISC-V designs made up over 70% of new IoT silicon shipments in 2024. This choice raises switching risk as clients chase better performance-per-watt or lower BOM costs. VIA must keep innovating — e.g., lowering platform TCO by 10–20% or adding unique security/IP to retain customers.

Low Switching Costs for Modular Systems

Modern industrial PCs use modular compute-on-module standards (e.g., COM Express, SMARC) so customers can swap modules without redesigning systems, lowering switching costs and raising buyer power against VIA Technologies.

This modularity lets buyers shift to rivals; industry data show embedded module market grew 6.8% in 2024 to $3.9B, increasing supplier options and price pressure on VIA.

As a result, VIA must keep service SLAs, rapid firmware updates, and competitive pricing—else risk losing long-term OEM contracts that often represent 20–40% of revenue per customer.

Demand for Integrated Software Solutions

Buyers now prefer hardware bundled with AI and computer vision software, pushing demand for plug-and-play industrial AI; in 2024, global edge AI software revenue hit about $4.6B, up 28% year-over-year, so VIA must offer integrated stacks not just chips.

VIA’s competitiveness hinges on delivering end-to-end solutions, including deployment support and model updates, or risk losing deals to firms that bundle software and services with similar silicon.

- Edge AI software market ~ $4.6B (2024, +28% YoY)

- Buyers seek integrated bundles, not raw silicon

- VIA needs plug-and-play AI + support to win industrial deals

Price Sensitivity in IoT Markets

Mass-market IoT buyers are highly price sensitive; a 1–3% unit-cost gap can sway OEM choices, and global IoT device average selling price fell ~6% in 2024 to about $18 per unit, intensifying pressure on margins.

Customers use strong competition—Qualcomm, MediaTek, NXP, Realtek—to force price concessions; chip industry gross margins averaged ~30% in 2024, but mass-IoT segments often sit below 20%.

VIA must tilt toward higher-margin verticals (industrial, medical) while accepting thin margins in consumer IoT to keep volume and scale.

- 1–3% unit-cost sensitivity

- IoT ASP ≈ $18 in 2024 (−6% YoY)

- Chip gross margins: industry ~30%, mass-IoT <20%

- Strategy: pursue specialized apps for margin

Buyer Power & ARM/RISC‑V Shift Compress VIA's Margins Amid Edge‑AI Stack Demand

Large enterprise buyers give VIA high bargaining power—top clients can drive 15–30% revenue swings and force 5–10ppt margin cuts; embedded customers’ modular standards and ARM/RISC-V adoption (70% of new IoT silicon, 2024) raise switching risk. Edge AI software growth ($4.6B, +28% YoY, 2024) means buyers prefer integrated stacks; price sensitivity (IoT ASP ≈ $18, −6% YoY) compresses mass-market margins.

| Metric | 2024 |

|---|---|

| Top-client revenue swing | 15–30% |

| ARM/RISC-V share | ≈70% |

| Edge AI software | $4.6B (+28%) |

| IoT ASP | $18 (−6%) |

Same Document Delivered

VIA Technologies Porter's Five Forces Analysis

This preview shows the exact VIA Technologies Porter's Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

VIA Technologies faces moderate buyer power and intense rivalry from larger chipmakers, while supplier leverage and capital barriers temper new entrants; substitutes and regulator shifts add asymmetric risks that shape strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VIA Technologies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on Tier-One Foundries

As a fabless company VIA Technologies depends on Tier-One foundries like TSMC and UMC for chip fabrication; TSMC alone held ~56% of global foundry revenue in 2024, giving it leverage over pricing and allocation.

Advanced nodes are capacity-constrained—TSMC’s 5nm/3nm lines ran near full utilization in 2024—so any price hikes or priority shifts for high-demand customers can raise VIA’s COGS and delay shipments.

Dominance of EDA Tool Providers

The IC design relies on a few EDA vendors—Cadence Design Systems and Synopsys dominate ~70–80% of the global market (2024 revenue: Synopsys $5.6B, Cadence $4.6B), giving them high supplier power; their tools are essential and switching costs (retraining, IP migration) are large, so VIA must keep strong vendor ties for latest methodologies and priority support to avoid design delays and extra costs.

Intellectual Property Licensing Constraints

VIA relies on third-party IP cores such as ARM, where typical licensing can demand upfront fees plus per-unit royalties of $0.50–$2.00, squeezing gross margins; ARM reported licensing revenue of $1.9bn in FY2024, underscoring supplier leverage.

Because ARM and similar providers control industry-standard ISAs, VIA cannot easily cut costs without building proprietary CPU designs—a path requiring multi-year R&D and hundreds of millions in capex—or shifting to open ISAs like RISC-V, which still lack equivalent ecosystem maturity.

Specialized Component Shortages

The embedded-systems supply chain relies on substrates and high-grade silicon wafers; in 2024 global wafer shortages pushed foundry lead times to 20–28 weeks, giving niche suppliers short-term pricing power and causing component price jumps of 8–15% in some segments.

VIA must hedge via multi-sourcing, inventory buffers (6–12 weeks), and long-term purchase agreements to protect industrial and automotive lines from production delays and margin erosion.

- Wafers: 20–28 week lead times (2024)

- Price spikes: 8–15% in niche components

- Recommended buffer: 6–12 weeks inventory

- Mitigation: multi-source + long-term contracts

Geographic Concentration of Supply

- 65–75% suppliers in Taiwan/mainland China

- 28% shipping delay spike seen in 2022

- $486M VIA revenue FY2024

- Mitigations: sourcing diversification, buffers

High supplier power: TSMC dominance, capacity crunch, Taiwan concentration risk

Supplier power is high: TSMC/UMC dominance (TSMC ~56% foundry revenue 2024) and constrained advanced-node capacity (5nm/3nm near-full in 2024) raise VIA’s COGS and delay risk; EDA/IP vendors (Synopsys $5.6B, Cadence $4.6B 2024; ARM licensing $1.9B FY2024) add switching costs and royalties; 65–75% suppliers in Taiwan/China concentrate logistics risk; mitigate via multi-sourcing, 6–12 week buffers, LTAs.

| Metric | Value |

|---|---|

| TSMC market share (2024) | ~56% |

| Foundry lead times (2024) | 20–28 weeks |

| EDA revenues (2024) | Synopsys $5.6B; Cadence $4.6B |

| ARM licensing (FY2024) | $1.9B |

| Supplier regional concentration (2025) | 65–75% Taiwan/China |

| VIA revenue (FY2024) | $486M |

What is included in the product

Tailored Porter's Five Forces analysis for VIA Technologies, uncovering competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic implications for pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for VIA Technologies—quickly reveal supplier/customer leverage, competitive rivalry, threat of entrants/substitutes, and strategic choke points to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Industrial Clients

VIA’s focus on industrial automation and transportation means a large share of revenue comes from a few high-volume enterprise clients, with top 5 customers historically representing roughly 45–60% of embedded systems sales in comparable firms (2024 industry median). These large organizations wield strong bargaining power, demanding custom features, longer payment terms, and aggressive price discounts often cutting margins by 5–10 percentage points. Losing a single major contract could swing VIA’s embedded-segment revenue by 15–30% and materially hurt quarterly EBITDA. That concentration raises client-driven execution and cash-flow risk for VIA.

Availability of Alternative Architectures

Customers in IoT and embedded markets choose among x86, ARM, and fast-growing RISC-V options, giving buyers strong leverage; IDC reported ARM/RISC-V designs made up over 70% of new IoT silicon shipments in 2024. This choice raises switching risk as clients chase better performance-per-watt or lower BOM costs. VIA must keep innovating — e.g., lowering platform TCO by 10–20% or adding unique security/IP to retain customers.

Low Switching Costs for Modular Systems

Modern industrial PCs use modular compute-on-module standards (e.g., COM Express, SMARC) so customers can swap modules without redesigning systems, lowering switching costs and raising buyer power against VIA Technologies.

This modularity lets buyers shift to rivals; industry data show embedded module market grew 6.8% in 2024 to $3.9B, increasing supplier options and price pressure on VIA.

As a result, VIA must keep service SLAs, rapid firmware updates, and competitive pricing—else risk losing long-term OEM contracts that often represent 20–40% of revenue per customer.

Demand for Integrated Software Solutions

Buyers now prefer hardware bundled with AI and computer vision software, pushing demand for plug-and-play industrial AI; in 2024, global edge AI software revenue hit about $4.6B, up 28% year-over-year, so VIA must offer integrated stacks not just chips.

VIA’s competitiveness hinges on delivering end-to-end solutions, including deployment support and model updates, or risk losing deals to firms that bundle software and services with similar silicon.

- Edge AI software market ~ $4.6B (2024, +28% YoY)

- Buyers seek integrated bundles, not raw silicon

- VIA needs plug-and-play AI + support to win industrial deals

Price Sensitivity in IoT Markets

Mass-market IoT buyers are highly price sensitive; a 1–3% unit-cost gap can sway OEM choices, and global IoT device average selling price fell ~6% in 2024 to about $18 per unit, intensifying pressure on margins.

Customers use strong competition—Qualcomm, MediaTek, NXP, Realtek—to force price concessions; chip industry gross margins averaged ~30% in 2024, but mass-IoT segments often sit below 20%.

VIA must tilt toward higher-margin verticals (industrial, medical) while accepting thin margins in consumer IoT to keep volume and scale.

- 1–3% unit-cost sensitivity

- IoT ASP ≈ $18 in 2024 (−6% YoY)

- Chip gross margins: industry ~30%, mass-IoT <20%

- Strategy: pursue specialized apps for margin

Buyer Power & ARM/RISC‑V Shift Compress VIA's Margins Amid Edge‑AI Stack Demand

Large enterprise buyers give VIA high bargaining power—top clients can drive 15–30% revenue swings and force 5–10ppt margin cuts; embedded customers’ modular standards and ARM/RISC-V adoption (70% of new IoT silicon, 2024) raise switching risk. Edge AI software growth ($4.6B, +28% YoY, 2024) means buyers prefer integrated stacks; price sensitivity (IoT ASP ≈ $18, −6% YoY) compresses mass-market margins.

| Metric | 2024 |

|---|---|

| Top-client revenue swing | 15–30% |

| ARM/RISC-V share | ≈70% |

| Edge AI software | $4.6B (+28%) |

| IoT ASP | $18 (−6%) |

Same Document Delivered

VIA Technologies Porter's Five Forces Analysis

This preview shows the exact VIA Technologies Porter's Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.