Voestalpine Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

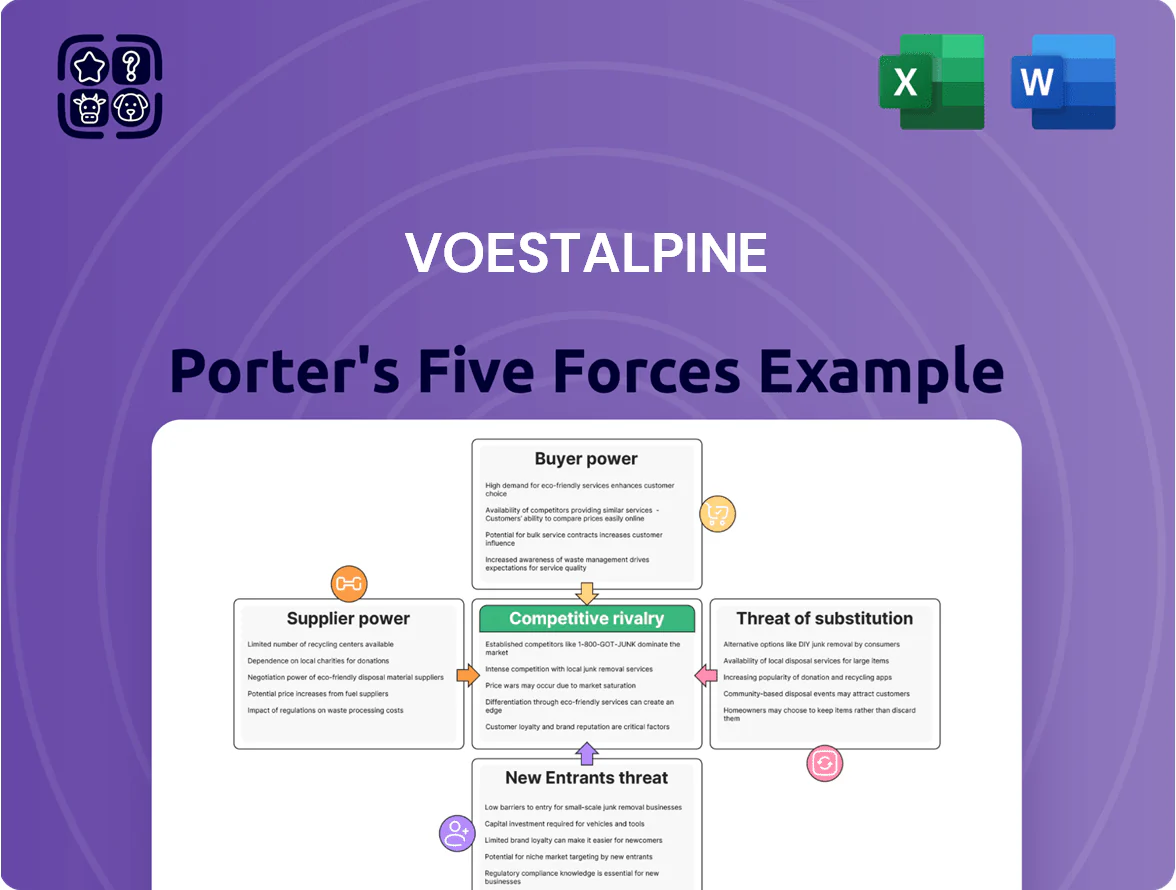

Voestalpine faces mixed pressures: strong supplier influence for specialized steel inputs, high buyer power in commoditized segments, moderate threat from substitutes and new entrants due to high capital intensity, and intense rivalry among global steelmakers—this snapshot highlights strategic vulnerabilities and opportunities.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Voestalpine’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Market Concentration

The global iron ore and coking coal supply is concentrated: in 2024 the top five miners (BHP, Rio Tinto, Vale, Anglo American, Glencore) supplied ~70% of seaborne iron ore and top three coal exporters (Australia, Indonesia, Russia) dominated coking coal exports, giving suppliers pricing power over steelmakers like Voestalpine.

Voestalpine depends on these inputs for ~80% of its blast furnace feedstock; spot iron ore jumped 45% in 2021–2022 and remained volatile, raising input-cost risk and margin pressure.

By late 2025 demand for higher-grade ores for low-CO2 routes trimmed viable suppliers by an estimated 20–30%, further concentrating supply and increasing bargaining power versus Voestalpine.

Energy Transition and Utility Providers

As Voestalpine shifts to greentec steel, its need for reliable renewable power and green hydrogen rises, boosting suppliers’ bargaining power; Europe’s industrial green hydrogen capacity was ~0.2 GW electrolyser in 2023 vs projected 40 GW needed by 2030, so supply lags demand. Hydrogen delivery infrastructure is nascent, driving premium prices—industrial green H2 contracts quoted €3–6/kg in 2024—so Voestalpine must lock long-term deals to control decarbonization costs and capex.

Specialized Technology and Equipment Vendors

Voestalpine depends on highly specialized machinery and digital solutions for precision and aerospace parts, and only a handful of global vendors (eg, Siemens, ABB, FANUC) supply advanced sensors and automation, concentrating supply; this lets suppliers hold firm pricing—vendor contracts rose ~6–8% annually in the sector in 2024—and demand long-term service agreements, raising capex predictability but increasing supplier bargaining power.

Logistics and Transport Constraints

Suppliers of rail and maritime freight exert strong leverage over voestalpine because steel and slabs are bulky—transport can account for 10–20% of delivered cost. In 2025, S&P Global estimated container freight volatility rose 28% vs. 2019 and EU carbon transport taxes added €15–€30/tonne CO2 on routes, shrinking low-cost carrier options.

Voestalpine must secure long-term rail slots and shift more volume to short-sea and inland waterways to limit transport cost exposure and preserve margins.

- Transport = 10–20% of delivered cost

- Freight volatility +28% vs 2019 (S&P Global, 2025)

- EU transport carbon cost €15–€30/tCO2 (2025)

- Need: long-term rail contracts, short-sea, inland waterways

Scrap Metal Availability

Scrap metal availability tightens Voestalpine’s supplier power: rising electric arc furnace (EAF) adoption across Europe drove premium scrap prices up ~28% from 2020–2024, and Voestalpine reports higher input cost pressure and shorter procurement windows to meet 2030 CO2 targets.

Regulation and circular-economy competition mean suppliers extract premiums; Voestalpine faces bigger working-capital needs and a need to secure long-term scrap contracts to avoid margin erosion.

- Premium scrap price rise ~28% (2020–2024)

- Higher working-capital needs

- Shorter supply windows, tighter contracts

- Regulation boosts supplier bargaining power

Supplier squeeze: ore concentration, rising costs & dwindling high‑grade supply

Suppliers hold high bargaining power: seaborne iron ore/top miners ~70% (2024), Voestalpine relies on ~80% blast-furnace feedstock, spot ore volatility (45% jump 2021–22) and 20–30% fewer viable high-grade suppliers (late 2025) raise costs; green H2 €3–6/kg (2024) and EU transport carbon €15–30/tCO2 (2025) add pressure; scrap +28% (2020–24) tightens supply.

| Metric | Value |

|---|---|

| Seaborne iron ore share | ~70% (top5, 2024) |

| Blast-furnace feedstock dependence | ~80% |

| Spot ore move | +45% (2021–22) |

| High-grade supplier drop | 20–30% (by late 2025) |

| Green H2 price | €3–6/kg (2024) |

| EU transport carbon | €15–30/tCO2 (2025) |

| Scrap price change | +28% (2020–24) |

What is included in the product

Tailored exclusively for Voestalpine, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers and substitutes, and highlights disruptive threats and pricing pressures shaping the company's profitability.

Concise Porter's Five Forces snapshot for voestalpine—quickly assess competitive pressures and relieve decision fatigue with a single, slide-ready summary.

Customers Bargaining Power

Consolidation of Automotive OEMs

The automotive sector is Voestalpine’s key customer; global OEMs consolidated into roughly 20 major groups by 2024, concentrating purchasing power and pushing for lower input costs as they invest ~$330 billion in electric vehicle platforms through 2025. Large OEMs demand high-performance materials at scale to cut vehicle weight and costs, raising price pressure on suppliers. Voestalpine defends margin by selling proprietary high-strength steels—about 15% of steel mix in 2024—critical for safety and mass reduction, which limits OEMs’ ability to switch.

Switching Costs in Aerospace and Railway

In aerospace and railway infrastructure, switching costs are high because safety certifications and specs take years and cost millions; for example, EASA and FAA certification programs can exceed $5–20m per component. Voestalpine's certified rail systems and turbine parts create technical lock-in, making supplier replacement risky and costly for buyers and lowering customers' immediate bargaining power despite contracts often worth €10–50m each.

Price Sensitivity in Commodity Steel Segments

Voestalpine’s commodity steel lines face strong price pressure as global buyers can switch suppliers; standardized coils and plates trade near global spot averages, compressing margins to single digits in 2024–25. By end-2025, weaker demand and raw-material volatility made buyers 15–20% more price-sensitive, lowering loyalty and prioritizing cost over brand. Voestalpine therefore pushes value-added services—processing, just-in-time logistics—to protect pricing and recover ~€50–80/tonne in premium.

Demand for Green Steel Certifications

Industrial buyers face rising Scope 3 reporting rules—EU ETS/CBAM and corporate targets pushed 30–50% of steel users in 2024 to request low‑carbon inputs—so customers can demand certified green steel and penalize opaque footprints.

Carbon transparency is now a bargaining lever; Voestalpine’s 2024 output of ~0.5 Mt green steel and investments in H2 routes let it satisfy buyers, but clients expect green as standard with minimal price premium.

Direct Sales and Digital Platforms

The rise of digital procurement platforms has raised price and lead-time transparency, giving smaller buyers more negotiating power; industry surveys showed 46% of steel buyers used digital marketplaces in 2024.

Voestalpine built proprietary digital interfaces and EDI/API integrations, improving data sharing and shortening order cycles by up to 20% in pilot programs.

This keeps customer ties closer but forces ongoing UX and data-analytics investment to stop migration to third-party marketplaces.

- 46% of buyers used digital marketplaces (2024)

- Voestalpine pilots cut order cycles ~20%

- Proprietary APIs improve data integration

- Continuous innovation needed to retain buyers

Mixed buyer power: OEM price pressure, high-cert buyers, carbon & digital shift negotiations

Customers’ bargaining power is mixed: consolidated auto OEMs (≈20 groups) push prices amid ~$330bn EV platform spend through 2025, while certified aerospace/rail buyers face high switching costs (certifications €5–20m). Commodity lines see single‑digit margins; buyers 15–20% more price‑sensitive by end‑2025. Carbon (0.5 Mt green steel in 2024) and digital procurement (46% adoption 2024) shift negotiations toward footprint and service.

| Metric | 2024–25 |

|---|---|

| Auto OEM groups | ≈20 |

| EV platform spend | ≈€330bn to 2025 |

| Green steel output | ≈0.5 Mt (2024) |

| Digital procurement use | 46% (2024) |

| Buyer price sensitivity | +15–20% (end‑2025) |

What You See Is What You Get

Voestalpine Porter's Five Forces Analysis

This preview shows the exact Voestalpine Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Voestalpine faces mixed pressures: strong supplier influence for specialized steel inputs, high buyer power in commoditized segments, moderate threat from substitutes and new entrants due to high capital intensity, and intense rivalry among global steelmakers—this snapshot highlights strategic vulnerabilities and opportunities.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Voestalpine’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Market Concentration

The global iron ore and coking coal supply is concentrated: in 2024 the top five miners (BHP, Rio Tinto, Vale, Anglo American, Glencore) supplied ~70% of seaborne iron ore and top three coal exporters (Australia, Indonesia, Russia) dominated coking coal exports, giving suppliers pricing power over steelmakers like Voestalpine.

Voestalpine depends on these inputs for ~80% of its blast furnace feedstock; spot iron ore jumped 45% in 2021–2022 and remained volatile, raising input-cost risk and margin pressure.

By late 2025 demand for higher-grade ores for low-CO2 routes trimmed viable suppliers by an estimated 20–30%, further concentrating supply and increasing bargaining power versus Voestalpine.

Energy Transition and Utility Providers

As Voestalpine shifts to greentec steel, its need for reliable renewable power and green hydrogen rises, boosting suppliers’ bargaining power; Europe’s industrial green hydrogen capacity was ~0.2 GW electrolyser in 2023 vs projected 40 GW needed by 2030, so supply lags demand. Hydrogen delivery infrastructure is nascent, driving premium prices—industrial green H2 contracts quoted €3–6/kg in 2024—so Voestalpine must lock long-term deals to control decarbonization costs and capex.

Specialized Technology and Equipment Vendors

Voestalpine depends on highly specialized machinery and digital solutions for precision and aerospace parts, and only a handful of global vendors (eg, Siemens, ABB, FANUC) supply advanced sensors and automation, concentrating supply; this lets suppliers hold firm pricing—vendor contracts rose ~6–8% annually in the sector in 2024—and demand long-term service agreements, raising capex predictability but increasing supplier bargaining power.

Logistics and Transport Constraints

Suppliers of rail and maritime freight exert strong leverage over voestalpine because steel and slabs are bulky—transport can account for 10–20% of delivered cost. In 2025, S&P Global estimated container freight volatility rose 28% vs. 2019 and EU carbon transport taxes added €15–€30/tonne CO2 on routes, shrinking low-cost carrier options.

Voestalpine must secure long-term rail slots and shift more volume to short-sea and inland waterways to limit transport cost exposure and preserve margins.

- Transport = 10–20% of delivered cost

- Freight volatility +28% vs 2019 (S&P Global, 2025)

- EU transport carbon cost €15–€30/tCO2 (2025)

- Need: long-term rail contracts, short-sea, inland waterways

Scrap Metal Availability

Scrap metal availability tightens Voestalpine’s supplier power: rising electric arc furnace (EAF) adoption across Europe drove premium scrap prices up ~28% from 2020–2024, and Voestalpine reports higher input cost pressure and shorter procurement windows to meet 2030 CO2 targets.

Regulation and circular-economy competition mean suppliers extract premiums; Voestalpine faces bigger working-capital needs and a need to secure long-term scrap contracts to avoid margin erosion.

- Premium scrap price rise ~28% (2020–2024)

- Higher working-capital needs

- Shorter supply windows, tighter contracts

- Regulation boosts supplier bargaining power

Supplier squeeze: ore concentration, rising costs & dwindling high‑grade supply

Suppliers hold high bargaining power: seaborne iron ore/top miners ~70% (2024), Voestalpine relies on ~80% blast-furnace feedstock, spot ore volatility (45% jump 2021–22) and 20–30% fewer viable high-grade suppliers (late 2025) raise costs; green H2 €3–6/kg (2024) and EU transport carbon €15–30/tCO2 (2025) add pressure; scrap +28% (2020–24) tightens supply.

| Metric | Value |

|---|---|

| Seaborne iron ore share | ~70% (top5, 2024) |

| Blast-furnace feedstock dependence | ~80% |

| Spot ore move | +45% (2021–22) |

| High-grade supplier drop | 20–30% (by late 2025) |

| Green H2 price | €3–6/kg (2024) |

| EU transport carbon | €15–30/tCO2 (2025) |

| Scrap price change | +28% (2020–24) |

What is included in the product

Tailored exclusively for Voestalpine, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, entry barriers and substitutes, and highlights disruptive threats and pricing pressures shaping the company's profitability.

Concise Porter's Five Forces snapshot for voestalpine—quickly assess competitive pressures and relieve decision fatigue with a single, slide-ready summary.

Customers Bargaining Power

Consolidation of Automotive OEMs

The automotive sector is Voestalpine’s key customer; global OEMs consolidated into roughly 20 major groups by 2024, concentrating purchasing power and pushing for lower input costs as they invest ~$330 billion in electric vehicle platforms through 2025. Large OEMs demand high-performance materials at scale to cut vehicle weight and costs, raising price pressure on suppliers. Voestalpine defends margin by selling proprietary high-strength steels—about 15% of steel mix in 2024—critical for safety and mass reduction, which limits OEMs’ ability to switch.

Switching Costs in Aerospace and Railway

In aerospace and railway infrastructure, switching costs are high because safety certifications and specs take years and cost millions; for example, EASA and FAA certification programs can exceed $5–20m per component. Voestalpine's certified rail systems and turbine parts create technical lock-in, making supplier replacement risky and costly for buyers and lowering customers' immediate bargaining power despite contracts often worth €10–50m each.

Price Sensitivity in Commodity Steel Segments

Voestalpine’s commodity steel lines face strong price pressure as global buyers can switch suppliers; standardized coils and plates trade near global spot averages, compressing margins to single digits in 2024–25. By end-2025, weaker demand and raw-material volatility made buyers 15–20% more price-sensitive, lowering loyalty and prioritizing cost over brand. Voestalpine therefore pushes value-added services—processing, just-in-time logistics—to protect pricing and recover ~€50–80/tonne in premium.

Demand for Green Steel Certifications

Industrial buyers face rising Scope 3 reporting rules—EU ETS/CBAM and corporate targets pushed 30–50% of steel users in 2024 to request low‑carbon inputs—so customers can demand certified green steel and penalize opaque footprints.

Carbon transparency is now a bargaining lever; Voestalpine’s 2024 output of ~0.5 Mt green steel and investments in H2 routes let it satisfy buyers, but clients expect green as standard with minimal price premium.

Direct Sales and Digital Platforms

The rise of digital procurement platforms has raised price and lead-time transparency, giving smaller buyers more negotiating power; industry surveys showed 46% of steel buyers used digital marketplaces in 2024.

Voestalpine built proprietary digital interfaces and EDI/API integrations, improving data sharing and shortening order cycles by up to 20% in pilot programs.

This keeps customer ties closer but forces ongoing UX and data-analytics investment to stop migration to third-party marketplaces.

- 46% of buyers used digital marketplaces (2024)

- Voestalpine pilots cut order cycles ~20%

- Proprietary APIs improve data integration

- Continuous innovation needed to retain buyers

Mixed buyer power: OEM price pressure, high-cert buyers, carbon & digital shift negotiations

Customers’ bargaining power is mixed: consolidated auto OEMs (≈20 groups) push prices amid ~$330bn EV platform spend through 2025, while certified aerospace/rail buyers face high switching costs (certifications €5–20m). Commodity lines see single‑digit margins; buyers 15–20% more price‑sensitive by end‑2025. Carbon (0.5 Mt green steel in 2024) and digital procurement (46% adoption 2024) shift negotiations toward footprint and service.

| Metric | 2024–25 |

|---|---|

| Auto OEM groups | ≈20 |

| EV platform spend | ≈€330bn to 2025 |

| Green steel output | ≈0.5 Mt (2024) |

| Digital procurement use | 46% (2024) |

| Buyer price sensitivity | +15–20% (end‑2025) |

What You See Is What You Get

Voestalpine Porter's Five Forces Analysis

This preview shows the exact Voestalpine Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate download and use.