Volker Wessels Stevin NV Porter's Five Forces Analysis

Don't Miss the Bigger Picture

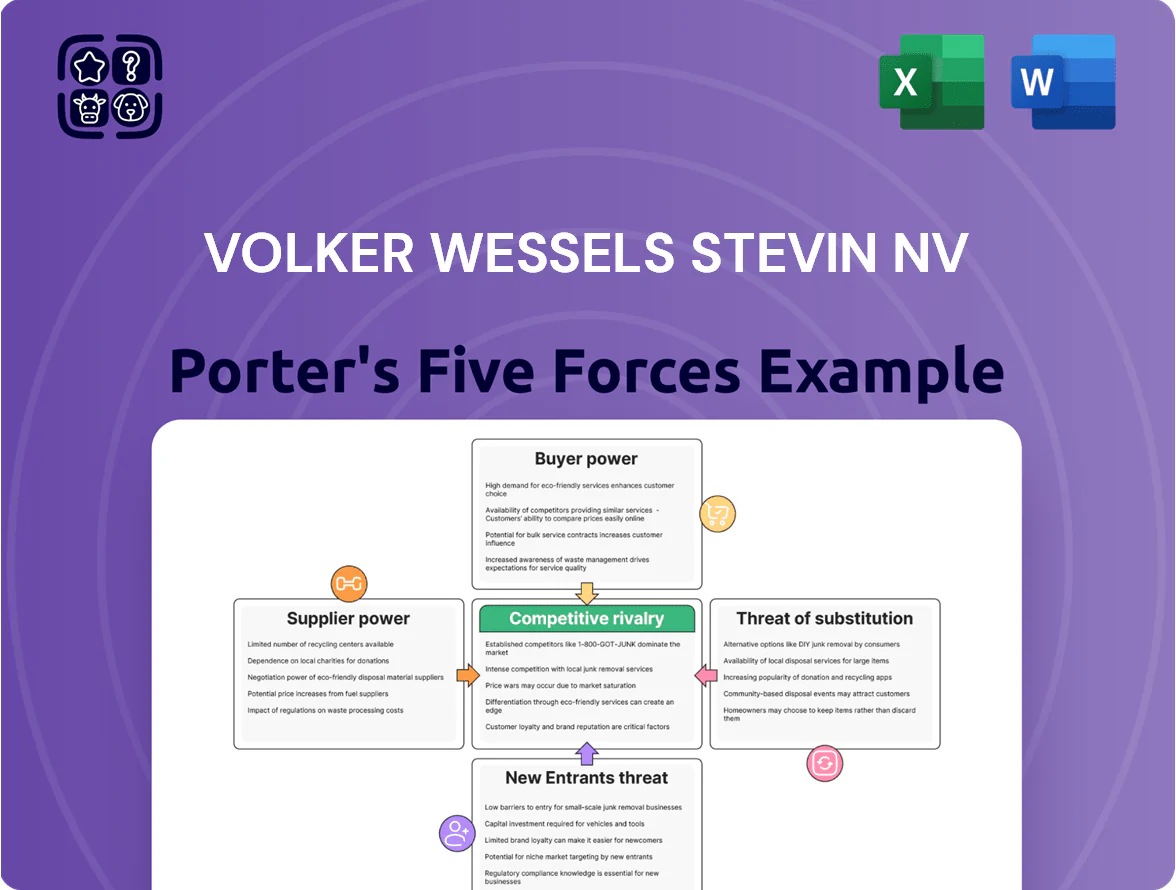

Volker Wessels Stevin NV faces moderate supplier power and high competitive rivalry in infrastructure and construction, with barriers to entry bolstered by scale and regulatory know‑how while buyer power and substitutes exert uneven pressure across segments. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Volker Wessels Stevin NV’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Raw material prices for steel, timber and cement stayed volatile into late 2025, with global steel billet prices up ~18% year-on-year and European cement spot up ~12% amid higher energy costs and supply bottlenecks.

VolkerWessels Stevin NV must use long-term purchase agreements and price-indexation clauses—historically cutting margin swings by ~3–5 percentage points—to insulate project gross margins.

Large integrated producers of steel and cement therefore hold significant supplier leverage, able to pass through cost shocks and influence delivery timing for major infrastructure projects.

Scarcity of specialized labor

A persistent shortage of skilled technicians and engineers across Europe raises supplier power for VolkerWessels Stevin NV, with Eurostat reporting a 2024 EU construction skills gap of ~12% and national shortages up to 20% in the Netherlands. VolkerWessels must pay competitive wages—2024 Dutch construction technician median pay rose 6%—and invest in training programs (estimated €30k–€50k per engineer lifecycle) to secure talent for complex infrastructure projects. This tight labor market limits the company’s ability to cut execution costs and can add 3–5% to project margins through higher labor and subcontractor rates.

Energy transition requirements

Suppliers of certified green materials and zero-emission machinery gain strong leverage as EU and Dutch rules tighten through 2025; about 60% of construction firms report supplier concentration for low-carbon tech in 2024.

VolkerWessels Stevin NV’s carbon-neutral target raises dependence on a few vetted vendors, increasing single-supplier risk and switching costs.

Those niche suppliers can charge premiums—reported 10–25% higher prices for certified equipment in 2023–24—compressing margins unless VolkerWessels secures long-term contracts or vertical partnerships.

Subcontractor dependence

VolkerWessels’ decentralized model depends on local subcontractors for specialist work and regional know-how, creating supplier power where demand is high; in 2024 Dutch construction activity rose ~6%, boosting subcontractor leverage.

In busy regions subcontractors often pick among projects, letting them set prices and schedules; delays or price hikes risk project margins and timelines.

Maintaining long-term partnerships and multi-year frameworks (common in 2023–24 contracts) is critical to secure continuity and quality.

- Decentralized reliance raises supplier leverage

- 2024 NL construction +6% increases subcontractor options

- Subcontractors can dictate price/schedule in hot markets

- Multi-year contracts and strong relationships reduce risk

Logistics and supply chain disruptions

Suppliers with integrated distribution reduced lead times by ~25% in 2024, creating bargaining power; VolkerWessels must diversify suppliers and use regional spare‑parts hubs to avoid single‑source hostage risk.

- 2024 freight cost +18%

- Integrated distributors cut lead times ~25%

- Diversify suppliers; add regional hubs

Supplier squeeze: input costs surge, VolkerWessels shields margins with long-term contracts

Suppliers (steel, cement, green tech, skilled labor, logistics) hold high bargaining power—2024: steel +18% y/y, cement +12%, freight +18%, EU construction skills gap ~12%—forcing VolkerWessels Stevin NV to use long-term contracts, price indexation, training (€30k–€50k/engineer) and supplier diversification to protect margins (typical risk add 3–5%; green premiums 10–25%).

| Metric | 2024–25 |

|---|---|

| Steel | +18% y/y |

| Cement | +12% y/y |

| Freight | +18% y/y |

| Skills gap (EU) | ~12% |

| Green premium | 10–25% |

| Engineer training | €30k–€50k |

What is included in the product

Tailored Porter's Five Forces analysis for Volker Wessels Stevin NV that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic recommendations to protect market share and profitability.

A concise, one-sheet Porter's Five Forces summary for Volker Wessels Stevin NV—ideal for swift strategic decisions and boardroom briefs.

Customers Bargaining Power

Public sector dominance

Government bodies and provincial authorities account for roughly 40–60% of Dutch infrastructure spend, so public contracts drive VolkerWessels Stevin NVs pipeline and pricing pressure.

Competitive tendering and requirements for social value and CO2 reductions force aggressive bids; public tenders trimmed contractor margins to single digits—VolkerWessels reported 2024 EBT margins near 3–4% for civil units.

Large-scale projects therefore often yield thin margins, higher working-capital demands, and increased bid frequency to secure backlog; winning share depends on cost control and compliance with strict environmental KPIs.

Increased demand for green building

Private developers and institutional investors prioritized ESG in 2025: 68% of European real estate funds required BREEAM/LEED in acquisitions, per MSCI Real Assets, giving buyers strong leverage.

Customers now demand high certifications; contractors failing to meet BREEAM Excellent or LEED Gold risk losing contracts worth up to 30% of project pipeline in urban Netherlands, per 2024 market reports.

This demand forces VolkerWessels Stevin NV to adopt low-carbon tech and circular materials, letting buyers effectively set the environmental and tech agenda for new developments.

Low switching costs

In residential and non-residential sectors, clients often pick among several large contractors with comparable capabilities, making switching easy and raising buyer power against VolkerWessels Stevin NV.

That pressure forces VolkerWessels to compete on service quality and on-time delivery; in 2024 the Dutch construction sector saw a 6% rise in tender price sensitivity, amplifying this need.

Price stays key—buyers can leverage rival bids during negotiations, and with gross margins around 6–8% industry-wide in 2024, small price moves materially affect competitiveness.

Price sensitivity in tender processes

Despite a shift to quality-based selection, the lowest-price-technically-acceptable model still governs many EU tenders, especially in infrastructure where 60% of public contracts in 2023 used price-weighted scoring (EU Commission data).

Clients exploit intense rivalry among top-tier firms to push down margins, with winning bids often 5–12% below average market estimates in 2024 rail and road tenders.

VolkerWessels must sustain extreme operational efficiency—tight cost control and productivity gains of 3–6% annually—to protect profitability during bidding.

- 60% of EU public tenders price-weighted (2023)

- Winning bids 5–12% below market estimates (2024)

- Required efficiency gains 3–6% annually

Consolidation of private clients

Large REITs and multinationals are pooling spend—Global listed REITs controlled ~1.2 trillion EUR AUM in 2024—so they press VolkerWessels Stevin for volume discounts and multi-year pricing.

Their procurement teams secure favorable payment and performance terms; repeat regional work (often 30–50% of project pipeline) gives these buyers strong leverage over contractors.

- REIT AUM ~1.2T EUR (2024)

- Repeat work often 30–50% of pipeline

- Volume pricing lowers contractor margins

- Multi-year contracts shift risk to suppliers

Public buyers & REITs squeeze margins—contractors need 3–6% annual productivity gains

Buyers (public bodies 40–60% of spend) wield high price and ESG leverage, forcing single-digit margins (VolkerWessels civil EBT ~3–4% in 2024) and frequent bids; 60% of EU tenders were price-weighted (2023). Large REITs (~1.2T EUR AUM, 2024) drive volume discounts and multi-year terms, shifting risk and lowering margins; contractors need 3–6% annual productivity gains to stay competitive.

| Metric | Value |

|---|---|

| Public spend share | 40–60% |

| Civil EBT (VolkerWessels, 2024) | 3–4% |

| EU price-weighted tenders (2023) | 60% |

| REIT AUM (2024) | ~1.2T EUR |

| Needed productivity gains | 3–6% p.a. |

Preview the Actual Deliverable

Volker Wessels Stevin NV Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Volker Wessels Stevin NV you'll receive immediately after purchase—no surprises, no placeholders.

It covers competitive rivalry, buyer and supplier power, threats of substitution and entry, and strategic implications—fully formatted and ready to use.

Once you buy, you’ll get instant access to this same complete, professionally written document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Volker Wessels Stevin NV faces moderate supplier power and high competitive rivalry in infrastructure and construction, with barriers to entry bolstered by scale and regulatory know‑how while buyer power and substitutes exert uneven pressure across segments. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Volker Wessels Stevin NV’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Raw material prices for steel, timber and cement stayed volatile into late 2025, with global steel billet prices up ~18% year-on-year and European cement spot up ~12% amid higher energy costs and supply bottlenecks.

VolkerWessels Stevin NV must use long-term purchase agreements and price-indexation clauses—historically cutting margin swings by ~3–5 percentage points—to insulate project gross margins.

Large integrated producers of steel and cement therefore hold significant supplier leverage, able to pass through cost shocks and influence delivery timing for major infrastructure projects.

Scarcity of specialized labor

A persistent shortage of skilled technicians and engineers across Europe raises supplier power for VolkerWessels Stevin NV, with Eurostat reporting a 2024 EU construction skills gap of ~12% and national shortages up to 20% in the Netherlands. VolkerWessels must pay competitive wages—2024 Dutch construction technician median pay rose 6%—and invest in training programs (estimated €30k–€50k per engineer lifecycle) to secure talent for complex infrastructure projects. This tight labor market limits the company’s ability to cut execution costs and can add 3–5% to project margins through higher labor and subcontractor rates.

Energy transition requirements

Suppliers of certified green materials and zero-emission machinery gain strong leverage as EU and Dutch rules tighten through 2025; about 60% of construction firms report supplier concentration for low-carbon tech in 2024.

VolkerWessels Stevin NV’s carbon-neutral target raises dependence on a few vetted vendors, increasing single-supplier risk and switching costs.

Those niche suppliers can charge premiums—reported 10–25% higher prices for certified equipment in 2023–24—compressing margins unless VolkerWessels secures long-term contracts or vertical partnerships.

Subcontractor dependence

VolkerWessels’ decentralized model depends on local subcontractors for specialist work and regional know-how, creating supplier power where demand is high; in 2024 Dutch construction activity rose ~6%, boosting subcontractor leverage.

In busy regions subcontractors often pick among projects, letting them set prices and schedules; delays or price hikes risk project margins and timelines.

Maintaining long-term partnerships and multi-year frameworks (common in 2023–24 contracts) is critical to secure continuity and quality.

- Decentralized reliance raises supplier leverage

- 2024 NL construction +6% increases subcontractor options

- Subcontractors can dictate price/schedule in hot markets

- Multi-year contracts and strong relationships reduce risk

Logistics and supply chain disruptions

Suppliers with integrated distribution reduced lead times by ~25% in 2024, creating bargaining power; VolkerWessels must diversify suppliers and use regional spare‑parts hubs to avoid single‑source hostage risk.

- 2024 freight cost +18%

- Integrated distributors cut lead times ~25%

- Diversify suppliers; add regional hubs

Supplier squeeze: input costs surge, VolkerWessels shields margins with long-term contracts

Suppliers (steel, cement, green tech, skilled labor, logistics) hold high bargaining power—2024: steel +18% y/y, cement +12%, freight +18%, EU construction skills gap ~12%—forcing VolkerWessels Stevin NV to use long-term contracts, price indexation, training (€30k–€50k/engineer) and supplier diversification to protect margins (typical risk add 3–5%; green premiums 10–25%).

| Metric | 2024–25 |

|---|---|

| Steel | +18% y/y |

| Cement | +12% y/y |

| Freight | +18% y/y |

| Skills gap (EU) | ~12% |

| Green premium | 10–25% |

| Engineer training | €30k–€50k |

What is included in the product

Tailored Porter's Five Forces analysis for Volker Wessels Stevin NV that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic recommendations to protect market share and profitability.

A concise, one-sheet Porter's Five Forces summary for Volker Wessels Stevin NV—ideal for swift strategic decisions and boardroom briefs.

Customers Bargaining Power

Public sector dominance

Government bodies and provincial authorities account for roughly 40–60% of Dutch infrastructure spend, so public contracts drive VolkerWessels Stevin NVs pipeline and pricing pressure.

Competitive tendering and requirements for social value and CO2 reductions force aggressive bids; public tenders trimmed contractor margins to single digits—VolkerWessels reported 2024 EBT margins near 3–4% for civil units.

Large-scale projects therefore often yield thin margins, higher working-capital demands, and increased bid frequency to secure backlog; winning share depends on cost control and compliance with strict environmental KPIs.

Increased demand for green building

Private developers and institutional investors prioritized ESG in 2025: 68% of European real estate funds required BREEAM/LEED in acquisitions, per MSCI Real Assets, giving buyers strong leverage.

Customers now demand high certifications; contractors failing to meet BREEAM Excellent or LEED Gold risk losing contracts worth up to 30% of project pipeline in urban Netherlands, per 2024 market reports.

This demand forces VolkerWessels Stevin NV to adopt low-carbon tech and circular materials, letting buyers effectively set the environmental and tech agenda for new developments.

Low switching costs

In residential and non-residential sectors, clients often pick among several large contractors with comparable capabilities, making switching easy and raising buyer power against VolkerWessels Stevin NV.

That pressure forces VolkerWessels to compete on service quality and on-time delivery; in 2024 the Dutch construction sector saw a 6% rise in tender price sensitivity, amplifying this need.

Price stays key—buyers can leverage rival bids during negotiations, and with gross margins around 6–8% industry-wide in 2024, small price moves materially affect competitiveness.

Price sensitivity in tender processes

Despite a shift to quality-based selection, the lowest-price-technically-acceptable model still governs many EU tenders, especially in infrastructure where 60% of public contracts in 2023 used price-weighted scoring (EU Commission data).

Clients exploit intense rivalry among top-tier firms to push down margins, with winning bids often 5–12% below average market estimates in 2024 rail and road tenders.

VolkerWessels must sustain extreme operational efficiency—tight cost control and productivity gains of 3–6% annually—to protect profitability during bidding.

- 60% of EU public tenders price-weighted (2023)

- Winning bids 5–12% below market estimates (2024)

- Required efficiency gains 3–6% annually

Consolidation of private clients

Large REITs and multinationals are pooling spend—Global listed REITs controlled ~1.2 trillion EUR AUM in 2024—so they press VolkerWessels Stevin for volume discounts and multi-year pricing.

Their procurement teams secure favorable payment and performance terms; repeat regional work (often 30–50% of project pipeline) gives these buyers strong leverage over contractors.

- REIT AUM ~1.2T EUR (2024)

- Repeat work often 30–50% of pipeline

- Volume pricing lowers contractor margins

- Multi-year contracts shift risk to suppliers

Public buyers & REITs squeeze margins—contractors need 3–6% annual productivity gains

Buyers (public bodies 40–60% of spend) wield high price and ESG leverage, forcing single-digit margins (VolkerWessels civil EBT ~3–4% in 2024) and frequent bids; 60% of EU tenders were price-weighted (2023). Large REITs (~1.2T EUR AUM, 2024) drive volume discounts and multi-year terms, shifting risk and lowering margins; contractors need 3–6% annual productivity gains to stay competitive.

| Metric | Value |

|---|---|

| Public spend share | 40–60% |

| Civil EBT (VolkerWessels, 2024) | 3–4% |

| EU price-weighted tenders (2023) | 60% |

| REIT AUM (2024) | ~1.2T EUR |

| Needed productivity gains | 3–6% p.a. |

Preview the Actual Deliverable

Volker Wessels Stevin NV Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Volker Wessels Stevin NV you'll receive immediately after purchase—no surprises, no placeholders.

It covers competitive rivalry, buyer and supplier power, threats of substitution and entry, and strategic implications—fully formatted and ready to use.

Once you buy, you’ll get instant access to this same complete, professionally written document.