GOL Porter's Five Forces Analysis

From Overview to Strategy Blueprint

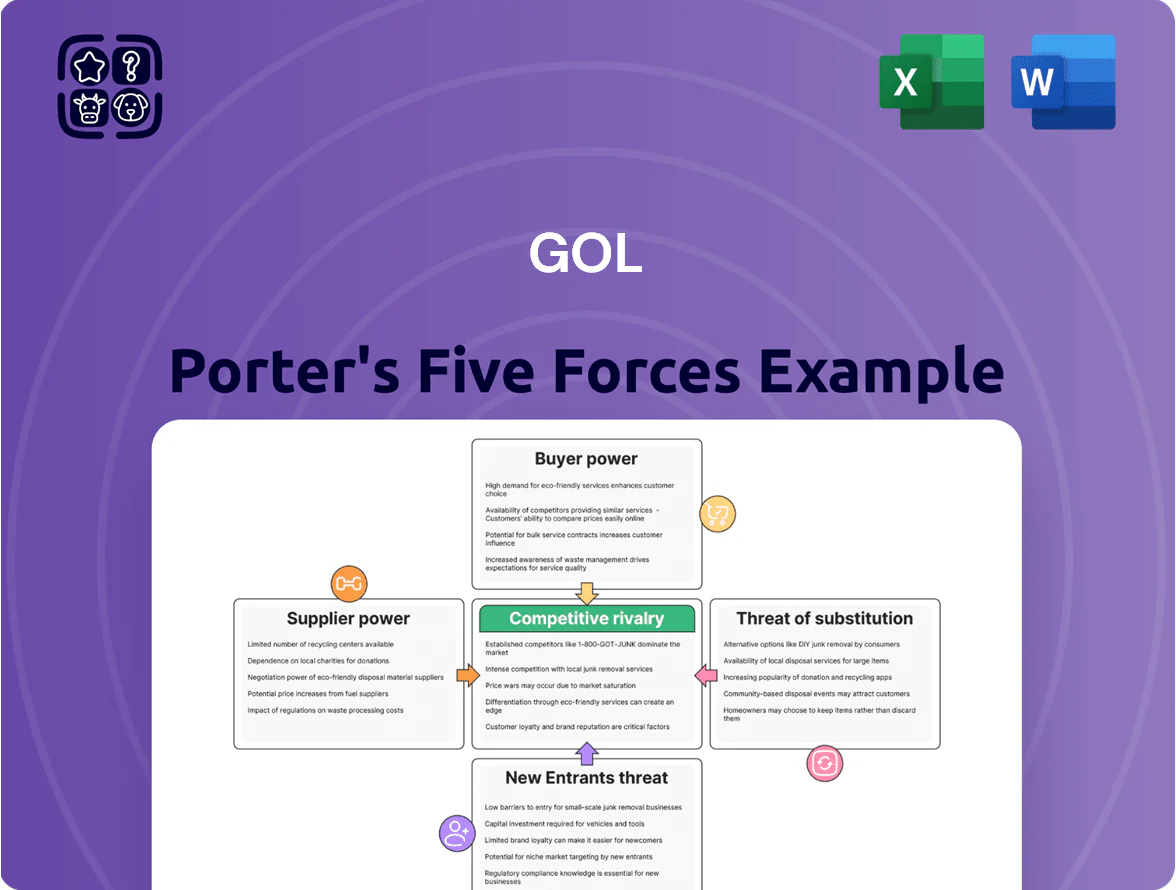

GOL faces intense competitive rivalry from domestic carriers and low-cost entrants, while fluctuating fuel costs and concentrated suppliers pressure margins and operational resilience.

Buyer power is elevated by price-sensitive travelers and corporate contracts, and the threat of substitutes—rail, buses, and virtual meetings—tempers pricing flexibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GOL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Aircraft Manufacturers

The global commercial jet market is a Boeing-Airbus duopoly, and GOL’s reliance on Boeing 737 MAX gives Boeing outsized leverage in pricing, delivery schedules and technical support.

Supply-chain disruptions and MAX delivery delays through 2025 cut GOL’s planned fleet growth by roughly 15% and slowed retirements of older, less fuel-efficient aircraft, raising unit costs.

With few OEM alternatives, GOL faces limited negotiating power on purchase terms, spare parts pricing and warranty support, increasing operational and capital expenditure risk.

Fuel Supply and Petrobras Dominance

Aviation kerosene is among GOL’s largest costs, about 30–35% of operating expenses in 2024; in Brazil Petrobras (Petróleo Brasileiro S.A.) controls ~70–80% of fuel distribution, limiting local supplier choice.

International price-parity rules exist, but Petrobras’ regional pricing and logistical bottlenecks exposed GOL to fuel-cost swings of ±15–20% year-on-year in 2023–24, tightening margins.

GOL’s bargaining power is weak: monopolistic domestic infrastructure and limited storage capacity constrain long-term hedges and volume discounts, raising fuel-cost risk.

Influence of Aircraft Lessors

As GOL emerges from Chapter 11 at end-2025, aircraft lessors hold strong leverage: they control lease renewals and repossessions that directly affect GOL’s ability to operate its ~130 narrow-body fleet (A320 family/737 NG), and global lessor demand kept narrow-body lease rates ~5–10% higher in 2024–25. Successful contract renegotiations in restructuring reduced near-term cash outflows, but lessors retain bargaining power given tight used-aircraft markets and limited alternative funding.

Infrastructure and Airport Monopolies

Airport operators in Brazil—state-run and private concessionaires—hold strong bargaining power because their services (runways, terminals, slots) are essential and non-substitutable for GOL; in 2024 aeroportuária charges made up roughly 8–10% of domestic unit costs for Brazilian carriers.

GOL pays regulated landing, parking and passenger fees that are largely non-negotiable and indexed to inflation; ANAC/infraero concession terms raised average airport tariffs ~4.5% in 2023–24.

Limited slots at congested airports like São Paulo Congonhas (operating near 100% daytime capacity, ~1,300 movements/day in 2024) increase supplier leverage, constraining GOL’s scheduling flexibility and yield management.

- Essential, non-substitutable services → high leverage

- Fees non-negotiable, inflation-linked (~4–5% recent hikes)

- Congonhas ~100% capacity → scarce slots, pricing power

Specialized Labor Unions

GOL faces strong supplier power from specialized labor unions for pilots and maintenance techs in Brazil; in 2024 Brazil’s commercial pilot shortage tightened, pushing average pilot wages up ~12% year-over-year and technician pay by ~9%.

Collective bargaining sets crew costs that were ~22% of GOL’s 2024 operating expenses, reducing flexibility; strikes or wage demands can cut capacity and add immediate cash costs.

Skills are hard to replace quickly—training a commercial pilot takes 18–24 months—so labor actions directly hit revenues and margin.

- 2024: pilot wages +12%

- 2024: tech wages +9%

- Crew costs ≈22% of operating expenses (2024)

- Pilot training 18–24 months

GOL under supplier squeeze: fuel, lessors & wages drive costs skyward

GOL faces high supplier power: Boeing duopoly limits aircraft leverage; Petrobras controls ~70–80% fuel distribution making fuel 30–35% of opex (2024); lessors and airports hold strong leverage with lease rates +5–10% and airport charges ~8–10% of unit costs; pilot/tech wages rose ~12%/9% in 2024, crew costs ≈22% of opex.

| Item | 2024–25 |

|---|---|

| Fuel share of opex | 30–35% |

| Petrobras market share | 70–80% |

| Crew costs | ≈22% opex |

| Pilot wage change | +12% |

| Leasing rate gap | +5–10% |

| Airport charges | 8–10% unit costs |

What is included in the product

Tailored Porter's Five Forces analysis for GOL that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to its market share, with strategic commentary for decision-making.

A concise Porter's Five Forces snapshot for GOL that highlights competitive pressures and opportunity levers—ideal for rapid strategic decisions.

Customers Bargaining Power

High Price Sensitivity in the Low-Cost Segment

GOL’s core customers are leisure and price-sensitive business flyers who pick fares over loyalty; in 2024 domestic leisure traffic made up ~68% of passengers, pushing intense price focus.

Real-time fare comparison via OTAs and metasearch (Skyscanner, Google Flights) means GOL matches market fares; Brazil’s online share hit ~55% of bookings in 2024.

That price transparency caps GOL’s pricing power, so during 2023–24 fuel and inflation shocks the carrier absorbed costs rather than raising fares, squeezing margins—EBIT margin swung to ~3% in 2024.

Low Switching Costs for Passengers

For most domestic Brazilian routes, passengers face no financial penalty switching from GOL to LATAM or Azul, and industry data shows leisure fares fluctuate by 5–15% across carriers as of 2025, reinforcing easy switching. Air travel is commoditized: on-time performance and seat offering are within single-digit percentage points among the three, so buyers pick schedule and price. This low friction concentrates bargaining power with travelers, pressuring GOLs yields and ancillary revenue.

Influence of Digital Comparison Tools

Online Travel Agencies (OTAs) and meta-search engines like Booking Holdings and Google Flights give customers full visibility into fares, timings, and baggage fees, boosting buyer power; OTAs accounted for about 38% of global airline bookings in 2024, so many decisions happen off-airline sites.

These tools show aggregated price and duration in seconds, and GOL must optimize distribution and pay up to 15–25% commission or bid higher on metasearch to keep inventory prominent and attractive.

Corporate Travel Procurement Power

Loyalty Program Stickiness and Redemption

Loyalty program Smiles boosts retention but breeds savvy users who wait for promotional redemptions or exhaust miles to avoid cash fares, pressuring GOL’s yield management; in 2024 Smiles accounted for ~18% of passenger revenue redemptions, lowering average ticket yield by an estimated 6–8% on redeemed seats.

GOL faces a trade-off: subsidize attractive earn/redeem rates—Smiles liabilities were BRL 1.2bn at end-2024—or push cash sales, risking churn among high-value members.

Leisure-led demand, OTAs & Smiles redemptions squeeze yields—EBIT ≈3%, discounts bite

Buyers hold strong power: leisure price-focus (68% of passengers 2024) plus 55% online booking share and OTA/meta visibility cap fares; yields compressed (EBIT ≈3% 2024). Corporate buyers (≈18% market 2024) extract discounts, cutting unit margins ~150–250 bps. Smiles redemptions ≈18% passenger revenue and BRL 1.2bn liability (FY2024) lower yield ~6–8% on redeemed seats.

| Metric | Value (2024) |

|---|---|

| Leisure share | 68% |

| Online booking share | 55% |

| EBIT margin | ≈3% |

| Corporate market share | 18% |

| Smiles redemptions | ≈18% passenger rev |

| Smiles liability | BRL 1.2bn |

Same Document Delivered

GOL Porter's Five Forces Analysis

This preview shows the exact GOL Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

GOL faces intense competitive rivalry from domestic carriers and low-cost entrants, while fluctuating fuel costs and concentrated suppliers pressure margins and operational resilience.

Buyer power is elevated by price-sensitive travelers and corporate contracts, and the threat of substitutes—rail, buses, and virtual meetings—tempers pricing flexibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GOL’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Aircraft Manufacturers

The global commercial jet market is a Boeing-Airbus duopoly, and GOL’s reliance on Boeing 737 MAX gives Boeing outsized leverage in pricing, delivery schedules and technical support.

Supply-chain disruptions and MAX delivery delays through 2025 cut GOL’s planned fleet growth by roughly 15% and slowed retirements of older, less fuel-efficient aircraft, raising unit costs.

With few OEM alternatives, GOL faces limited negotiating power on purchase terms, spare parts pricing and warranty support, increasing operational and capital expenditure risk.

Fuel Supply and Petrobras Dominance

Aviation kerosene is among GOL’s largest costs, about 30–35% of operating expenses in 2024; in Brazil Petrobras (Petróleo Brasileiro S.A.) controls ~70–80% of fuel distribution, limiting local supplier choice.

International price-parity rules exist, but Petrobras’ regional pricing and logistical bottlenecks exposed GOL to fuel-cost swings of ±15–20% year-on-year in 2023–24, tightening margins.

GOL’s bargaining power is weak: monopolistic domestic infrastructure and limited storage capacity constrain long-term hedges and volume discounts, raising fuel-cost risk.

Influence of Aircraft Lessors

As GOL emerges from Chapter 11 at end-2025, aircraft lessors hold strong leverage: they control lease renewals and repossessions that directly affect GOL’s ability to operate its ~130 narrow-body fleet (A320 family/737 NG), and global lessor demand kept narrow-body lease rates ~5–10% higher in 2024–25. Successful contract renegotiations in restructuring reduced near-term cash outflows, but lessors retain bargaining power given tight used-aircraft markets and limited alternative funding.

Infrastructure and Airport Monopolies

Airport operators in Brazil—state-run and private concessionaires—hold strong bargaining power because their services (runways, terminals, slots) are essential and non-substitutable for GOL; in 2024 aeroportuária charges made up roughly 8–10% of domestic unit costs for Brazilian carriers.

GOL pays regulated landing, parking and passenger fees that are largely non-negotiable and indexed to inflation; ANAC/infraero concession terms raised average airport tariffs ~4.5% in 2023–24.

Limited slots at congested airports like São Paulo Congonhas (operating near 100% daytime capacity, ~1,300 movements/day in 2024) increase supplier leverage, constraining GOL’s scheduling flexibility and yield management.

- Essential, non-substitutable services → high leverage

- Fees non-negotiable, inflation-linked (~4–5% recent hikes)

- Congonhas ~100% capacity → scarce slots, pricing power

Specialized Labor Unions

GOL faces strong supplier power from specialized labor unions for pilots and maintenance techs in Brazil; in 2024 Brazil’s commercial pilot shortage tightened, pushing average pilot wages up ~12% year-over-year and technician pay by ~9%.

Collective bargaining sets crew costs that were ~22% of GOL’s 2024 operating expenses, reducing flexibility; strikes or wage demands can cut capacity and add immediate cash costs.

Skills are hard to replace quickly—training a commercial pilot takes 18–24 months—so labor actions directly hit revenues and margin.

- 2024: pilot wages +12%

- 2024: tech wages +9%

- Crew costs ≈22% of operating expenses (2024)

- Pilot training 18–24 months

GOL under supplier squeeze: fuel, lessors & wages drive costs skyward

GOL faces high supplier power: Boeing duopoly limits aircraft leverage; Petrobras controls ~70–80% fuel distribution making fuel 30–35% of opex (2024); lessors and airports hold strong leverage with lease rates +5–10% and airport charges ~8–10% of unit costs; pilot/tech wages rose ~12%/9% in 2024, crew costs ≈22% of opex.

| Item | 2024–25 |

|---|---|

| Fuel share of opex | 30–35% |

| Petrobras market share | 70–80% |

| Crew costs | ≈22% opex |

| Pilot wage change | +12% |

| Leasing rate gap | +5–10% |

| Airport charges | 8–10% unit costs |

What is included in the product

Tailored Porter's Five Forces analysis for GOL that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats to its market share, with strategic commentary for decision-making.

A concise Porter's Five Forces snapshot for GOL that highlights competitive pressures and opportunity levers—ideal for rapid strategic decisions.

Customers Bargaining Power

High Price Sensitivity in the Low-Cost Segment

GOL’s core customers are leisure and price-sensitive business flyers who pick fares over loyalty; in 2024 domestic leisure traffic made up ~68% of passengers, pushing intense price focus.

Real-time fare comparison via OTAs and metasearch (Skyscanner, Google Flights) means GOL matches market fares; Brazil’s online share hit ~55% of bookings in 2024.

That price transparency caps GOL’s pricing power, so during 2023–24 fuel and inflation shocks the carrier absorbed costs rather than raising fares, squeezing margins—EBIT margin swung to ~3% in 2024.

Low Switching Costs for Passengers

For most domestic Brazilian routes, passengers face no financial penalty switching from GOL to LATAM or Azul, and industry data shows leisure fares fluctuate by 5–15% across carriers as of 2025, reinforcing easy switching. Air travel is commoditized: on-time performance and seat offering are within single-digit percentage points among the three, so buyers pick schedule and price. This low friction concentrates bargaining power with travelers, pressuring GOLs yields and ancillary revenue.

Influence of Digital Comparison Tools

Online Travel Agencies (OTAs) and meta-search engines like Booking Holdings and Google Flights give customers full visibility into fares, timings, and baggage fees, boosting buyer power; OTAs accounted for about 38% of global airline bookings in 2024, so many decisions happen off-airline sites.

These tools show aggregated price and duration in seconds, and GOL must optimize distribution and pay up to 15–25% commission or bid higher on metasearch to keep inventory prominent and attractive.

Corporate Travel Procurement Power

Loyalty Program Stickiness and Redemption

Loyalty program Smiles boosts retention but breeds savvy users who wait for promotional redemptions or exhaust miles to avoid cash fares, pressuring GOL’s yield management; in 2024 Smiles accounted for ~18% of passenger revenue redemptions, lowering average ticket yield by an estimated 6–8% on redeemed seats.

GOL faces a trade-off: subsidize attractive earn/redeem rates—Smiles liabilities were BRL 1.2bn at end-2024—or push cash sales, risking churn among high-value members.

Leisure-led demand, OTAs & Smiles redemptions squeeze yields—EBIT ≈3%, discounts bite

Buyers hold strong power: leisure price-focus (68% of passengers 2024) plus 55% online booking share and OTA/meta visibility cap fares; yields compressed (EBIT ≈3% 2024). Corporate buyers (≈18% market 2024) extract discounts, cutting unit margins ~150–250 bps. Smiles redemptions ≈18% passenger revenue and BRL 1.2bn liability (FY2024) lower yield ~6–8% on redeemed seats.

| Metric | Value (2024) |

|---|---|

| Leisure share | 68% |

| Online booking share | 55% |

| EBIT margin | ≈3% |

| Corporate market share | 18% |

| Smiles redemptions | ≈18% passenger rev |

| Smiles liability | BRL 1.2bn |

Same Document Delivered

GOL Porter's Five Forces Analysis

This preview shows the exact GOL Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or mockups.