Vietin Bank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

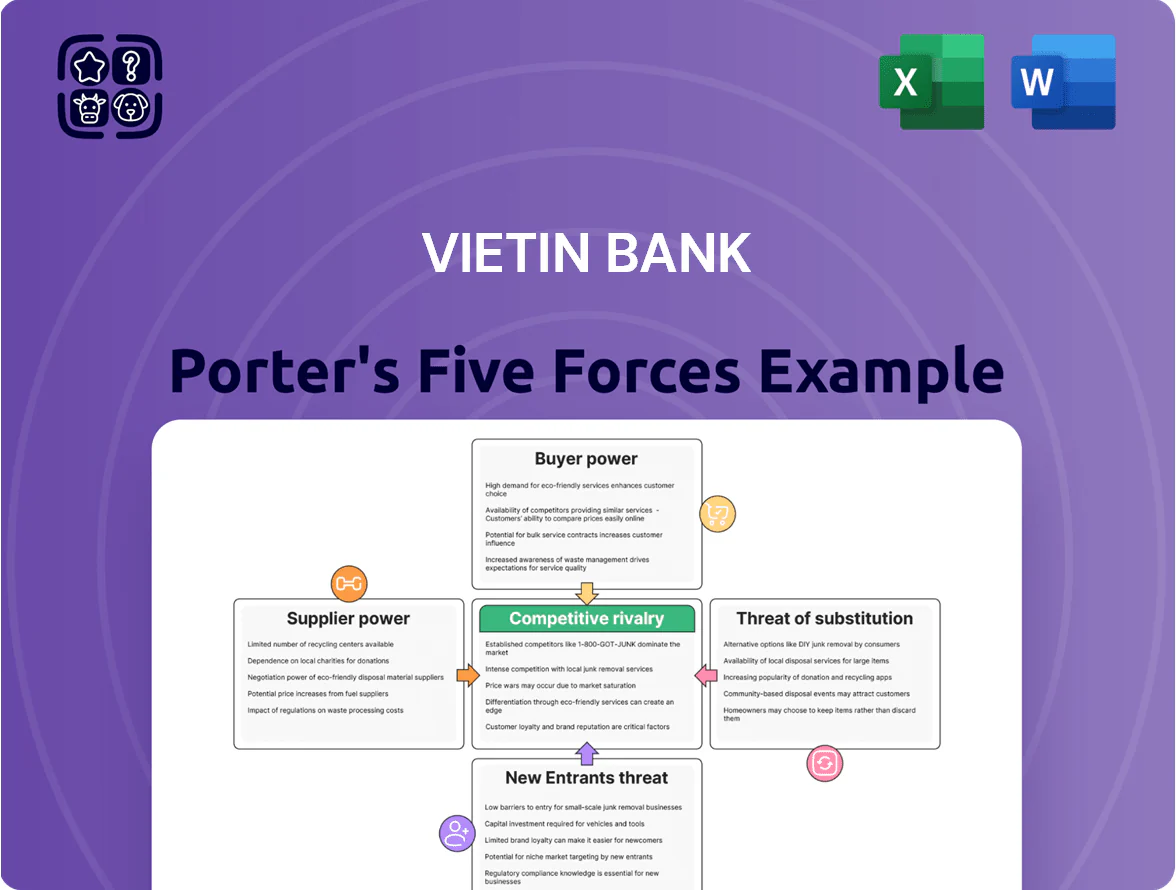

Vietin Bank faces moderate competitive rivalry driven by large state-owned peers and growing fintech disruption, while regulatory oversight and capital access temper both supplier and entrant threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vietin Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Individual and Corporate Depositors

Depositors are VietinBank’s primary capital suppliers and their bargaining power is moderate: by late 2025 Vietnam had about 50 licensed banks and retail deposit competition rose, so customers shop rates and apps.

VietinBank’s state-owned status adds trust—its market deposit share was ~12.5% in 2024—but depositors now react to small rate moves and app quality; retail churn rose after 2023 rate hikes.

To retain funds the bank must match top-tier deposit rates (market time deposit avg ~5.8% in 2025) and deliver seamless mobile banking; otherwise customers shift to private joint-stock banks with better digital UX.

The State Bank of Vietnam

As Vietnam’s central bank, the State Bank of Vietnam is the primary supplier of liquidity and regulator; by end-2025 it retains exceptionally high power over VietinBank via mandated reserve requirement ratio (RRR) changes and credit growth quotas—SBV set RRR at 3.0–4.5% in 2024 and tightened credit growth target to 14% for 2025, directly constraining VietinBank’s loan book expansion.

Technology and Infrastructure Providers

VietinBank depends on global and local tech firms for core banking, cybersecurity, and cloud services; switching major systems often costs >$50m and takes 12–24 months, so supplier power is high.

As VietinBank targets full digital transformation by 2026, reliance on specialist AI and data-analytics vendors grew; 2024 vendor spend rose ~18% to an estimated $120m, boosting suppliers’ strategic leverage.

Skilled Human Capital

The market for high-tier financial and IT talent in Vietnam is highly competitive, giving suppliers of skilled labor strong bargaining power; VietinBank faces rivals including BIDV, Techcombank, regional fintechs like GrabPay, and multinationals such as Standard Chartered.

This competition raised average fintech specialist salaries ~18% in 2024 and pushed VietinBank to boost pay, invest in upskilling, and revamp culture to limit turnover above the banking sector average of 12%.

- High competition: local banks, fintechs, MNCs

- Salary rise: ~18% for fintech/IT roles in 2024

- Sector turnover: ~12% in banking

- Action: higher pay, training, culture upgrades

International Capital Markets

VietinBank relies on international bondholders and strategic foreign investors to meet Basel III buffers and fund expansion; these suppliers wield high bargaining power by demanding transparency, ESG compliance, and investment-grade ratings.

In 2025 global markets, VietinBank needs a CET1 ratio near 10.5–11% and a Moody’s-equivalent Baa3/BBB- or better to secure lower spreads; recent offshore bond deals show spreads widening 50–120bp when ratings slip.

- High supplier power: demands for ESG, transparency, ratings

- Target CET1 ~10.5–11% in 2025

- Investment-grade needed to avoid +50–120bp spread

- International funding critical for Basel III compliance

VietinBank faces mixed supplier power: strong regulator and investors, moderate depositors

Supplier power over VietinBank is mixed: depositors' power is moderate (market deposit share ~12.5% in 2024; avg time deposit ~5.8% in 2025), SBV (regulator/liquidity) is very strong (RRR 3.0–4.5% in 2024; credit growth cap 14% for 2025), IT/vendors and global investors hold high leverage (2024 vendor spend ~$120m; CET1 target ~10.5–11% for 2025).

| Supplier | Power | Key metric |

|---|---|---|

| Depositors | Moderate | Deposit share 12.5%; time dep 5.8% |

| SBV | High | RRR 3.0–4.5%; credit cap 14% |

| IT vendors | High | Spend $120m (2024) |

| Intl investors | High | CET1 target 10.5–11% |

What is included in the product

Tailored Porter's Five Forces analysis for Vietin Bank, uncovering competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats to its market position.

A concise VietinBank Porter's Five Forces snapshot that highlights competitive threats and relief strategies—ideal for fast risk assessment and board-ready slides.

Customers Bargaining Power

Large State-Owned Enterprises

Large state-owned enterprises (SOEs) exert high bargaining power at VietinBank because their corporate deposits and lending needs account for roughly 30% of VietinBank’s corporate loan book (2024 annual report), enabling them to demand lower interest spreads and bespoke products unavailable to smaller clients.

Retail Banking Consumers

Individual retail customers gained notable bargaining power by late 2025 as digital comparison tools raised transparency and switching costs fell below $5 per transfer; a 2024 Kantar/Banking report showed 38% of Vietnamese users would switch banks within 12 months for better digital UX or rewards.

Digital-only banks captured 12% of new retail deposits in 2024, letting users move funds fast for higher cashback or better apps.

VietinBank counters by embedding banking into a lifestyle ecosystem—linking payments, e-commerce, and travel—and expanding loyalty tiers that raised monthly active wallet retention by 9% in 2025.

Small and Medium Enterprises

SMEs in Vietnam grew 4.5% in number in 2023 to ~1.2M firms, giving them moderate bargaining power as they can choose traditional banks or fintechs; market share of nonbank lenders rose to 12% of SME credit in 2024.

SMEs value speed and flexible collateral more than brand, so VietinBank automated credit scoring in 2024 to cut SME loan approval time from ~10 days to 48–72 hours for standard cases.

Institutional Investors and Asset Management

Institutional clients using VietinBank for custody and investment banking demand advanced reporting and risk controls; their leverage is high because institutional trades can represent over 20% of corporate banking fees and a single asset manager may move >$100m if service drops.

VietinBank must upgrade its investment banking platform and reporting—investing in real-time risk systems and ISO 20022-compatible feeds—to retain mandates against global custodians.

- High expectation: professional reporting, risk controls

- Power source: large ticket sizes, portability of mandates

- Financial weight: institutional flows >20% of fees

- Required action: real-time risk systems, ISO 20022 feeds

Export and Import Businesses

Vietnam’s trade-led economy (2024 exports + imports ~ US$857bn) gives export/import firms strong bargaining power for trade finance and FX services.

They can switch to global banks—HSBC, Standard Chartered—so VietinBank must use its 1,000+ branches and offer competitive FX spreads to retain them.

In 2024 corporates accounted for ~45% of VietinBank fee income, so losing clients would hit revenue materially.

- Trade volume: ~US$857bn (2024)

- VietinBank branches: 1,000+

- Corp fee share: ~45% (2024)

Powerful, Diverse Customer Bargaining: SOEs, Institutions, Retail & Trade Reshape Banking

Customers exert strong, varied bargaining power: SOEs and institutional mandates drive pricing (30% corporate loans; institutional flows >20% fees), SMEs and fintechs push for speed (SME loans cut to 48–72h), retail digital churn rose (38% willing to switch; digital banks took 12% new deposits in 2024), trade firms demand competitive FX (Vietnam trade ~US$857bn 2024).

| Segment | Key metric |

|---|---|

| SOEs | 30% corporate loans (2024) |

| Institutions | >20% fee flows |

| Retail | 38% switch; 12% deposits (2024) |

| Trade | US$857bn trade (2024) |

Full Version Awaits

Vietin Bank Porter's Five Forces Analysis

This preview shows the exact Vietin Bank Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders; the full document is fully formatted, comprehensive, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Vietin Bank faces moderate competitive rivalry driven by large state-owned peers and growing fintech disruption, while regulatory oversight and capital access temper both supplier and entrant threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vietin Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Individual and Corporate Depositors

Depositors are VietinBank’s primary capital suppliers and their bargaining power is moderate: by late 2025 Vietnam had about 50 licensed banks and retail deposit competition rose, so customers shop rates and apps.

VietinBank’s state-owned status adds trust—its market deposit share was ~12.5% in 2024—but depositors now react to small rate moves and app quality; retail churn rose after 2023 rate hikes.

To retain funds the bank must match top-tier deposit rates (market time deposit avg ~5.8% in 2025) and deliver seamless mobile banking; otherwise customers shift to private joint-stock banks with better digital UX.

The State Bank of Vietnam

As Vietnam’s central bank, the State Bank of Vietnam is the primary supplier of liquidity and regulator; by end-2025 it retains exceptionally high power over VietinBank via mandated reserve requirement ratio (RRR) changes and credit growth quotas—SBV set RRR at 3.0–4.5% in 2024 and tightened credit growth target to 14% for 2025, directly constraining VietinBank’s loan book expansion.

Technology and Infrastructure Providers

VietinBank depends on global and local tech firms for core banking, cybersecurity, and cloud services; switching major systems often costs >$50m and takes 12–24 months, so supplier power is high.

As VietinBank targets full digital transformation by 2026, reliance on specialist AI and data-analytics vendors grew; 2024 vendor spend rose ~18% to an estimated $120m, boosting suppliers’ strategic leverage.

Skilled Human Capital

The market for high-tier financial and IT talent in Vietnam is highly competitive, giving suppliers of skilled labor strong bargaining power; VietinBank faces rivals including BIDV, Techcombank, regional fintechs like GrabPay, and multinationals such as Standard Chartered.

This competition raised average fintech specialist salaries ~18% in 2024 and pushed VietinBank to boost pay, invest in upskilling, and revamp culture to limit turnover above the banking sector average of 12%.

- High competition: local banks, fintechs, MNCs

- Salary rise: ~18% for fintech/IT roles in 2024

- Sector turnover: ~12% in banking

- Action: higher pay, training, culture upgrades

International Capital Markets

VietinBank relies on international bondholders and strategic foreign investors to meet Basel III buffers and fund expansion; these suppliers wield high bargaining power by demanding transparency, ESG compliance, and investment-grade ratings.

In 2025 global markets, VietinBank needs a CET1 ratio near 10.5–11% and a Moody’s-equivalent Baa3/BBB- or better to secure lower spreads; recent offshore bond deals show spreads widening 50–120bp when ratings slip.

- High supplier power: demands for ESG, transparency, ratings

- Target CET1 ~10.5–11% in 2025

- Investment-grade needed to avoid +50–120bp spread

- International funding critical for Basel III compliance

VietinBank faces mixed supplier power: strong regulator and investors, moderate depositors

Supplier power over VietinBank is mixed: depositors' power is moderate (market deposit share ~12.5% in 2024; avg time deposit ~5.8% in 2025), SBV (regulator/liquidity) is very strong (RRR 3.0–4.5% in 2024; credit growth cap 14% for 2025), IT/vendors and global investors hold high leverage (2024 vendor spend ~$120m; CET1 target ~10.5–11% for 2025).

| Supplier | Power | Key metric |

|---|---|---|

| Depositors | Moderate | Deposit share 12.5%; time dep 5.8% |

| SBV | High | RRR 3.0–4.5%; credit cap 14% |

| IT vendors | High | Spend $120m (2024) |

| Intl investors | High | CET1 target 10.5–11% |

What is included in the product

Tailored Porter's Five Forces analysis for Vietin Bank, uncovering competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats to its market position.

A concise VietinBank Porter's Five Forces snapshot that highlights competitive threats and relief strategies—ideal for fast risk assessment and board-ready slides.

Customers Bargaining Power

Large State-Owned Enterprises

Large state-owned enterprises (SOEs) exert high bargaining power at VietinBank because their corporate deposits and lending needs account for roughly 30% of VietinBank’s corporate loan book (2024 annual report), enabling them to demand lower interest spreads and bespoke products unavailable to smaller clients.

Retail Banking Consumers

Individual retail customers gained notable bargaining power by late 2025 as digital comparison tools raised transparency and switching costs fell below $5 per transfer; a 2024 Kantar/Banking report showed 38% of Vietnamese users would switch banks within 12 months for better digital UX or rewards.

Digital-only banks captured 12% of new retail deposits in 2024, letting users move funds fast for higher cashback or better apps.

VietinBank counters by embedding banking into a lifestyle ecosystem—linking payments, e-commerce, and travel—and expanding loyalty tiers that raised monthly active wallet retention by 9% in 2025.

Small and Medium Enterprises

SMEs in Vietnam grew 4.5% in number in 2023 to ~1.2M firms, giving them moderate bargaining power as they can choose traditional banks or fintechs; market share of nonbank lenders rose to 12% of SME credit in 2024.

SMEs value speed and flexible collateral more than brand, so VietinBank automated credit scoring in 2024 to cut SME loan approval time from ~10 days to 48–72 hours for standard cases.

Institutional Investors and Asset Management

Institutional clients using VietinBank for custody and investment banking demand advanced reporting and risk controls; their leverage is high because institutional trades can represent over 20% of corporate banking fees and a single asset manager may move >$100m if service drops.

VietinBank must upgrade its investment banking platform and reporting—investing in real-time risk systems and ISO 20022-compatible feeds—to retain mandates against global custodians.

- High expectation: professional reporting, risk controls

- Power source: large ticket sizes, portability of mandates

- Financial weight: institutional flows >20% of fees

- Required action: real-time risk systems, ISO 20022 feeds

Export and Import Businesses

Vietnam’s trade-led economy (2024 exports + imports ~ US$857bn) gives export/import firms strong bargaining power for trade finance and FX services.

They can switch to global banks—HSBC, Standard Chartered—so VietinBank must use its 1,000+ branches and offer competitive FX spreads to retain them.

In 2024 corporates accounted for ~45% of VietinBank fee income, so losing clients would hit revenue materially.

- Trade volume: ~US$857bn (2024)

- VietinBank branches: 1,000+

- Corp fee share: ~45% (2024)

Powerful, Diverse Customer Bargaining: SOEs, Institutions, Retail & Trade Reshape Banking

Customers exert strong, varied bargaining power: SOEs and institutional mandates drive pricing (30% corporate loans; institutional flows >20% fees), SMEs and fintechs push for speed (SME loans cut to 48–72h), retail digital churn rose (38% willing to switch; digital banks took 12% new deposits in 2024), trade firms demand competitive FX (Vietnam trade ~US$857bn 2024).

| Segment | Key metric |

|---|---|

| SOEs | 30% corporate loans (2024) |

| Institutions | >20% fee flows |

| Retail | 38% switch; 12% deposits (2024) |

| Trade | US$857bn trade (2024) |

Full Version Awaits

Vietin Bank Porter's Five Forces Analysis

This preview shows the exact Vietin Bank Porter's Five Forces analysis you'll receive immediately after purchase—no samples or placeholders; the full document is fully formatted, comprehensive, and ready for download and use the moment you buy.