Volution Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

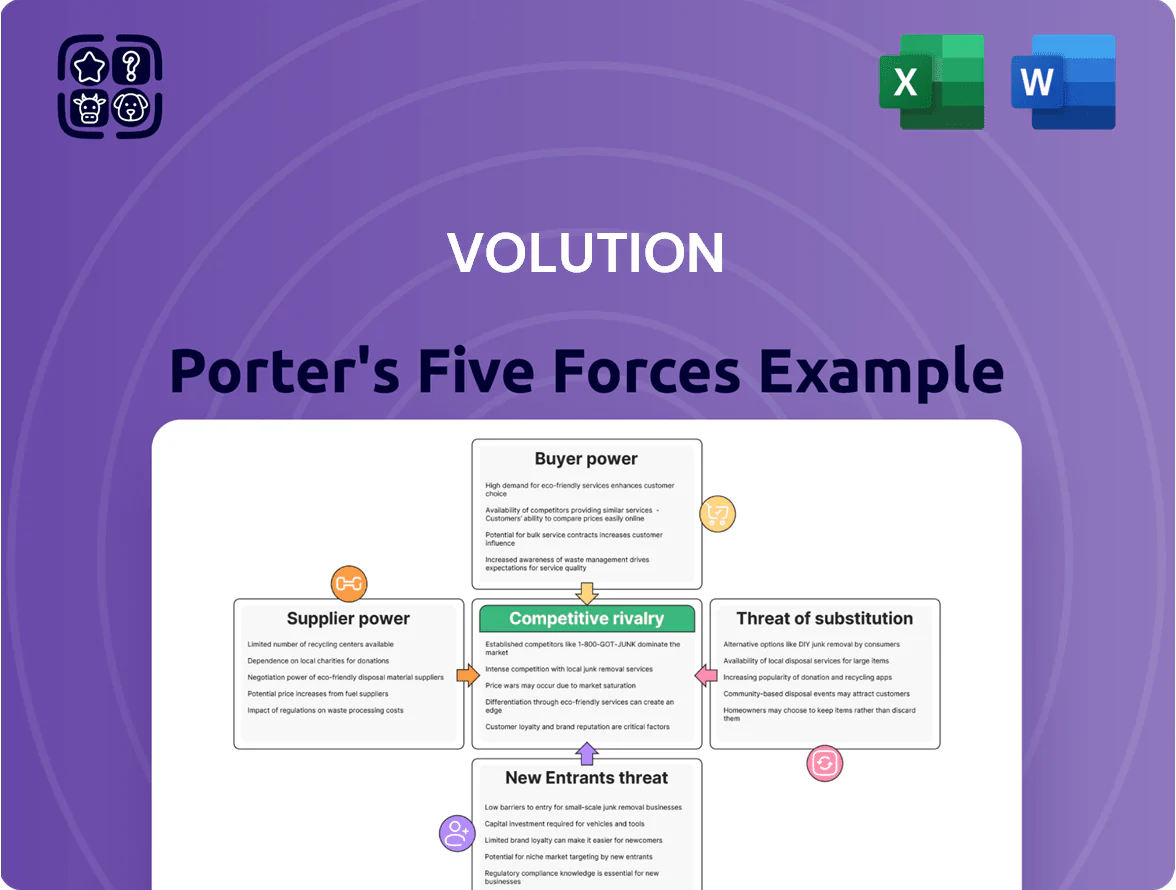

Volution faces moderate supplier power, fragmented buyers, and steady rivalry driven by HVAC consolidation and innovation—while new entrants and substitutes pose limited but rising threats due to energy-efficiency trends.

Suppliers Bargaining Power

Raw Material and Component Dependency

Volution Group depends on plastics, copper, and specialized electronic parts for motors and controls; in 2025 plastics prices rose ~8% YoY and copper was up ~15% YoY, so commodity volatility materially affects COGS.

Diversified sourcing across 4 regional suppliers and 3 contract manufacturers cuts localized risk, but global lead times average 14–20 weeks in 2025.

Suppliers of high-efficiency EC (electronically commutated) motors exert strong leverage since EC motors are mandatory for meeting EU Ecodesign and UK energy rules; EC motor components represent ~18% of BOM cost and limited qualified vendors keep bargaining power high.

Specialized Electronic Component Sourcing

Specialized semiconductor and electronic suppliers gain bargaining power as Volution adds sensors and smart controls; global chip shortages pushed lead times to 20+ weeks in 2021–22 and still tighten pricing, raising component costs by ~12% in 2023–24.

These suppliers serve auto, telecom, and consumer electronics, so Volution competes for allocations during demand spikes and peak seasons across sectors.

To secure continuity for high-margin smart fans, Volution signs multi-year supply contracts and committed-volume deals, reducing stockouts and stabilizing gross margins for smart ranges.

Geographic Supplier Concentration

Geographic supplier concentration: Volution sources key components from low-cost regions in Eastern Europe and Southeast Asia, meaning about 35% of component spend is regionally clustered (FY2024 supplier spend mix). This raises supplier power if alternatives are scarce or if trade disruptions occur—e.g., 2024 Suez/Red Sea disruptions spiked lead times by ~18%. The group dual-sources critical parts to balance cost and resilience, reducing single-source exposure to under 20% per SKU.

Sustainability and Compliance Standards

Suppliers offering recycled inputs or verified low‑carbon components are gaining leverage as EU and UK rules tighten; Green Claims Code and EU Carbon Border Adjustment Mechanism raise compliance costs—suppliers with documentation saw demand increase ~18% in 2024.

Volution’s ESG targets (net‑zero by 2040 commitment reported 2025) restrict eligible vendors, concentrating spend and letting certified suppliers charge 5–12% premiums for audit-ready supply chains.

- Demand for certified low‑carbon parts up ~18% (2024)

- Volution net‑zero by 2040 narrows vendor pool

- Certified suppliers capture 5–12% price premium

- Compliance documentation becomes non‑negotiable

Impact of Logistics and Freight Costs

The cost of shipping raw materials and finished components from international suppliers materially affects Volution Group plc’s gross margins; freight surcharges added roughly 1.2–1.8 percentage points to COGS in 2024, per carrier and customs data.

Global shipping consolidation after 2022 gave logistics providers pricing power, keeping spot rates 20–35% above pre-2020 averages through 2024, raising supplier bargaining leverage.

Volution reduces exposure by tightening inventory turns (12–14 turns/year in 2024), shifting to regional assembly in the UK and EU, and cutting average transport distance for bulky fans by ~30%, lowering freight spend.

- Freight added 1.2–1.8pp to COGS (2024)

- Spot rates 20–35% above pre-2020 (through 2024)

- Inventory turns 12–14/year (2024)

- Regional assembly cut transport distance ~30%

Suppliers Tighten Grip: Premiums, Commodities & Freight Lift COGS; Dual‑sourcing Cuts Risk

Suppliers hold moderate‑to‑high power: EC motors, semiconductors, and recycled inputs are scarce and command 5–18% premiums; commodity swings (plastics +8%, copper +15% in 2025) and freight (added 1.2–1.8pp COGS in 2024) raise costs; multi‑year contracts, dual‑sourcing and regional assembly cut single‑source exposure <20% and trimmed transport distance ~30%.

| Metric | 2024–25 |

|---|---|

| Plastics YoY | +8% |

| Copper YoY | +15% |

| Component premiums | 5–18% |

| Freight impact | +1.2–1.8pp COGS |

| Lead times | 14–20+ weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Volution that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies strategic levers and emerging disruptions to protect market share and profitability.

Quickly assess Volution’s competitive dynamics with a concise Porter's Five Forces snapshot—perfect for fast strategy calls or investor briefs.

Customers Bargaining Power

Concentration of Electrical Wholesalers

Price Sensitivity in Residential Construction

Influence of Professional Installers

Electrical contractors and ventilation installers are key decision-makers influencing final product choice, often prioritizing ease of installation and reliability over bulk pricing; installers drive an estimated 60–70% of homeowner brand selection in retrofit projects per 2024 UK trade surveys.

Volution reports spending ~£6m in 2024 on installer training and technical support, aiming to make its products the default recommendation through hands-on demos, CPD courses, and 24/7 spec support.

Growth of Direct-to-Consumer and Retail Channels

The rise of DIY home improvement and online retail gives consumers price and feature transparency, letting them compare standard domestic fans and switch to cheaper options; in the UK 2024 online home-improv sales grew ~9% year-on-year, intensifying price pressure on commodity fans.

Volution defends premium lines by highlighting verified gains—up to 30% lower energy use and 4 dB quieter operation in specific models—so buyers pay for clear value.

- Online DIY sales +9% UK 2024

- Switching raises price sensitivity

- Volution claims up to 30% energy savings

- Volution claims 4 dB noise reduction

Demand for Integrated Smart Home Solutions

Modern buyers expect ventilation to link with building management and smart-home platforms, shifting power to tech-savvy customers who pay premiums for interoperability; global smart HVAC market reached $24.5bn in 2024, up 8% YoY, showing buyer demand for connected systems.

Volution must offer connected solutions—APIs, Matter/KNX support, and remote diagnostics—to defend premium pricing; 35% of UK new-builds in 2024 specified smart ventilation, so failure to integrate risks margin erosion.

- Smart HVAC market $24.5bn (2024)

- 8% YoY growth (2024)

- 35% UK new-builds specify smart ventilation (2024)

- Interoperability (Matter/KNX), APIs, remote diagnostics required

Volution shields margins amid rising customer power—R&D, tiering & £6m installer support

| Metric | 2024/2025 |

|---|---|

| UK sales via wholesalers | 40% |

| Installers influence | 60–70% |

| New-builds need smart | 35% |

| Online DIY growth | +9% YoY |

| Installer support spend | £6m |

Preview the Actual Deliverable

Volution Porter's Five Forces Analysis

This preview shows the exact Volution Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're viewing the same professionally written document that will be available for instant download upon payment, containing comprehensive force assessments, supporting evidence, and strategic implications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Volution faces moderate supplier power, fragmented buyers, and steady rivalry driven by HVAC consolidation and innovation—while new entrants and substitutes pose limited but rising threats due to energy-efficiency trends.

Suppliers Bargaining Power

Raw Material and Component Dependency

Volution Group depends on plastics, copper, and specialized electronic parts for motors and controls; in 2025 plastics prices rose ~8% YoY and copper was up ~15% YoY, so commodity volatility materially affects COGS.

Diversified sourcing across 4 regional suppliers and 3 contract manufacturers cuts localized risk, but global lead times average 14–20 weeks in 2025.

Suppliers of high-efficiency EC (electronically commutated) motors exert strong leverage since EC motors are mandatory for meeting EU Ecodesign and UK energy rules; EC motor components represent ~18% of BOM cost and limited qualified vendors keep bargaining power high.

Specialized Electronic Component Sourcing

Specialized semiconductor and electronic suppliers gain bargaining power as Volution adds sensors and smart controls; global chip shortages pushed lead times to 20+ weeks in 2021–22 and still tighten pricing, raising component costs by ~12% in 2023–24.

These suppliers serve auto, telecom, and consumer electronics, so Volution competes for allocations during demand spikes and peak seasons across sectors.

To secure continuity for high-margin smart fans, Volution signs multi-year supply contracts and committed-volume deals, reducing stockouts and stabilizing gross margins for smart ranges.

Geographic Supplier Concentration

Geographic supplier concentration: Volution sources key components from low-cost regions in Eastern Europe and Southeast Asia, meaning about 35% of component spend is regionally clustered (FY2024 supplier spend mix). This raises supplier power if alternatives are scarce or if trade disruptions occur—e.g., 2024 Suez/Red Sea disruptions spiked lead times by ~18%. The group dual-sources critical parts to balance cost and resilience, reducing single-source exposure to under 20% per SKU.

Sustainability and Compliance Standards

Suppliers offering recycled inputs or verified low‑carbon components are gaining leverage as EU and UK rules tighten; Green Claims Code and EU Carbon Border Adjustment Mechanism raise compliance costs—suppliers with documentation saw demand increase ~18% in 2024.

Volution’s ESG targets (net‑zero by 2040 commitment reported 2025) restrict eligible vendors, concentrating spend and letting certified suppliers charge 5–12% premiums for audit-ready supply chains.

- Demand for certified low‑carbon parts up ~18% (2024)

- Volution net‑zero by 2040 narrows vendor pool

- Certified suppliers capture 5–12% price premium

- Compliance documentation becomes non‑negotiable

Impact of Logistics and Freight Costs

The cost of shipping raw materials and finished components from international suppliers materially affects Volution Group plc’s gross margins; freight surcharges added roughly 1.2–1.8 percentage points to COGS in 2024, per carrier and customs data.

Global shipping consolidation after 2022 gave logistics providers pricing power, keeping spot rates 20–35% above pre-2020 averages through 2024, raising supplier bargaining leverage.

Volution reduces exposure by tightening inventory turns (12–14 turns/year in 2024), shifting to regional assembly in the UK and EU, and cutting average transport distance for bulky fans by ~30%, lowering freight spend.

- Freight added 1.2–1.8pp to COGS (2024)

- Spot rates 20–35% above pre-2020 (through 2024)

- Inventory turns 12–14/year (2024)

- Regional assembly cut transport distance ~30%

Suppliers Tighten Grip: Premiums, Commodities & Freight Lift COGS; Dual‑sourcing Cuts Risk

Suppliers hold moderate‑to‑high power: EC motors, semiconductors, and recycled inputs are scarce and command 5–18% premiums; commodity swings (plastics +8%, copper +15% in 2025) and freight (added 1.2–1.8pp COGS in 2024) raise costs; multi‑year contracts, dual‑sourcing and regional assembly cut single‑source exposure <20% and trimmed transport distance ~30%.

| Metric | 2024–25 |

|---|---|

| Plastics YoY | +8% |

| Copper YoY | +15% |

| Component premiums | 5–18% |

| Freight impact | +1.2–1.8pp COGS |

| Lead times | 14–20+ weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Volution that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies strategic levers and emerging disruptions to protect market share and profitability.

Quickly assess Volution’s competitive dynamics with a concise Porter's Five Forces snapshot—perfect for fast strategy calls or investor briefs.

Customers Bargaining Power

Concentration of Electrical Wholesalers

Price Sensitivity in Residential Construction

Influence of Professional Installers

Electrical contractors and ventilation installers are key decision-makers influencing final product choice, often prioritizing ease of installation and reliability over bulk pricing; installers drive an estimated 60–70% of homeowner brand selection in retrofit projects per 2024 UK trade surveys.

Volution reports spending ~£6m in 2024 on installer training and technical support, aiming to make its products the default recommendation through hands-on demos, CPD courses, and 24/7 spec support.

Growth of Direct-to-Consumer and Retail Channels

The rise of DIY home improvement and online retail gives consumers price and feature transparency, letting them compare standard domestic fans and switch to cheaper options; in the UK 2024 online home-improv sales grew ~9% year-on-year, intensifying price pressure on commodity fans.

Volution defends premium lines by highlighting verified gains—up to 30% lower energy use and 4 dB quieter operation in specific models—so buyers pay for clear value.

- Online DIY sales +9% UK 2024

- Switching raises price sensitivity

- Volution claims up to 30% energy savings

- Volution claims 4 dB noise reduction

Demand for Integrated Smart Home Solutions

Modern buyers expect ventilation to link with building management and smart-home platforms, shifting power to tech-savvy customers who pay premiums for interoperability; global smart HVAC market reached $24.5bn in 2024, up 8% YoY, showing buyer demand for connected systems.

Volution must offer connected solutions—APIs, Matter/KNX support, and remote diagnostics—to defend premium pricing; 35% of UK new-builds in 2024 specified smart ventilation, so failure to integrate risks margin erosion.

- Smart HVAC market $24.5bn (2024)

- 8% YoY growth (2024)

- 35% UK new-builds specify smart ventilation (2024)

- Interoperability (Matter/KNX), APIs, remote diagnostics required

Volution shields margins amid rising customer power—R&D, tiering & £6m installer support

| Metric | 2024/2025 |

|---|---|

| UK sales via wholesalers | 40% |

| Installers influence | 60–70% |

| New-builds need smart | 35% |

| Online DIY growth | +9% YoY |

| Installer support spend | £6m |

Preview the Actual Deliverable

Volution Porter's Five Forces Analysis

This preview shows the exact Volution Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're viewing the same professionally written document that will be available for instant download upon payment, containing comprehensive force assessments, supporting evidence, and strategic implications.