Vicor Porter's Five Forces Analysis

From Overview to Strategy Blueprint

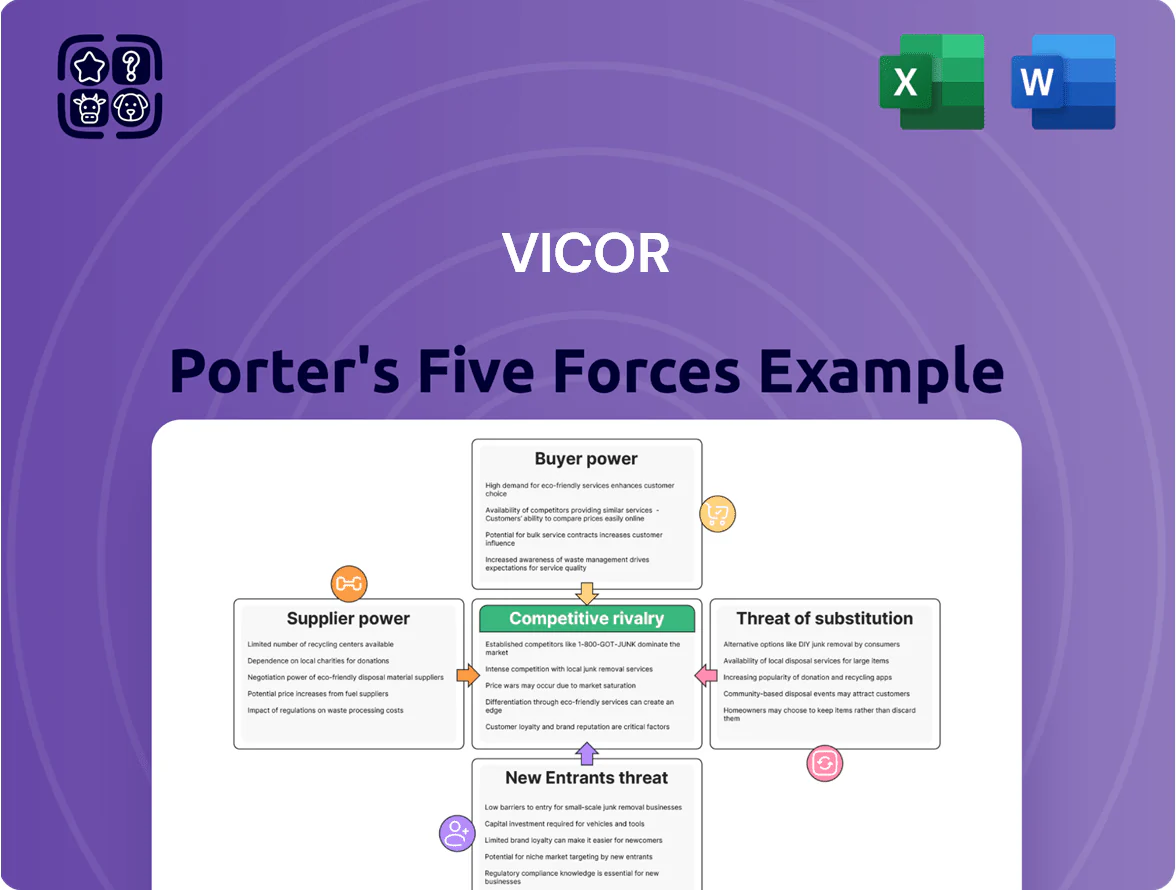

Vicor faces intense supplier and buyer dynamics driven by specialized power-conversion components and demanding OEM relationships, while moderate threat from new entrants is tempered by high engineering barriers and IP; substitutes and competitive rivalry hinge on innovation speed and cost-efficiency.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Vicor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Semiconductor Foundries

Vicor depends on a handful of advanced foundries—mainly TSMC, Samsung, and GlobalFoundries—that together control >70% of leading-node capacity; by Q4 2025 wafer lead times for specialty analog power processes averaged 18–26 weeks, giving suppliers strong pricing and schedule leverage.

Critical Raw Material Dependencies

Critical raw material dependencies: Vicor’s high-density power modules rely on rare earths (neodymium, praseodymium) and high-grade magnetic alloys for inductors; about 40–60% of global NdFeB (neodymium-iron-boron) supply was sourced from China in 2024, concentrating supplier power. Suppliers control refined supply chains and mining hubs, so a 10–20% disruption in rare-earth output can delay module production and degrade Vicor’s efficiency targets.

Proprietary Equipment Manufacturers

Vicor’s Converter housed in Package tech needs custom production machinery, so suppliers of proprietary equipment hold significant bargaining power; few vendors meet Vicor’s packaging specs, raising supplier concentration risk. In 2024 Vicor reported gross margin pressure tied to supply-chain costs, and long lead times (often 20+ weeks) force multiyear contracts and co-investments. Suppliers’ R&D cadence must match Vicor’s product roadmap or production bottlenecks and unit-cost increases follow.

High Switching Costs for Custom Components

Many of Vicor’s internal components are custom-designed to tight specs, raising switching costs; replacing a supplier risks redesign expenses and delays in certification for aerospace and automotive programs, where time-to-market matters and noncompliance can void contracts.

Suppliers thus gain leverage: Vicor’s 2024 product mix—over 40% revenue from high-reliability markets—means supplier hold-up can affect margins and delivery schedules, so suppliers can press for price or lead-time concessions.

- Custom parts: hard to replicate

- Redesign/certification delays: high cost

- 2024: ~40% revenue from aerospace/auto

- Suppliers can demand price/lead-time concessions

Impact of Global Logistics and Lead Times

- Consolidation raised premiums 12–18% (2024–2025)

- Expedited logistics add ~1.0–1.5% to Vicor COGS

- Priority-slot on-time availability down to ~82% by end-2025

Supplier concentration squeezes margins: foundries, China rare-earths, long lead times

Suppliers hold high bargaining power: >70% leading-node foundry control, 40–60% rare-earths from China (2024), 18–26 week wafer lead times (Q4 2025), logistics premiums +12–18% (2024–25) and expedited shipping adds ~1.0–1.5% COGS; supplier concentration forces multiyear contracts, co-investments, and raises redesign risk for aerospace/auto programs (~40% 2024 revenue).

| Metric | Value |

|---|---|

| Foundry control | >70% |

| Rare-earths from China (2024) | 40–60% |

| Wafer lead times (Q4 2025) | 18–26 wks |

| Logistics premium (2024–25) | +12–18% |

| Expedited COGS impact | +1.0–1.5% |

What is included in the product

Tailored exclusively for Vicor, this Porter’s Five Forces analysis uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and potential disruptors, with strategic commentary to inform pricing, profitability, and defensive or growth tactics.

Concise Porter's Five Forces snapshot for Vicor—one-sheet clarity to spot competitive pain points and prioritize strategic moves.

Customers Bargaining Power

Concentration of High-Volume Data Center Clients

Rigorous Certification and Qualification Standards

Customers in aerospace, defense, and automotive force Vicor to meet AS9100, DO-160, and ISO 26262 levels, raising testing and documentation costs—industry estimates put qualification runs at $250k–$1M per program.

This certification barrier limits new entrants but increases buyer leverage, since big OEMs can demand custom design changes and claim supply concessions; top 10 customers often account for >40% of revenue.

Low Switching Costs in Standardized Segments

In commoditized industrial power segments, low switching costs let buyers shift vendors quickly; in 2024 Vicor (NASDAQ: VICR) faces price-sensitive customers where alternatives undercut premium offerings by 10–30% on list price. If Vicor’s efficiency gains (often 1–3% system-level) don’t justify higher prices, customers move to standard DC-to-DC converters, pressuring margins and forcing ongoing R&D and product refreshes to defend a price premium.

Vertical Integration by Tech Giants

Major tech firms like Apple, Amazon, and Google are designing in-house power delivery for their chips, raising credible backward-integration threats that boost customer bargaining power.

Vicor must show its modular converters beat in-house builds on cost and time; a 2024 Intel/Google survey found 28% of hyperscalers planned vertical power design within 3 years, and developing in-house PDUs can cost $5–15M and 12–24 months.

Prove total cost of ownership savings, faster time-to-market, and IP protection to retain contracts.

- 28% hyperscalers planning in-house power (2024 survey)

- In-house dev: $5–15M, 12–24 months

- Vicor must show lower TCO and faster deployment

Price Sensitivity in Emerging EV Markets

As EV makers scale to mass-market, every powertrain component cost matters; in 2024 EV production grew ~40% YoY to 15.5M units, pushing buyers to demand price parity with legacy suppliers who make 50–70% lower per-unit costs from scale.

Vicor’s high-performance converters face margin pressure as OEMs leverage projected volumes to seek 10–25% price reductions from innovators; loss of contracts can cut revenue growth forecasts by similar percentages.

Concentrated Buyers & Hyperscalers Squeeze Prices—Top10 >40%, FY25 hyperscalers ~38%

| Metric | Value |

|---|---|

| Hyperscaler share (FY2025) | ~38% |

| Top10 rev share | >40% |

| Price cut demands | >15% YoY |

| Qualification cost | $250k–$1M |

| In-house PD plans (2024) | 28% |

| In-house dev cost/time | $5–15M, 12–24m |

| EV units (2024) | 15.5M |

| OEM price cut requests | 10–25% |

Preview the Actual Deliverable

Vicor Porter's Five Forces Analysis

This preview shows the exact Vicor Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Vicor faces intense supplier and buyer dynamics driven by specialized power-conversion components and demanding OEM relationships, while moderate threat from new entrants is tempered by high engineering barriers and IP; substitutes and competitive rivalry hinge on innovation speed and cost-efficiency.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Vicor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Semiconductor Foundries

Vicor depends on a handful of advanced foundries—mainly TSMC, Samsung, and GlobalFoundries—that together control >70% of leading-node capacity; by Q4 2025 wafer lead times for specialty analog power processes averaged 18–26 weeks, giving suppliers strong pricing and schedule leverage.

Critical Raw Material Dependencies

Critical raw material dependencies: Vicor’s high-density power modules rely on rare earths (neodymium, praseodymium) and high-grade magnetic alloys for inductors; about 40–60% of global NdFeB (neodymium-iron-boron) supply was sourced from China in 2024, concentrating supplier power. Suppliers control refined supply chains and mining hubs, so a 10–20% disruption in rare-earth output can delay module production and degrade Vicor’s efficiency targets.

Proprietary Equipment Manufacturers

Vicor’s Converter housed in Package tech needs custom production machinery, so suppliers of proprietary equipment hold significant bargaining power; few vendors meet Vicor’s packaging specs, raising supplier concentration risk. In 2024 Vicor reported gross margin pressure tied to supply-chain costs, and long lead times (often 20+ weeks) force multiyear contracts and co-investments. Suppliers’ R&D cadence must match Vicor’s product roadmap or production bottlenecks and unit-cost increases follow.

High Switching Costs for Custom Components

Many of Vicor’s internal components are custom-designed to tight specs, raising switching costs; replacing a supplier risks redesign expenses and delays in certification for aerospace and automotive programs, where time-to-market matters and noncompliance can void contracts.

Suppliers thus gain leverage: Vicor’s 2024 product mix—over 40% revenue from high-reliability markets—means supplier hold-up can affect margins and delivery schedules, so suppliers can press for price or lead-time concessions.

- Custom parts: hard to replicate

- Redesign/certification delays: high cost

- 2024: ~40% revenue from aerospace/auto

- Suppliers can demand price/lead-time concessions

Impact of Global Logistics and Lead Times

- Consolidation raised premiums 12–18% (2024–2025)

- Expedited logistics add ~1.0–1.5% to Vicor COGS

- Priority-slot on-time availability down to ~82% by end-2025

Supplier concentration squeezes margins: foundries, China rare-earths, long lead times

Suppliers hold high bargaining power: >70% leading-node foundry control, 40–60% rare-earths from China (2024), 18–26 week wafer lead times (Q4 2025), logistics premiums +12–18% (2024–25) and expedited shipping adds ~1.0–1.5% COGS; supplier concentration forces multiyear contracts, co-investments, and raises redesign risk for aerospace/auto programs (~40% 2024 revenue).

| Metric | Value |

|---|---|

| Foundry control | >70% |

| Rare-earths from China (2024) | 40–60% |

| Wafer lead times (Q4 2025) | 18–26 wks |

| Logistics premium (2024–25) | +12–18% |

| Expedited COGS impact | +1.0–1.5% |

What is included in the product

Tailored exclusively for Vicor, this Porter’s Five Forces analysis uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes, and potential disruptors, with strategic commentary to inform pricing, profitability, and defensive or growth tactics.

Concise Porter's Five Forces snapshot for Vicor—one-sheet clarity to spot competitive pain points and prioritize strategic moves.

Customers Bargaining Power

Concentration of High-Volume Data Center Clients

Rigorous Certification and Qualification Standards

Customers in aerospace, defense, and automotive force Vicor to meet AS9100, DO-160, and ISO 26262 levels, raising testing and documentation costs—industry estimates put qualification runs at $250k–$1M per program.

This certification barrier limits new entrants but increases buyer leverage, since big OEMs can demand custom design changes and claim supply concessions; top 10 customers often account for >40% of revenue.

Low Switching Costs in Standardized Segments

In commoditized industrial power segments, low switching costs let buyers shift vendors quickly; in 2024 Vicor (NASDAQ: VICR) faces price-sensitive customers where alternatives undercut premium offerings by 10–30% on list price. If Vicor’s efficiency gains (often 1–3% system-level) don’t justify higher prices, customers move to standard DC-to-DC converters, pressuring margins and forcing ongoing R&D and product refreshes to defend a price premium.

Vertical Integration by Tech Giants

Major tech firms like Apple, Amazon, and Google are designing in-house power delivery for their chips, raising credible backward-integration threats that boost customer bargaining power.

Vicor must show its modular converters beat in-house builds on cost and time; a 2024 Intel/Google survey found 28% of hyperscalers planned vertical power design within 3 years, and developing in-house PDUs can cost $5–15M and 12–24 months.

Prove total cost of ownership savings, faster time-to-market, and IP protection to retain contracts.

- 28% hyperscalers planning in-house power (2024 survey)

- In-house dev: $5–15M, 12–24 months

- Vicor must show lower TCO and faster deployment

Price Sensitivity in Emerging EV Markets

As EV makers scale to mass-market, every powertrain component cost matters; in 2024 EV production grew ~40% YoY to 15.5M units, pushing buyers to demand price parity with legacy suppliers who make 50–70% lower per-unit costs from scale.

Vicor’s high-performance converters face margin pressure as OEMs leverage projected volumes to seek 10–25% price reductions from innovators; loss of contracts can cut revenue growth forecasts by similar percentages.

Concentrated Buyers & Hyperscalers Squeeze Prices—Top10 >40%, FY25 hyperscalers ~38%

| Metric | Value |

|---|---|

| Hyperscaler share (FY2025) | ~38% |

| Top10 rev share | >40% |

| Price cut demands | >15% YoY |

| Qualification cost | $250k–$1M |

| In-house PD plans (2024) | 28% |

| In-house dev cost/time | $5–15M, 12–24m |

| EV units (2024) | 15.5M |

| OEM price cut requests | 10–25% |

Preview the Actual Deliverable

Vicor Porter's Five Forces Analysis

This preview shows the exact Vicor Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders or mockups.