Voltalia Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

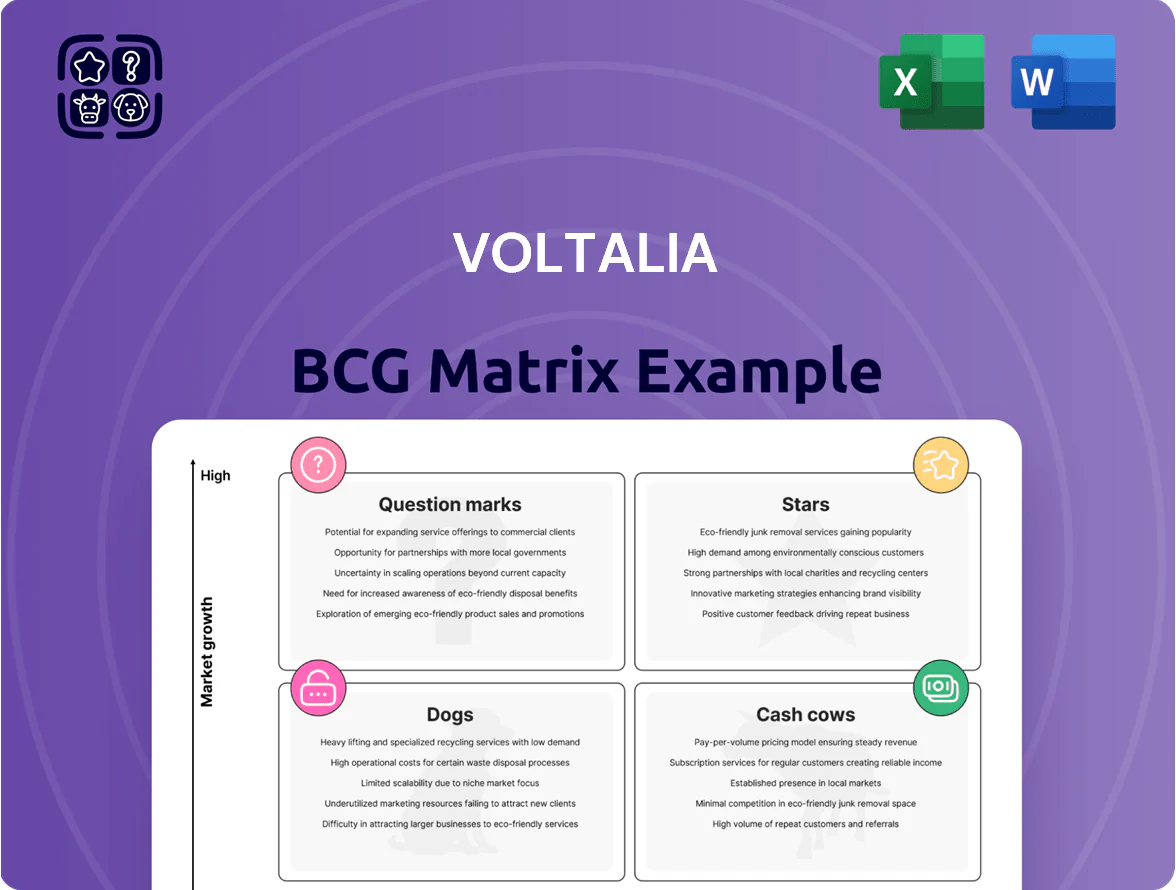

Voltalia’s BCG Matrix preview highlights how its renewable energy assets and service lines currently map to market growth and relative share—showing potential Stars in wind and solar, steady Cash Cows from long-term PPAs, and areas needing strategic focus. This snapshot teases data-driven positioning but leaves out quadrant-level metrics and actionable moves. Purchase the full BCG Matrix to receive a complete quadrant breakdown, strategic recommendations, and editable Word + Excel files to guide capital allocation and operational priorities with confidence.

Stars

European Solar Utility-Scale Projects

As of late 2025 Voltalia leads European utility-scale solar with ~1.4 GW operational and 3.2 GW in development, buoyed by REPowerEU-driven demand for energy independence and accelerated permitting.

These projects hold high market share in a European solar market growing ~12% CAGR (2023–2028) but need ongoing capex—estimated €150–220/MWh for grid upgrades and ~€200/kWh for battery storage additions.

The sector’s high growth keeps these assets the primary engine for Voltalia’s capacity increases, supporting projected group EBITDA growth of ~15% CAGR to 2028.

Energy Storage Systems (BESS)

The integration of large-scale battery energy storage systems (BESS) is a Star for Voltalia as grid volatility rises; global battery capacity additions hit ~120 GW in 2024 (IEA) and Voltalia scaled storage to ~600 MW of capacity by end-2024, capturing a top-10 share in European ancillary markets.

These projects drive high revenue growth—Voltalia reported storage-related revenue growth >70% YoY in 2024—but consume heavy upfront cash: capex per MWh ranges €350–€500, pressuring free cash flow while securing multi-year PPAs and grid services contracts.

Corporate PPA Solutions

Voltalia leads corporate PPA solutions, securing multi-year contracts with MNCs fighting to meet 2030 targets; in 2024 the segment grew ~48% y/y and represented about 28% of group backlog (€1.2bn of €4.3bn at end-2024).

Brazilian Wind Energy Expansion

Voltalia’s wind clusters in Brazil stay Stars: wind capacity factors exceed 55% in northeast sites and Voltalia owned ~1.2 GW there by Dec 2025, giving local dominance despite 2023–25 GDP volatility.

Brazil’s market growth is driven by rising industrial demand and a national green hydrogen roadmap targeting 2 GW electrolyzer capacity by 2030, keeping investment flows into wind to secure offtakes.

Voltalia keeps investing—capex of ~€220m in Brazil 2024–25—to protect share from Iberian and US entrants and to finance grid and storage tied to hybrid projects.

- ~1.2 GW Voltalia Brazil wind (Dec 2025)

- 55%+ capacity factors in NE sites

- €220m capex 2024–25 in Brazil

- Brazil target 2 GW green H2 electrolyzers by 2030

Hybrid Solar-Wind-Storage Plants

Hybrid Solar-Wind-Storage Plants are a Star in Voltalia’s BCG matrix: multi-technology sites deliver ~25–40% higher capacity factor than standalone solar, boosting reliability for grids and industry clients seeking firm renewable baseload.

Demand is strong—grid tenders for hybrid capacity rose 38% in 2024—and Voltalia, a first-mover, invested ~€120m in R&D and pilot projects in 2024 to keep its tech lead in this high-growth segment.

- Higher capacity factor: +25–40%

- Grid tenders up 38% in 2024

- Voltalia R&D/pilot spend ~€120m (2024)

Voltalia fuels 15% EBITDA CAGR with solar, Brazil wind, hybrids & rising storage revenues

Voltalia’s Stars: Europe solar (~1.4 GW op, 3.2 GW dev), Brazil wind (~1.2 GW, 55%+ CF), hybrids (+25–40% CF) and BESS (~600 MW end-2024) drive ~15% EBITDA CAGR to 2028 but need high capex (€150–€500/MWh; €220m Brazil 2024–25). Storage revenue +70% YoY (2024); corporate PPAs €1.2bn backlog (end-2024).

| Metric | Value |

|---|---|

| Solar op/dev | 1.4/3.2 GW |

| Wind Brazil | 1.2 GW |

| BESS | 600 MW |

| Capex range | €150–€500/MWh |

What is included in the product

In-depth BCG Matrix analysis of Voltalia’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Voltalia BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Established French Wind Farms

Voltalia’s established French wind farms sit in a low-growth, saturated market but deliver stable, high-margin cash flows—2019–2024 average EBITDA margin ~55% and ~€120m cumulative free cash flow (2021–2024) to the group. These assets largely run under long-term feed-in tariffs or fixed-price contracts, locking revenue and requiring minimal capex (annual maintenance ~€5–10m per park). Cash from France funds expansion: in 2024 Voltalia allocated ~€90m to Question Marks in Brazil and Africa.

Operations and Maintenance (O&M) Services

Voltalia’s third-party Operations and Maintenance (O&M) arm is a mature cash cow with ~600 MW under O&M and a top-quartile market share in Europe and Latin America as of 2025; the unit is known for technical excellence and >95% fleet availability.

The service business is low capital intensity versus asset ownership, produces recurring contracts that yielded ~€120m revenue and ~€40m EBITDA in 2024, and reliably funds debt service and corporate costs.

Small-Scale Hydroelectric Plants

Voltalia’s small-scale hydro fleet, concentrated in mature EU and Brazil markets, consists of long-life assets (30–80+ years) with limited new build due to strict environmental permits; total hydro capacity ~280 MW as of 2025, down from aggressive growth years.

After construction debt is amortized, operating costs drop below €10/MWh and gross margins exceed 60%, making these plants high-margin cash cows that fund growth.

They deliver stable EBITDA contribution—roughly 15–20% of group EBITDA in 2024—providing predictable liquidity despite volatility in wind and solar markets.

Mature Biomass Facilities

Voltalia’s mature biomass plants, notably the 7.5 MW Mana project in French Guiana (operational since 2016), now run at stable availability >92% with secured fuel contracts, delivering reliable baseload and predictable cash flow.

Growth for biomass is limited compared with Voltalia’s solar/wind pipeline (solar + wind projects >3.2 GW at end-2025), yet biomass yields steady EBITDA margins—typically 18–22%—and funds deployment into scalable renewables.

- Stable output: availability >92%

- Project size example: Mana 7.5 MW (operational 2016)

- EBITDA margins: ~18–22%

- Reinvestment: cash flows directed to solar/wind pipeline >3.2 GW (2025)

Project Development for Third Parties

The Project Development for Third Parties segment provides reliable upfront cash by selling ready-to-build projects; in 2024 Voltalia reported €123m in development sales, boosting liquidity without owning the assets.

In mature markets this leverages Voltalia’s development expertise while avoiding long-term capital tie-up, increasing ROIC and accelerating proprietary pipeline funding.

- 2024 development sales: €123m

- Improves short-term cash flow

- Reduces capital employed per project

- Funds proprietary pipeline growth

Voltalia’s cash cows: €120m FCF (2021–24), €90m capex funding >3.2GW pipeline

Voltalia’s cash cows (French wind, O&M, small hydro, biomass, third-party development) delivered ~€120m FCF 2021–24, ~15–20% group EBITDA in 2024, 2024 service revenue €120m/EBITDA €40m, hydro ~280 MW (2025), biomass margins 18–22% (Mana 7.5 MW). They fund ~€90m 2024 capex to Question Marks and pipeline >3.2 GW (end‑2025).

| Item | Metric |

|---|---|

| FCF 2021–24 | €120m |

| Group EBITDA 2024 | 15–20% |

| Service rev/EBITDA 2024 | €120m/€40m |

| Hydro capacity 2025 | ~280 MW |

| Pipeline end‑2025 | >3.2 GW |

Preview = Final Product

Voltalia BCG Matrix

The file you're previewing on this page is the final Voltalia BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report tailored for strategic clarity and professional use. This preview is identical to the downloadable file sent to your inbox, crafted with market-backed insights and ready for editing, printing, or presenting to stakeholders without any surprises. Purchase delivers the exact document shown here.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Voltalia’s BCG Matrix preview highlights how its renewable energy assets and service lines currently map to market growth and relative share—showing potential Stars in wind and solar, steady Cash Cows from long-term PPAs, and areas needing strategic focus. This snapshot teases data-driven positioning but leaves out quadrant-level metrics and actionable moves. Purchase the full BCG Matrix to receive a complete quadrant breakdown, strategic recommendations, and editable Word + Excel files to guide capital allocation and operational priorities with confidence.

Stars

European Solar Utility-Scale Projects

As of late 2025 Voltalia leads European utility-scale solar with ~1.4 GW operational and 3.2 GW in development, buoyed by REPowerEU-driven demand for energy independence and accelerated permitting.

These projects hold high market share in a European solar market growing ~12% CAGR (2023–2028) but need ongoing capex—estimated €150–220/MWh for grid upgrades and ~€200/kWh for battery storage additions.

The sector’s high growth keeps these assets the primary engine for Voltalia’s capacity increases, supporting projected group EBITDA growth of ~15% CAGR to 2028.

Energy Storage Systems (BESS)

The integration of large-scale battery energy storage systems (BESS) is a Star for Voltalia as grid volatility rises; global battery capacity additions hit ~120 GW in 2024 (IEA) and Voltalia scaled storage to ~600 MW of capacity by end-2024, capturing a top-10 share in European ancillary markets.

These projects drive high revenue growth—Voltalia reported storage-related revenue growth >70% YoY in 2024—but consume heavy upfront cash: capex per MWh ranges €350–€500, pressuring free cash flow while securing multi-year PPAs and grid services contracts.

Corporate PPA Solutions

Voltalia leads corporate PPA solutions, securing multi-year contracts with MNCs fighting to meet 2030 targets; in 2024 the segment grew ~48% y/y and represented about 28% of group backlog (€1.2bn of €4.3bn at end-2024).

Brazilian Wind Energy Expansion

Voltalia’s wind clusters in Brazil stay Stars: wind capacity factors exceed 55% in northeast sites and Voltalia owned ~1.2 GW there by Dec 2025, giving local dominance despite 2023–25 GDP volatility.

Brazil’s market growth is driven by rising industrial demand and a national green hydrogen roadmap targeting 2 GW electrolyzer capacity by 2030, keeping investment flows into wind to secure offtakes.

Voltalia keeps investing—capex of ~€220m in Brazil 2024–25—to protect share from Iberian and US entrants and to finance grid and storage tied to hybrid projects.

- ~1.2 GW Voltalia Brazil wind (Dec 2025)

- 55%+ capacity factors in NE sites

- €220m capex 2024–25 in Brazil

- Brazil target 2 GW green H2 electrolyzers by 2030

Hybrid Solar-Wind-Storage Plants

Hybrid Solar-Wind-Storage Plants are a Star in Voltalia’s BCG matrix: multi-technology sites deliver ~25–40% higher capacity factor than standalone solar, boosting reliability for grids and industry clients seeking firm renewable baseload.

Demand is strong—grid tenders for hybrid capacity rose 38% in 2024—and Voltalia, a first-mover, invested ~€120m in R&D and pilot projects in 2024 to keep its tech lead in this high-growth segment.

- Higher capacity factor: +25–40%

- Grid tenders up 38% in 2024

- Voltalia R&D/pilot spend ~€120m (2024)

Voltalia fuels 15% EBITDA CAGR with solar, Brazil wind, hybrids & rising storage revenues

Voltalia’s Stars: Europe solar (~1.4 GW op, 3.2 GW dev), Brazil wind (~1.2 GW, 55%+ CF), hybrids (+25–40% CF) and BESS (~600 MW end-2024) drive ~15% EBITDA CAGR to 2028 but need high capex (€150–€500/MWh; €220m Brazil 2024–25). Storage revenue +70% YoY (2024); corporate PPAs €1.2bn backlog (end-2024).

| Metric | Value |

|---|---|

| Solar op/dev | 1.4/3.2 GW |

| Wind Brazil | 1.2 GW |

| BESS | 600 MW |

| Capex range | €150–€500/MWh |

What is included in the product

In-depth BCG Matrix analysis of Voltalia’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Voltalia BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

Established French Wind Farms

Voltalia’s established French wind farms sit in a low-growth, saturated market but deliver stable, high-margin cash flows—2019–2024 average EBITDA margin ~55% and ~€120m cumulative free cash flow (2021–2024) to the group. These assets largely run under long-term feed-in tariffs or fixed-price contracts, locking revenue and requiring minimal capex (annual maintenance ~€5–10m per park). Cash from France funds expansion: in 2024 Voltalia allocated ~€90m to Question Marks in Brazil and Africa.

Operations and Maintenance (O&M) Services

Voltalia’s third-party Operations and Maintenance (O&M) arm is a mature cash cow with ~600 MW under O&M and a top-quartile market share in Europe and Latin America as of 2025; the unit is known for technical excellence and >95% fleet availability.

The service business is low capital intensity versus asset ownership, produces recurring contracts that yielded ~€120m revenue and ~€40m EBITDA in 2024, and reliably funds debt service and corporate costs.

Small-Scale Hydroelectric Plants

Voltalia’s small-scale hydro fleet, concentrated in mature EU and Brazil markets, consists of long-life assets (30–80+ years) with limited new build due to strict environmental permits; total hydro capacity ~280 MW as of 2025, down from aggressive growth years.

After construction debt is amortized, operating costs drop below €10/MWh and gross margins exceed 60%, making these plants high-margin cash cows that fund growth.

They deliver stable EBITDA contribution—roughly 15–20% of group EBITDA in 2024—providing predictable liquidity despite volatility in wind and solar markets.

Mature Biomass Facilities

Voltalia’s mature biomass plants, notably the 7.5 MW Mana project in French Guiana (operational since 2016), now run at stable availability >92% with secured fuel contracts, delivering reliable baseload and predictable cash flow.

Growth for biomass is limited compared with Voltalia’s solar/wind pipeline (solar + wind projects >3.2 GW at end-2025), yet biomass yields steady EBITDA margins—typically 18–22%—and funds deployment into scalable renewables.

- Stable output: availability >92%

- Project size example: Mana 7.5 MW (operational 2016)

- EBITDA margins: ~18–22%

- Reinvestment: cash flows directed to solar/wind pipeline >3.2 GW (2025)

Project Development for Third Parties

The Project Development for Third Parties segment provides reliable upfront cash by selling ready-to-build projects; in 2024 Voltalia reported €123m in development sales, boosting liquidity without owning the assets.

In mature markets this leverages Voltalia’s development expertise while avoiding long-term capital tie-up, increasing ROIC and accelerating proprietary pipeline funding.

- 2024 development sales: €123m

- Improves short-term cash flow

- Reduces capital employed per project

- Funds proprietary pipeline growth

Voltalia’s cash cows: €120m FCF (2021–24), €90m capex funding >3.2GW pipeline

Voltalia’s cash cows (French wind, O&M, small hydro, biomass, third-party development) delivered ~€120m FCF 2021–24, ~15–20% group EBITDA in 2024, 2024 service revenue €120m/EBITDA €40m, hydro ~280 MW (2025), biomass margins 18–22% (Mana 7.5 MW). They fund ~€90m 2024 capex to Question Marks and pipeline >3.2 GW (end‑2025).

| Item | Metric |

|---|---|

| FCF 2021–24 | €120m |

| Group EBITDA 2024 | 15–20% |

| Service rev/EBITDA 2024 | €120m/€40m |

| Hydro capacity 2025 | ~280 MW |

| Pipeline end‑2025 | >3.2 GW |

Preview = Final Product

Voltalia BCG Matrix

The file you're previewing on this page is the final Voltalia BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report tailored for strategic clarity and professional use. This preview is identical to the downloadable file sent to your inbox, crafted with market-backed insights and ready for editing, printing, or presenting to stakeholders without any surprises. Purchase delivers the exact document shown here.