Vicat PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate Vicat’s future with our concise PESTLE snapshot—spot regulatory threats, environmental pressures, and market opportunities shaping cement and construction materials. Ideal for investors and strategists, this ready-to-use analysis saves time and informs smarter decisions. Purchase the full PESTLE for a detailed, editable breakdown and actionable insights you can apply immediately.

Political factors

Geopolitical stability in emerging markets

Vicat's operations in West Africa, Egypt and Kazakhstan expose it to geopolitical risks that can disrupt cement production and logistics; in 2024 these regions accounted for roughly 18% of consolidated revenue, making stability crucial. By end-2025 shifts in government policy and regional security incidents require strengthened asset protection and diversified supply routes to mitigate potential EBITDA volatility. Investors watch repatriation limits and export restrictions that could affect free cash flow and ROE.

EU Carbon Border Adjustment Mechanism implementation

The EU Carbon Border Adjustment Mechanism full implementation by late 2025 levels the playing field for Vicat in Europe by taxing imports priced on carbon intensity, protecting European cement producers who cut emissions; EU estimates suggest CBAM could cover 10–15% of emissions in affected sectors and raise import costs by €20–€60/tCO2e. This supports industrial sovereignty and benefits Vicat, which reported Scope 1+2 emissions reductions of ~18% between 2015–2023, while forcing continent-wide green investment to meet CBAM-adjusted price competitiveness.

Infrastructure spending and government stimulus

Government-led infrastructure packages in the US (Bipartisan Infrastructure Law, $1.2 trillion through 2026) and France (France 2030 and local urban renewal funds, €100+ billion commitments) remain primary drivers of cement demand in 2025, supporting global volumetric growth. Political decisions on public works funding and urban renewal create a stable backlog for Vicat's ready-mix and aggregates, with French operations benefiting from a ~15% revenue share tied to public projects. Strategic alignment with state-funded initiatives is crucial for long-term revenue forecasting and capacity planning in developed markets, as 2024–25 public construction spending rose 6–8% YOY.

Trade policies and protectionist measures

Increasing protectionist policies have raised tariffs on construction materials; for example, U.S. average applied tariffs on cement-related imports rose to 6.2% in 2024, increasing clinker sourcing costs for Vicat and reducing export margins.

Vicat faces divergent local content rules and tariff bands across Asia and North America—Asian markets often impose 5–15% duties while North American measures and antidumping probes have effectively limited exports since 2023.

These political barriers reshape cross-border logistics viability and competitive positioning: restricted exports of surplus clinker can reduce utilization and press mid-2025 EBITDA margins by several percentage points for international peers.

- Tariffs: U.S. ~6.2% (2024); Asia 5–15%

- Antidumping/local content constraints limiting exports since 2023

- Potential EBITDA pressure in 2025 from constrained clinker exports

Regulatory pressure on industrial decarbonization

- EU ETS ~€80–€100/t (2024–25) pressure on cement margins

- Vicat: 15% CO2 reduction vs 2019 (2024)

- Targets: clinker CO2 intensity cuts ~20–30% by 2025

- Subsidies/permits tied to measurable emission reductions

Vicat: 18% geopolitics, carbon costs rise, tariffs risk 2025 EBITDA hit

Geopolitical exposure: West Africa/Egypt/Kazakhstan ≈18% revenue (2024); export/repatriation risks. CBAM impact: €20–€60/tCO2e; EU ETS €80–€100/t (2024–25). Public demand: US $1.2tn infra (through 2026); France €100bn+; public projects ≈15% Vicat revenue. Tariffs/AD: US ~6.2% (2024); Asia 5–15%; constrained clinker exports may depress 2025 EBITDA.

| Metric | Value |

|---|---|

| Revenue exposure (2024) | ~18% |

| EU ETS price (2024–25) | €80–€100/t |

| CBAM import price effect | €20–€60/tCO2e |

| Public projects share | ~15% |

| Tariffs | US 6.2% / Asia 5–15% |

What is included in the product

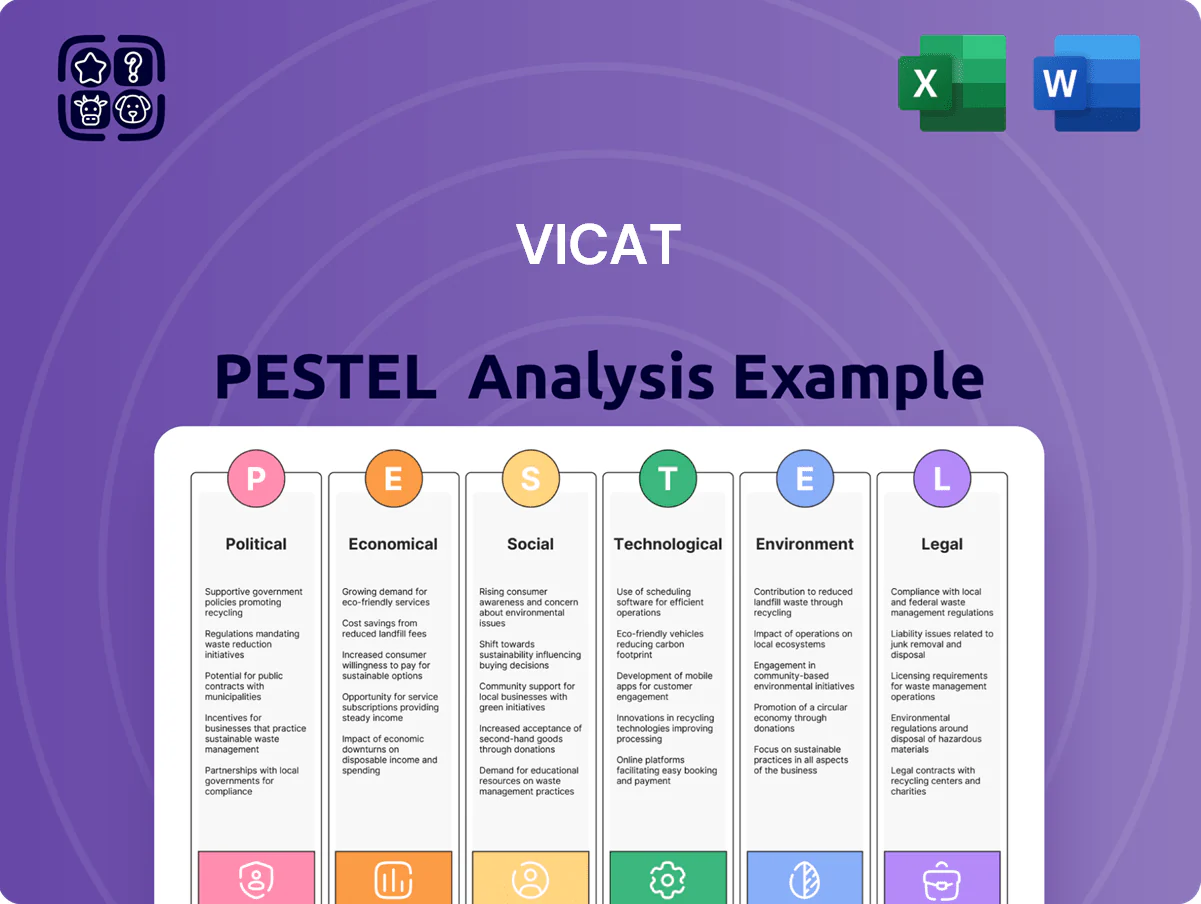

Explores how external macro-environmental factors uniquely affect Vicat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, support scenario planning, and inform investors, executives, and consultants with ready-to-use insights tailored to Vicat’s industry and regional dynamics.

Condenses Vicat's full PESTLE into a sharp, shareable brief that teams can drop into presentations or planning packs for fast alignment on external risks and market positioning.

Economic factors

Impact of high interest rates on construction

The prolonged environment of elevated interest rates through 2025 has tempered residential real estate growth in Europe and North America, with EU mortgage rates averaging ~3.5–4.0% and US 30-year mortgage near 6.7% in 2024–25, reducing new housing starts by ~10% vs 2019–21 peaks. Higher borrowing costs for developers and homebuyers slow new housing starts, directly lowering Vicat's cement and concrete volumes—France and US markets account for ~35% of group sales. Analysts monitor Vicat's net debt/EBITDA (around 2.0x in 2024) and capex discipline (€200–€250m guidance) to assess resilience in this restrictive monetary climate.

Energy price volatility and fuel transition

Energy remains one of Vicat’s largest variable costs—electricity and thermal fuels drove ~18% of 2024 COGS, with European gas prices swinging 45% year-on-year and industrial electricity up ~22% in 2023–24, compressing margins.

The group’s resilience depends on substituting fossil fuels with waste-derived fuels: Vicat reported 24% alternative fuel use in 2024 versus 16% in 2021, lowering thermal energy costs by an estimated €6–8/t clinker.

By end-2025, cement economic viability hinges on energy efficiency gains and hedging: a 5% improvement in specific energy consumption can offset a ~€3/t cement increase from fuel price spikes, making utility cost management critical.

Currency fluctuation and exchange rate risk

As an international group, Vicat faces currency translation risk from the Egyptian pound (EGP), Turkish lira (TRY) and West African CFA franc (XOF); between 2023–2025 EGP weakened ~20% vs EUR, TRY volatility exceeded 40% annual swings and XOF remained pegged but tied to EUR exposure, all of which can erode reported Euro-zone earnings despite strong local EBITDA.

Mitigation requires sophisticated hedging and natural offsets: Vicat reported FX sensitivity in 2024 noting potential EUR-reported EBITDA swings of several percentage points; active use of forwards, currency swaps and centralized treasury can protect shareholder value in the Eurozone.

Urbanization trends in developing economies

Rapid urbanization in India (urban population projected to reach 40% by 2030) and Senegal (urbanization ~46% in 2025) provides Vicat a structural demand boost for cement and aggregates, supporting revenue growth despite slower EU volumes.

Demand for affordable housing and basic infrastructure in these markets—India housing shortage ~25 million units (2024 estimate), Senegal urban infrastructure investment rising ~6% annually—creates higher-margin opportunities that offset mature-market stagnation.

Geographic diversification into high-growth Africa and South Asia helped Vicat limit regional exposure: in 2024, international operations contributed roughly 45% of group sales, balancing localized downturns.

- India urbanization ~40% by 2030; housing gap ~25M units (2024)

- Senegal urban pop ~46% (2025); infrastructure spend +6% YoY

- Vicat: ~45% sales from international markets (2024)

Inflationary pressures on raw materials

Persistent inflation across cement feedstocks, energy and freight raised input costs ~8-12% y/y in 2024; global logistics rates remained elevated into 2025, squeezing margins.

Vicat's ability to raise average cement prices by ~6-9% in 2024 signaled some pricing power, but full pass-through is uneven across regions.

Maintaining EBITDA margins near 14-16% requires strict cost controls, efficiency gains and tighter vertical-integration synergies.

- Raw material & energy inflation ~8-12% (2024)

- Price increases realized ~6-9% (2024)

- Target EBITDA margin range 14-16%

Cement resilience: 2.0x net debt, €200–250m capex; margins pressured by energy/feedstock

Higher rates dampen EU/US housing starts (~-10% vs 2019–21) reducing volumes; net debt/EBITDA ~2.0x (2024) and capex €200–€250m guide resilience. Energy (18% COGS) and feedstock inflation (+8–12% 2024) pressure margins; alt fuels at 24% (2024) cut ~€6–8/t clinker. International sales ~45% (2024) offset mature-market weakness; India housing gap ~25M (2024), Senegal urban ~46% (2025).

| Metric | 2024/25 |

|---|---|

| Net debt/EBITDA | ~2.0x |

| Capex guidance | €200–€250m |

| Energy share COGS | ~18% |

| Alt fuel use | 24% |

| Intl sales | ~45% |

Same Document Delivered

Vicat PESTLE Analysis

The preview shown here is the exact Vicat PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate Vicat’s future with our concise PESTLE snapshot—spot regulatory threats, environmental pressures, and market opportunities shaping cement and construction materials. Ideal for investors and strategists, this ready-to-use analysis saves time and informs smarter decisions. Purchase the full PESTLE for a detailed, editable breakdown and actionable insights you can apply immediately.

Political factors

Geopolitical stability in emerging markets

Vicat's operations in West Africa, Egypt and Kazakhstan expose it to geopolitical risks that can disrupt cement production and logistics; in 2024 these regions accounted for roughly 18% of consolidated revenue, making stability crucial. By end-2025 shifts in government policy and regional security incidents require strengthened asset protection and diversified supply routes to mitigate potential EBITDA volatility. Investors watch repatriation limits and export restrictions that could affect free cash flow and ROE.

EU Carbon Border Adjustment Mechanism implementation

The EU Carbon Border Adjustment Mechanism full implementation by late 2025 levels the playing field for Vicat in Europe by taxing imports priced on carbon intensity, protecting European cement producers who cut emissions; EU estimates suggest CBAM could cover 10–15% of emissions in affected sectors and raise import costs by €20–€60/tCO2e. This supports industrial sovereignty and benefits Vicat, which reported Scope 1+2 emissions reductions of ~18% between 2015–2023, while forcing continent-wide green investment to meet CBAM-adjusted price competitiveness.

Infrastructure spending and government stimulus

Government-led infrastructure packages in the US (Bipartisan Infrastructure Law, $1.2 trillion through 2026) and France (France 2030 and local urban renewal funds, €100+ billion commitments) remain primary drivers of cement demand in 2025, supporting global volumetric growth. Political decisions on public works funding and urban renewal create a stable backlog for Vicat's ready-mix and aggregates, with French operations benefiting from a ~15% revenue share tied to public projects. Strategic alignment with state-funded initiatives is crucial for long-term revenue forecasting and capacity planning in developed markets, as 2024–25 public construction spending rose 6–8% YOY.

Trade policies and protectionist measures

Increasing protectionist policies have raised tariffs on construction materials; for example, U.S. average applied tariffs on cement-related imports rose to 6.2% in 2024, increasing clinker sourcing costs for Vicat and reducing export margins.

Vicat faces divergent local content rules and tariff bands across Asia and North America—Asian markets often impose 5–15% duties while North American measures and antidumping probes have effectively limited exports since 2023.

These political barriers reshape cross-border logistics viability and competitive positioning: restricted exports of surplus clinker can reduce utilization and press mid-2025 EBITDA margins by several percentage points for international peers.

- Tariffs: U.S. ~6.2% (2024); Asia 5–15%

- Antidumping/local content constraints limiting exports since 2023

- Potential EBITDA pressure in 2025 from constrained clinker exports

Regulatory pressure on industrial decarbonization

- EU ETS ~€80–€100/t (2024–25) pressure on cement margins

- Vicat: 15% CO2 reduction vs 2019 (2024)

- Targets: clinker CO2 intensity cuts ~20–30% by 2025

- Subsidies/permits tied to measurable emission reductions

Vicat: 18% geopolitics, carbon costs rise, tariffs risk 2025 EBITDA hit

Geopolitical exposure: West Africa/Egypt/Kazakhstan ≈18% revenue (2024); export/repatriation risks. CBAM impact: €20–€60/tCO2e; EU ETS €80–€100/t (2024–25). Public demand: US $1.2tn infra (through 2026); France €100bn+; public projects ≈15% Vicat revenue. Tariffs/AD: US ~6.2% (2024); Asia 5–15%; constrained clinker exports may depress 2025 EBITDA.

| Metric | Value |

|---|---|

| Revenue exposure (2024) | ~18% |

| EU ETS price (2024–25) | €80–€100/t |

| CBAM import price effect | €20–€60/tCO2e |

| Public projects share | ~15% |

| Tariffs | US 6.2% / Asia 5–15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vicat across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, support scenario planning, and inform investors, executives, and consultants with ready-to-use insights tailored to Vicat’s industry and regional dynamics.

Condenses Vicat's full PESTLE into a sharp, shareable brief that teams can drop into presentations or planning packs for fast alignment on external risks and market positioning.

Economic factors

Impact of high interest rates on construction

The prolonged environment of elevated interest rates through 2025 has tempered residential real estate growth in Europe and North America, with EU mortgage rates averaging ~3.5–4.0% and US 30-year mortgage near 6.7% in 2024–25, reducing new housing starts by ~10% vs 2019–21 peaks. Higher borrowing costs for developers and homebuyers slow new housing starts, directly lowering Vicat's cement and concrete volumes—France and US markets account for ~35% of group sales. Analysts monitor Vicat's net debt/EBITDA (around 2.0x in 2024) and capex discipline (€200–€250m guidance) to assess resilience in this restrictive monetary climate.

Energy price volatility and fuel transition

Energy remains one of Vicat’s largest variable costs—electricity and thermal fuels drove ~18% of 2024 COGS, with European gas prices swinging 45% year-on-year and industrial electricity up ~22% in 2023–24, compressing margins.

The group’s resilience depends on substituting fossil fuels with waste-derived fuels: Vicat reported 24% alternative fuel use in 2024 versus 16% in 2021, lowering thermal energy costs by an estimated €6–8/t clinker.

By end-2025, cement economic viability hinges on energy efficiency gains and hedging: a 5% improvement in specific energy consumption can offset a ~€3/t cement increase from fuel price spikes, making utility cost management critical.

Currency fluctuation and exchange rate risk

As an international group, Vicat faces currency translation risk from the Egyptian pound (EGP), Turkish lira (TRY) and West African CFA franc (XOF); between 2023–2025 EGP weakened ~20% vs EUR, TRY volatility exceeded 40% annual swings and XOF remained pegged but tied to EUR exposure, all of which can erode reported Euro-zone earnings despite strong local EBITDA.

Mitigation requires sophisticated hedging and natural offsets: Vicat reported FX sensitivity in 2024 noting potential EUR-reported EBITDA swings of several percentage points; active use of forwards, currency swaps and centralized treasury can protect shareholder value in the Eurozone.

Urbanization trends in developing economies

Rapid urbanization in India (urban population projected to reach 40% by 2030) and Senegal (urbanization ~46% in 2025) provides Vicat a structural demand boost for cement and aggregates, supporting revenue growth despite slower EU volumes.

Demand for affordable housing and basic infrastructure in these markets—India housing shortage ~25 million units (2024 estimate), Senegal urban infrastructure investment rising ~6% annually—creates higher-margin opportunities that offset mature-market stagnation.

Geographic diversification into high-growth Africa and South Asia helped Vicat limit regional exposure: in 2024, international operations contributed roughly 45% of group sales, balancing localized downturns.

- India urbanization ~40% by 2030; housing gap ~25M units (2024)

- Senegal urban pop ~46% (2025); infrastructure spend +6% YoY

- Vicat: ~45% sales from international markets (2024)

Inflationary pressures on raw materials

Persistent inflation across cement feedstocks, energy and freight raised input costs ~8-12% y/y in 2024; global logistics rates remained elevated into 2025, squeezing margins.

Vicat's ability to raise average cement prices by ~6-9% in 2024 signaled some pricing power, but full pass-through is uneven across regions.

Maintaining EBITDA margins near 14-16% requires strict cost controls, efficiency gains and tighter vertical-integration synergies.

- Raw material & energy inflation ~8-12% (2024)

- Price increases realized ~6-9% (2024)

- Target EBITDA margin range 14-16%

Cement resilience: 2.0x net debt, €200–250m capex; margins pressured by energy/feedstock

Higher rates dampen EU/US housing starts (~-10% vs 2019–21) reducing volumes; net debt/EBITDA ~2.0x (2024) and capex €200–€250m guide resilience. Energy (18% COGS) and feedstock inflation (+8–12% 2024) pressure margins; alt fuels at 24% (2024) cut ~€6–8/t clinker. International sales ~45% (2024) offset mature-market weakness; India housing gap ~25M (2024), Senegal urban ~46% (2025).

| Metric | 2024/25 |

|---|---|

| Net debt/EBITDA | ~2.0x |

| Capex guidance | €200–€250m |

| Energy share COGS | ~18% |

| Alt fuel use | 24% |

| Intl sales | ~45% |

Same Document Delivered

Vicat PESTLE Analysis

The preview shown here is the exact Vicat PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and investment decisions.