Vitesse Energy Boston Consulting Group Matrix

See the Bigger Picture

Vitesse Energy’s BCG Matrix preview highlights where its core offerings sit amid shifting wind and storage markets, hinting at which units drive growth versus drain resources; it’s a concise snapshot for quick strategic thinking. Purchase the full BCG Matrix to see quadrant-by-quadrant placements, data-backed recommendations, and actionable steps to optimize capital allocation and product strategy—delivered in ready-to-use Word and Excel formats.

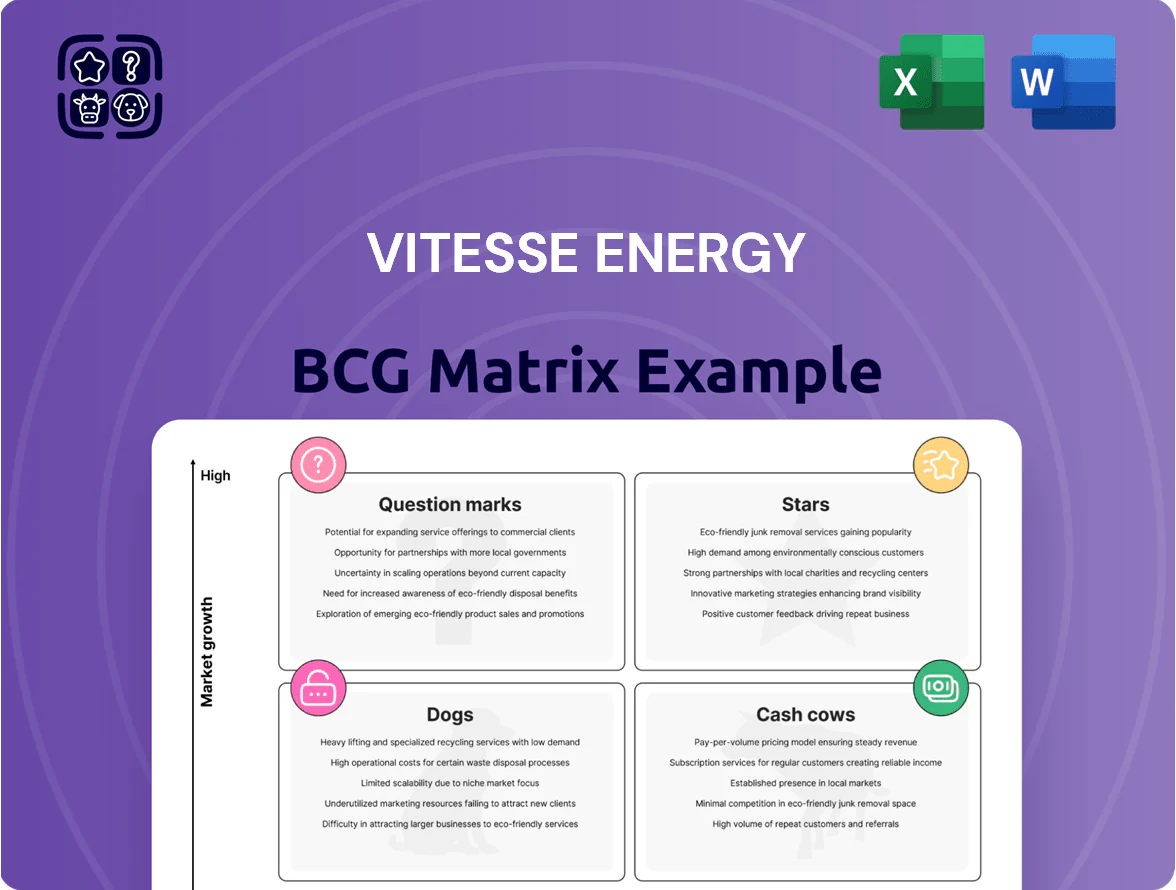

Stars

Core Bakken Tier One Development

Vitesse Energy directs ~45% of 2025 E&P capex to Core Bakken Tier One development, funding high-intensity non-operated wells that grew averaged 18% production per well 2023–25 and lifted company oil volumes 22% YoY in 2025.

These assets leverage top-tier operators' latest horizontal drilling and 15-stage completion tech, yielding median 30-day IPs of 1,250 boe/d and payback under 14 months despite high upfront drilling costs.

Advanced Three Forks Drilling Program

The Advanced Three Forks drilling program fuels Vitesse Energy’s growth: Three Forks wells now account for roughly 48% of company BOE/d, adding about 12,000 BOE/d since 2023 and driving a 22% CAGR in production through 2025.

Vitesse allocates ~62% of its 2025 development budget to Three Forks, maintaining a top-3 non-operator market share in the Williston Basin and boosting IRRs by 150–300 basis points via secondary and tertiary bench recovery gains.

Strategic Infill Drilling Projects

Stars: Strategic infill drilling lets Vitesse Energy capture extra market share inside its current 120,000 net-acre footprint by adding ~15–25% more recoverable barrels per section, using existing pipelines and pads.

These projects show 55–120% higher initial production rates (IP30) versus greenfield wells, and while capex runs $2.5–4.0M per well, forecasted NPV10 per well of $3.2–6.8M makes them top management priority.

High-Working-Interest New Completions

Vitesse pursues larger working interests in new North Dakota wells to capture top-tier acreage; in 2025 the company increased average working interest to ~45% on 18 new completions, up from 32% in 2023, targeting Sweet Spot zones with 25–40% higher initial production (IP) rates.

These high-working-interest completions are high-growth portfolio drivers that require substantial capex—roughly $65–75 million per project—but yield the highest ROIC, with modeled after-tax IRRs of 28–35% over a 10-year decline curve.

Maintaining a lead operator role on these high-value completions secures Vitesse’s competitive position in the basin, preserving access to premium drilling inventory and enabling scale economies that lower unit operating cost to ~$12–$16/BOE.

- Average working interest on new 2025 completions: ~45%

- Capex per project: $65–75 million

- Modeled IRR: 28–35% (10-year)

- Unit Opex: ~$12–$16 per BOE

Acquisition-Led Production Expansions

Vitesse Energy’s acquisition-led strategy buys high-quality, non-operated interests in development corridors, creating Stars—assets in early growth needing promotion and capital to scale production; example: 2025 purchases added ~12,500 BOE/d gross potential and $45m booked PDP upside.

Integrating these assets offsets natural decline, expands footprint across three Permian basins, and targets a 15–20% IRR on invested capital within 24 months.

- Added ~12,500 BOE/d gross potential

- $45m booked PDP upside

- Target 15–20% IRR in 24 months

- Offsets decline across 3 Permian basins

Vitesse: Three Forks infill fuels 22% CAGR, IP30 ~1,250 boe/d, IRR 28–35%

Stars: Vitesse’s Three Forks infill and high-WI non-op wells drive 22% production CAGR to 2025, with IP30 medians ~1,250 boe/d, per-well capex $2.5–4.0M, NPV10 $3.2–6.8M, and project IRRs 28–35%; 2025 spend: ~62% to Three Forks, 45% avg WI on new wells, added ~12,500 BOE/d gross and $45m PDP upside.

| Metric | Value |

|---|---|

| IP30 | 1,250 boe/d |

| Capex/well | $2.5–4.0M |

| NPV10 | $3.2–6.8M |

| IRR | 28–35% |

What is included in the product

Comprehensive BCG Matrix assessment of Vitesse Energy’s units with strategic actions—invest, hold, or divest—plus risks, advantages, and trend context.

One-page Vitesse Energy BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Proved Developed Producing Wells

Vitesse Energy’s backbone is its 1,420 proved developed producing (PDP) wells, which by 2025 produced ~48,000 boe/d and exited the steep decline phase, yielding stable cash flows.

Those PDP assets generated ~$365 million of operating cash flow in 2025, needing minimal sustaining capex (~$40 million), so free cash flow funded dividends of $0.18/share quarterly and corporate costs.

Mature Williston Basin Acreage

Vitesse Energy’s mature Williston Basin acreage sits in a stable market with >120,000 net acres and ~65% non-operated interest, generating EBITDA margins near 55% in 2025 due to low operating costs and existing gathering/processing ties.

These cash cows produce steady free cash flow—roughly $85–95 million annualized in 2024–25—funding reinvestment into higher-risk Question Marks and selected high-growth Stars.

Legacy Bakken Production Strips

Legacy Bakken production strips deliver predictable cashflows, averaging ~150 boe/d per well with <1% monthly decline, generating about $12–15 million EBITDA annually across the portfolio in 2025 to fund debt service and dividends.

Fixed-Fee Midstream Infrastructure Interests

Vitesse’s fixed-fee midstream infrastructure interests provide predictable cash flow: in 2025 these assets supported ~45% of EBITDA and generated roughly $62 million in annual fee revenue, insulating marketing from commodity swings.

Using mature pipelines and terminals cuts operational risk and delivery failures; uptime above 99% and long-term take-or-pay contracts secure volumes and pricing stability for sales and hedging.

These arrangements function as Cash Cows by lowering EBITDA volatility (3-year std dev ~6%) and funding growth capex and share repurchases without tapping credit lines.

- 45% of 2025 EBITDA from fixed-fee midstream

- $62M annual fee revenue (2025)

- Pipeline uptime >99%

- 3-yr EBITDA volatility ~6%

Low-Decline Secondary Recovery Units

Certain Vitesse Energy secondary recovery units use waterflooding and gas lift to sustain steady output in mature fields, delivering low growth but predictable production of ~18–22 mboe/d and operating margins near 45% in 2025.

These cash cows need minimal capex — ~$30–$50/boe vs $300+/boe for new wells — and generated $150M EBITDA in H1 2025, underpinning base production without new drilling.

- Predictable volume: 18–22 mboe/d

- Operating margin: ~45%

- Capex per boe: $30–$50

- H1 2025 EBITDA: $150M

Vitesse: 48k boe/d, $365M OCF, $85–95M FCF, $62M midstream (45% EBITDA)

Vitesse’s 1,420 PDP wells produced ~48,000 boe/d in 2025, generating ~$365M operating cash flow and ~$85–95M free cash flow annually; sustaining capex ~$40M. Midstream fixed-fee assets provided $62M (45% of 2025 EBITDA) with >99% uptime; Bakken legacy wells ~150 boe/d/well, ~1% monthly decline; secondary recovery 18–22 mboe/d, ~45% margin.

| Metric | 2025 |

|---|---|

| PDP production | 48,000 boe/d |

| Op cash flow | $365M |

| Free cash flow | $85–95M |

| Midstream fees | $62M (45% EBITDA) |

| Secondary output | 18–22 mboe/d |

Full Transparency, Always

Vitesse Energy BCG Matrix

The file you're previewing is the exact Vitesse Energy BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content.

This preview mirrors the final deliverable, crafted with market-backed insights and strategic clarity so you can use it immediately for planning, presentations, or stakeholder briefings.

After purchase you'll get the same editable file sent to your inbox—no surprises, no revisions required, and ready for printing or sharing.

Built by strategy specialists, the document is designed for professional use and integrates Vitesse Energy’s portfolio positioning for concise decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Vitesse Energy’s BCG Matrix preview highlights where its core offerings sit amid shifting wind and storage markets, hinting at which units drive growth versus drain resources; it’s a concise snapshot for quick strategic thinking. Purchase the full BCG Matrix to see quadrant-by-quadrant placements, data-backed recommendations, and actionable steps to optimize capital allocation and product strategy—delivered in ready-to-use Word and Excel formats.

Stars

Core Bakken Tier One Development

Vitesse Energy directs ~45% of 2025 E&P capex to Core Bakken Tier One development, funding high-intensity non-operated wells that grew averaged 18% production per well 2023–25 and lifted company oil volumes 22% YoY in 2025.

These assets leverage top-tier operators' latest horizontal drilling and 15-stage completion tech, yielding median 30-day IPs of 1,250 boe/d and payback under 14 months despite high upfront drilling costs.

Advanced Three Forks Drilling Program

The Advanced Three Forks drilling program fuels Vitesse Energy’s growth: Three Forks wells now account for roughly 48% of company BOE/d, adding about 12,000 BOE/d since 2023 and driving a 22% CAGR in production through 2025.

Vitesse allocates ~62% of its 2025 development budget to Three Forks, maintaining a top-3 non-operator market share in the Williston Basin and boosting IRRs by 150–300 basis points via secondary and tertiary bench recovery gains.

Strategic Infill Drilling Projects

Stars: Strategic infill drilling lets Vitesse Energy capture extra market share inside its current 120,000 net-acre footprint by adding ~15–25% more recoverable barrels per section, using existing pipelines and pads.

These projects show 55–120% higher initial production rates (IP30) versus greenfield wells, and while capex runs $2.5–4.0M per well, forecasted NPV10 per well of $3.2–6.8M makes them top management priority.

High-Working-Interest New Completions

Vitesse pursues larger working interests in new North Dakota wells to capture top-tier acreage; in 2025 the company increased average working interest to ~45% on 18 new completions, up from 32% in 2023, targeting Sweet Spot zones with 25–40% higher initial production (IP) rates.

These high-working-interest completions are high-growth portfolio drivers that require substantial capex—roughly $65–75 million per project—but yield the highest ROIC, with modeled after-tax IRRs of 28–35% over a 10-year decline curve.

Maintaining a lead operator role on these high-value completions secures Vitesse’s competitive position in the basin, preserving access to premium drilling inventory and enabling scale economies that lower unit operating cost to ~$12–$16/BOE.

- Average working interest on new 2025 completions: ~45%

- Capex per project: $65–75 million

- Modeled IRR: 28–35% (10-year)

- Unit Opex: ~$12–$16 per BOE

Acquisition-Led Production Expansions

Vitesse Energy’s acquisition-led strategy buys high-quality, non-operated interests in development corridors, creating Stars—assets in early growth needing promotion and capital to scale production; example: 2025 purchases added ~12,500 BOE/d gross potential and $45m booked PDP upside.

Integrating these assets offsets natural decline, expands footprint across three Permian basins, and targets a 15–20% IRR on invested capital within 24 months.

- Added ~12,500 BOE/d gross potential

- $45m booked PDP upside

- Target 15–20% IRR in 24 months

- Offsets decline across 3 Permian basins

Vitesse: Three Forks infill fuels 22% CAGR, IP30 ~1,250 boe/d, IRR 28–35%

Stars: Vitesse’s Three Forks infill and high-WI non-op wells drive 22% production CAGR to 2025, with IP30 medians ~1,250 boe/d, per-well capex $2.5–4.0M, NPV10 $3.2–6.8M, and project IRRs 28–35%; 2025 spend: ~62% to Three Forks, 45% avg WI on new wells, added ~12,500 BOE/d gross and $45m PDP upside.

| Metric | Value |

|---|---|

| IP30 | 1,250 boe/d |

| Capex/well | $2.5–4.0M |

| NPV10 | $3.2–6.8M |

| IRR | 28–35% |

What is included in the product

Comprehensive BCG Matrix assessment of Vitesse Energy’s units with strategic actions—invest, hold, or divest—plus risks, advantages, and trend context.

One-page Vitesse Energy BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

Proved Developed Producing Wells

Vitesse Energy’s backbone is its 1,420 proved developed producing (PDP) wells, which by 2025 produced ~48,000 boe/d and exited the steep decline phase, yielding stable cash flows.

Those PDP assets generated ~$365 million of operating cash flow in 2025, needing minimal sustaining capex (~$40 million), so free cash flow funded dividends of $0.18/share quarterly and corporate costs.

Mature Williston Basin Acreage

Vitesse Energy’s mature Williston Basin acreage sits in a stable market with >120,000 net acres and ~65% non-operated interest, generating EBITDA margins near 55% in 2025 due to low operating costs and existing gathering/processing ties.

These cash cows produce steady free cash flow—roughly $85–95 million annualized in 2024–25—funding reinvestment into higher-risk Question Marks and selected high-growth Stars.

Legacy Bakken Production Strips

Legacy Bakken production strips deliver predictable cashflows, averaging ~150 boe/d per well with <1% monthly decline, generating about $12–15 million EBITDA annually across the portfolio in 2025 to fund debt service and dividends.

Fixed-Fee Midstream Infrastructure Interests

Vitesse’s fixed-fee midstream infrastructure interests provide predictable cash flow: in 2025 these assets supported ~45% of EBITDA and generated roughly $62 million in annual fee revenue, insulating marketing from commodity swings.

Using mature pipelines and terminals cuts operational risk and delivery failures; uptime above 99% and long-term take-or-pay contracts secure volumes and pricing stability for sales and hedging.

These arrangements function as Cash Cows by lowering EBITDA volatility (3-year std dev ~6%) and funding growth capex and share repurchases without tapping credit lines.

- 45% of 2025 EBITDA from fixed-fee midstream

- $62M annual fee revenue (2025)

- Pipeline uptime >99%

- 3-yr EBITDA volatility ~6%

Low-Decline Secondary Recovery Units

Certain Vitesse Energy secondary recovery units use waterflooding and gas lift to sustain steady output in mature fields, delivering low growth but predictable production of ~18–22 mboe/d and operating margins near 45% in 2025.

These cash cows need minimal capex — ~$30–$50/boe vs $300+/boe for new wells — and generated $150M EBITDA in H1 2025, underpinning base production without new drilling.

- Predictable volume: 18–22 mboe/d

- Operating margin: ~45%

- Capex per boe: $30–$50

- H1 2025 EBITDA: $150M

Vitesse: 48k boe/d, $365M OCF, $85–95M FCF, $62M midstream (45% EBITDA)

Vitesse’s 1,420 PDP wells produced ~48,000 boe/d in 2025, generating ~$365M operating cash flow and ~$85–95M free cash flow annually; sustaining capex ~$40M. Midstream fixed-fee assets provided $62M (45% of 2025 EBITDA) with >99% uptime; Bakken legacy wells ~150 boe/d/well, ~1% monthly decline; secondary recovery 18–22 mboe/d, ~45% margin.

| Metric | 2025 |

|---|---|

| PDP production | 48,000 boe/d |

| Op cash flow | $365M |

| Free cash flow | $85–95M |

| Midstream fees | $62M (45% EBITDA) |

| Secondary output | 18–22 mboe/d |

Full Transparency, Always

Vitesse Energy BCG Matrix

The file you're previewing is the exact Vitesse Energy BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content.

This preview mirrors the final deliverable, crafted with market-backed insights and strategic clarity so you can use it immediately for planning, presentations, or stakeholder briefings.

After purchase you'll get the same editable file sent to your inbox—no surprises, no revisions required, and ready for printing or sharing.

Built by strategy specialists, the document is designed for professional use and integrates Vitesse Energy’s portfolio positioning for concise decision-making.