Virgin Money UK PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

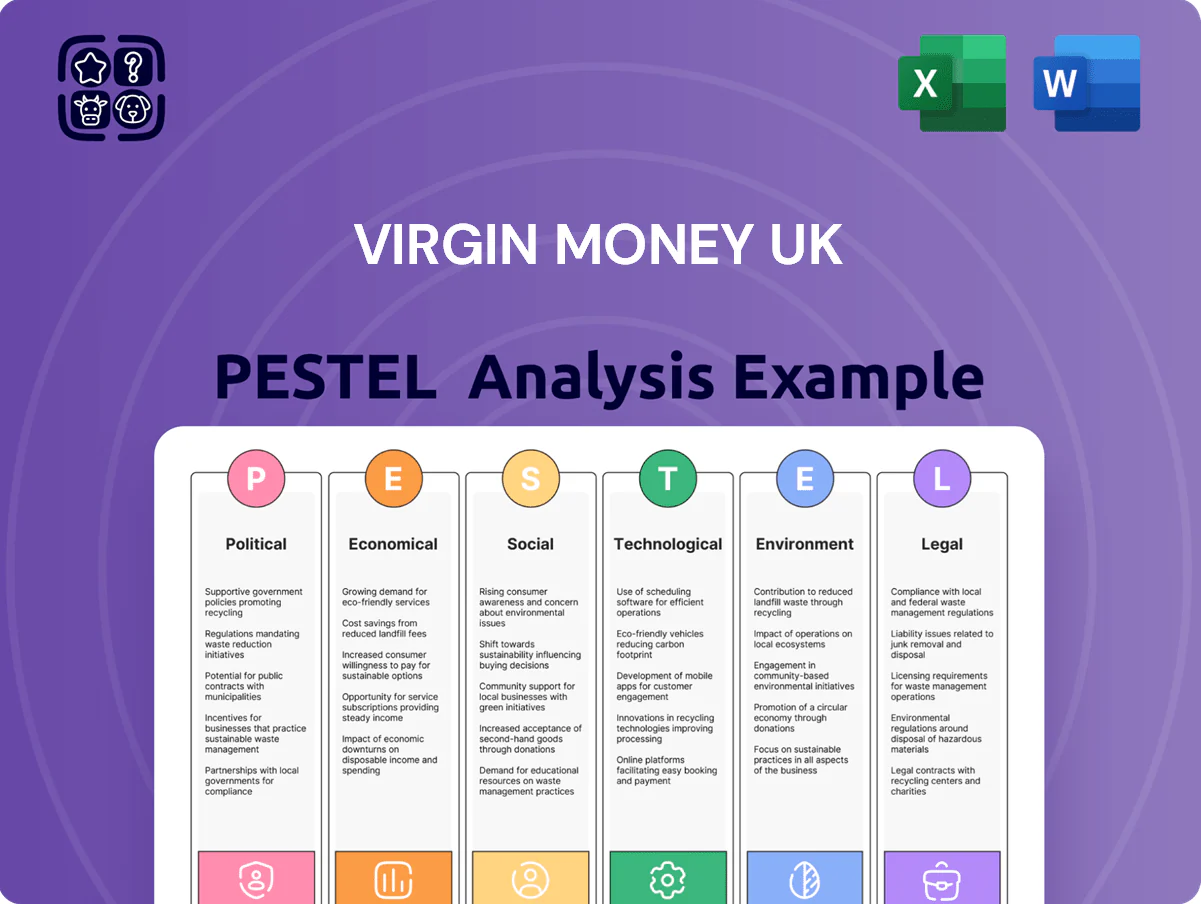

Gain a strategic advantage with our PESTLE Analysis of Virgin Money UK—concise, timely insights into the political, economic, social, technological, legal, and environmental forces shaping its prospects; ideal for investors and strategists. Purchase the full report to unlock detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Nationwide Acquisition Integration

By end-2025 the Nationwide–Virgin Money integration entered a critical phase, creating a combined balance sheet exceeding £300bn and altering UK retail banking concentration as the merged group holds ~18% of current account market share.

Regulators and Competition and Markets Authority oversight continue to demand safeguards to prevent reduced competition, influencing divestment and conduct commitments tied to the merger approval.

Ongoing dialogue with HM Treasury and the Bank of England is required to align the enlarged group's lending targets and branch commitments with UK economic priorities, including SME lending and regional access.

UK Government Housing Policies

UK government initiatives to boost home ownership and reform rentals—such as Help to Buy legacy impacts and proposed rental reforms—directly affect Virgin Money’s mortgage volumes; in 2024 UK mortgage approvals averaged ~63,000 per month, so shifts in schemes can move demand materially.

As a major mortgage provider, Virgin Money must adapt products to align with first-time buyer schemes and the 300,000 new homes target by 2025, affecting LTV mix and pricing strategies.

Changes in political leadership or housing strategy can rapidly shift residential lending demand across the UK, altering originations and credit risk profiles within quarters.

Regulatory Alignment Post-Brexit

As the UK refines its post-Brexit financial rules, Virgin Money faces evolving standards that may raise compliance costs; UK Treasury estimates in 2024 put additional regulatory conformity costs for banks at roughly 0.1–0.3% of operating income. Political choices on divergence versus alignment affect operational complexity and cross-border passporting, with 2025 trade negotiations and UK-EU equivalence reviews being material to strategy. Stability of UK relations with key markets like the US and EU remains critical for funding and capital access.

Fiscal Policy and Bank Levies

Decisions in the 2024 Autumn Statement and Spring Budget—such as the UK's 25% corporation tax on profits above £250,000 and the 2024 one-off bank levy proposals raising ~£1.2bn sector receipts—directly compress Virgin Money's net margins and ROE.

Political calls to tax banking windfalls risk ad hoc levies; a 1% profit-based surcharge could cut Virgin Money's 2025 pre-tax profit by an estimated ~£40–60m given 2024 profit run-rates.

Consequently, strategic planning must model scenarios for higher corporate tax and levy incidence to protect dividend policy and CET1 ratios.

- 2024 UK corporation tax rate 25% (profits >£250k)

- One-off bank levies ≈£1.2bn sector impact in 2024

- Estimated 1% profit surcharge ≈£40–60m hit to Virgin Money (2025 est.)

Geopolitical Stability and Trade

Ongoing geopolitical tensions, including Russia-Ukraine and US-China frictions, continue to weigh on UK trade and investment; UK goods exports fell 3.6% year-on-year in 2024 Q3, amplifying downside risks to growth.

Virgin Money, primarily UK-focused, remains exposed to indirect effects as weaker trade and investor caution reduced bank lending growth to small businesses to 1.2% in 2024.

Political volatility drives market swings that can raise bank funding costs—UK 10-year gilt yield rose to ~4.2% in late 2024—straining creditworthiness of business-banking clients and tightening margins.

- Geopolitical shocks depress trade and investment: UK exports -3.6% YoY (2024 Q3)

- Business lending growth slow: +1.2% (2024)

- Higher sovereign yields: UK 10y ~4.2% (late 2024)

Virgin Money political risks: taxes, levies, Brexit costs and macro shocks

Political risks for Virgin Money include post‑merger CMA/regulatory conditions, tax/levy changes (25% corp tax; 2024 one‑off bank levies ≈£1.2bn; 1% surcharge ≈£40–60m hit), Brexit rule divergence raising compliance costs (0.1–0.3% operating income), and macro impacts from geopolitical shocks (UK exports -3.6% YoY 2024 Q3; UK 10y ~4.2% late‑2024).

| Item | Metric |

|---|---|

| Corp tax rate | 25% (2024) |

| One‑off levies | ≈£1.2bn sector (2024) |

| Profit surcharge impact | ≈£40–60m (2025 est.) |

| Compliance cost | 0.1–0.3% operating income |

| UK exports | -3.6% YoY (2024 Q3) |

| UK 10y gilt | ~4.2% (late 2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Virgin Money UK, with data-driven trends and actionable insights to identify risks, opportunities, and strategic responses for executives and investors.

A concise, visually segmented PESTLE summary for Virgin Money UK that eases meeting prep, supports risk discussions and can be dropped into presentations or shared across teams for quick strategic alignment.

Economic factors

Bank of England Monetary Policy

The Bank of England base rate, which stood at 5.25% in December 2025, will be the primary determinant of Virgin Money’s net interest margin through 2025; a downshift from its 2023 peak compresses NIM if deposit repricing lags asset yields.

As UK CPI eased to 3.9% year-on-year in Dec 2025, falling inflation reduced upward rate pressure, prompting expectations of rate cuts that influence mortgage pricing and deposit costs across Virgin Money’s book.

Virgin Money must actively manage duration and funding mix—securing cheaper retail deposits and hedging fixed-rate mortgage exposures—to protect 2025 earnings amid a shifting BoE rate cycle.

Mortgage Market Competition

Economic pressure in the UK housing market has intensified competition as mortgage lending grew 6.8% year-on-year to £274bn in 2024, pushing lenders to protect loan book volumes.

Virgin Money faces stiff pricing pressure from high-street banks and digital challengers, with online mortgage share rising to ~22% in 2024.

Success hinges on offering competitive rates—average two-year fixed rates fell to 3.5% in late 2024—while preserving disciplined risk management and strict underwriting standards.

Cost of Living Credit Risk

SME Economic Sentiment

The health of the UK SME sector is central to Virgin Money’s business banking growth; SMEs contributed about 52% of private-sector turnover in 2023 and make up 99.9% of businesses, driving demand for deposits and lending.

Economic uncertainty — with GDP growth slowing to 0.2% QoQ in Q3 2024 and CPI at ~4% in late 2024 — can curb investment and reduce demand for commercial loans.

Conversely, sustained growth (BoE forecasts ~0.8%–1.2% in 2025) would enable Virgin Money to expand SME deposits and lending market share.

- SMEs = 99.9% of UK businesses; 52% private turnover (2023)

- Q3 2024 GDP growth 0.2% QoQ; CPI ~4% late 2024

- BoE 2025 GDP outlook ~0.8%–1.2%

Inflationary Pressure on Operating Costs

Persistent inflation pushed UK CPI to 4.0% in 2024, driving wage growth and higher third-party fees that pressure Virgin Money’s cost-to-income ratio, which rose to about 59% in H1 2024 per peer group data.

The bank must pursue strict cost controls and efficiency gains—targeting process automation and branch rationalisation—to offset rising operating expenses while funding digital transformation.

- Inflation 2024: UK CPI ~4.0%

- Virgin/peer cost-to-income ~59% H1 2024

- Actions: automation, branch cuts, tech investment trade-off

BoE 5.25% & CPI 3.9%: Mortgages, household strain and SME resilience

BoE base rate 5.25% (Dec 2025) drives NIM; UK CPI 3.9% (Dec 2025) eases rate pressure. Mortgage market: lending £274bn (2024), online share ~22%; two‑year fixed ~3.5% (late 2024). Household income -1.2% vs pre‑pandemic (Q3 2024); employment 74.8% (late 2024). SME: 99.9% businesses, 52% private turnover (2023); GDP Q3 2024 +0.2% QoQ.

| Metric | Value |

|---|---|

| BoE base rate | 5.25% (Dec 2025) |

| CPI | 3.9% (Dec 2025) |

| Mortgage lending | £274bn (2024) |

| Online mortgage share | ~22% (2024) |

| Employment | 74.8% (late 2024) |

Preview Before You Purchase

Virgin Money UK PESTLE Analysis

The preview shown here is the exact Virgin Money UK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Virgin Money UK—concise, timely insights into the political, economic, social, technological, legal, and environmental forces shaping its prospects; ideal for investors and strategists. Purchase the full report to unlock detailed risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Nationwide Acquisition Integration

By end-2025 the Nationwide–Virgin Money integration entered a critical phase, creating a combined balance sheet exceeding £300bn and altering UK retail banking concentration as the merged group holds ~18% of current account market share.

Regulators and Competition and Markets Authority oversight continue to demand safeguards to prevent reduced competition, influencing divestment and conduct commitments tied to the merger approval.

Ongoing dialogue with HM Treasury and the Bank of England is required to align the enlarged group's lending targets and branch commitments with UK economic priorities, including SME lending and regional access.

UK Government Housing Policies

UK government initiatives to boost home ownership and reform rentals—such as Help to Buy legacy impacts and proposed rental reforms—directly affect Virgin Money’s mortgage volumes; in 2024 UK mortgage approvals averaged ~63,000 per month, so shifts in schemes can move demand materially.

As a major mortgage provider, Virgin Money must adapt products to align with first-time buyer schemes and the 300,000 new homes target by 2025, affecting LTV mix and pricing strategies.

Changes in political leadership or housing strategy can rapidly shift residential lending demand across the UK, altering originations and credit risk profiles within quarters.

Regulatory Alignment Post-Brexit

As the UK refines its post-Brexit financial rules, Virgin Money faces evolving standards that may raise compliance costs; UK Treasury estimates in 2024 put additional regulatory conformity costs for banks at roughly 0.1–0.3% of operating income. Political choices on divergence versus alignment affect operational complexity and cross-border passporting, with 2025 trade negotiations and UK-EU equivalence reviews being material to strategy. Stability of UK relations with key markets like the US and EU remains critical for funding and capital access.

Fiscal Policy and Bank Levies

Decisions in the 2024 Autumn Statement and Spring Budget—such as the UK's 25% corporation tax on profits above £250,000 and the 2024 one-off bank levy proposals raising ~£1.2bn sector receipts—directly compress Virgin Money's net margins and ROE.

Political calls to tax banking windfalls risk ad hoc levies; a 1% profit-based surcharge could cut Virgin Money's 2025 pre-tax profit by an estimated ~£40–60m given 2024 profit run-rates.

Consequently, strategic planning must model scenarios for higher corporate tax and levy incidence to protect dividend policy and CET1 ratios.

- 2024 UK corporation tax rate 25% (profits >£250k)

- One-off bank levies ≈£1.2bn sector impact in 2024

- Estimated 1% profit surcharge ≈£40–60m hit to Virgin Money (2025 est.)

Geopolitical Stability and Trade

Ongoing geopolitical tensions, including Russia-Ukraine and US-China frictions, continue to weigh on UK trade and investment; UK goods exports fell 3.6% year-on-year in 2024 Q3, amplifying downside risks to growth.

Virgin Money, primarily UK-focused, remains exposed to indirect effects as weaker trade and investor caution reduced bank lending growth to small businesses to 1.2% in 2024.

Political volatility drives market swings that can raise bank funding costs—UK 10-year gilt yield rose to ~4.2% in late 2024—straining creditworthiness of business-banking clients and tightening margins.

- Geopolitical shocks depress trade and investment: UK exports -3.6% YoY (2024 Q3)

- Business lending growth slow: +1.2% (2024)

- Higher sovereign yields: UK 10y ~4.2% (late 2024)

Virgin Money political risks: taxes, levies, Brexit costs and macro shocks

Political risks for Virgin Money include post‑merger CMA/regulatory conditions, tax/levy changes (25% corp tax; 2024 one‑off bank levies ≈£1.2bn; 1% surcharge ≈£40–60m hit), Brexit rule divergence raising compliance costs (0.1–0.3% operating income), and macro impacts from geopolitical shocks (UK exports -3.6% YoY 2024 Q3; UK 10y ~4.2% late‑2024).

| Item | Metric |

|---|---|

| Corp tax rate | 25% (2024) |

| One‑off levies | ≈£1.2bn sector (2024) |

| Profit surcharge impact | ≈£40–60m (2025 est.) |

| Compliance cost | 0.1–0.3% operating income |

| UK exports | -3.6% YoY (2024 Q3) |

| UK 10y gilt | ~4.2% (late 2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Virgin Money UK, with data-driven trends and actionable insights to identify risks, opportunities, and strategic responses for executives and investors.

A concise, visually segmented PESTLE summary for Virgin Money UK that eases meeting prep, supports risk discussions and can be dropped into presentations or shared across teams for quick strategic alignment.

Economic factors

Bank of England Monetary Policy

The Bank of England base rate, which stood at 5.25% in December 2025, will be the primary determinant of Virgin Money’s net interest margin through 2025; a downshift from its 2023 peak compresses NIM if deposit repricing lags asset yields.

As UK CPI eased to 3.9% year-on-year in Dec 2025, falling inflation reduced upward rate pressure, prompting expectations of rate cuts that influence mortgage pricing and deposit costs across Virgin Money’s book.

Virgin Money must actively manage duration and funding mix—securing cheaper retail deposits and hedging fixed-rate mortgage exposures—to protect 2025 earnings amid a shifting BoE rate cycle.

Mortgage Market Competition

Economic pressure in the UK housing market has intensified competition as mortgage lending grew 6.8% year-on-year to £274bn in 2024, pushing lenders to protect loan book volumes.

Virgin Money faces stiff pricing pressure from high-street banks and digital challengers, with online mortgage share rising to ~22% in 2024.

Success hinges on offering competitive rates—average two-year fixed rates fell to 3.5% in late 2024—while preserving disciplined risk management and strict underwriting standards.

Cost of Living Credit Risk

SME Economic Sentiment

The health of the UK SME sector is central to Virgin Money’s business banking growth; SMEs contributed about 52% of private-sector turnover in 2023 and make up 99.9% of businesses, driving demand for deposits and lending.

Economic uncertainty — with GDP growth slowing to 0.2% QoQ in Q3 2024 and CPI at ~4% in late 2024 — can curb investment and reduce demand for commercial loans.

Conversely, sustained growth (BoE forecasts ~0.8%–1.2% in 2025) would enable Virgin Money to expand SME deposits and lending market share.

- SMEs = 99.9% of UK businesses; 52% private turnover (2023)

- Q3 2024 GDP growth 0.2% QoQ; CPI ~4% late 2024

- BoE 2025 GDP outlook ~0.8%–1.2%

Inflationary Pressure on Operating Costs

Persistent inflation pushed UK CPI to 4.0% in 2024, driving wage growth and higher third-party fees that pressure Virgin Money’s cost-to-income ratio, which rose to about 59% in H1 2024 per peer group data.

The bank must pursue strict cost controls and efficiency gains—targeting process automation and branch rationalisation—to offset rising operating expenses while funding digital transformation.

- Inflation 2024: UK CPI ~4.0%

- Virgin/peer cost-to-income ~59% H1 2024

- Actions: automation, branch cuts, tech investment trade-off

BoE 5.25% & CPI 3.9%: Mortgages, household strain and SME resilience

BoE base rate 5.25% (Dec 2025) drives NIM; UK CPI 3.9% (Dec 2025) eases rate pressure. Mortgage market: lending £274bn (2024), online share ~22%; two‑year fixed ~3.5% (late 2024). Household income -1.2% vs pre‑pandemic (Q3 2024); employment 74.8% (late 2024). SME: 99.9% businesses, 52% private turnover (2023); GDP Q3 2024 +0.2% QoQ.

| Metric | Value |

|---|---|

| BoE base rate | 5.25% (Dec 2025) |

| CPI | 3.9% (Dec 2025) |

| Mortgage lending | £274bn (2024) |

| Online mortgage share | ~22% (2024) |

| Employment | 74.8% (late 2024) |

Preview Before You Purchase

Virgin Money UK PESTLE Analysis

The preview shown here is the exact Virgin Money UK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.