VINCI Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

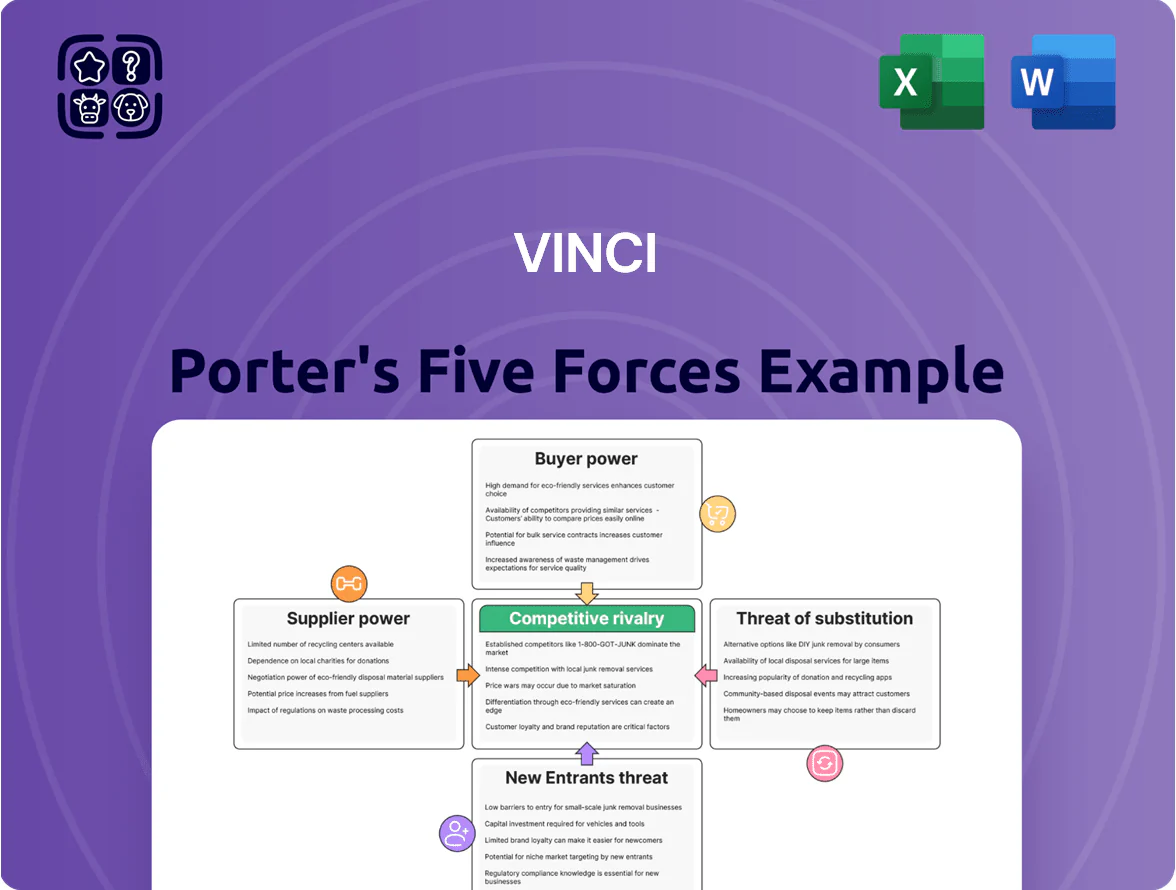

VINCI faces varied competitive pressures—strong supplier networks, scale-driven buyer expectations, and moderate threat from new entrants and substitutes shaped by high capital intensity and regulatory barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VINCI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Procurement of steel, cement and bitumen faces global commodity swings that can cut VINCI project margins; steel futures rose ~18% in 2025 H2 and international cement prices climbed ~12% through Q3 2025. VINCI uses scale—€57bn 2024 revenue—to lock multi-year supply contracts and hedges, but sudden late-2025 geopolitical spikes exposed gaps. Suppliers hold moderate power when global infrastructure demand peaks, pushing short-term pass-throughs to clients.

Specialized Labor Scarcity

The chronic shortage of skilled engineers and technical workers in Europe and North America—estimated at 1.2 million construction roles unfilled in the EU and 400,000 in the US in 2024—gives suppliers of specialized labor high bargaining power over VINCI, raising wage premiums and consultancy rates by 10–20% year-on-year.

VINCI must boost training and pay: a 2025 internal upskilling plan and a 15–25% compensation premium for niche roles cut projected delay risk from 18% to ~8% in internal models.

Energy and Fuel Dependencies

Operational costs for VINCI's heavy machinery and asphalt plants track electricity and diesel prices; in 2024 diesel averaged €1.70/l and industrial electricity €0.22/kWh in France, pushing fuel-linked margins down.

As VINCI shifts to renewables, dependence on specific offshore wind and solar providers plus grid operators rises, concentrating supplier leverage.

Mandatory EU carbon cuts (55% by 2030 vs 1990) and France’s 2030 targets increase bargaining power of low-carbon energy suppliers, who can command premium contracts and green tariffs.

Strategic Procurement Scale

VINCI centralizes procurement across ~222,000 employees and €59.1bn 2024 revenue, using volume to negotiate lower prices and longer payment terms with smaller regional suppliers.

Many vendors depend on VINCI for 10–40% of orders in local markets, weakening their bargaining power versus VINCI’s buying scale and diversified project backlog.

- €59.1bn 2024 revenue

- ~222,000 employees

- Suppliers often 10–40% revenue exposure

Subcontractor Dependency

VINCI depends on specialized subcontractors for niche tasks on large projects; in 2024 subcontracting accounted for about 45% of VINCI Construction revenues, giving suppliers leverage when they hold unique tech or local dominance.

VINCI mitigates risk via long-term agreements, certification programs, and centralized procurement; delays from key subcontractors can push project timelines up to 12+ weeks and raise costs by 3–6%.

- 45% of construction revenue from subcontracting (2024)

- Key-supplier delays can add 12+ weeks

- Delay-related cost impact: ~3–6%

- Controls: long-term contracts, certifications, centralized procurement

Suppliers tighten screws: commodity spikes and labor shortages test VINCI’s scale

Suppliers exert moderate-to-high power: commodity swings (steel +18% 2025 H2; cement +12% YTD 2025) and skilled-labour shortages (EU 1.2M, US 400k unfilled 2024) raise costs; VINCI’s scale (€59.1bn revenue, 2024) and central procurement cut prices, while subcontracting (45% of construction revenue, 2024) and specialist providers keep leverage for niche services.

| Metric | Value |

|---|---|

| Revenue (2024) | €59.1bn |

| Subcontracting share (2024) | 45% |

| Steel futures change (2025 H2) | +18% |

| Cement price change (2025 Q3) | +12% |

| EU construction vacancies (2024) | 1.2M |

| US construction vacancies (2024) | 400,000 |

What is included in the product

Tailored Porter's Five Forces analysis for VINCI, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with actionable strategic commentary.

A concise VINCI-focused Porter’s Five Forces one-sheet that highlights competitive pressures and relieves strategic uncertainty for faster, board-ready decisions.

Customers Bargaining Power

Public Sector Contract Concentration

About 40% of VINCI’s 2024 revenue (EUR 66.1bn total) came from public-sector contracts, giving governments high bargaining power; public authorities set strict tender specs and often define concession scope and pricing for 20–50 year assets. Such clients can require discounting, added performance clauses, or renegotiation rights, so VINCI must sustain political and institutional ties—often via joint ventures or local partners—to stay a preferred national infrastructure contractor.

Competitive Bidding Processes

Open, transparent bidding for public works lets governments compare offers and push prices down; in 2024 EU procurement awards saw 38% of large contracts go to lowest-price bids, lowering margins for contractors like VINCI (2024 revenue €54.9bn). Clients’ emphasis on lowest cost or best value-for-money forces VINCI to trim costs and improve efficiency, shifting bargaining power to buyers during initial contract awards.

Concession User Price Sensitivity

Contractual Rigidities

Quality and Sustainability Demands

Modern clients now make ESG (environmental, social, governance) compliance a contract gate—public procurement in the EU saw 42% of tenders include explicit sustainability criteria in 2023, so customers can set technical and green benchmarks that bidders must meet.

That shifts bargaining power: VINCI must invest in low-carbon materials and reporting systems or risk losing bids to nimbler rivals; VINCI reported €2.4bn green capex in 2024, showing this pressure already affects cash allocation.

- 42% EU tenders had sustainability criteria (2023)

- VINCI green capex €2.4bn (2024)

- Clients set specs and benchmarks

- Non-compliance risks lost contracts

Public buyers squeeze VINCI: tenders, tariffs and €2.4bn green capex hit margins

Buyers (mainly governments) hold strong bargaining power over VINCI via public tenders (≈40% of 2024 revenue), long-term concession clauses (20–50 years) and tariff caps (68% of global port concessions include review clauses in 2024), plus ESG procurement rules (42% EU tenders 2023) that force €2.4bn green capex (2024), compressing margins and limiting pricing flexibility.

| Metric | Value |

|---|---|

| Share public-sector revenue (2024) | ≈40% |

| Total revenue (2024) | €66.1bn |

| Port concessions w/ tariff clauses (2024) | 68% |

| EU tenders w/ sustainability (2023) | 42% |

| VINCI green capex (2024) | €2.4bn |

Full Version Awaits

VINCI Porter's Five Forces Analysis

This preview shows the exact VINCI Porter’s Five Forces analysis you’ll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

VINCI faces varied competitive pressures—strong supplier networks, scale-driven buyer expectations, and moderate threat from new entrants and substitutes shaped by high capital intensity and regulatory barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore VINCI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Procurement of steel, cement and bitumen faces global commodity swings that can cut VINCI project margins; steel futures rose ~18% in 2025 H2 and international cement prices climbed ~12% through Q3 2025. VINCI uses scale—€57bn 2024 revenue—to lock multi-year supply contracts and hedges, but sudden late-2025 geopolitical spikes exposed gaps. Suppliers hold moderate power when global infrastructure demand peaks, pushing short-term pass-throughs to clients.

Specialized Labor Scarcity

The chronic shortage of skilled engineers and technical workers in Europe and North America—estimated at 1.2 million construction roles unfilled in the EU and 400,000 in the US in 2024—gives suppliers of specialized labor high bargaining power over VINCI, raising wage premiums and consultancy rates by 10–20% year-on-year.

VINCI must boost training and pay: a 2025 internal upskilling plan and a 15–25% compensation premium for niche roles cut projected delay risk from 18% to ~8% in internal models.

Energy and Fuel Dependencies

Operational costs for VINCI's heavy machinery and asphalt plants track electricity and diesel prices; in 2024 diesel averaged €1.70/l and industrial electricity €0.22/kWh in France, pushing fuel-linked margins down.

As VINCI shifts to renewables, dependence on specific offshore wind and solar providers plus grid operators rises, concentrating supplier leverage.

Mandatory EU carbon cuts (55% by 2030 vs 1990) and France’s 2030 targets increase bargaining power of low-carbon energy suppliers, who can command premium contracts and green tariffs.

Strategic Procurement Scale

VINCI centralizes procurement across ~222,000 employees and €59.1bn 2024 revenue, using volume to negotiate lower prices and longer payment terms with smaller regional suppliers.

Many vendors depend on VINCI for 10–40% of orders in local markets, weakening their bargaining power versus VINCI’s buying scale and diversified project backlog.

- €59.1bn 2024 revenue

- ~222,000 employees

- Suppliers often 10–40% revenue exposure

Subcontractor Dependency

VINCI depends on specialized subcontractors for niche tasks on large projects; in 2024 subcontracting accounted for about 45% of VINCI Construction revenues, giving suppliers leverage when they hold unique tech or local dominance.

VINCI mitigates risk via long-term agreements, certification programs, and centralized procurement; delays from key subcontractors can push project timelines up to 12+ weeks and raise costs by 3–6%.

- 45% of construction revenue from subcontracting (2024)

- Key-supplier delays can add 12+ weeks

- Delay-related cost impact: ~3–6%

- Controls: long-term contracts, certifications, centralized procurement

Suppliers tighten screws: commodity spikes and labor shortages test VINCI’s scale

Suppliers exert moderate-to-high power: commodity swings (steel +18% 2025 H2; cement +12% YTD 2025) and skilled-labour shortages (EU 1.2M, US 400k unfilled 2024) raise costs; VINCI’s scale (€59.1bn revenue, 2024) and central procurement cut prices, while subcontracting (45% of construction revenue, 2024) and specialist providers keep leverage for niche services.

| Metric | Value |

|---|---|

| Revenue (2024) | €59.1bn |

| Subcontracting share (2024) | 45% |

| Steel futures change (2025 H2) | +18% |

| Cement price change (2025 Q3) | +12% |

| EU construction vacancies (2024) | 1.2M |

| US construction vacancies (2024) | 400,000 |

What is included in the product

Tailored Porter's Five Forces analysis for VINCI, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with actionable strategic commentary.

A concise VINCI-focused Porter’s Five Forces one-sheet that highlights competitive pressures and relieves strategic uncertainty for faster, board-ready decisions.

Customers Bargaining Power

Public Sector Contract Concentration

About 40% of VINCI’s 2024 revenue (EUR 66.1bn total) came from public-sector contracts, giving governments high bargaining power; public authorities set strict tender specs and often define concession scope and pricing for 20–50 year assets. Such clients can require discounting, added performance clauses, or renegotiation rights, so VINCI must sustain political and institutional ties—often via joint ventures or local partners—to stay a preferred national infrastructure contractor.

Competitive Bidding Processes

Open, transparent bidding for public works lets governments compare offers and push prices down; in 2024 EU procurement awards saw 38% of large contracts go to lowest-price bids, lowering margins for contractors like VINCI (2024 revenue €54.9bn). Clients’ emphasis on lowest cost or best value-for-money forces VINCI to trim costs and improve efficiency, shifting bargaining power to buyers during initial contract awards.

Concession User Price Sensitivity

Contractual Rigidities

Quality and Sustainability Demands

Modern clients now make ESG (environmental, social, governance) compliance a contract gate—public procurement in the EU saw 42% of tenders include explicit sustainability criteria in 2023, so customers can set technical and green benchmarks that bidders must meet.

That shifts bargaining power: VINCI must invest in low-carbon materials and reporting systems or risk losing bids to nimbler rivals; VINCI reported €2.4bn green capex in 2024, showing this pressure already affects cash allocation.

- 42% EU tenders had sustainability criteria (2023)

- VINCI green capex €2.4bn (2024)

- Clients set specs and benchmarks

- Non-compliance risks lost contracts

Public buyers squeeze VINCI: tenders, tariffs and €2.4bn green capex hit margins

Buyers (mainly governments) hold strong bargaining power over VINCI via public tenders (≈40% of 2024 revenue), long-term concession clauses (20–50 years) and tariff caps (68% of global port concessions include review clauses in 2024), plus ESG procurement rules (42% EU tenders 2023) that force €2.4bn green capex (2024), compressing margins and limiting pricing flexibility.

| Metric | Value |

|---|---|

| Share public-sector revenue (2024) | ≈40% |

| Total revenue (2024) | €66.1bn |

| Port concessions w/ tariff clauses (2024) | 68% |

| EU tenders w/ sustainability (2023) | 42% |

| VINCI green capex (2024) | €2.4bn |

Full Version Awaits

VINCI Porter's Five Forces Analysis

This preview shows the exact VINCI Porter’s Five Forces analysis you’ll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.