Vodafone Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

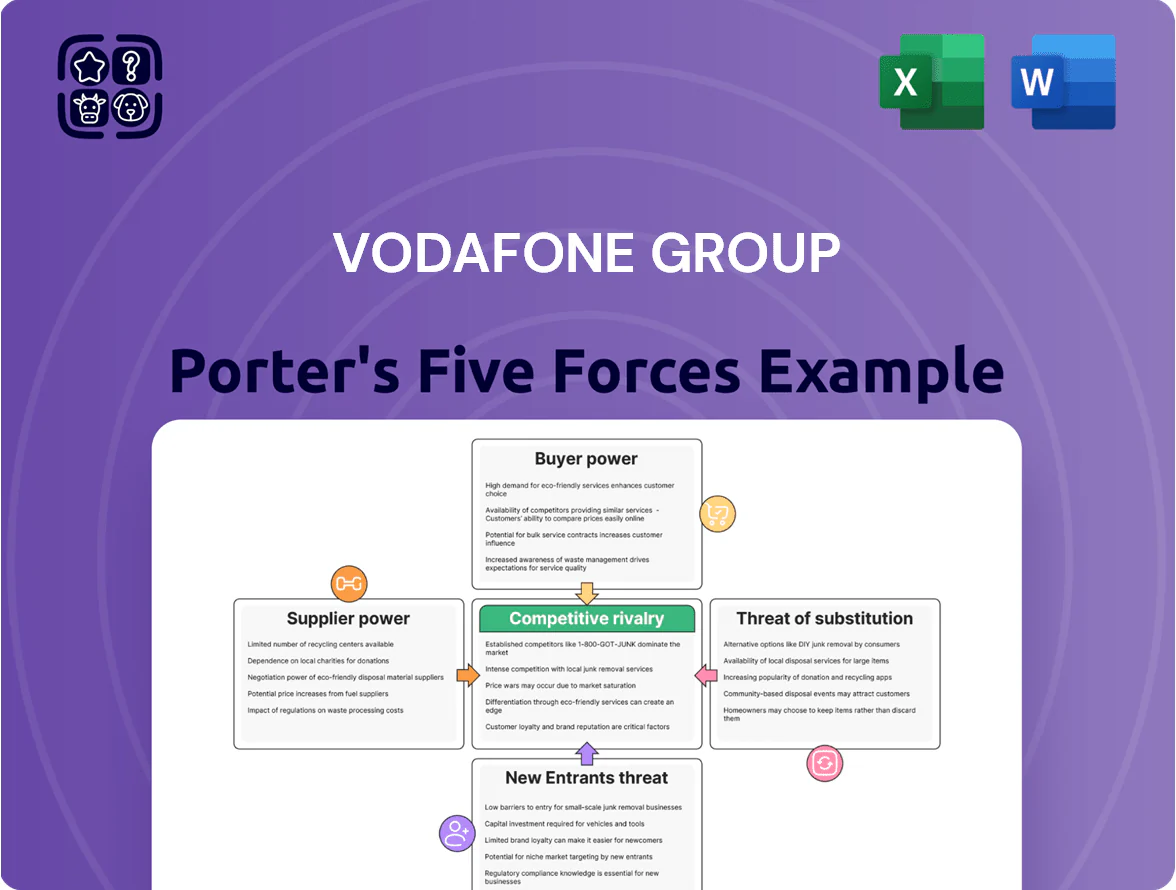

Vodafone Group faces intense rivalry from global and regional telecoms, significant buyer power from enterprise and retail segments, and moderate supplier leverage for network infrastructure—while regulatory hurdles and digital substitutes shape strategic risks.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Vodafone’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Equipment Vendors

The telecom sector depends on a handful of global vendors such as Ericsson and Nokia for 5G and core network kit, concentrating supplier power; Ericsson and Nokia together held roughly 50–60% of global RAN (radio access network) market share in 2024. After EU and UK exclusions of certain high-risk vendors by late 2025, bargaining power of remaining suppliers rose as alternative capacity shrank, pushing vendor pricing and lead times up—Vodafone reported capex exposure to supplier consolidation in its 2024 annual report. Vodafone must keep close, strategic partnerships with these few suppliers to secure network uptime, timely 5G rollouts, and feature parity with rivals.

Dependence on High-End Handset Manufacturers

Vodafone’s appeal hinges on device availability and subsidies from Apple and Samsung, whose combined global smartphone market share was ~50% in 2025, driving demand for high-speed data and 5G plans; Apple devices alone accounted for ~60% of UK smartphone activations in 2024. These manufacturers can demand better subsidy terms or prefer direct channels, and a shift in their distribution strategy could force Vodafone to raise handset subsidies, hurt ARPU, and risk losing premium subscribers.

Government Control Over Spectrum Allocation

National governments act as suppliers by licensing radio spectrum; auctions cost Vodafone Group billions—eg, UK 5G spectrum raised £1.4bn in 2021 and EU mid-band auctions saw €8–12bn per country in 2023–24—giving regulators leverage over Vodafone’s network rollout.

High reserve prices, coverage obligations, and timing constraints tied to licenses constrain Vodafone’s capital allocation and launch schedules, increasing operating risk and forcing spectrum-driven capex choices.

By end-2025, securing mid-band and millimeter-wave bands for 5G Advanced is critical: industry estimates show mid-band availability cuts latency and boosts capacity by 2–4x, making spectrum access a strategic bottleneck.

Energy Providers and Operational Costs

Vodafone consumes large power volumes for data centers and 113,000 UK and European sites, so energy price swings hit EBITDA—energy costs rose ~8% in 2022 industry-wide and can shift margins by several hundred basis points for operators.

Vodafone signed long-term renewable PPAs covering ~70% of its European power needs by end-2024, yet grid supply and wholesale markets remain concentrated among few utilities, keeping supplier leverage high.

Price volatility also risks delaying Vodafone’s net-zero targets (target: net-zero emissions by 2040 for operations) and raises capex for backup/efficiency projects.

- High energy intensity: thousands of towers/datacenters

- PPAs cover ~70% Europe (end-2024)

- Supplier concentration increases bargaining power

- Energy-driven margin and capex risk to 2040 net-zero

Cloud and Software-as-a-Service Partners

Vodafone depends heavily on hyperscale clouds—Microsoft Azure and AWS—for enterprise services and internal IT; this underpins its IoT and cybersecurity stacks and creates strong technical dependence.

Switching large cloud estates is costly: typical migration estimates run 15–30% of annual cloud spend, and Vodafone reported cloud and IT op spend of ~€3.1bn in 2024, so vendor leverage is material.

- High dependency on Azure/AWS for IoT/security

- Switching cost ~15–30% of annual cloud spend

- Vodafone cloud/IT spend ~€3.1bn in 2024

- Suppliers hold notable bargaining power

Supplier concentration fuels pricing, lead-time and capex risk for Vodafone

Suppliers wield high leverage over Vodafone: Ericsson/Nokia held ~50–60% RAN share (2024), Apple/Samsung ~50% smartphone share (2025), hyperscalers (Azure/AWS) tied to ~€3.1bn cloud spend (2024), and PPAs cover ~70% EU power (end-2024), while spectrum auctions cost billions (UK £1.4bn 2021). These concentrations raise pricing, lead-time, and capex risk for Vodafone.

| Supplier | Key metric |

|---|---|

| RAN vendors | 50–60% market share (2024) |

| Smartphones | ~50% Apple+Samsung (2025) |

| Cloud spend | €3.1bn (2024) |

| PPAs | ~70% EU power (end-2024) |

| Spectrum cost | UK £1.4bn (2021) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Vodafone Group, highlighting competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and strategic implications for pricing, margins, and market positioning.

A concise Vodafone Group Porter’s Five Forces one-sheet that pinpoints competitive pressures, so you can quickly prioritize strategy changes and investor talking points.

Customers Bargaining Power

High Price Sensitivity in Consumer Segments

In mature European markets Vodafone faces commoditisation of mobile and fixed services, driving high price sensitivity among retail customers and a 2024–25 churn risk spike tied to rising household cost pressures; Vodafone reported a 1.2% YoY retail service revenue decline in Europe H1 2025. To retain subscribers Vodafone relies on frequent promotions and bundled offers—postpaid ARPU fell ~3% in 2024, prompting wider value-added bundles. By late 2025, surveys show 62% of consumers prioritize low-cost data plans, forcing deeper discounting and tighter margin management.

Low Switching Costs via Regulatory Support

Mobile Number Portability rules in most Vodafone markets let customers switch providers while keeping numbers, lowering switching costs and raising buyer power; GSMA reported 85% of EU countries had porting times under 1 day as of 2024. This ease of exit means subscribers can move for small price or quality gains, pressuring Vodafone’s ARPU (2024 group ARPU ~8.5 EUR/month) and retention. Vodafone spends heavily on loyalty and CX—2024 capex and opex included ~11.2 billion EUR—to reduce churn risk.

Volume Leverage of Enterprise and Government Clients

Large corporate and public-sector customers account for about 30% of Vodafone Group’s 2024 service revenue, giving them strong volume leverage to demand bespoke SLAs, integrated IoT platforms, and steep discounts not offered to retail users.

Competitive tenders let buyers pit Vodafone against Orange, Telefónica and DT, often cutting margins by 5–15 percentage points on enterprise deals; public-sector procurement rules further boost buyer bargaining power.

Availability of Transparent Comparison Tools

In 2025, price-comparison sites and real-time network review apps give UK consumers instant access to metrics like Vodafone UK’s 4G/5G median download speeds (e.g., 120 Mbps) and plan-price comparisons, cutting information asymmetry and shifting decisions to data over brand.

This forces Vodafone to sustain top-tier network KPIs and aggressive pricing—Vodafone UK saw ARPU près £20 in 2024—else it risks visibility loss on comparison platforms and churn to rivals.

- Instant access to speed/coverage data

- Decisions driven by objective metrics

- Need for competitive pricing vs ARPU £≈20

- High KPIs required to avoid churn

Demand for Converged and Flexible Bundling

Modern consumers demand converged mobile, broadband and TV bundles, letting buyers push for higher value—Vodafone’s 2024 fixed-mobile converged ARPU fell 3.2% in key EU markets, pressuring per-service margins.

If Vodafone fails to offer seamless, cost-effective bundles, customers can churn whole ecosystems; quad-play churn risk rose after 2023 price hikes, with churn up to 1.6% quarterly in Spain.

- Bundling reduces per-service margin

- 2024 FMC ARPU down 3.2% in EU

- Quad-play churn hit 1.6% q/q in Spain

Strong customer bargaining drags ARPU and margins as churn and price pressure rise

Customers hold strong bargaining power: retail price sensitivity and easy porting drove EURO H1 2025 retail revenue −1.2% YoY and group ARPU ≈€8.5/month; enterprise tenders cut margins 5–15ppt on ~30% service revenue; UK median 4G/5G speeds ~120 Mbps (2025) and price-comparison apps amplify switching; FMC/quad-play ARPU down ~3.2% (2024), Spain quarterly churn reached 1.6% (post‑2023 hikes).

| Metric | Value |

|---|---|

| Group ARPU (2024) | €8.5/mo |

| EU retail rev H1 2025 YoY | −1.2% |

| FMC ARPU change (2024) | −3.2% |

| Spain quad-play churn (q) | 1.6% |

| Enterprise revenue share (2024) | ≈30% |

What You See Is What You Get

Vodafone Group Porter's Five Forces Analysis

This preview shows the exact Vodafone Group Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download; no samples, placeholders, or mockups. The document covers threat of new entrants, bargaining power of suppliers and buyers, rivalry intensity, and threat of substitutes with data-driven insights and strategic implications. Instant access upon payment—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Vodafone Group faces intense rivalry from global and regional telecoms, significant buyer power from enterprise and retail segments, and moderate supplier leverage for network infrastructure—while regulatory hurdles and digital substitutes shape strategic risks.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Vodafone’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Infrastructure Equipment Vendors

The telecom sector depends on a handful of global vendors such as Ericsson and Nokia for 5G and core network kit, concentrating supplier power; Ericsson and Nokia together held roughly 50–60% of global RAN (radio access network) market share in 2024. After EU and UK exclusions of certain high-risk vendors by late 2025, bargaining power of remaining suppliers rose as alternative capacity shrank, pushing vendor pricing and lead times up—Vodafone reported capex exposure to supplier consolidation in its 2024 annual report. Vodafone must keep close, strategic partnerships with these few suppliers to secure network uptime, timely 5G rollouts, and feature parity with rivals.

Dependence on High-End Handset Manufacturers

Vodafone’s appeal hinges on device availability and subsidies from Apple and Samsung, whose combined global smartphone market share was ~50% in 2025, driving demand for high-speed data and 5G plans; Apple devices alone accounted for ~60% of UK smartphone activations in 2024. These manufacturers can demand better subsidy terms or prefer direct channels, and a shift in their distribution strategy could force Vodafone to raise handset subsidies, hurt ARPU, and risk losing premium subscribers.

Government Control Over Spectrum Allocation

National governments act as suppliers by licensing radio spectrum; auctions cost Vodafone Group billions—eg, UK 5G spectrum raised £1.4bn in 2021 and EU mid-band auctions saw €8–12bn per country in 2023–24—giving regulators leverage over Vodafone’s network rollout.

High reserve prices, coverage obligations, and timing constraints tied to licenses constrain Vodafone’s capital allocation and launch schedules, increasing operating risk and forcing spectrum-driven capex choices.

By end-2025, securing mid-band and millimeter-wave bands for 5G Advanced is critical: industry estimates show mid-band availability cuts latency and boosts capacity by 2–4x, making spectrum access a strategic bottleneck.

Energy Providers and Operational Costs

Vodafone consumes large power volumes for data centers and 113,000 UK and European sites, so energy price swings hit EBITDA—energy costs rose ~8% in 2022 industry-wide and can shift margins by several hundred basis points for operators.

Vodafone signed long-term renewable PPAs covering ~70% of its European power needs by end-2024, yet grid supply and wholesale markets remain concentrated among few utilities, keeping supplier leverage high.

Price volatility also risks delaying Vodafone’s net-zero targets (target: net-zero emissions by 2040 for operations) and raises capex for backup/efficiency projects.

- High energy intensity: thousands of towers/datacenters

- PPAs cover ~70% Europe (end-2024)

- Supplier concentration increases bargaining power

- Energy-driven margin and capex risk to 2040 net-zero

Cloud and Software-as-a-Service Partners

Vodafone depends heavily on hyperscale clouds—Microsoft Azure and AWS—for enterprise services and internal IT; this underpins its IoT and cybersecurity stacks and creates strong technical dependence.

Switching large cloud estates is costly: typical migration estimates run 15–30% of annual cloud spend, and Vodafone reported cloud and IT op spend of ~€3.1bn in 2024, so vendor leverage is material.

- High dependency on Azure/AWS for IoT/security

- Switching cost ~15–30% of annual cloud spend

- Vodafone cloud/IT spend ~€3.1bn in 2024

- Suppliers hold notable bargaining power

Supplier concentration fuels pricing, lead-time and capex risk for Vodafone

Suppliers wield high leverage over Vodafone: Ericsson/Nokia held ~50–60% RAN share (2024), Apple/Samsung ~50% smartphone share (2025), hyperscalers (Azure/AWS) tied to ~€3.1bn cloud spend (2024), and PPAs cover ~70% EU power (end-2024), while spectrum auctions cost billions (UK £1.4bn 2021). These concentrations raise pricing, lead-time, and capex risk for Vodafone.

| Supplier | Key metric |

|---|---|

| RAN vendors | 50–60% market share (2024) |

| Smartphones | ~50% Apple+Samsung (2025) |

| Cloud spend | €3.1bn (2024) |

| PPAs | ~70% EU power (end-2024) |

| Spectrum cost | UK £1.4bn (2021) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Vodafone Group, highlighting competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and strategic implications for pricing, margins, and market positioning.

A concise Vodafone Group Porter’s Five Forces one-sheet that pinpoints competitive pressures, so you can quickly prioritize strategy changes and investor talking points.

Customers Bargaining Power

High Price Sensitivity in Consumer Segments

In mature European markets Vodafone faces commoditisation of mobile and fixed services, driving high price sensitivity among retail customers and a 2024–25 churn risk spike tied to rising household cost pressures; Vodafone reported a 1.2% YoY retail service revenue decline in Europe H1 2025. To retain subscribers Vodafone relies on frequent promotions and bundled offers—postpaid ARPU fell ~3% in 2024, prompting wider value-added bundles. By late 2025, surveys show 62% of consumers prioritize low-cost data plans, forcing deeper discounting and tighter margin management.

Low Switching Costs via Regulatory Support

Mobile Number Portability rules in most Vodafone markets let customers switch providers while keeping numbers, lowering switching costs and raising buyer power; GSMA reported 85% of EU countries had porting times under 1 day as of 2024. This ease of exit means subscribers can move for small price or quality gains, pressuring Vodafone’s ARPU (2024 group ARPU ~8.5 EUR/month) and retention. Vodafone spends heavily on loyalty and CX—2024 capex and opex included ~11.2 billion EUR—to reduce churn risk.

Volume Leverage of Enterprise and Government Clients

Large corporate and public-sector customers account for about 30% of Vodafone Group’s 2024 service revenue, giving them strong volume leverage to demand bespoke SLAs, integrated IoT platforms, and steep discounts not offered to retail users.

Competitive tenders let buyers pit Vodafone against Orange, Telefónica and DT, often cutting margins by 5–15 percentage points on enterprise deals; public-sector procurement rules further boost buyer bargaining power.

Availability of Transparent Comparison Tools

In 2025, price-comparison sites and real-time network review apps give UK consumers instant access to metrics like Vodafone UK’s 4G/5G median download speeds (e.g., 120 Mbps) and plan-price comparisons, cutting information asymmetry and shifting decisions to data over brand.

This forces Vodafone to sustain top-tier network KPIs and aggressive pricing—Vodafone UK saw ARPU près £20 in 2024—else it risks visibility loss on comparison platforms and churn to rivals.

- Instant access to speed/coverage data

- Decisions driven by objective metrics

- Need for competitive pricing vs ARPU £≈20

- High KPIs required to avoid churn

Demand for Converged and Flexible Bundling

Modern consumers demand converged mobile, broadband and TV bundles, letting buyers push for higher value—Vodafone’s 2024 fixed-mobile converged ARPU fell 3.2% in key EU markets, pressuring per-service margins.

If Vodafone fails to offer seamless, cost-effective bundles, customers can churn whole ecosystems; quad-play churn risk rose after 2023 price hikes, with churn up to 1.6% quarterly in Spain.

- Bundling reduces per-service margin

- 2024 FMC ARPU down 3.2% in EU

- Quad-play churn hit 1.6% q/q in Spain

Strong customer bargaining drags ARPU and margins as churn and price pressure rise

Customers hold strong bargaining power: retail price sensitivity and easy porting drove EURO H1 2025 retail revenue −1.2% YoY and group ARPU ≈€8.5/month; enterprise tenders cut margins 5–15ppt on ~30% service revenue; UK median 4G/5G speeds ~120 Mbps (2025) and price-comparison apps amplify switching; FMC/quad-play ARPU down ~3.2% (2024), Spain quarterly churn reached 1.6% (post‑2023 hikes).

| Metric | Value |

|---|---|

| Group ARPU (2024) | €8.5/mo |

| EU retail rev H1 2025 YoY | −1.2% |

| FMC ARPU change (2024) | −3.2% |

| Spain quad-play churn (q) | 1.6% |

| Enterprise revenue share (2024) | ≈30% |

What You See Is What You Get

Vodafone Group Porter's Five Forces Analysis

This preview shows the exact Vodafone Group Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download; no samples, placeholders, or mockups. The document covers threat of new entrants, bargaining power of suppliers and buyers, rivalry intensity, and threat of substitutes with data-driven insights and strategic implications. Instant access upon payment—what you see is what you get.