VINCI PESTLE Analysis

Skip the Research. Get the Strategy.

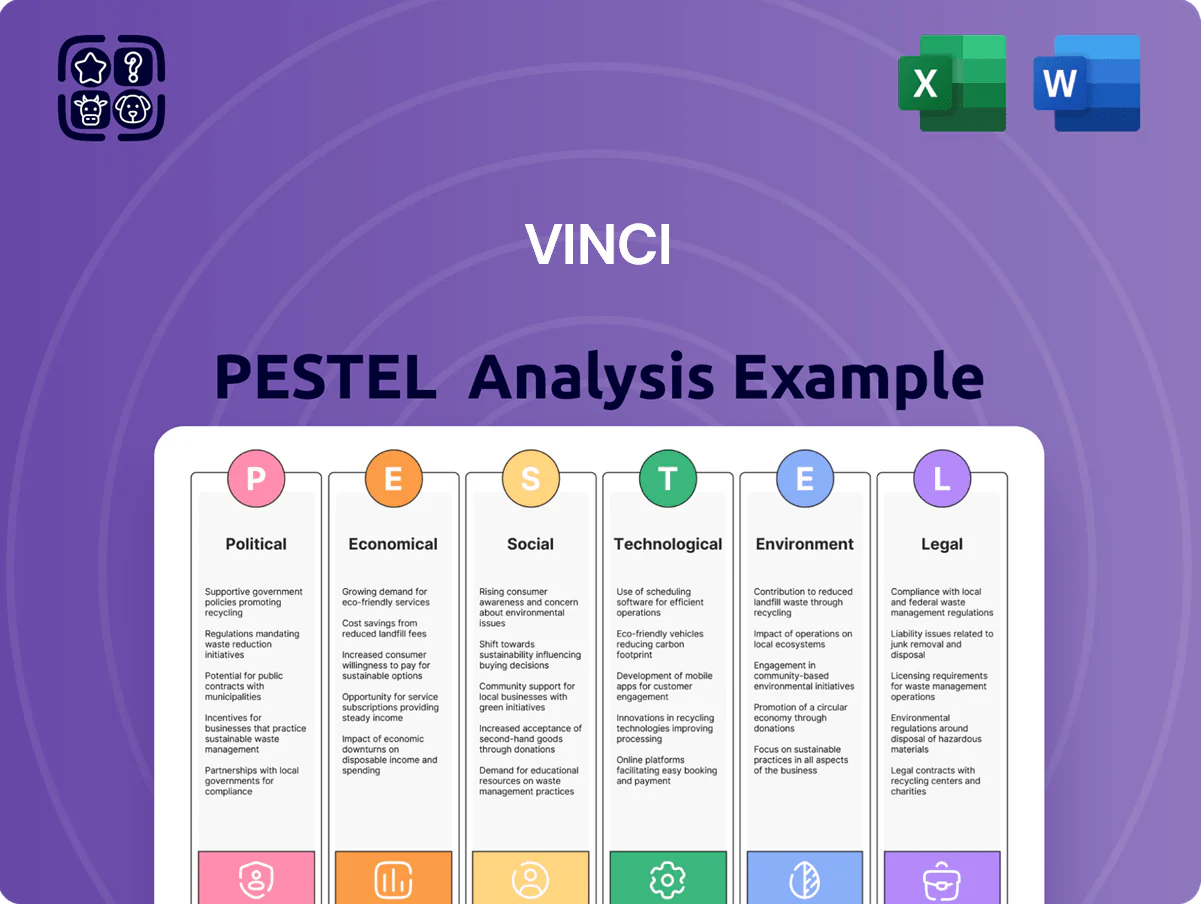

Unlock strategic clarity with our PESTLE Analysis of VINCI—concise, expert-led insight into the political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; ideal for investors, advisors, and strategists. Purchase the full report to access ready-to-use, editable findings and actionable recommendations that save time and strengthen your decisions.

Political factors

Geopolitical stability and international expansion

VINCI operates in over 120 countries, so its €61.5bn 2023 revenue is highly sensitive to geopolitical tensions and France’s diplomatic ties with host nations.

Political shifts in key markets such as Brazil, Mexico and Southeast Asia threaten long-term concession security for assets like the €7.3bn VINCI Airports portfolio and large toll concessions.

Strategic planning must factor localized volatility risks that could delay projects, increase financing costs or trigger renegotiations, as seen in sector-wide 2022–24 risk premia rises.

Government infrastructure spending and stimulus

VINCI secures roughly 60% of revenues from public-sector contracts, so government infrastructure spending shapes backlog and margins; EU Recovery and Resilience Facility disbursements (over €723bn committed 2021–2026) and France’s €30bn France 2030 plan drive tender volumes for transport and urban works.

Regulatory oversight of concession contracts

As operator of ~4,400 km of motorways and 46 airports, VINCI faces intense political scrutiny on toll and aeronautical pricing; governments have capped toll rises in France (2024 cap ~2.6%) and renegotiated PPP terms affecting cash flows. State interventions risk reducing projected EBITDA for concession portfolios—concessions contributed ~55% of VINCI Concessions 2024 revenues (€13.8bn). Maintaining strong government ties is therefore critical to protect long-term contracted cash flows and credit metrics.

Trade policies and protectionism

Fluctuations in global trade policies and tariffs on inputs like steel (world steel price up ~15% in 2024 vs 2023) can raise VINCI construction costs and compress margins on large projects.

Rising protectionism and local content rules in markets such as the US and Brazil force VINCI to reconfigure supply chains and local hiring, increasing capex and operational complexity.

Active monitoring of trade agreements (e.g., EU–UK, USMCA updates) is vital to protect profitability on cross-border engineering contracts.

- Tariff-driven input cost volatility (steel, aluminum)

- Local content requirements raise sourcing and labor costs

- Need for trade-agreement monitoring to safeguard margins

Political focus on energy sovereignty

The EU’s push for energy sovereignty—EUR 300bn+ in Fit for 55-related investments and Member State nuclear revivals—boosts demand for VINCI’s nuclear and renewables engineering, aligning with VINCI Energies which reported 2024 revenue of ~EUR 19.1bn across energy services.

Political mandates to cut fossil fuels (targeting 55% emissions reduction by 2030) create procurement pipelines and government-backed projects where VINCI can leverage its EPC capabilities and capture public investment.

- EU energy investment >EUR 300bn (Fit for 55)

- VINCI Energies 2024 revenue ~EUR 19.1bn

- 2030 emissions cut target 55% drives public projects

VINCI: €61.5bn revenue, high political risk—public contracts, toll caps & rising costs

VINCI’s €61.5bn 2023 revenue and €13.8bn Concessions 2024 revenue are highly exposed to political risk across 120+ countries; public contracts ~60% of revenue; EU Recovery funds (€723bn) and Fit for 55 (>€300bn) drive tenders; toll caps (France 2024 ~2.6%) and tariff-driven steel +15% (2024 vs 2023) pressure margins; local content rules raise capex and operational complexity.

| Metric | Value |

|---|---|

| 2023 revenue | €61.5bn |

| Concessions 2024 rev | €13.8bn |

| Public-contract share | ~60% |

| EU Recovery | €723bn (2021–26) |

| Fit for 55 | >€300bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect VINCI across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise VINCI PESTLE summary that distills external risks and opportunities into clear categories for quick reference during meetings or presentations, helping teams align strategy and decision-making efficiently.

Economic factors

Interest rate environment and debt servicing

VINCI’s capital-intensive model relies on €57.5bn net debt at end-2024; higher rates in 2022–2024 raised average cost of debt to ~2.8% in 2024, squeezing concession margins and increasing project financing costs.

Persistently elevated rates made acquisitions pricier and delayed some bids, but rate stabilization and declines through 2025 opened refinancing windows, potentially lowering interest expense and enabling more acquisitive growth.

Inflationary pressures on material and labor costs

Volatility in energy, bitumen, steel and cement—steel futures rose ~18% in 2024 and global oil averaged $85/barrel in 2024—erodes margins on VINCI’s fixed‑price contracts, while inflation‑linked toll indexation in some concessions offsets only after implementation lags, creating short‑term margin pressure; managing rising labor costs (French construction wages up ~4.5% in 2024) through tighter project management and automation is a key economic challenge.

Global tourism and air traffic recovery

The economic health of VINCI Airports is closely linked to global travel demand and passenger disposable income; in 2024 global air passenger traffic reached about 85% of 2019 levels according to IATA, boosting passenger-related revenue. Economic slowdowns in key markets such as the EU or China can reduce flight frequencies and cut non-aeronautical income—retail and parking—already pressuring margins in 2023–24. Growth in aviation, notably in emerging markets where passenger volumes rose double digits in 2024, is critical for VINCI’s high-margin concession business. VINCI Airports’ 2024 traffic recovery supported a rebound in concession revenues versus 2022, underpinning EBITDA resilience.

Currency exchange rate fluctuations

With roughly 65% of VINCI’s 2024 revenue generated outside the Eurozone, the group faces transaction and translation exposure to the US dollar, British pound and various emerging-market currencies; a 5% EUR depreciation vs USD could raise reported overseas revenue materially.

Currency volatility can compress margins and weaken bid competitiveness in foreign tenders, as seen when FX swings affected unit bid costs in 2023–24.

VINCI uses hedging—forwards, options and natural hedges—to limit P&L and balance-sheet impacts, with net foreign exchange hedges reported at about €X billion in 2024.

- ~65% revenue outside Eurozone

- Exposure to USD, GBP and emerging currencies

- 5% EUR move materially shifts reported revenue

- Hedging via forwards/options and natural offsets (~€Xbn hedged in 2024)

Urbanization and infrastructure demand

Rapid urbanization in Asia and Africa — UN projects 1.7 billion more urban residents by 2050, concentrated in these regions — drives sustained demand for transport and utility infrastructure, aligning with VINCI’s construction and concessions model.

Rising GDP per capita (IMF 2024: Sub-Saharan Africa ~3.5% growth; South Asia ~5%) enables user-pay tolls and PPPs, matching VINCI’s revenue-stable concession investments.

VINCI’s growth outside Europe hinges on winning bids in fast-growing markets; in 2024 concessions represented ~27% of group revenue, showing leverage if geographic expansion succeeds.

- Urban population +1.7B by 2050 (UN)

- Regional GDP growth: Africa ~3.5%, South Asia ~5% (IMF 2024)

- Concessions ~27% of VINCI 2024 revenue

High leverage (€57.5bn) and global revenues amid rising costs and recovering air traffic

Capital intensity: €57.5bn net debt (end‑2024); avg cost of debt ~2.8% (2024). Inflation/commodities: oil ~$85/bbl (2024), steel +18% (2024); French construction wages +4.5% (2024). Revenue mix: ~65% outside Eurozone; concessions ~27% of 2024 revenue; air traffic ~85% of 2019 (2024).

| Metric | 2024 |

|---|---|

| Net debt | €57.5bn |

| Cost of debt | ~2.8% |

| Revenue outside EZ | ~65% |

| Concessions | 27% |

Same Document Delivered

VINCI PESTLE Analysis

The preview shown here is the exact VINCI PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll download immediately after buying—no placeholders or teasers.

No surprises: this is the real, finished file, professionally structured and ready for application in your research or presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of VINCI—concise, expert-led insight into the political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; ideal for investors, advisors, and strategists. Purchase the full report to access ready-to-use, editable findings and actionable recommendations that save time and strengthen your decisions.

Political factors

Geopolitical stability and international expansion

VINCI operates in over 120 countries, so its €61.5bn 2023 revenue is highly sensitive to geopolitical tensions and France’s diplomatic ties with host nations.

Political shifts in key markets such as Brazil, Mexico and Southeast Asia threaten long-term concession security for assets like the €7.3bn VINCI Airports portfolio and large toll concessions.

Strategic planning must factor localized volatility risks that could delay projects, increase financing costs or trigger renegotiations, as seen in sector-wide 2022–24 risk premia rises.

Government infrastructure spending and stimulus

VINCI secures roughly 60% of revenues from public-sector contracts, so government infrastructure spending shapes backlog and margins; EU Recovery and Resilience Facility disbursements (over €723bn committed 2021–2026) and France’s €30bn France 2030 plan drive tender volumes for transport and urban works.

Regulatory oversight of concession contracts

As operator of ~4,400 km of motorways and 46 airports, VINCI faces intense political scrutiny on toll and aeronautical pricing; governments have capped toll rises in France (2024 cap ~2.6%) and renegotiated PPP terms affecting cash flows. State interventions risk reducing projected EBITDA for concession portfolios—concessions contributed ~55% of VINCI Concessions 2024 revenues (€13.8bn). Maintaining strong government ties is therefore critical to protect long-term contracted cash flows and credit metrics.

Trade policies and protectionism

Fluctuations in global trade policies and tariffs on inputs like steel (world steel price up ~15% in 2024 vs 2023) can raise VINCI construction costs and compress margins on large projects.

Rising protectionism and local content rules in markets such as the US and Brazil force VINCI to reconfigure supply chains and local hiring, increasing capex and operational complexity.

Active monitoring of trade agreements (e.g., EU–UK, USMCA updates) is vital to protect profitability on cross-border engineering contracts.

- Tariff-driven input cost volatility (steel, aluminum)

- Local content requirements raise sourcing and labor costs

- Need for trade-agreement monitoring to safeguard margins

Political focus on energy sovereignty

The EU’s push for energy sovereignty—EUR 300bn+ in Fit for 55-related investments and Member State nuclear revivals—boosts demand for VINCI’s nuclear and renewables engineering, aligning with VINCI Energies which reported 2024 revenue of ~EUR 19.1bn across energy services.

Political mandates to cut fossil fuels (targeting 55% emissions reduction by 2030) create procurement pipelines and government-backed projects where VINCI can leverage its EPC capabilities and capture public investment.

- EU energy investment >EUR 300bn (Fit for 55)

- VINCI Energies 2024 revenue ~EUR 19.1bn

- 2030 emissions cut target 55% drives public projects

VINCI: €61.5bn revenue, high political risk—public contracts, toll caps & rising costs

VINCI’s €61.5bn 2023 revenue and €13.8bn Concessions 2024 revenue are highly exposed to political risk across 120+ countries; public contracts ~60% of revenue; EU Recovery funds (€723bn) and Fit for 55 (>€300bn) drive tenders; toll caps (France 2024 ~2.6%) and tariff-driven steel +15% (2024 vs 2023) pressure margins; local content rules raise capex and operational complexity.

| Metric | Value |

|---|---|

| 2023 revenue | €61.5bn |

| Concessions 2024 rev | €13.8bn |

| Public-contract share | ~60% |

| EU Recovery | €723bn (2021–26) |

| Fit for 55 | >€300bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect VINCI across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise VINCI PESTLE summary that distills external risks and opportunities into clear categories for quick reference during meetings or presentations, helping teams align strategy and decision-making efficiently.

Economic factors

Interest rate environment and debt servicing

VINCI’s capital-intensive model relies on €57.5bn net debt at end-2024; higher rates in 2022–2024 raised average cost of debt to ~2.8% in 2024, squeezing concession margins and increasing project financing costs.

Persistently elevated rates made acquisitions pricier and delayed some bids, but rate stabilization and declines through 2025 opened refinancing windows, potentially lowering interest expense and enabling more acquisitive growth.

Inflationary pressures on material and labor costs

Volatility in energy, bitumen, steel and cement—steel futures rose ~18% in 2024 and global oil averaged $85/barrel in 2024—erodes margins on VINCI’s fixed‑price contracts, while inflation‑linked toll indexation in some concessions offsets only after implementation lags, creating short‑term margin pressure; managing rising labor costs (French construction wages up ~4.5% in 2024) through tighter project management and automation is a key economic challenge.

Global tourism and air traffic recovery

The economic health of VINCI Airports is closely linked to global travel demand and passenger disposable income; in 2024 global air passenger traffic reached about 85% of 2019 levels according to IATA, boosting passenger-related revenue. Economic slowdowns in key markets such as the EU or China can reduce flight frequencies and cut non-aeronautical income—retail and parking—already pressuring margins in 2023–24. Growth in aviation, notably in emerging markets where passenger volumes rose double digits in 2024, is critical for VINCI’s high-margin concession business. VINCI Airports’ 2024 traffic recovery supported a rebound in concession revenues versus 2022, underpinning EBITDA resilience.

Currency exchange rate fluctuations

With roughly 65% of VINCI’s 2024 revenue generated outside the Eurozone, the group faces transaction and translation exposure to the US dollar, British pound and various emerging-market currencies; a 5% EUR depreciation vs USD could raise reported overseas revenue materially.

Currency volatility can compress margins and weaken bid competitiveness in foreign tenders, as seen when FX swings affected unit bid costs in 2023–24.

VINCI uses hedging—forwards, options and natural hedges—to limit P&L and balance-sheet impacts, with net foreign exchange hedges reported at about €X billion in 2024.

- ~65% revenue outside Eurozone

- Exposure to USD, GBP and emerging currencies

- 5% EUR move materially shifts reported revenue

- Hedging via forwards/options and natural offsets (~€Xbn hedged in 2024)

Urbanization and infrastructure demand

Rapid urbanization in Asia and Africa — UN projects 1.7 billion more urban residents by 2050, concentrated in these regions — drives sustained demand for transport and utility infrastructure, aligning with VINCI’s construction and concessions model.

Rising GDP per capita (IMF 2024: Sub-Saharan Africa ~3.5% growth; South Asia ~5%) enables user-pay tolls and PPPs, matching VINCI’s revenue-stable concession investments.

VINCI’s growth outside Europe hinges on winning bids in fast-growing markets; in 2024 concessions represented ~27% of group revenue, showing leverage if geographic expansion succeeds.

- Urban population +1.7B by 2050 (UN)

- Regional GDP growth: Africa ~3.5%, South Asia ~5% (IMF 2024)

- Concessions ~27% of VINCI 2024 revenue

High leverage (€57.5bn) and global revenues amid rising costs and recovering air traffic

Capital intensity: €57.5bn net debt (end‑2024); avg cost of debt ~2.8% (2024). Inflation/commodities: oil ~$85/bbl (2024), steel +18% (2024); French construction wages +4.5% (2024). Revenue mix: ~65% outside Eurozone; concessions ~27% of 2024 revenue; air traffic ~85% of 2019 (2024).

| Metric | 2024 |

|---|---|

| Net debt | €57.5bn |

| Cost of debt | ~2.8% |

| Revenue outside EZ | ~65% |

| Concessions | 27% |

Same Document Delivered

VINCI PESTLE Analysis

The preview shown here is the exact VINCI PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are exactly what you’ll download immediately after buying—no placeholders or teasers.

No surprises: this is the real, finished file, professionally structured and ready for application in your research or presentations.