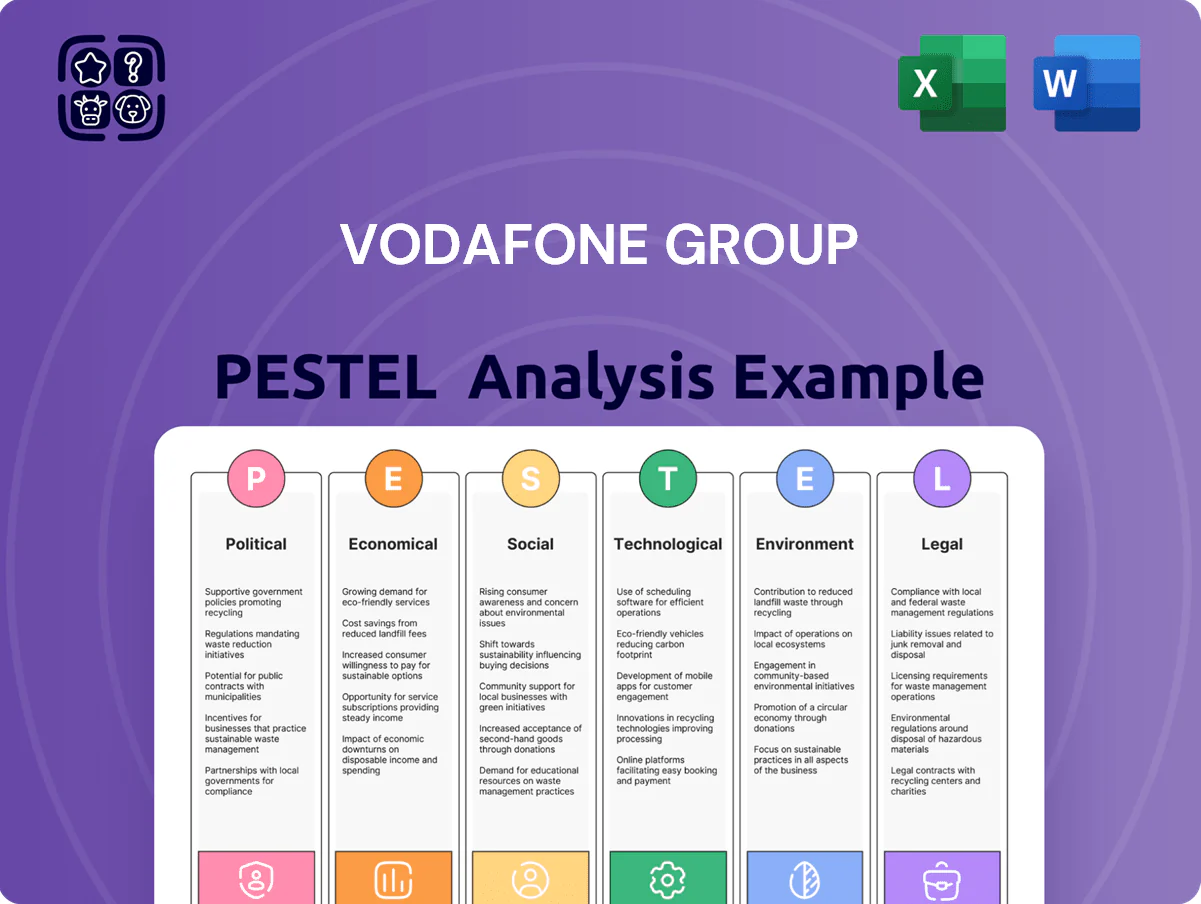

Vodafone Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Navigate Vodafone Group’s external landscape with our concise PESTLE snapshot—highlighting regulatory risks, macroeconomic pressures, tech disruption, and social shifts that shape strategy and valuation; buy the full PESTLE for a detailed, actionable report you can use in investor decks or strategic plans.

Political factors

Geopolitical instability in African markets

Vodafone’s exposure in Africa via Vodacom—which generated ZAR 66.1bn revenue in FY2024—faces risks from political volatility and regime changes that can threaten infrastructure security and service continuity. Recent government shifts in countries like Sudan and Ethiopia have forced intensified diplomatic engagement to protect assets and licences. Analysts should watch for nationalization risk and abrupt telecom policy changes that could affect EBITDA and capex forecasts.

EU regulatory alignment and digital sovereignty

The EU push for digital sovereignty compels Vodafone to localize data processing and favor trusted infrastructure partners, impacting capital allocation—Vodafone reported c.€3.2bn in network capex in FY2024, with vendor swaps for 5G upgrades adding hundreds of millions in transition costs. Political pressure to exclude high‑risk vendors accelerated equipment replacements and strategic pivots, while balancing Brussels’ directives with divergent national policies remains a top management challenge.

Post-Brexit UK telecommunications policy

Post-Brexit scrutiny intensified after Vodafone’s planned merger with Three UK triggered investigations by the CMA and National Security Advisors, raising risks to deal approval and potential remedies that could exceed 1–2 billion GBP; UK policy on digital infrastructure—pledged 5 billion GBP under Project Gigabit targets—will directly shape Vodafone’s capex and network integration timelines through 2025–2030.

Governmental influence on spectrum auctions

Government agendas shape timing and pricing of spectrum auctions crucial for Vodafone’s 5G rollout; UK 5G auctions raised about 1.4 billion GBP in 2021 and EU-wide auctions generated over 10 billion EUR in 2022, increasing licensing costs and pressuring Vodafone’s capital expenditures and balance sheet.

High reserve prices aimed at revenue can prioritize state coffers over network quality, while strategic lobbying and regulatory engagement are essential to push auction designs that lower upfront fees, enable installment payments, or reserve spectrum for coverage obligations to support sustainable deployment.

- 2021 UK auctions: ~1.4 billion GBP raised

- EU auctions (2022): >10 billion EUR

- High license costs increase CAPEX and leverage risks

- Lobbying can secure favorable payment terms and coverage-focused auction rules

Trade relations and global supply chain policies

Ongoing US-China tensions and EU export controls have raised prices for semiconductors and 5G radio units; global chip supply shortages in 2024 pushed telecom capex up ~8%, squeezing Vodafone Group EBITDA margins (2024 revenue €42.2bn, capex €6.1bn).

Sanctions and export controls force Vodafone to adjust procurement for vendors and delay 5G/FTTH rollouts; supplier diversification increased sourcing costs and inventory levels in 2024.

Changes in trade agreements and potential tariffs on imported network equipment could raise unit costs, reducing profitability on international projects and increasing total cost of ownership for infrastructure.

- 2024 revenue €42.2bn, capex €6.1bn

- Capex +8% vs prior year due partly to supply-driven price rises

- Supply-chain risk: sanctions/export controls impacting vendor choices

- Tariff shifts threaten equipment unit cost and project margins

Regulatory, nationalization and spectrum risks squeeze Vodafone & Vodacom margins

Political volatility in Africa (Vodacom ZAR 66.1bn FY2024) and nationalization risks threaten assets and EBITDA; EU digital sovereignty and vendor exclusions raised Vodafone capex pressure (c.€6.1bn capex, €42.2bn revenue FY2024) while UK merger scrutiny and high spectrum fees (UK 2021 ~£1.4bn; EU 2022 >€10bn) add regulatory deal and cost risks.

| Item | Metric |

|---|---|

| Vodacom revenue FY2024 | ZAR 66.1bn |

| Vodafone revenue FY2024 | €42.2bn |

| Vodafone capex FY2024 | €6.1bn (+8%) |

| UK spectrum (2021) | ~£1.4bn |

| EU spectrum (2022) | >€10bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vodafone Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

A concise PESTLE summary of Vodafone Group that’s visually segmented for quick interpretation, easily dropped into presentations, editable for regional or business-line notes, and ideal for aligning teams on external risks and market positioning during planning sessions.

Economic factors

Inflationary pressures on operating costs

Persistently high inflation across Vodafone’s European markets pushed energy and labor costs up; Euro area CPI averaged 5.6% in 2024, increasing OPEX for Vodafone’s ~100,000-strong workforce and network sites.

To protect margins Vodafone implemented inflation-linked contractual price rises—Vodafone Group reported a 3.5% blended price increase in 2024—risking higher churn as ARPU pressure mounts.

Balancing rising input costs against consumer affordability remains critical: Vodafone’s 2024 operating margin fell 0.9 percentage points year-on-year, highlighting the tight trade-off between pass-through and retention.

Interest rate volatility and debt servicing

As a capital‑intensive operator with net debt of about 33.6 billion euros at FY2024 (March 2024), Vodafone is highly sensitive to central bank rate moves; a 100bp rise can materially raise annual interest expense on refinancings. Higher rates increase costs for funding fiber‑to‑the‑home rollout and M&A, while analysts monitor Vodafone’s FY2024 EBITDA/net debt ~2.6x and interest coverage to assess refinancing risk amid shifting global monetary policy.

Currency exchange rate fluctuations

Vodafone operates across 20+ countries and reports material exposure to the euro, pound and multiple African currencies; FX moves cut reported EBITDA — FX translation reduced FY2024 group service revenue by about 1.2% and adjusted EBITDA by ~1.5% versus constant currency, per Vodafone FY2024 results.

Economic growth rates in core markets

The demand for premium mobile and data services tracks GDP and disposable income; Vodafone’s European markets saw GDP growth of just 0.6% in 2023–2024, constraining upgrades to high-tier plans and enterprise digital spend.

Stagnant European growth limits ARPU expansion, while African markets—growing GDP ~3–4% and urbanization rates rising—boost uptake of mobile money and data, contributing double-digit revenue growth in select markets.

- European GDP ~0.6% (2023–24) depresses premium plan uptake

- Africa GDP ~3–4% with rising urbanization supports mobile financial services

- Stagnant growth limits ARPU/enterprise spend; African growth offers revenue tailwinds

Consolidation and market competition dynamics

The economic rationale for consolidation, exemplified by the proposed £15.3bn merger with Three UK, is to achieve scale for c.£20–30bn industry 5G capex needs and reduce duplicated network costs, improving capital efficiency.

Intense price pressure from MVNOs and rivals has pushed UK ARPU down; Vodafone UK ARPU fell about 3% y/y to ~£20 in 2024, compressing margins.

Vodafone’s strategy emphasizes portfolio optimization—exiting non-core markets and cost synergies to lift free cash flow and shareholder returns.

- Merger target: £15.3bn (Three deal)

- Estimated 5G capex: £20–30bn industry-wide

- UK ARPU 2024: ~£20 (down ~3% y/y)

- Focus: exits, synergies, FCF improvement

Vodafone: Inflation, FX and debt squeeze growth—EU ARPU down, Africa offsets

High inflation raised OPEX; Euro area CPI 5.6% (2024) and FY2024 net debt €33.6bn increased funding costs. Vodafone posted 3.5% blended price rises (2024) while FY2024 EBITDA/net debt ~2.6x; FX reduced service revenue ~1.2% and adj. EBITDA ~1.5%. European GDP ~0.6% (2023–24) constrained ARPU (~£20 UK, -3% y/y), African GDP ~3–4% supported data/mobile money growth.

| Metric | 2024 |

|---|---|

| Euro CPI | 5.6% |

| Net debt | €33.6bn |

| Price rise | 3.5% |

| EBITDA/net debt | ~2.6x |

| FX hit | Rev -1.2%, EBITDA -1.5% |

| UK ARPU | ~£20 (-3%) |

| EU GDP | ~0.6% |

| Africa GDP | 3–4% |

What You See Is What You Get

Vodafone Group PESTLE Analysis

The preview shown here is the exact Vodafone Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Navigate Vodafone Group’s external landscape with our concise PESTLE snapshot—highlighting regulatory risks, macroeconomic pressures, tech disruption, and social shifts that shape strategy and valuation; buy the full PESTLE for a detailed, actionable report you can use in investor decks or strategic plans.

Political factors

Geopolitical instability in African markets

Vodafone’s exposure in Africa via Vodacom—which generated ZAR 66.1bn revenue in FY2024—faces risks from political volatility and regime changes that can threaten infrastructure security and service continuity. Recent government shifts in countries like Sudan and Ethiopia have forced intensified diplomatic engagement to protect assets and licences. Analysts should watch for nationalization risk and abrupt telecom policy changes that could affect EBITDA and capex forecasts.

EU regulatory alignment and digital sovereignty

The EU push for digital sovereignty compels Vodafone to localize data processing and favor trusted infrastructure partners, impacting capital allocation—Vodafone reported c.€3.2bn in network capex in FY2024, with vendor swaps for 5G upgrades adding hundreds of millions in transition costs. Political pressure to exclude high‑risk vendors accelerated equipment replacements and strategic pivots, while balancing Brussels’ directives with divergent national policies remains a top management challenge.

Post-Brexit UK telecommunications policy

Post-Brexit scrutiny intensified after Vodafone’s planned merger with Three UK triggered investigations by the CMA and National Security Advisors, raising risks to deal approval and potential remedies that could exceed 1–2 billion GBP; UK policy on digital infrastructure—pledged 5 billion GBP under Project Gigabit targets—will directly shape Vodafone’s capex and network integration timelines through 2025–2030.

Governmental influence on spectrum auctions

Government agendas shape timing and pricing of spectrum auctions crucial for Vodafone’s 5G rollout; UK 5G auctions raised about 1.4 billion GBP in 2021 and EU-wide auctions generated over 10 billion EUR in 2022, increasing licensing costs and pressuring Vodafone’s capital expenditures and balance sheet.

High reserve prices aimed at revenue can prioritize state coffers over network quality, while strategic lobbying and regulatory engagement are essential to push auction designs that lower upfront fees, enable installment payments, or reserve spectrum for coverage obligations to support sustainable deployment.

- 2021 UK auctions: ~1.4 billion GBP raised

- EU auctions (2022): >10 billion EUR

- High license costs increase CAPEX and leverage risks

- Lobbying can secure favorable payment terms and coverage-focused auction rules

Trade relations and global supply chain policies

Ongoing US-China tensions and EU export controls have raised prices for semiconductors and 5G radio units; global chip supply shortages in 2024 pushed telecom capex up ~8%, squeezing Vodafone Group EBITDA margins (2024 revenue €42.2bn, capex €6.1bn).

Sanctions and export controls force Vodafone to adjust procurement for vendors and delay 5G/FTTH rollouts; supplier diversification increased sourcing costs and inventory levels in 2024.

Changes in trade agreements and potential tariffs on imported network equipment could raise unit costs, reducing profitability on international projects and increasing total cost of ownership for infrastructure.

- 2024 revenue €42.2bn, capex €6.1bn

- Capex +8% vs prior year due partly to supply-driven price rises

- Supply-chain risk: sanctions/export controls impacting vendor choices

- Tariff shifts threaten equipment unit cost and project margins

Regulatory, nationalization and spectrum risks squeeze Vodafone & Vodacom margins

Political volatility in Africa (Vodacom ZAR 66.1bn FY2024) and nationalization risks threaten assets and EBITDA; EU digital sovereignty and vendor exclusions raised Vodafone capex pressure (c.€6.1bn capex, €42.2bn revenue FY2024) while UK merger scrutiny and high spectrum fees (UK 2021 ~£1.4bn; EU 2022 >€10bn) add regulatory deal and cost risks.

| Item | Metric |

|---|---|

| Vodacom revenue FY2024 | ZAR 66.1bn |

| Vodafone revenue FY2024 | €42.2bn |

| Vodafone capex FY2024 | €6.1bn (+8%) |

| UK spectrum (2021) | ~£1.4bn |

| EU spectrum (2022) | >€10bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vodafone Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context.

A concise PESTLE summary of Vodafone Group that’s visually segmented for quick interpretation, easily dropped into presentations, editable for regional or business-line notes, and ideal for aligning teams on external risks and market positioning during planning sessions.

Economic factors

Inflationary pressures on operating costs

Persistently high inflation across Vodafone’s European markets pushed energy and labor costs up; Euro area CPI averaged 5.6% in 2024, increasing OPEX for Vodafone’s ~100,000-strong workforce and network sites.

To protect margins Vodafone implemented inflation-linked contractual price rises—Vodafone Group reported a 3.5% blended price increase in 2024—risking higher churn as ARPU pressure mounts.

Balancing rising input costs against consumer affordability remains critical: Vodafone’s 2024 operating margin fell 0.9 percentage points year-on-year, highlighting the tight trade-off between pass-through and retention.

Interest rate volatility and debt servicing

As a capital‑intensive operator with net debt of about 33.6 billion euros at FY2024 (March 2024), Vodafone is highly sensitive to central bank rate moves; a 100bp rise can materially raise annual interest expense on refinancings. Higher rates increase costs for funding fiber‑to‑the‑home rollout and M&A, while analysts monitor Vodafone’s FY2024 EBITDA/net debt ~2.6x and interest coverage to assess refinancing risk amid shifting global monetary policy.

Currency exchange rate fluctuations

Vodafone operates across 20+ countries and reports material exposure to the euro, pound and multiple African currencies; FX moves cut reported EBITDA — FX translation reduced FY2024 group service revenue by about 1.2% and adjusted EBITDA by ~1.5% versus constant currency, per Vodafone FY2024 results.

Economic growth rates in core markets

The demand for premium mobile and data services tracks GDP and disposable income; Vodafone’s European markets saw GDP growth of just 0.6% in 2023–2024, constraining upgrades to high-tier plans and enterprise digital spend.

Stagnant European growth limits ARPU expansion, while African markets—growing GDP ~3–4% and urbanization rates rising—boost uptake of mobile money and data, contributing double-digit revenue growth in select markets.

- European GDP ~0.6% (2023–24) depresses premium plan uptake

- Africa GDP ~3–4% with rising urbanization supports mobile financial services

- Stagnant growth limits ARPU/enterprise spend; African growth offers revenue tailwinds

Consolidation and market competition dynamics

The economic rationale for consolidation, exemplified by the proposed £15.3bn merger with Three UK, is to achieve scale for c.£20–30bn industry 5G capex needs and reduce duplicated network costs, improving capital efficiency.

Intense price pressure from MVNOs and rivals has pushed UK ARPU down; Vodafone UK ARPU fell about 3% y/y to ~£20 in 2024, compressing margins.

Vodafone’s strategy emphasizes portfolio optimization—exiting non-core markets and cost synergies to lift free cash flow and shareholder returns.

- Merger target: £15.3bn (Three deal)

- Estimated 5G capex: £20–30bn industry-wide

- UK ARPU 2024: ~£20 (down ~3% y/y)

- Focus: exits, synergies, FCF improvement

Vodafone: Inflation, FX and debt squeeze growth—EU ARPU down, Africa offsets

High inflation raised OPEX; Euro area CPI 5.6% (2024) and FY2024 net debt €33.6bn increased funding costs. Vodafone posted 3.5% blended price rises (2024) while FY2024 EBITDA/net debt ~2.6x; FX reduced service revenue ~1.2% and adj. EBITDA ~1.5%. European GDP ~0.6% (2023–24) constrained ARPU (~£20 UK, -3% y/y), African GDP ~3–4% supported data/mobile money growth.

| Metric | 2024 |

|---|---|

| Euro CPI | 5.6% |

| Net debt | €33.6bn |

| Price rise | 3.5% |

| EBITDA/net debt | ~2.6x |

| FX hit | Rev -1.2%, EBITDA -1.5% |

| UK ARPU | ~£20 (-3%) |

| EU GDP | ~0.6% |

| Africa GDP | 3–4% |

What You See Is What You Get

Vodafone Group PESTLE Analysis

The preview shown here is the exact Vodafone Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the file you’ll download immediately after payment, with no placeholders or surprises.