Vocus PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and tech disruption are reshaping Vocus’s prospects—our concise PESTLE snapshot highlights the external risks and opportunities you need to know; purchase the full analysis to unlock detailed, actionable insights and editable reports for strategy, investment, or boardroom use.

Political factors

Government Infrastructure Investment

The Australian government’s A$1.2bn Regional Connectivity Program and A$2.0bn Digital Infrastructure Fund offer subsidy opportunities for Vocus to expand its 23,000km fiber network, aligning with national digital sovereignty goals.

Geopolitical Stability in Indo-Pacific

Vocus’s subsea investments like the Australia–Singapore Cable (commissioned 2018, capacity 40 Tb/s) face risks from Indo-Pacific geopolitical shifts between Western allies and regional states; 2024 tensions around South China Sea transit and a 12% rise in contested maritime incidents raise security and insurance costs for undersea assets.

Cybersecurity Policy Mandates

By end-2025 Australia and New Zealand mandated stricter cybersecurity frameworks for critical infrastructure, increasing compliance costs; Vocus faces estimated industry compliance spending rises of 15–25%, adding up to NZD/AUD tens of millions regionally.

Vocus must align operations to counter state-sponsored threats to national data integrity, or risk losing large public-sector contracts that represent roughly 20–30% of telco enterprise revenues in comparable providers.

Telecommunications Regulatory Oversight

Political pressure to boost competition shapes ACCC and NZCC actions on wholesale pricing and access; recent ACCC wholesale reviews and NZCC consultation in 2024 targeted price remedies affecting ~A$2.5bn in annual sector revenue.

Legislative moves to close the digital divide—Australia’s $1.5bn Regional Connectivity Program (2024) and NZ’s UFB extensions—force Vocus to reconcile universal service obligations with margins in retail and wholesale.

Navigating these policy shifts is vital to protect Vocus’s enterprise and wholesale share (enterprise revenue ~A$900m FY2024) amid stricter access rules and potential price caps.

- Regulators: ACCC/NZCC reviews impacting ~A$2.5bn sector revenue

- Government funding: A$1.5bn Regional Connectivity Program (2024)

- Vocus exposure: enterprise revenue ~A$900m FY2024

- Risk: mandated access/pricing can compress wholesale margins

Trade Relations and Supply Chain

Trade policies affecting imports of high-tech networking gear can delay Vocus’s FY2025 capex, with tariffs adding up to 15% on equipment from certain regions and supplier lead times up 40% YoY in 2024-25.

Political alignment with key tech producers in 2025 influences fiber-optic component costs, which rose ~12% YoY, impacting margins and project timelines.

Strategic procurement and diversified sourcing are required to mitigate risks from trade barriers and sanctions; Vocus should target multiple suppliers and contingency stock equal to ~3 months of demand.

- Tariffs up to 15% and 40% longer lead times (2024-25)

- Fiber component costs +12% YoY (2025)

- Contingency stock ≈ 3 months demand

Vocus faces subsidy-led growth, regulatory squeeze, rising cyber & supply costs

Government subsidies (A$1.2–1.5bn) and ACCC/NZCC reviews (impacting ~A$2.5bn sector revenue) create growth and regulation pressures for Vocus (enterprise revenue ~A$900m FY2024); subsea security incidents (+12% contested events 2024) and tightened cyber rules (compliance +15–25%) raise costs; trade tariffs up to 15% and 12% YoY fiber cost rise squeeze margins; procurement diversification and 3-month contingency stock recommended.

| Metric | Value |

|---|---|

| Regional funding | A$1.2–1.5bn |

| Sector revenue impacted | ~A$2.5bn |

| Vocus enterprise rev | ~A$900m FY2024 |

| Cyber compliance cost rise | 15–25% |

| Subsea contested incidents | +12% (2024) |

| Tariffs / fiber cost | Up to 15% / +12% YoY |

| Contingency stock | ~3 months |

What is included in the product

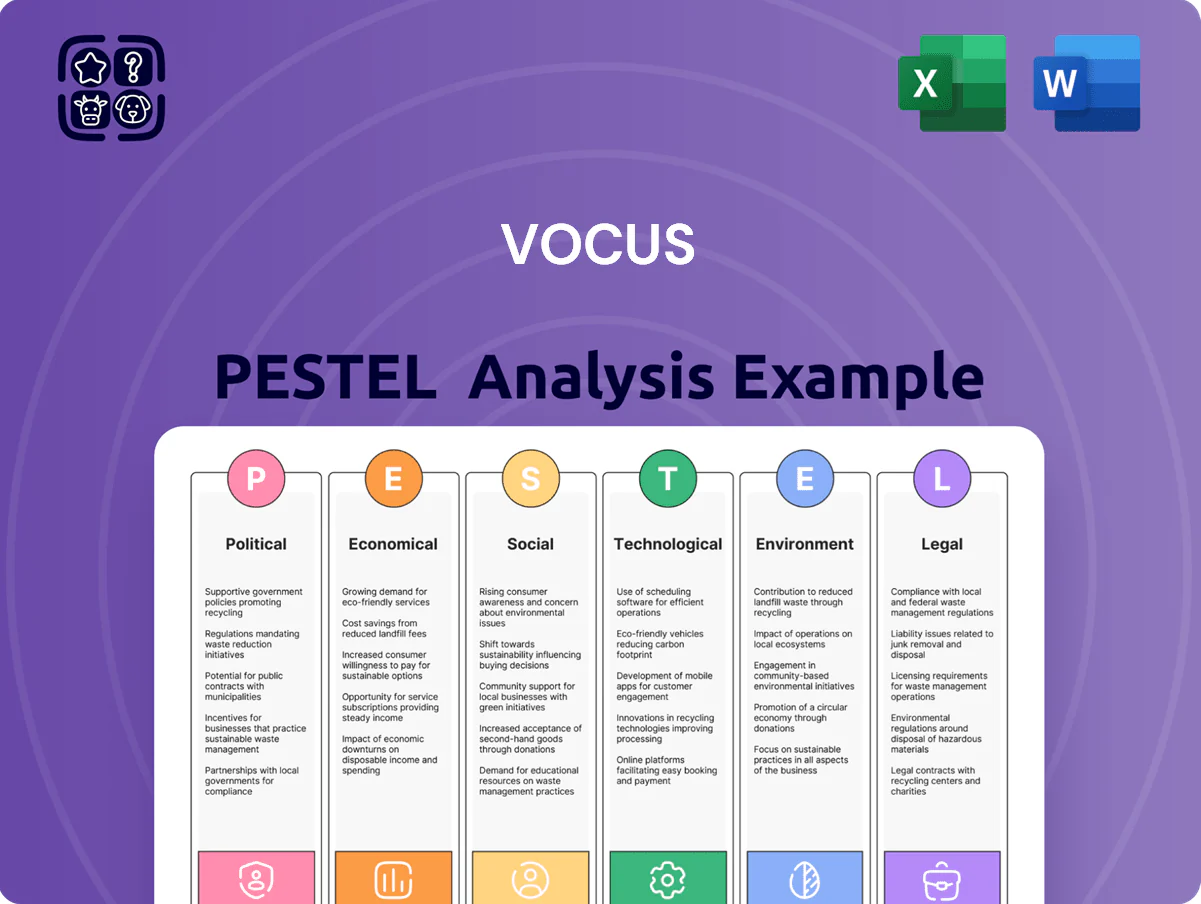

Explores how external macro-environmental factors uniquely affect Vocus across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Vocus's full PESTLE into a clear, shareable summary that teams can drop into presentations or planning sessions for fast alignment on external risks and market positioning.

Economic factors

Interest Rate Environment

The prevailing interest rate environment in late 2025—with the RBA cash rate at 4.35% and 10-year Australian government yields around 3.9%—raises Vocus’s cost of debt for capital-intensive fiber projects, potentially compressing EBITDA margins by several percentage points. High rates can slow network expansion by increasing financing costs, while a stabilizing rate path would permit more aggressive CAPEX; analysts note Vocus’s net debt/EBITDA stood near 3.0x in FY2025, a key liquidity metric.

Enterprise Digital Transformation Spending

Economic cycles shape Vocus’s enterprise digital transformation spend: in 2024 Australian ICT investment rose 3.8% to A$145bn, boosting demand from large corporates and government for high-capacity cloud and SD-WAN services. A strong GDP (Australia ~2.5% in 2024) nudges customers toward premium bandwidth and managed services, increasing ARPU potential. In downturns clients prioritize cost optimization—upgrading slows as capex shifts to Opex and existing links are right-sized.

Inflationary Pressure on Operations

Persistent inflation in 2024–25 pushed Australian CPI to about 4.1% (yearly), raising labor, energy and materials costs for Vocus’s ~40,000 km fibre network; wage pressures and higher diesel/electricity bills increased OPEX across maintenance and build projects.

Vocus must reallocate resources, improve operational efficiency and consider tariff adjustments for wholesale partners to offset rising unit costs while protecting margins.

The core economic risk is passing through higher costs without losing competitiveness; with wholesale bandwidth prices under pressure, Vocus’s ability to increase prices is constrained by market elasticity and industry capex commitments.

Foreign Exchange Fluctuations

The AUD weakened ~6% vs USD in 2024, increasing Vocus's international bandwidth lease costs and USD-denominated debt servicing for subsea assets; NZD/AUD shifts similarly affect trans-Tasman operations.

Hedging is essential: forward contracts and FX swaps reduced Vocus-like carriers' FX exposure by ~70% in 2024, protecting EBITDA margins against volatility.

- Exposure: AUD, NZD, USD movements

- Impact: higher lease costs & foreign debt servicing

- Mitigation: forwards, swaps, 70% coverage benchmark

Labor Market Dynamics

The demand for specialized telecommunications engineers and cybersecurity experts drove average tech wages up 6.2% YoY in 2024, pressuring Vocus’s payroll and raising industry hiring costs by an estimated A$4–6k per hire.

Competition for talent risks project delays and higher contractor use; Vocus reported 12% of network projects delayed in 2024 due to resourcing constraints.

As of 2025 Vocus is investing in automation and upskilling—targeting a 20% reduction in labor hours on key tasks and a training budget increase of ~15% to control costs.

- Wage growth: +6.2% YoY (2024)

- Project delays: 12% of network projects (2024)

- Training budget increase: ~15% (2025)

- Target labor hours reduction: 20% via automation (2025)

Rising rates and FX pain tighten CAPEX as ICT demand holds; hedges cushion 70%

Rising rates (RBA 4.35%, 10y 3.9% in late-2025) lift cost of debt; net debt/EBITDA ~3.0x (FY2025) strains CAPEX. 2024 ICT spend +3.8% to A$145bn and GDP ~2.5% support demand, but CPI ~4.1% and wage growth +6.2% raise OPEX. FX: AUD −6% vs USD (2024) increases lease/debt costs; hedging ~70% mitigates risk.

| Metric | Value |

|---|---|

| RBA cash rate | 4.35% |

| Net debt/EBITDA | ~3.0x |

| ICT spend 2024 | A$145bn (+3.8%) |

| CPI 2024 | 4.1% |

| Wage growth 2024 | +6.2% |

| AUD vs USD 2024 | −6% |

| Hedging coverage | ~70% |

What You See Is What You Get

Vocus PESTLE Analysis

The preview shown here is the exact Vocus PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are identical to the file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and tech disruption are reshaping Vocus’s prospects—our concise PESTLE snapshot highlights the external risks and opportunities you need to know; purchase the full analysis to unlock detailed, actionable insights and editable reports for strategy, investment, or boardroom use.

Political factors

Government Infrastructure Investment

The Australian government’s A$1.2bn Regional Connectivity Program and A$2.0bn Digital Infrastructure Fund offer subsidy opportunities for Vocus to expand its 23,000km fiber network, aligning with national digital sovereignty goals.

Geopolitical Stability in Indo-Pacific

Vocus’s subsea investments like the Australia–Singapore Cable (commissioned 2018, capacity 40 Tb/s) face risks from Indo-Pacific geopolitical shifts between Western allies and regional states; 2024 tensions around South China Sea transit and a 12% rise in contested maritime incidents raise security and insurance costs for undersea assets.

Cybersecurity Policy Mandates

By end-2025 Australia and New Zealand mandated stricter cybersecurity frameworks for critical infrastructure, increasing compliance costs; Vocus faces estimated industry compliance spending rises of 15–25%, adding up to NZD/AUD tens of millions regionally.

Vocus must align operations to counter state-sponsored threats to national data integrity, or risk losing large public-sector contracts that represent roughly 20–30% of telco enterprise revenues in comparable providers.

Telecommunications Regulatory Oversight

Political pressure to boost competition shapes ACCC and NZCC actions on wholesale pricing and access; recent ACCC wholesale reviews and NZCC consultation in 2024 targeted price remedies affecting ~A$2.5bn in annual sector revenue.

Legislative moves to close the digital divide—Australia’s $1.5bn Regional Connectivity Program (2024) and NZ’s UFB extensions—force Vocus to reconcile universal service obligations with margins in retail and wholesale.

Navigating these policy shifts is vital to protect Vocus’s enterprise and wholesale share (enterprise revenue ~A$900m FY2024) amid stricter access rules and potential price caps.

- Regulators: ACCC/NZCC reviews impacting ~A$2.5bn sector revenue

- Government funding: A$1.5bn Regional Connectivity Program (2024)

- Vocus exposure: enterprise revenue ~A$900m FY2024

- Risk: mandated access/pricing can compress wholesale margins

Trade Relations and Supply Chain

Trade policies affecting imports of high-tech networking gear can delay Vocus’s FY2025 capex, with tariffs adding up to 15% on equipment from certain regions and supplier lead times up 40% YoY in 2024-25.

Political alignment with key tech producers in 2025 influences fiber-optic component costs, which rose ~12% YoY, impacting margins and project timelines.

Strategic procurement and diversified sourcing are required to mitigate risks from trade barriers and sanctions; Vocus should target multiple suppliers and contingency stock equal to ~3 months of demand.

- Tariffs up to 15% and 40% longer lead times (2024-25)

- Fiber component costs +12% YoY (2025)

- Contingency stock ≈ 3 months demand

Vocus faces subsidy-led growth, regulatory squeeze, rising cyber & supply costs

Government subsidies (A$1.2–1.5bn) and ACCC/NZCC reviews (impacting ~A$2.5bn sector revenue) create growth and regulation pressures for Vocus (enterprise revenue ~A$900m FY2024); subsea security incidents (+12% contested events 2024) and tightened cyber rules (compliance +15–25%) raise costs; trade tariffs up to 15% and 12% YoY fiber cost rise squeeze margins; procurement diversification and 3-month contingency stock recommended.

| Metric | Value |

|---|---|

| Regional funding | A$1.2–1.5bn |

| Sector revenue impacted | ~A$2.5bn |

| Vocus enterprise rev | ~A$900m FY2024 |

| Cyber compliance cost rise | 15–25% |

| Subsea contested incidents | +12% (2024) |

| Tariffs / fiber cost | Up to 15% / +12% YoY |

| Contingency stock | ~3 months |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vocus across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Vocus's full PESTLE into a clear, shareable summary that teams can drop into presentations or planning sessions for fast alignment on external risks and market positioning.

Economic factors

Interest Rate Environment

The prevailing interest rate environment in late 2025—with the RBA cash rate at 4.35% and 10-year Australian government yields around 3.9%—raises Vocus’s cost of debt for capital-intensive fiber projects, potentially compressing EBITDA margins by several percentage points. High rates can slow network expansion by increasing financing costs, while a stabilizing rate path would permit more aggressive CAPEX; analysts note Vocus’s net debt/EBITDA stood near 3.0x in FY2025, a key liquidity metric.

Enterprise Digital Transformation Spending

Economic cycles shape Vocus’s enterprise digital transformation spend: in 2024 Australian ICT investment rose 3.8% to A$145bn, boosting demand from large corporates and government for high-capacity cloud and SD-WAN services. A strong GDP (Australia ~2.5% in 2024) nudges customers toward premium bandwidth and managed services, increasing ARPU potential. In downturns clients prioritize cost optimization—upgrading slows as capex shifts to Opex and existing links are right-sized.

Inflationary Pressure on Operations

Persistent inflation in 2024–25 pushed Australian CPI to about 4.1% (yearly), raising labor, energy and materials costs for Vocus’s ~40,000 km fibre network; wage pressures and higher diesel/electricity bills increased OPEX across maintenance and build projects.

Vocus must reallocate resources, improve operational efficiency and consider tariff adjustments for wholesale partners to offset rising unit costs while protecting margins.

The core economic risk is passing through higher costs without losing competitiveness; with wholesale bandwidth prices under pressure, Vocus’s ability to increase prices is constrained by market elasticity and industry capex commitments.

Foreign Exchange Fluctuations

The AUD weakened ~6% vs USD in 2024, increasing Vocus's international bandwidth lease costs and USD-denominated debt servicing for subsea assets; NZD/AUD shifts similarly affect trans-Tasman operations.

Hedging is essential: forward contracts and FX swaps reduced Vocus-like carriers' FX exposure by ~70% in 2024, protecting EBITDA margins against volatility.

- Exposure: AUD, NZD, USD movements

- Impact: higher lease costs & foreign debt servicing

- Mitigation: forwards, swaps, 70% coverage benchmark

Labor Market Dynamics

The demand for specialized telecommunications engineers and cybersecurity experts drove average tech wages up 6.2% YoY in 2024, pressuring Vocus’s payroll and raising industry hiring costs by an estimated A$4–6k per hire.

Competition for talent risks project delays and higher contractor use; Vocus reported 12% of network projects delayed in 2024 due to resourcing constraints.

As of 2025 Vocus is investing in automation and upskilling—targeting a 20% reduction in labor hours on key tasks and a training budget increase of ~15% to control costs.

- Wage growth: +6.2% YoY (2024)

- Project delays: 12% of network projects (2024)

- Training budget increase: ~15% (2025)

- Target labor hours reduction: 20% via automation (2025)

Rising rates and FX pain tighten CAPEX as ICT demand holds; hedges cushion 70%

Rising rates (RBA 4.35%, 10y 3.9% in late-2025) lift cost of debt; net debt/EBITDA ~3.0x (FY2025) strains CAPEX. 2024 ICT spend +3.8% to A$145bn and GDP ~2.5% support demand, but CPI ~4.1% and wage growth +6.2% raise OPEX. FX: AUD −6% vs USD (2024) increases lease/debt costs; hedging ~70% mitigates risk.

| Metric | Value |

|---|---|

| RBA cash rate | 4.35% |

| Net debt/EBITDA | ~3.0x |

| ICT spend 2024 | A$145bn (+3.8%) |

| CPI 2024 | 4.1% |

| Wage growth 2024 | +6.2% |

| AUD vs USD 2024 | −6% |

| Hedging coverage | ~70% |

What You See Is What You Get

Vocus PESTLE Analysis

The preview shown here is the exact Vocus PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are identical to the file you’ll download immediately after payment.