Vieworks Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

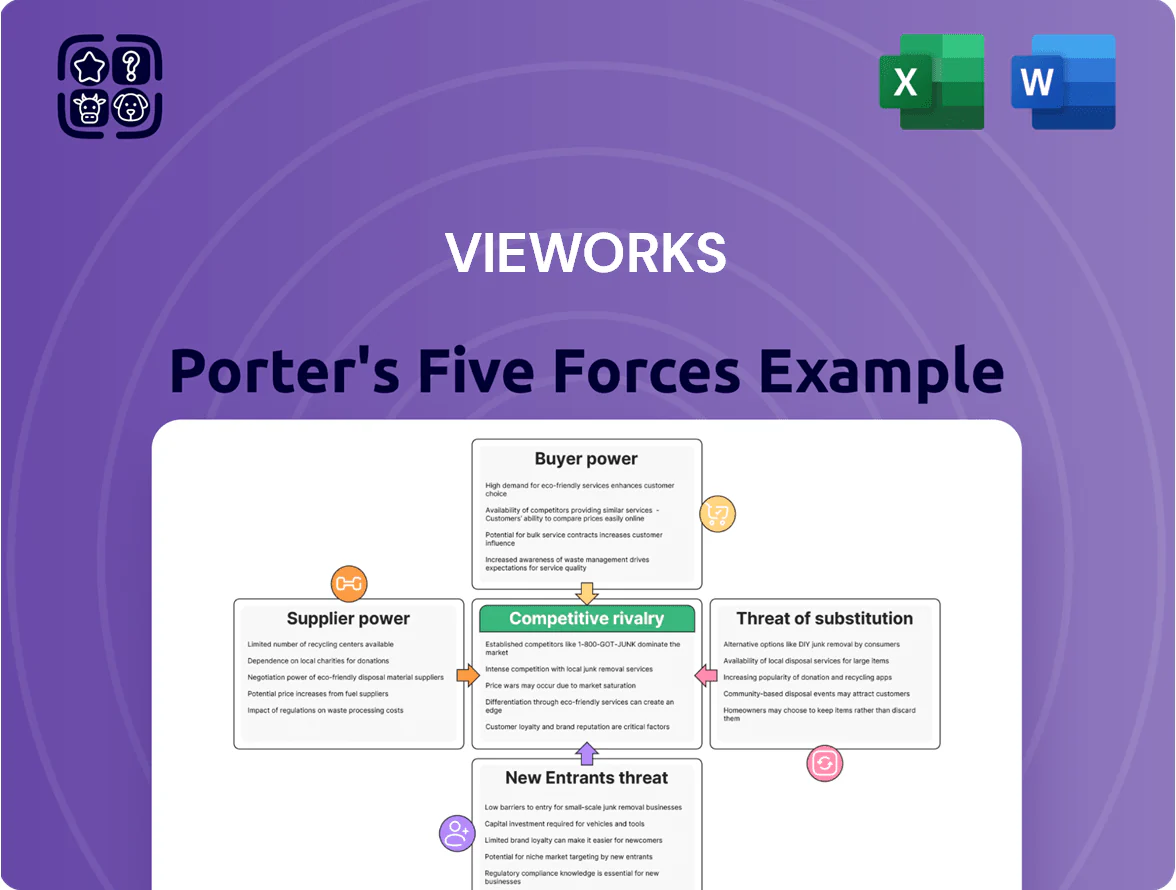

Vieworks faces nuanced competitive pressures—from supplier concentration in specialized components to moderate buyer power driven by niche imaging customers; substitutes and new entrants pose limited but growing threats due to tech advances.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vieworks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of high-end CMOS sensor manufacturers

Vieworks relies on a few specialized semiconductor suppliers for high-performance CMOS/CCD sensors; Sony and ON Semiconductor (ON Semi) held about 55–65% combined market share of high-end industrial/medical imaging sensors by Q4 2025, concentrating supply and raising supplier power.

These sensors are not easily interchangeable, so Vieworks secures long-term contracts and design collaborations to gain priority allocation and stabilize pricing; supplier-led price swings of 8–12% in 2024–25 show the risk.

Scarcity of specialized scintillator materials

The production of flat-panel detectors depends on scintillators like cesium iodide, supplied by a handful of chemical firms; Cesium Iodide accounted for ~60–70% of component cost in industry estimates through 2024, so a supplier disruption can cut detector output by 20–40% in a quarter. With few high-quality alternatives, suppliers set prices and lead times; Vieworks faces concentrated supplier leverage and meaningful margin and delivery risk.

Intellectual property and licensing constraints

Many core digital-imaging technologies rely on third-party patents and Vieworks often signs complex licenses for algorithms and high-speed data architectures; in 2024 Vieworks paid an estimated 6–9% of COGS to IP licensing and royalties, letting suppliers set fees and support terms that directly raise unit costs and margins; this concentration increases supplier bargaining power and can slow product iterations when license renegotiations or exclusivity limits arise.

High switching costs for custom electronic components

Vieworks often builds imaging systems around specific microprocessors and FPGA units that need heavy customization and firmware work; replacing a supplier typically forces full hardware and software redesign, adding R&D costs often exceeding $2–5M and 9–18 months to time-to-market based on industry benchmarks for medical/industrial imaging.

As a result, integrated suppliers gain strong bargaining power across product lifecycles, raising supplier leverage and procurement risk, especially when single-sourced for critical components.

- High redesign cost: $2–5M typical

- Time hit: 9–18 months delay

- Single-source raises leverage

- Long product lifecycles magnify dependence

Global logistics and raw material volatility

Vieworks, a South Korean imaging-maker, faces raw-material and logistics cost swings—aluminum and specialty glass rose ~18% in 2021–24, and ocean freight rates spiked 250% in 2021 then normalized but remain volatile into 2025.

By end-2025, geopolitical strain tightened supply of rare earths for high-end lenses, raising lead times and giving upstream suppliers pricing power; Vieworks must absorb costs or use hedges and longer-term contracts.

- Aluminum/glass +18% (2021–24)

- Ocean freight peak +250% (2021)

- Rare-earth procurement risk elevated by 2025

- Suppliers control channels—forces hedging or margin pressure

High supplier concentration and cost volatility threaten Vieworks’ margins and delivery

Vieworks faces high supplier power: Sony/ON Semi 55–65% share Q4 2025, sensor price swings 8–12% (2024–25), CsI ~60–70% component cost, IP fees 6–9% of COGS (2024), redesign cost $2–5M and 9–18 months delay; single-sourcing and rare-earth/transport volatility raise procurement and margin risk.

| Metric | Value |

|---|---|

| Top sensor market share | 55–65% (Q4 2025) |

| Sensor price volatility | 8–12% (2024–25) |

| CsI cost share | 60–70% |

| IP fees | 6–9% COGS (2024) |

| Redesign cost/time | $2–5M; 9–18 mo |

What is included in the product

Tailored Porter's Five Forces analysis for Vieworks that uncovers competitive pressures, supplier and buyer power, entry barriers, substitute threats, and strategic implications to protect market share and drive pricing power.

A concise Porter's Five Forces snapshot for Vieworks that highlights competitive pressures and strategic levers—ideal for swift, boardroom-ready decisions.

Customers Bargaining Power

Consolidation of medical equipment OEMs

A large share of Vieworks revenue comes from selling flat‑panel detectors to a few global medical OEMs; the top 5 integrators account for roughly 60–70% of industry system purchases (2024 industry reports), giving them strong leverage.

These OEMs buy in high volumes and can switch among suppliers, forcing Vieworks to offer lower prices and longer payment terms; Vieworks gross margin fell to ~28% in FY2024, reflecting this pressure.

High technical standards and performance requirements

Customers in industrial and scientific markets demand precise metrics—high frame rates (often >120 fps) and low read noise (<2 e-)—which extends negotiation cycles and raises customization costs for Vieworks.

Technically savvy buyers can benchmark Vieworks sensors against rivals like Teledyne DALSA and Basler, using public datasheets to pressure price and warranty terms.

Transparency in specs forces Vieworks to meet higher quality at tighter margins; in 2024 global machine vision spending hit $6.8B, increasing buyer leverage.

Price sensitivity in emerging healthcare markets

As Vieworks expands in developing regions, customers face tighter budgets—WHO data show low-income countries spend median health per capita $41 in 2022—so buyers prioritize price over advanced features, pushing Vieworks to sell affordable entry-level imaging at 20–40% discounts versus flagship lines.

Low switching costs for standardized industrial cameras

Low-end industrial cameras are commoditized, so buyers often switch on price; global machine vision camera ASPs fell ~8% 2024–25 to about $1,100, raising price sensitivity.

High-end scientific cameras keep loyalty via features like EMCCD/Back-illuminated sensors, so Vieworks still retains premium clients.

Overall, low integration effort lets customers migrate easily, forcing Vieworks to invest in support and software to protect share.

- ASP drop ~8% (2024–25)

- High-end retention: feature-driven

- Low switching cost → focus on support

Influence of government and institutional procurement

Government and large hospital group tenders account for roughly 40–60% of medical imaging procurement in key markets like the US, EU, and China, using competitive bids that pressure margins and demand strict SLAs.

The structured procurement process shifts leverage to buyers; a single lost contract (often worth 5–15% of annual revenue for mid-size vendors like Vieworks) can materially hit targets.

- 40–60% market share via tenders

- Bids drive price cuts, tighter SLAs

- Single contract = 5–15% revenue risk

Buyer dominance squeezes Vieworks—Top OEMs, tenders drive deep price pressure, margins fall

Buyers hold strong leverage: top 5 OEMs drive ~60–70% system purchases (2024), tenders account for 40–60% in key markets, and single contracts can equal 5–15% of Vieworks revenue, forcing price concessions and longer terms; FY2024 gross margin fell to ~28% under pressure.

| Metric | Value |

|---|---|

| Top‑5 OEM share | 60–70% (2024) |

| Tender reliance | 40–60% |

| FY2024 gross margin | ~28% |

| ASP change | -8% (2024–25) |

Same Document Delivered

Vieworks Porter's Five Forces Analysis

This preview shows the exact Vieworks Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, final, and ready to download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Vieworks faces nuanced competitive pressures—from supplier concentration in specialized components to moderate buyer power driven by niche imaging customers; substitutes and new entrants pose limited but growing threats due to tech advances.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vieworks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of high-end CMOS sensor manufacturers

Vieworks relies on a few specialized semiconductor suppliers for high-performance CMOS/CCD sensors; Sony and ON Semiconductor (ON Semi) held about 55–65% combined market share of high-end industrial/medical imaging sensors by Q4 2025, concentrating supply and raising supplier power.

These sensors are not easily interchangeable, so Vieworks secures long-term contracts and design collaborations to gain priority allocation and stabilize pricing; supplier-led price swings of 8–12% in 2024–25 show the risk.

Scarcity of specialized scintillator materials

The production of flat-panel detectors depends on scintillators like cesium iodide, supplied by a handful of chemical firms; Cesium Iodide accounted for ~60–70% of component cost in industry estimates through 2024, so a supplier disruption can cut detector output by 20–40% in a quarter. With few high-quality alternatives, suppliers set prices and lead times; Vieworks faces concentrated supplier leverage and meaningful margin and delivery risk.

Intellectual property and licensing constraints

Many core digital-imaging technologies rely on third-party patents and Vieworks often signs complex licenses for algorithms and high-speed data architectures; in 2024 Vieworks paid an estimated 6–9% of COGS to IP licensing and royalties, letting suppliers set fees and support terms that directly raise unit costs and margins; this concentration increases supplier bargaining power and can slow product iterations when license renegotiations or exclusivity limits arise.

High switching costs for custom electronic components

Vieworks often builds imaging systems around specific microprocessors and FPGA units that need heavy customization and firmware work; replacing a supplier typically forces full hardware and software redesign, adding R&D costs often exceeding $2–5M and 9–18 months to time-to-market based on industry benchmarks for medical/industrial imaging.

As a result, integrated suppliers gain strong bargaining power across product lifecycles, raising supplier leverage and procurement risk, especially when single-sourced for critical components.

- High redesign cost: $2–5M typical

- Time hit: 9–18 months delay

- Single-source raises leverage

- Long product lifecycles magnify dependence

Global logistics and raw material volatility

Vieworks, a South Korean imaging-maker, faces raw-material and logistics cost swings—aluminum and specialty glass rose ~18% in 2021–24, and ocean freight rates spiked 250% in 2021 then normalized but remain volatile into 2025.

By end-2025, geopolitical strain tightened supply of rare earths for high-end lenses, raising lead times and giving upstream suppliers pricing power; Vieworks must absorb costs or use hedges and longer-term contracts.

- Aluminum/glass +18% (2021–24)

- Ocean freight peak +250% (2021)

- Rare-earth procurement risk elevated by 2025

- Suppliers control channels—forces hedging or margin pressure

High supplier concentration and cost volatility threaten Vieworks’ margins and delivery

Vieworks faces high supplier power: Sony/ON Semi 55–65% share Q4 2025, sensor price swings 8–12% (2024–25), CsI ~60–70% component cost, IP fees 6–9% of COGS (2024), redesign cost $2–5M and 9–18 months delay; single-sourcing and rare-earth/transport volatility raise procurement and margin risk.

| Metric | Value |

|---|---|

| Top sensor market share | 55–65% (Q4 2025) |

| Sensor price volatility | 8–12% (2024–25) |

| CsI cost share | 60–70% |

| IP fees | 6–9% COGS (2024) |

| Redesign cost/time | $2–5M; 9–18 mo |

What is included in the product

Tailored Porter's Five Forces analysis for Vieworks that uncovers competitive pressures, supplier and buyer power, entry barriers, substitute threats, and strategic implications to protect market share and drive pricing power.

A concise Porter's Five Forces snapshot for Vieworks that highlights competitive pressures and strategic levers—ideal for swift, boardroom-ready decisions.

Customers Bargaining Power

Consolidation of medical equipment OEMs

A large share of Vieworks revenue comes from selling flat‑panel detectors to a few global medical OEMs; the top 5 integrators account for roughly 60–70% of industry system purchases (2024 industry reports), giving them strong leverage.

These OEMs buy in high volumes and can switch among suppliers, forcing Vieworks to offer lower prices and longer payment terms; Vieworks gross margin fell to ~28% in FY2024, reflecting this pressure.

High technical standards and performance requirements

Customers in industrial and scientific markets demand precise metrics—high frame rates (often >120 fps) and low read noise (<2 e-)—which extends negotiation cycles and raises customization costs for Vieworks.

Technically savvy buyers can benchmark Vieworks sensors against rivals like Teledyne DALSA and Basler, using public datasheets to pressure price and warranty terms.

Transparency in specs forces Vieworks to meet higher quality at tighter margins; in 2024 global machine vision spending hit $6.8B, increasing buyer leverage.

Price sensitivity in emerging healthcare markets

As Vieworks expands in developing regions, customers face tighter budgets—WHO data show low-income countries spend median health per capita $41 in 2022—so buyers prioritize price over advanced features, pushing Vieworks to sell affordable entry-level imaging at 20–40% discounts versus flagship lines.

Low switching costs for standardized industrial cameras

Low-end industrial cameras are commoditized, so buyers often switch on price; global machine vision camera ASPs fell ~8% 2024–25 to about $1,100, raising price sensitivity.

High-end scientific cameras keep loyalty via features like EMCCD/Back-illuminated sensors, so Vieworks still retains premium clients.

Overall, low integration effort lets customers migrate easily, forcing Vieworks to invest in support and software to protect share.

- ASP drop ~8% (2024–25)

- High-end retention: feature-driven

- Low switching cost → focus on support

Influence of government and institutional procurement

Government and large hospital group tenders account for roughly 40–60% of medical imaging procurement in key markets like the US, EU, and China, using competitive bids that pressure margins and demand strict SLAs.

The structured procurement process shifts leverage to buyers; a single lost contract (often worth 5–15% of annual revenue for mid-size vendors like Vieworks) can materially hit targets.

- 40–60% market share via tenders

- Bids drive price cuts, tighter SLAs

- Single contract = 5–15% revenue risk

Buyer dominance squeezes Vieworks—Top OEMs, tenders drive deep price pressure, margins fall

Buyers hold strong leverage: top 5 OEMs drive ~60–70% system purchases (2024), tenders account for 40–60% in key markets, and single contracts can equal 5–15% of Vieworks revenue, forcing price concessions and longer terms; FY2024 gross margin fell to ~28% under pressure.

| Metric | Value |

|---|---|

| Top‑5 OEM share | 60–70% (2024) |

| Tender reliance | 40–60% |

| FY2024 gross margin | ~28% |

| ASP change | -8% (2024–25) |

Same Document Delivered

Vieworks Porter's Five Forces Analysis

This preview shows the exact Vieworks Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, final, and ready to download with no placeholders or samples.