Vitesco Technologies Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

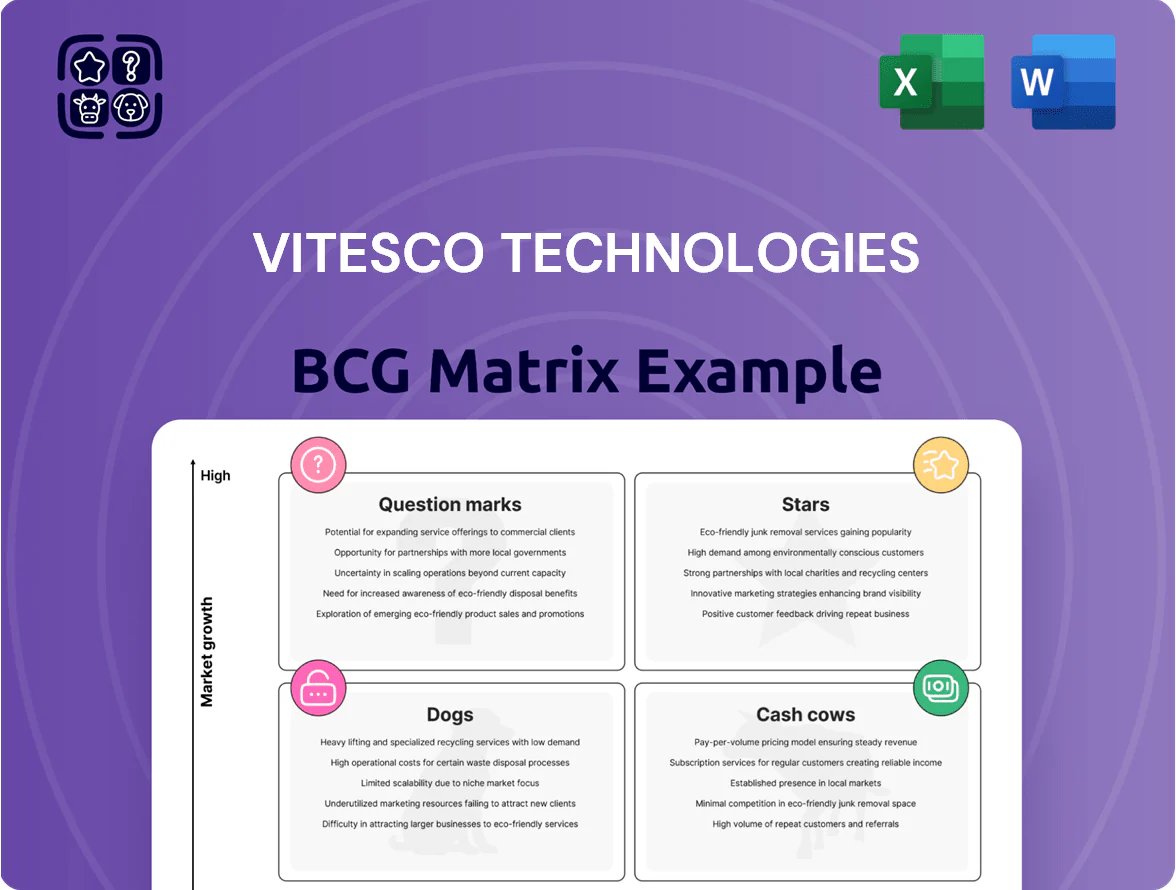

Vitesco Technologies shows mixed signals across powertrain segments—some electrification products behave like emerging Stars with high growth potential, while legacy ICE components resemble Cash Cows sustaining cash flow; a few niche lines risk becoming Dogs without strategic reinvestment. This preview highlights where competitive strength and market growth diverge, but the full BCG Matrix maps each product into its quadrant with data-driven scoring and strategic implications. Purchase the complete report for quadrant-by-quadrant recommendations, editable Word and Excel deliverables, and a clear roadmap to optimize portfolio allocation.

Stars

Integrated Axle Drives

The EMR4 and upcoming EMR5 platforms are Vitesco Technologies’ flagship high-growth integrated axle drives, combining motor, inverter and reduction gear into one unit and holding roughly a 22% global OEM share in BEV powertrains as of 2025.

Vitesco invested €420 million into EMR programs in 2024–2025 to scale production; management targets 30% revenue CAGR for EMR products through 2026 as global BEV stock rises toward 200 million vehicles by 2030.

High-Voltage Inverters

Vitesco Technologies’ silicon carbide high-voltage inverters lead the premium EV segment, supplying about 35% of 800V platform vehicles in 2025 and driving roughly €1.2bn revenue under multi-year contracts.

The 800-volt focus gives a durable moat via ~98% peak conversion efficiency and 20–30% lower cooling needs, but R&D runs near €150m/year to maintain edge against Infineon and STMicro.

Battery Management Systems

Vitesco Technologies leads in high-voltage battery management systems (BMS), supplying modular hardware and software used across BEVs; the unit captures a double-digit market share in a global BMS market growing ~18% CAGR to $48B by 2028 (Forecast 2025–28).

Modular, scalable BMS designs let Vitesco serve compact to luxury segments, supporting estimated 2025 BMS revenues near €350M and keeping share expansion in fast-growing electrified powertrain demand.

The push into wireless BMS (over-the-air cell monitoring and reduced wiring) positions this business as a Star, with pilots announced 2024–25 and anticipated margin upside as adoption rises.

Thermal Management Systems

Thermal Management Systems: Efficient heating and cooling are critical for EV range, making Vitesco Technologies AGs integrated thermal management modules a high-growth priority; Vitesco reported a 2024 order backlog growth of ~12% in electrification segments, reflecting strong OEM demand.

By combining pumps, valves, and sensors into unified modules, Vitesco has become a go-to supplier for OEMs simplifying vehicle architecture; integrated modules can reduce system mass by ~8% and lower installation time, boosting adoption.

This segment attracts heavy investment to optimize fluid control and energy efficiency for next-generation platforms; Vitesco invested ~EUR 120m in e-thermal R&D in 2024 to improve COP and reduce parasitic losses.

- High growth: 12% 2024 backlog rise

- Integration benefit: ~8% mass reduction

- R&D spend: ~EUR 120m in 2024

- Focus: fluid control, COP, parasitic loss cuts

Power Electronics for Hybrids

Power Electronics for Hybrids is a Star: plug-in hybrid (PHEV) market projected to grow ~9% CAGR to 2030, and Vitesco (FY2024 revenue €7.1bn) leads with DC/DC converters and power distribution modules that cut system losses by up to 12% in real tests.

Their modules enable complex hybrid powertrains and higher electrification share as global CO2 rules tighten; EU CO2 fleet targets 2025–2030 push OEM demand, keeping this segment high-margin and capex-light for Vitesco.

- Market: PHEV ~9% CAGR to 2030

- Vitesco FY2024 sales €7.1bn

- Tech: DC/DC cut losses ~12%

- Drivers: stricter CO2 regs 2025–2030

Vitesco bets big: EMR/SiC stars and BMS/thermal R&D fuel strong 2025 growth

Vitesco’s EMR4/EMR5 axle drives, 22% OEM BEV share (2025), and 800V SiC inverters (35% of 800V cars; ~€1.2bn revenue 2025) form Stars, backed by €420m EMR capex (2024–25) and ~€150m/year SiC R&D; BMS (~€350m 2025) and thermal modules (12% 2024 backlog growth; €120m e-thermal R&D 2024) add growth and margin upside.

| Item | Key metric |

|---|---|

| EMR share | 22% (2025) |

| EMR capex | €420m (2024–25) |

| SiC inverters | 35% of 800V; €1.2bn (2025) |

| SiC R&D | ~€150m/yr |

| BMS revenue | ~€350m (2025) |

| Thermal backlog | +12% (2024) |

| e-thermal R&D | €120m (2024) |

What is included in the product

Comprehensive BCG Matrix for Vitesco: identifies Stars, Cash Cows, Question Marks, Dogs with strategic actions, risks, and investment priorities.

One-page overview placing each Vitesco business unit in a quadrant to streamline strategic decisions and investor briefings.

Cash Cows

Electronic Control Units

Vitesco Technologies’ electronic control units (ECUs) for internal combustion engines generate steady, high-margin cash: 2024 segment revenue from powertrain products was about EUR 2.1 billion, with ECU legacy lines contributing a majority and requiring minimal capex as the market is mature and low-growth (global ICE vehicle production fell ~4% in 2023–24).

These ECUs hold top market share in core ICE applications, giving predictable free cash flow; operating margins on legacy powertrain products stayed above 12% in 2024, funding R&D and capex for electrification programs.

Management uses ECU cash to accelerate electromobility: Vitesco invested EUR 450 million in 2024–2025 into e-powertrain and software, financed largely by legacy ECU profitability, so transition funding is de-risked while demand for ICE control units tapers slowly.

Sensors for Combustion Engines

Pressure, temperature, and NOx sensors for combustion engines remain Vitesco Technologies’ cash cows, supplying sensors to roughly 50–60 million internal combustion vehicles produced annually as of 2024; with a fully depreciated manufacturing base these parts yield margins north of 20% and require minimal marketing.

They generated an estimated €400–500 million in steady EBIT contribution in 2024, funding debt service and R&D for electrification programs while needing little capex; these sensors act as a reliable cash engine during the transition to e-mobility.

Actuators and Solenoids

Mechanical actuators and solenoids for traditional transmissions and engine air management are in peak maturity with Vitesco holding high market share; standardized designs across platforms drive unit costs down and gross margins up—R&D-light production.

These modules deliver steady cash flow: in FY2024 Vitesco reported ~€1.8bn segment revenue (electromechanical & electrification combined) with cash from legacy actuator lines funding Electrification Solutions’ 2024–25 capex ramp.

Dosing Systems

Vitesco’s Selective Catalytic Reduction (SCR) dosing systems are cash cows: mature tech with ~15–20% global market share in diesel SCR modules (2024), low market growth (~2% CAGR to 2029) and stable OEM plus aftermarket demand, delivering predictable margins and steady free cash flow.

- Market share: ~15–20% (2024)

- Growth: ~2% CAGR (2024–29)

- Drivers: strict but stable emissions regs

- Revenue mix: steady OEM + replacement orders

Transmission Controllers

The market for conventional automatic and dual-clutch transmission control units (TCUs) is mature, with global vehicle production of ~78 million light vehicles in 2024 and stable TCU demand generating high-volume revenue for Vitesco Technologies (Vitesco SE, listed; fiscal 2024 revenue €8.2bn).

Vitesco optimized TCU production over decades, delivering low unit costs and gross margins above company average; TCUs require minimal capex—maintenance-level tooling spend under 5% of segment revenue—making them a reliable cash source for R&D and electrification investments.

- High-volume stable demand: ~78M LVs (2024)

- Contributes to Vitesco 2024 revenue €8.2bn

- Low capex: <5% of segment revenue

- Lean cost base → above-average gross margins

Vitesco’s ICE components: €2.7–3.0bn revenue, ~€0.8–1.0bn EBIT — high margins, low capex

Vitesco’s ICE ECUs, sensors, actuators, TCUs and SCR modules were stable cash cows in 2024, collectively generating ~€2.7–3.0bn revenue and ~€800–1,000m EBIT (2024), funding €450m electrification capex (2024–25) while requiring low maintenance capex and showing high margins (sensors ~20%+, ECUs ~12%+).

| Product | 2024 rev (€bn) | EBIT est (€m) | Margin | Capex need |

|---|---|---|---|---|

| ECUs | 2.1 | 250–300 | 12%+ | low |

| Sensors | 0.5 | 200–250 | 20%+ | very low |

| Actuators/TCUs | 0.9 | 200–300 | above avg | low |

| SCR | 0.2 | 100–150 | 15–20% | low |

Full Transparency, Always

Vitesco Technologies BCG Matrix

The file you're previewing is the exact Vitesco Technologies BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just a fully formatted, strategy-ready document crafted with market-backed analysis for immediate use in presentations, planning, or client deliverables.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Vitesco Technologies shows mixed signals across powertrain segments—some electrification products behave like emerging Stars with high growth potential, while legacy ICE components resemble Cash Cows sustaining cash flow; a few niche lines risk becoming Dogs without strategic reinvestment. This preview highlights where competitive strength and market growth diverge, but the full BCG Matrix maps each product into its quadrant with data-driven scoring and strategic implications. Purchase the complete report for quadrant-by-quadrant recommendations, editable Word and Excel deliverables, and a clear roadmap to optimize portfolio allocation.

Stars

Integrated Axle Drives

The EMR4 and upcoming EMR5 platforms are Vitesco Technologies’ flagship high-growth integrated axle drives, combining motor, inverter and reduction gear into one unit and holding roughly a 22% global OEM share in BEV powertrains as of 2025.

Vitesco invested €420 million into EMR programs in 2024–2025 to scale production; management targets 30% revenue CAGR for EMR products through 2026 as global BEV stock rises toward 200 million vehicles by 2030.

High-Voltage Inverters

Vitesco Technologies’ silicon carbide high-voltage inverters lead the premium EV segment, supplying about 35% of 800V platform vehicles in 2025 and driving roughly €1.2bn revenue under multi-year contracts.

The 800-volt focus gives a durable moat via ~98% peak conversion efficiency and 20–30% lower cooling needs, but R&D runs near €150m/year to maintain edge against Infineon and STMicro.

Battery Management Systems

Vitesco Technologies leads in high-voltage battery management systems (BMS), supplying modular hardware and software used across BEVs; the unit captures a double-digit market share in a global BMS market growing ~18% CAGR to $48B by 2028 (Forecast 2025–28).

Modular, scalable BMS designs let Vitesco serve compact to luxury segments, supporting estimated 2025 BMS revenues near €350M and keeping share expansion in fast-growing electrified powertrain demand.

The push into wireless BMS (over-the-air cell monitoring and reduced wiring) positions this business as a Star, with pilots announced 2024–25 and anticipated margin upside as adoption rises.

Thermal Management Systems

Thermal Management Systems: Efficient heating and cooling are critical for EV range, making Vitesco Technologies AGs integrated thermal management modules a high-growth priority; Vitesco reported a 2024 order backlog growth of ~12% in electrification segments, reflecting strong OEM demand.

By combining pumps, valves, and sensors into unified modules, Vitesco has become a go-to supplier for OEMs simplifying vehicle architecture; integrated modules can reduce system mass by ~8% and lower installation time, boosting adoption.

This segment attracts heavy investment to optimize fluid control and energy efficiency for next-generation platforms; Vitesco invested ~EUR 120m in e-thermal R&D in 2024 to improve COP and reduce parasitic losses.

- High growth: 12% 2024 backlog rise

- Integration benefit: ~8% mass reduction

- R&D spend: ~EUR 120m in 2024

- Focus: fluid control, COP, parasitic loss cuts

Power Electronics for Hybrids

Power Electronics for Hybrids is a Star: plug-in hybrid (PHEV) market projected to grow ~9% CAGR to 2030, and Vitesco (FY2024 revenue €7.1bn) leads with DC/DC converters and power distribution modules that cut system losses by up to 12% in real tests.

Their modules enable complex hybrid powertrains and higher electrification share as global CO2 rules tighten; EU CO2 fleet targets 2025–2030 push OEM demand, keeping this segment high-margin and capex-light for Vitesco.

- Market: PHEV ~9% CAGR to 2030

- Vitesco FY2024 sales €7.1bn

- Tech: DC/DC cut losses ~12%

- Drivers: stricter CO2 regs 2025–2030

Vitesco bets big: EMR/SiC stars and BMS/thermal R&D fuel strong 2025 growth

Vitesco’s EMR4/EMR5 axle drives, 22% OEM BEV share (2025), and 800V SiC inverters (35% of 800V cars; ~€1.2bn revenue 2025) form Stars, backed by €420m EMR capex (2024–25) and ~€150m/year SiC R&D; BMS (~€350m 2025) and thermal modules (12% 2024 backlog growth; €120m e-thermal R&D 2024) add growth and margin upside.

| Item | Key metric |

|---|---|

| EMR share | 22% (2025) |

| EMR capex | €420m (2024–25) |

| SiC inverters | 35% of 800V; €1.2bn (2025) |

| SiC R&D | ~€150m/yr |

| BMS revenue | ~€350m (2025) |

| Thermal backlog | +12% (2024) |

| e-thermal R&D | €120m (2024) |

What is included in the product

Comprehensive BCG Matrix for Vitesco: identifies Stars, Cash Cows, Question Marks, Dogs with strategic actions, risks, and investment priorities.

One-page overview placing each Vitesco business unit in a quadrant to streamline strategic decisions and investor briefings.

Cash Cows

Electronic Control Units

Vitesco Technologies’ electronic control units (ECUs) for internal combustion engines generate steady, high-margin cash: 2024 segment revenue from powertrain products was about EUR 2.1 billion, with ECU legacy lines contributing a majority and requiring minimal capex as the market is mature and low-growth (global ICE vehicle production fell ~4% in 2023–24).

These ECUs hold top market share in core ICE applications, giving predictable free cash flow; operating margins on legacy powertrain products stayed above 12% in 2024, funding R&D and capex for electrification programs.

Management uses ECU cash to accelerate electromobility: Vitesco invested EUR 450 million in 2024–2025 into e-powertrain and software, financed largely by legacy ECU profitability, so transition funding is de-risked while demand for ICE control units tapers slowly.

Sensors for Combustion Engines

Pressure, temperature, and NOx sensors for combustion engines remain Vitesco Technologies’ cash cows, supplying sensors to roughly 50–60 million internal combustion vehicles produced annually as of 2024; with a fully depreciated manufacturing base these parts yield margins north of 20% and require minimal marketing.

They generated an estimated €400–500 million in steady EBIT contribution in 2024, funding debt service and R&D for electrification programs while needing little capex; these sensors act as a reliable cash engine during the transition to e-mobility.

Actuators and Solenoids

Mechanical actuators and solenoids for traditional transmissions and engine air management are in peak maturity with Vitesco holding high market share; standardized designs across platforms drive unit costs down and gross margins up—R&D-light production.

These modules deliver steady cash flow: in FY2024 Vitesco reported ~€1.8bn segment revenue (electromechanical & electrification combined) with cash from legacy actuator lines funding Electrification Solutions’ 2024–25 capex ramp.

Dosing Systems

Vitesco’s Selective Catalytic Reduction (SCR) dosing systems are cash cows: mature tech with ~15–20% global market share in diesel SCR modules (2024), low market growth (~2% CAGR to 2029) and stable OEM plus aftermarket demand, delivering predictable margins and steady free cash flow.

- Market share: ~15–20% (2024)

- Growth: ~2% CAGR (2024–29)

- Drivers: strict but stable emissions regs

- Revenue mix: steady OEM + replacement orders

Transmission Controllers

The market for conventional automatic and dual-clutch transmission control units (TCUs) is mature, with global vehicle production of ~78 million light vehicles in 2024 and stable TCU demand generating high-volume revenue for Vitesco Technologies (Vitesco SE, listed; fiscal 2024 revenue €8.2bn).

Vitesco optimized TCU production over decades, delivering low unit costs and gross margins above company average; TCUs require minimal capex—maintenance-level tooling spend under 5% of segment revenue—making them a reliable cash source for R&D and electrification investments.

- High-volume stable demand: ~78M LVs (2024)

- Contributes to Vitesco 2024 revenue €8.2bn

- Low capex: <5% of segment revenue

- Lean cost base → above-average gross margins

Vitesco’s ICE components: €2.7–3.0bn revenue, ~€0.8–1.0bn EBIT — high margins, low capex

Vitesco’s ICE ECUs, sensors, actuators, TCUs and SCR modules were stable cash cows in 2024, collectively generating ~€2.7–3.0bn revenue and ~€800–1,000m EBIT (2024), funding €450m electrification capex (2024–25) while requiring low maintenance capex and showing high margins (sensors ~20%+, ECUs ~12%+).

| Product | 2024 rev (€bn) | EBIT est (€m) | Margin | Capex need |

|---|---|---|---|---|

| ECUs | 2.1 | 250–300 | 12%+ | low |

| Sensors | 0.5 | 200–250 | 20%+ | very low |

| Actuators/TCUs | 0.9 | 200–300 | above avg | low |

| SCR | 0.2 | 100–150 | 15–20% | low |

Full Transparency, Always

Vitesco Technologies BCG Matrix

The file you're previewing is the exact Vitesco Technologies BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just a fully formatted, strategy-ready document crafted with market-backed analysis for immediate use in presentations, planning, or client deliverables.