Vibra Energia Boston Consulting Group Matrix

Download Your Competitive Advantage

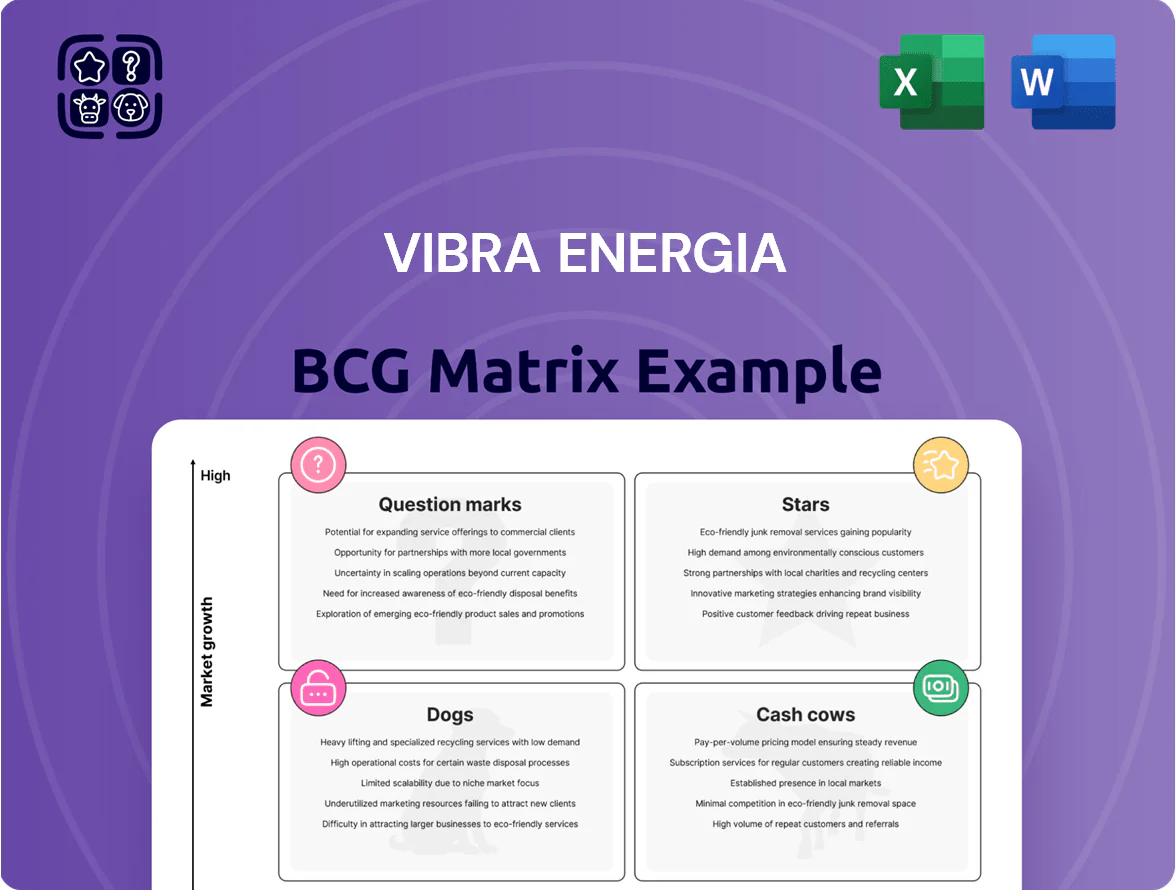

Vibra Energia’s BCG Matrix preview highlights shifting market shares across fuel distribution, lubricants, and renewable initiatives—showing potential Stars in renewables, Cash Cows in core fuel logistics, and Question Marks where new mobility bets need scale. This snapshot flags where capital allocation and divestment choices matter most for margin and growth. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Renewable Energy Solutions

Vibra Energia, via its Comerc Energia JV, has rapidly scaled distributed generation and energy management, capturing an estimated 28% market share in Brazil’s commercial solar contracts by Q4 2025 and adding ~420 MW of capacity since 2023.

Electric Vehicle Charging Infrastructure

Vibra Energia is rapidly scaling Vibra Move, its EV charging network, targeting urban Brazilian centers where EV registrations grew ~85% in 2024 to ~165k units nationwide (ANFAVEA).

The market is early-stage with projected CAGR >40% through 2030, demanding heavy tech and site investment to lock first-mover station density.

Vibra leverages ~13k retail points and logistics sites to secure share before competitors match density, cutting unit economics and rollout time.

Success preserves brand relevance as Brazil shifts from combustion: by 2025 each additional charger could lift forecourt revenue per site by an estimated 6–10%.

B2B Energy Management Services

Targeting large industrial and commercial clients, Vibra Energia’s B2B Energy Management Services offers efficiency audits and customized supply contracts, tapping a market where corporate energy spend rose ~9% in Brazil in 2024 and large users account for ~40% of commercial electricity consumption.

The segment is growing due to stricter ESG mandates and rising electricity costs, with projected CAGR ~12% for energy management services in LATAM through 2027, boosting demand for specialized expertise.

Leveraging existing corporate relationships, Vibra captures significant share of consultancy and services, reporting ~R$380m in related revenue in 2024 and cross-sell rates near 22%.

To stay ahead of boutique firms, Vibra must keep innovating digital monitoring tools—real-time telemetry and AI analytics—since vendors with advanced platforms see 15–20% higher client retention.

Sustainable Aviation Fuel (SAF)

Vibra Energia is positioning to lead Brazil’s sustainable aviation fuel (SAF) market by partnering with global producers to serve international airlines; Brazil handled 2.5% of world jet fuel in 2024, and SAF commitments to 2030 are growing 30% annually.

The niche offers high growth and barriers: ICAO and EU SAF mandates tighten emissions rules, creating premium pricing 20–40% above conventional jet fuel and long-term offtake opportunities.

Vibra is investing in logistics, storage, and ISCC Plus certification to secure supply chains and target a dominant share of Brazil’s nascent SAF market despite high upfront capital.

Strategic pivot: capital-intensive now, SAF aims to future-proof Vibra’s aviation unit as airline SAF blending mandates rise; expect multi-year payback tied to offtake contracts and carbon credit revenue.

- Brazil SAF demand growth ~30% CAGR to 2030

- SAF premium pricing 20–40% vs jet A1

- ISCC Plus and logistics focus to capture market

- High capex, multi-year payback, strong regulatory tailwinds

Biomethane and Green Hydrogen

Vibra is scaling into biomethane and green hydrogen via partnerships and biogas plant investments, targeting industrial and heavy-transport demand that grew ~35% in Brazil’s interior in 2024.

Its nationwide logistics and 1,200+ distribution sites (2025) give a share advantage over local producers, but capex of R$500–800m per 50 ktpa is needed to scale production and grid integration.

- High-growth market: ~35% demand rise (2024)

- Distribution edge: 1,200+ sites (2025)

- Capex need: R$500–800m / 50 ktpa

- Use case: heavy transport + industry

Vibra's 2024–25 Growth Surge: Solar +420MW, EVs +85%, R$380M Services, SAF Boom

Vibra’s Stars: strong 2024–25 growth in commercial solar (28% share, +420 MW since 2023), EV charging (Vibra Move; EVs +85% in 2024 to ~165k), B2B energy services (R$380m revenue in 2024, 22% cross-sell), and SAF push (Brazil SAF demand +30% CAGR to 2030; SAF premium 20–40%).

| Asset | Key metric | 2024–25 |

|---|---|---|

| Commercial solar | Market share / added MW | 28% / +420 MW |

| EV charging | EV fleet / growth | 165k units / +85% |

| Energy services | Revenue / cross-sell | R$380m / 22% |

| SAF | Demand CAGR / premium | ~30% / 20–40% |

What is included in the product

Concise BCG Matrix analysis of Vibra Energia’s units with strategic moves: invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG matrix placing Vibra Energia units into quadrants for quick portfolio clarity and executive decision-making.

Cash Cows

Retail Fuel Distribution

Vibra Energia runs Brazil’s largest service-station network with ~6,500 sites (2025), delivering steady cash from gasoline/diesel retail; retail fuels contributed ~65% of 2024 consolidated EBITDA (BRL 7.8bn) and ~BRL 3.2bn free cash flow.

The market is mature and consolidated, so Vibra prioritizes operational efficiency and cost cuts over expansion; retail fuels fund dividends and capex into renewables, and the segment’s dominant share boosts bargaining power with refineries and logistics partners.

Lubricants via Lubrax Brand

Lubrax is Brazil’s market leader in lubricants, holding roughly 30% national market share in 2024 with top-of-mind brand recognition and a distribution network covering 95% of fuel stations and major industrial clients.

The domestic lubricants market is mature and stable, with ~2% annual volume growth and gross margins near 40% in 2024, lowering the need for big marketing spend.

Lubrax produced ~BRL 1.2 billion operating cash flow in 2024, driven by scale manufacturing and integrated supply chains, funding Vibra Energia’s energy-transition investments.

B2B Diesel Supply

Supplying diesel to agriculture, mining and transport is a cash cow for Vibra Energia, generating about BRL 9.2bn in 2024 sales (~42% of total) thanks to Brazil’s commodity cycle and long-term supply contracts.

Market is mature with Vibra holding ~28% national B2B diesel share in 2024; volumes are stable and infrastructure largely fully depreciated, so margins convert to operating cash flow.

Low incremental capex needs (≈BRL 120m maintenance capex in 2024) sustain free cash flow, funding investments and dividends across the group.

Aviation Fuel Supply (Jet A-1)

Vibra Energia dominates Brazilian aviation fuel (Jet A-1), supplying major hubs and international carriers with >95% on-time delivery; this high reliability underpins steady volumes tied to GDP and tourism recovery—air traffic rose 18% in 2024 vs 2023 per ANAC.

High infrastructure barriers and long-term contracts keep entry costs steep, so the unit generates predictable cash rather than requiring heavy new capex; aviation fuel contributed ~22% of consolidated EBITDA in 2024 (Vibra reported BRL 1.8bn EBITDA contribution).

The company keeps market share via logistical excellence—integrated storage, pipeline access, and 24/7 operations—holding stable margins despite fuel price swings; average segment EBITDA margin ~28% in 2024.

- Dominant share; >95% on-time delivery

- Air traffic +18% in 2024 (ANAC)

- Aviation fuel ≈22% of EBITDA (BRL 1.8bn) in 2024

- EBITDA margin ~28%; low incremental capex

Convenience Stores (BR Mania)

The BR Mania franchise network, one of Brazil’s largest convenience chains with over 2,400 outlets as of 2025, delivers high-margin non-fuel sales anchored to Vibra Energia service stations, driving steady royalty and supply income while needing minimal parent capital due to franchising.

Its mature model leverages fuel-driven foot traffic to boost share of wallet, contributing an estimated 20–25% of station gross profit in 2024 and reinforcing the station ecosystem with low operational risk.

- ~2,400 outlets (2025)

- 20–25% of station gross profit (2024)

- Franchise model: low capex for Vibra

- Steady royalty + supply revenue stream

- Focus: maximize customer share of wallet

Vibra’s cash cows: Retail 65% EBITDA, Lubrax leader, B2B & Aviação driving strong cashflow

Vibra’s cash cows: retail fuels (~65% of 2024 EBITDA; BRL 7.8bn), Lubrax lubricants (~30% market share; OCF ≈BRL 1.2bn in 2024), B2B diesel (~BRL 9.2bn sales; ~28% B2B share), aviation fuel (~22% EBITDA ≈BRL 1.8bn; on‑time >95%), BR Mania (~2,400 outlets, 20–25% station gross profit).

| Unit | Key 2024/2025 |

|---|---|

| Retail | 65% EBITDA; BRL 7.8bn |

| Lubrax | 30% MS; BRL 1.2bn OCF |

| B2B diesel | BRL 9.2bn sales |

| Aviation | 22% EBITDA; BRL 1.8bn |

| BR Mania | 2,400 outlets (2025) |

Preview = Final Product

Vibra Energia BCG Matrix

The file you're previewing is the exact Vibra Energia BCG Matrix you'll receive after purchase—no watermarks, no demo elements—just a polished, analysis-ready report crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Vibra Energia’s BCG Matrix preview highlights shifting market shares across fuel distribution, lubricants, and renewable initiatives—showing potential Stars in renewables, Cash Cows in core fuel logistics, and Question Marks where new mobility bets need scale. This snapshot flags where capital allocation and divestment choices matter most for margin and growth. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Renewable Energy Solutions

Vibra Energia, via its Comerc Energia JV, has rapidly scaled distributed generation and energy management, capturing an estimated 28% market share in Brazil’s commercial solar contracts by Q4 2025 and adding ~420 MW of capacity since 2023.

Electric Vehicle Charging Infrastructure

Vibra Energia is rapidly scaling Vibra Move, its EV charging network, targeting urban Brazilian centers where EV registrations grew ~85% in 2024 to ~165k units nationwide (ANFAVEA).

The market is early-stage with projected CAGR >40% through 2030, demanding heavy tech and site investment to lock first-mover station density.

Vibra leverages ~13k retail points and logistics sites to secure share before competitors match density, cutting unit economics and rollout time.

Success preserves brand relevance as Brazil shifts from combustion: by 2025 each additional charger could lift forecourt revenue per site by an estimated 6–10%.

B2B Energy Management Services

Targeting large industrial and commercial clients, Vibra Energia’s B2B Energy Management Services offers efficiency audits and customized supply contracts, tapping a market where corporate energy spend rose ~9% in Brazil in 2024 and large users account for ~40% of commercial electricity consumption.

The segment is growing due to stricter ESG mandates and rising electricity costs, with projected CAGR ~12% for energy management services in LATAM through 2027, boosting demand for specialized expertise.

Leveraging existing corporate relationships, Vibra captures significant share of consultancy and services, reporting ~R$380m in related revenue in 2024 and cross-sell rates near 22%.

To stay ahead of boutique firms, Vibra must keep innovating digital monitoring tools—real-time telemetry and AI analytics—since vendors with advanced platforms see 15–20% higher client retention.

Sustainable Aviation Fuel (SAF)

Vibra Energia is positioning to lead Brazil’s sustainable aviation fuel (SAF) market by partnering with global producers to serve international airlines; Brazil handled 2.5% of world jet fuel in 2024, and SAF commitments to 2030 are growing 30% annually.

The niche offers high growth and barriers: ICAO and EU SAF mandates tighten emissions rules, creating premium pricing 20–40% above conventional jet fuel and long-term offtake opportunities.

Vibra is investing in logistics, storage, and ISCC Plus certification to secure supply chains and target a dominant share of Brazil’s nascent SAF market despite high upfront capital.

Strategic pivot: capital-intensive now, SAF aims to future-proof Vibra’s aviation unit as airline SAF blending mandates rise; expect multi-year payback tied to offtake contracts and carbon credit revenue.

- Brazil SAF demand growth ~30% CAGR to 2030

- SAF premium pricing 20–40% vs jet A1

- ISCC Plus and logistics focus to capture market

- High capex, multi-year payback, strong regulatory tailwinds

Biomethane and Green Hydrogen

Vibra is scaling into biomethane and green hydrogen via partnerships and biogas plant investments, targeting industrial and heavy-transport demand that grew ~35% in Brazil’s interior in 2024.

Its nationwide logistics and 1,200+ distribution sites (2025) give a share advantage over local producers, but capex of R$500–800m per 50 ktpa is needed to scale production and grid integration.

- High-growth market: ~35% demand rise (2024)

- Distribution edge: 1,200+ sites (2025)

- Capex need: R$500–800m / 50 ktpa

- Use case: heavy transport + industry

Vibra's 2024–25 Growth Surge: Solar +420MW, EVs +85%, R$380M Services, SAF Boom

Vibra’s Stars: strong 2024–25 growth in commercial solar (28% share, +420 MW since 2023), EV charging (Vibra Move; EVs +85% in 2024 to ~165k), B2B energy services (R$380m revenue in 2024, 22% cross-sell), and SAF push (Brazil SAF demand +30% CAGR to 2030; SAF premium 20–40%).

| Asset | Key metric | 2024–25 |

|---|---|---|

| Commercial solar | Market share / added MW | 28% / +420 MW |

| EV charging | EV fleet / growth | 165k units / +85% |

| Energy services | Revenue / cross-sell | R$380m / 22% |

| SAF | Demand CAGR / premium | ~30% / 20–40% |

What is included in the product

Concise BCG Matrix analysis of Vibra Energia’s units with strategic moves: invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG matrix placing Vibra Energia units into quadrants for quick portfolio clarity and executive decision-making.

Cash Cows

Retail Fuel Distribution

Vibra Energia runs Brazil’s largest service-station network with ~6,500 sites (2025), delivering steady cash from gasoline/diesel retail; retail fuels contributed ~65% of 2024 consolidated EBITDA (BRL 7.8bn) and ~BRL 3.2bn free cash flow.

The market is mature and consolidated, so Vibra prioritizes operational efficiency and cost cuts over expansion; retail fuels fund dividends and capex into renewables, and the segment’s dominant share boosts bargaining power with refineries and logistics partners.

Lubricants via Lubrax Brand

Lubrax is Brazil’s market leader in lubricants, holding roughly 30% national market share in 2024 with top-of-mind brand recognition and a distribution network covering 95% of fuel stations and major industrial clients.

The domestic lubricants market is mature and stable, with ~2% annual volume growth and gross margins near 40% in 2024, lowering the need for big marketing spend.

Lubrax produced ~BRL 1.2 billion operating cash flow in 2024, driven by scale manufacturing and integrated supply chains, funding Vibra Energia’s energy-transition investments.

B2B Diesel Supply

Supplying diesel to agriculture, mining and transport is a cash cow for Vibra Energia, generating about BRL 9.2bn in 2024 sales (~42% of total) thanks to Brazil’s commodity cycle and long-term supply contracts.

Market is mature with Vibra holding ~28% national B2B diesel share in 2024; volumes are stable and infrastructure largely fully depreciated, so margins convert to operating cash flow.

Low incremental capex needs (≈BRL 120m maintenance capex in 2024) sustain free cash flow, funding investments and dividends across the group.

Aviation Fuel Supply (Jet A-1)

Vibra Energia dominates Brazilian aviation fuel (Jet A-1), supplying major hubs and international carriers with >95% on-time delivery; this high reliability underpins steady volumes tied to GDP and tourism recovery—air traffic rose 18% in 2024 vs 2023 per ANAC.

High infrastructure barriers and long-term contracts keep entry costs steep, so the unit generates predictable cash rather than requiring heavy new capex; aviation fuel contributed ~22% of consolidated EBITDA in 2024 (Vibra reported BRL 1.8bn EBITDA contribution).

The company keeps market share via logistical excellence—integrated storage, pipeline access, and 24/7 operations—holding stable margins despite fuel price swings; average segment EBITDA margin ~28% in 2024.

- Dominant share; >95% on-time delivery

- Air traffic +18% in 2024 (ANAC)

- Aviation fuel ≈22% of EBITDA (BRL 1.8bn) in 2024

- EBITDA margin ~28%; low incremental capex

Convenience Stores (BR Mania)

The BR Mania franchise network, one of Brazil’s largest convenience chains with over 2,400 outlets as of 2025, delivers high-margin non-fuel sales anchored to Vibra Energia service stations, driving steady royalty and supply income while needing minimal parent capital due to franchising.

Its mature model leverages fuel-driven foot traffic to boost share of wallet, contributing an estimated 20–25% of station gross profit in 2024 and reinforcing the station ecosystem with low operational risk.

- ~2,400 outlets (2025)

- 20–25% of station gross profit (2024)

- Franchise model: low capex for Vibra

- Steady royalty + supply revenue stream

- Focus: maximize customer share of wallet

Vibra’s cash cows: Retail 65% EBITDA, Lubrax leader, B2B & Aviação driving strong cashflow

Vibra’s cash cows: retail fuels (~65% of 2024 EBITDA; BRL 7.8bn), Lubrax lubricants (~30% market share; OCF ≈BRL 1.2bn in 2024), B2B diesel (~BRL 9.2bn sales; ~28% B2B share), aviation fuel (~22% EBITDA ≈BRL 1.8bn; on‑time >95%), BR Mania (~2,400 outlets, 20–25% station gross profit).

| Unit | Key 2024/2025 |

|---|---|

| Retail | 65% EBITDA; BRL 7.8bn |

| Lubrax | 30% MS; BRL 1.2bn OCF |

| B2B diesel | BRL 9.2bn sales |

| Aviation | 22% EBITDA; BRL 1.8bn |

| BR Mania | 2,400 outlets (2025) |

Preview = Final Product

Vibra Energia BCG Matrix

The file you're previewing is the exact Vibra Energia BCG Matrix you'll receive after purchase—no watermarks, no demo elements—just a polished, analysis-ready report crafted for strategic clarity and professional presentation.