VINCI Energies SA Porter's Five Forces Analysis

Don't Miss the Bigger Picture

VINCI Energies faces moderate supplier power, intense rivalry among diversified engineering peers, and evolving buyer demands driven by digitalization and energy transition, while barriers to entry remain sizeable due to capital and technical know-how—creating a dynamic but navigable competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VINCI Energies SA’s competitive dynamics, market pressures, and strategic advantages in detail.

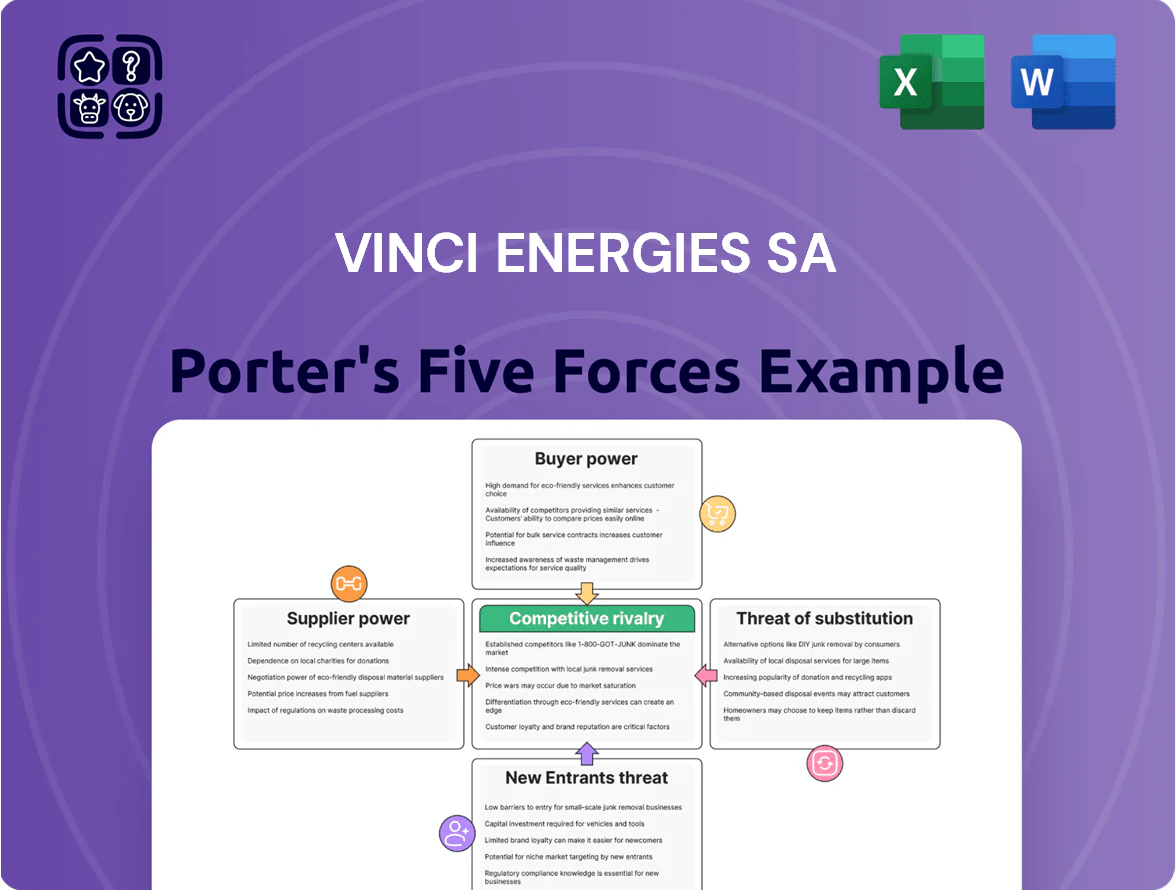

Suppliers Bargaining Power

Concentration of specialized equipment manufacturers

The market for high-tech electrical components and digital infrastructure is concentrated among Schneider Electric, Siemens, and ABB, which held roughly 40–50% combined share of global low-voltage and automation markets in 2024, giving suppliers strong leverage where proprietary tech is specified in designs and substitution is costly.

VINCI Energies reduces supplier power by pooling procurement across ~89 countries and EUR 16.5bn group revenue in 2024, negotiating volume discounts, long‑term framework contracts, and joint engineering to lower input costs and limit single‑vendor lock‑in.

Volatility in raw material costs

VINCI Energies is highly sensitive to copper, aluminum and steel price swings; copper rose 28% in 2023 and steel HRC averaged +15% in 2024, squeezing project margins before indexation clauses adjust prices.

Shortage of highly skilled technical labor

Specialized engineers act as internal suppliers; a 2024 global shortage of 1.2M skilled tech workers raises their bargaining power, pushing VINCI Energies SA to pay premiums and invest ~€220–€300M annually in training and retention programs.

High demand for experts in automation, cybersecurity, and renewable grids—where EU vacancy rates hit 9% in 2024—means VINCI faces costly recruitment and slower scaling of complex projects.

Dependence on niche software providers

As VINCI Energies’ Axians scales cloud and software deployments, dependence on niche devs and hyperscalers rises; Gartner reported 2024 enterprise SaaS spend grew 18% to $171B, pressuring long-term maintenance costs.

Subscription pricing and average annual SaaS price hikes of 6–8% give vendors leverage, and high migration costs—often 15–30% of project value—reduce VINCI’s bargaining power and squeeze margins.

- 2024 SaaS market +18% to $171B

- Avg annual SaaS price hikes 6–8%

- Migration cost 15–30% of project value

Local subcontractor availability

VINCI Energies depends on local subcontractors for large rollouts; in 2024 subcontracted labor accounted for about 30% of project workforce, raising supplier power in tight markets.

In high-construction regions subcontractors can push rates up 10–25% versus national averages, increasing risk of cost overruns and schedule slips.

Keeping a loyal, certified subcontractor pool reduces delay risk; VINCI reports vendor consolidation cut site delays by ~15% in 2023.

- 30% of workforce subcontracted in 2024

- Rates +10–25% in hot markets

- Vendor consolidation cut delays ~15% (2023)

Supplier concentration vs VINCI's procurement scale amid commodity, labor & subcontract risks

Suppliers—notably Schneider, Siemens, ABB—hold concentrated tech leverage (40–50% share in 2024), while VINCI Energies offsets this via group procurement (EUR 16.5bn, 89 countries) and long‑term contracts; commodity swings (copper +28% in 2023; steel HRC +15% in 2024) and a 1.2M 2024 skills shortfall raise costs, plus 30% subcontracting increases regional rate risk.

| Metric | 2024/2023 |

|---|---|

| Major supplier share | 40–50% |

| Group revenue / reach | EUR 16.5bn, 89 countries |

| Copper price change | +28% (2023) |

| Steel HRC change | +15% (2024) |

| Global tech worker shortage | 1.2M (2024) |

| Subcontracted workforce | 30% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for VINCI Energies SA, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive threats and strategic levers that shape its pricing, profitability, and market defenses.

A concise, one-sheet Porter's Five Forces for VINCI Energies that highlights competitive pressures and relief options—ideal for fast strategic decisions and slide-ready sharing.

Customers Bargaining Power

Public sector procurement dominance

Government clients account for an estimated 35–45% of VINCI Energies SA relevant infrastructure revenue, giving public procurement strong leverage in competitive bids and contract design; in 2024 EU public tenders awarded €1.2 trillion in contracts, letting buyers demand aggressive pricing and extended payment terms. These authorities also enforce strict ESG clauses—raising compliance costs by an estimated 3–6% of project value—and favor multi‑year awards that reduce supplier pricing power.

Consolidation of industrial clients

Large industrial clients in automotive, aerospace and chemicals are consolidating, enabling pan-European and global service agreements that increase buyer leverage; in 2024, 60% of OEMs reported centralised procurement for engineering services, pressuring regional suppliers like VINCI Energies SA.

These sophisticated buyers use professional procurement teams to run RFPs and benchmark bids, often pitting VINCI Energies against rivals such as Schneider Electric and Siemens to extract fee cuts of 5–15% on service contracts.

The bespoke nature of industrial automation—specialised skills, long lead times—offers VINCI Energies partial insulation, yet average EBITDA margins in the sector fell to ~8.5% in 2024, reflecting persistent margin pressure.

Low switching costs for maintenance services

In building solutions and facilities management, clients face low switching costs at contract renewal, with industry churn rates around 12–18% annually in Europe (2024), driving frequent re-tendering for lower price or advanced tech.

Commercial owners often select lowest bidder or a provider with IoT-enabled maintenance; procurement cycles average 6–12 months.

VINCI Energies raises switching barriers by embedding digital tools—predictive maintenance and cloud platforms—into operations, boosting client retention and recurring revenue.

Demand for integrated turnkey solutions

Modern clients increasingly prefer single-source turnkey providers for design, installation and digital maintenance; VINCI Energies reported 2024 group-wide solutions revenue up 6.8% to EUR 15.2bn, so bundled offers let VINCI capture higher margins.

That concentration gives customers leverage to demand performance guarantees and risk-sharing, and in 2024 42% of large European contracts included KPI-linked payments, raising customer bargaining power.

Clients can threaten to unbundle if integrated pricing seems uncompetitive, forcing VINCI to match component-level bids or offer tighter SLAs.

- Turnkey demand up: +6.8% revenue to EUR 15.2bn (2024)

- 42% large contracts: KPI-linked payments (2024)

- Customers push for guarantees, risk-sharing, price transparency

Transparency through digital benchmarking

Digital procurement platforms have grown 35% globally in platform spend 2023–2024, letting customers compare VINCI Energies against rivals on price and KPIs in real time.

This transparency shrinks information asymmetry that favored incumbents; buyers use benchmarking to contest bids and push for measurable efficiency gains, often linking 10–20% of contract value to energy-saving KPIs.

- Platform spend up 35% (2023–24)

- Clients demand 10–20% of fees tied to efficiency

- Real-time KPI comparison reduces bid premiums

Buyers' leverage rises: KPI contracts, fee cuts and digital platforms squeeze margins

Customers hold strong leverage—public buyers (35–45% revenue) and consolidated industrial OEMs push aggressive pricing, KPI-linked payments (42% large contracts) and 5–15% fee cuts; digital procurement growth (+35% platform spend 2023–24) raises price transparency while VINCI’s bundled solutions (EUR 15.2bn, +6.8% 2024) and embedded digital tools partly offset churn (12–18% industry rate).

| Metric | 2024/2023 |

|---|---|

| Public client share | 35–45% |

| Turnkey solutions revenue | EUR 15.2bn (+6.8%) |

| KPI-linked contracts | 42% |

| Industry churn | 12–18% |

| Platform spend growth | +35% (2023–24) |

Preview the Actual Deliverable

VINCI Energies SA Porter's Five Forces Analysis

This preview shows the exact VINCI Energies SA Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

VINCI Energies faces moderate supplier power, intense rivalry among diversified engineering peers, and evolving buyer demands driven by digitalization and energy transition, while barriers to entry remain sizeable due to capital and technical know-how—creating a dynamic but navigable competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VINCI Energies SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized equipment manufacturers

The market for high-tech electrical components and digital infrastructure is concentrated among Schneider Electric, Siemens, and ABB, which held roughly 40–50% combined share of global low-voltage and automation markets in 2024, giving suppliers strong leverage where proprietary tech is specified in designs and substitution is costly.

VINCI Energies reduces supplier power by pooling procurement across ~89 countries and EUR 16.5bn group revenue in 2024, negotiating volume discounts, long‑term framework contracts, and joint engineering to lower input costs and limit single‑vendor lock‑in.

Volatility in raw material costs

VINCI Energies is highly sensitive to copper, aluminum and steel price swings; copper rose 28% in 2023 and steel HRC averaged +15% in 2024, squeezing project margins before indexation clauses adjust prices.

Shortage of highly skilled technical labor

Specialized engineers act as internal suppliers; a 2024 global shortage of 1.2M skilled tech workers raises their bargaining power, pushing VINCI Energies SA to pay premiums and invest ~€220–€300M annually in training and retention programs.

High demand for experts in automation, cybersecurity, and renewable grids—where EU vacancy rates hit 9% in 2024—means VINCI faces costly recruitment and slower scaling of complex projects.

Dependence on niche software providers

As VINCI Energies’ Axians scales cloud and software deployments, dependence on niche devs and hyperscalers rises; Gartner reported 2024 enterprise SaaS spend grew 18% to $171B, pressuring long-term maintenance costs.

Subscription pricing and average annual SaaS price hikes of 6–8% give vendors leverage, and high migration costs—often 15–30% of project value—reduce VINCI’s bargaining power and squeeze margins.

- 2024 SaaS market +18% to $171B

- Avg annual SaaS price hikes 6–8%

- Migration cost 15–30% of project value

Local subcontractor availability

VINCI Energies depends on local subcontractors for large rollouts; in 2024 subcontracted labor accounted for about 30% of project workforce, raising supplier power in tight markets.

In high-construction regions subcontractors can push rates up 10–25% versus national averages, increasing risk of cost overruns and schedule slips.

Keeping a loyal, certified subcontractor pool reduces delay risk; VINCI reports vendor consolidation cut site delays by ~15% in 2023.

- 30% of workforce subcontracted in 2024

- Rates +10–25% in hot markets

- Vendor consolidation cut delays ~15% (2023)

Supplier concentration vs VINCI's procurement scale amid commodity, labor & subcontract risks

Suppliers—notably Schneider, Siemens, ABB—hold concentrated tech leverage (40–50% share in 2024), while VINCI Energies offsets this via group procurement (EUR 16.5bn, 89 countries) and long‑term contracts; commodity swings (copper +28% in 2023; steel HRC +15% in 2024) and a 1.2M 2024 skills shortfall raise costs, plus 30% subcontracting increases regional rate risk.

| Metric | 2024/2023 |

|---|---|

| Major supplier share | 40–50% |

| Group revenue / reach | EUR 16.5bn, 89 countries |

| Copper price change | +28% (2023) |

| Steel HRC change | +15% (2024) |

| Global tech worker shortage | 1.2M (2024) |

| Subcontracted workforce | 30% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for VINCI Energies SA, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive threats and strategic levers that shape its pricing, profitability, and market defenses.

A concise, one-sheet Porter's Five Forces for VINCI Energies that highlights competitive pressures and relief options—ideal for fast strategic decisions and slide-ready sharing.

Customers Bargaining Power

Public sector procurement dominance

Government clients account for an estimated 35–45% of VINCI Energies SA relevant infrastructure revenue, giving public procurement strong leverage in competitive bids and contract design; in 2024 EU public tenders awarded €1.2 trillion in contracts, letting buyers demand aggressive pricing and extended payment terms. These authorities also enforce strict ESG clauses—raising compliance costs by an estimated 3–6% of project value—and favor multi‑year awards that reduce supplier pricing power.

Consolidation of industrial clients

Large industrial clients in automotive, aerospace and chemicals are consolidating, enabling pan-European and global service agreements that increase buyer leverage; in 2024, 60% of OEMs reported centralised procurement for engineering services, pressuring regional suppliers like VINCI Energies SA.

These sophisticated buyers use professional procurement teams to run RFPs and benchmark bids, often pitting VINCI Energies against rivals such as Schneider Electric and Siemens to extract fee cuts of 5–15% on service contracts.

The bespoke nature of industrial automation—specialised skills, long lead times—offers VINCI Energies partial insulation, yet average EBITDA margins in the sector fell to ~8.5% in 2024, reflecting persistent margin pressure.

Low switching costs for maintenance services

In building solutions and facilities management, clients face low switching costs at contract renewal, with industry churn rates around 12–18% annually in Europe (2024), driving frequent re-tendering for lower price or advanced tech.

Commercial owners often select lowest bidder or a provider with IoT-enabled maintenance; procurement cycles average 6–12 months.

VINCI Energies raises switching barriers by embedding digital tools—predictive maintenance and cloud platforms—into operations, boosting client retention and recurring revenue.

Demand for integrated turnkey solutions

Modern clients increasingly prefer single-source turnkey providers for design, installation and digital maintenance; VINCI Energies reported 2024 group-wide solutions revenue up 6.8% to EUR 15.2bn, so bundled offers let VINCI capture higher margins.

That concentration gives customers leverage to demand performance guarantees and risk-sharing, and in 2024 42% of large European contracts included KPI-linked payments, raising customer bargaining power.

Clients can threaten to unbundle if integrated pricing seems uncompetitive, forcing VINCI to match component-level bids or offer tighter SLAs.

- Turnkey demand up: +6.8% revenue to EUR 15.2bn (2024)

- 42% large contracts: KPI-linked payments (2024)

- Customers push for guarantees, risk-sharing, price transparency

Transparency through digital benchmarking

Digital procurement platforms have grown 35% globally in platform spend 2023–2024, letting customers compare VINCI Energies against rivals on price and KPIs in real time.

This transparency shrinks information asymmetry that favored incumbents; buyers use benchmarking to contest bids and push for measurable efficiency gains, often linking 10–20% of contract value to energy-saving KPIs.

- Platform spend up 35% (2023–24)

- Clients demand 10–20% of fees tied to efficiency

- Real-time KPI comparison reduces bid premiums

Buyers' leverage rises: KPI contracts, fee cuts and digital platforms squeeze margins

Customers hold strong leverage—public buyers (35–45% revenue) and consolidated industrial OEMs push aggressive pricing, KPI-linked payments (42% large contracts) and 5–15% fee cuts; digital procurement growth (+35% platform spend 2023–24) raises price transparency while VINCI’s bundled solutions (EUR 15.2bn, +6.8% 2024) and embedded digital tools partly offset churn (12–18% industry rate).

| Metric | 2024/2023 |

|---|---|

| Public client share | 35–45% |

| Turnkey solutions revenue | EUR 15.2bn (+6.8%) |

| KPI-linked contracts | 42% |

| Industry churn | 12–18% |

| Platform spend growth | +35% (2023–24) |

Preview the Actual Deliverable

VINCI Energies SA Porter's Five Forces Analysis

This preview shows the exact VINCI Energies SA Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.