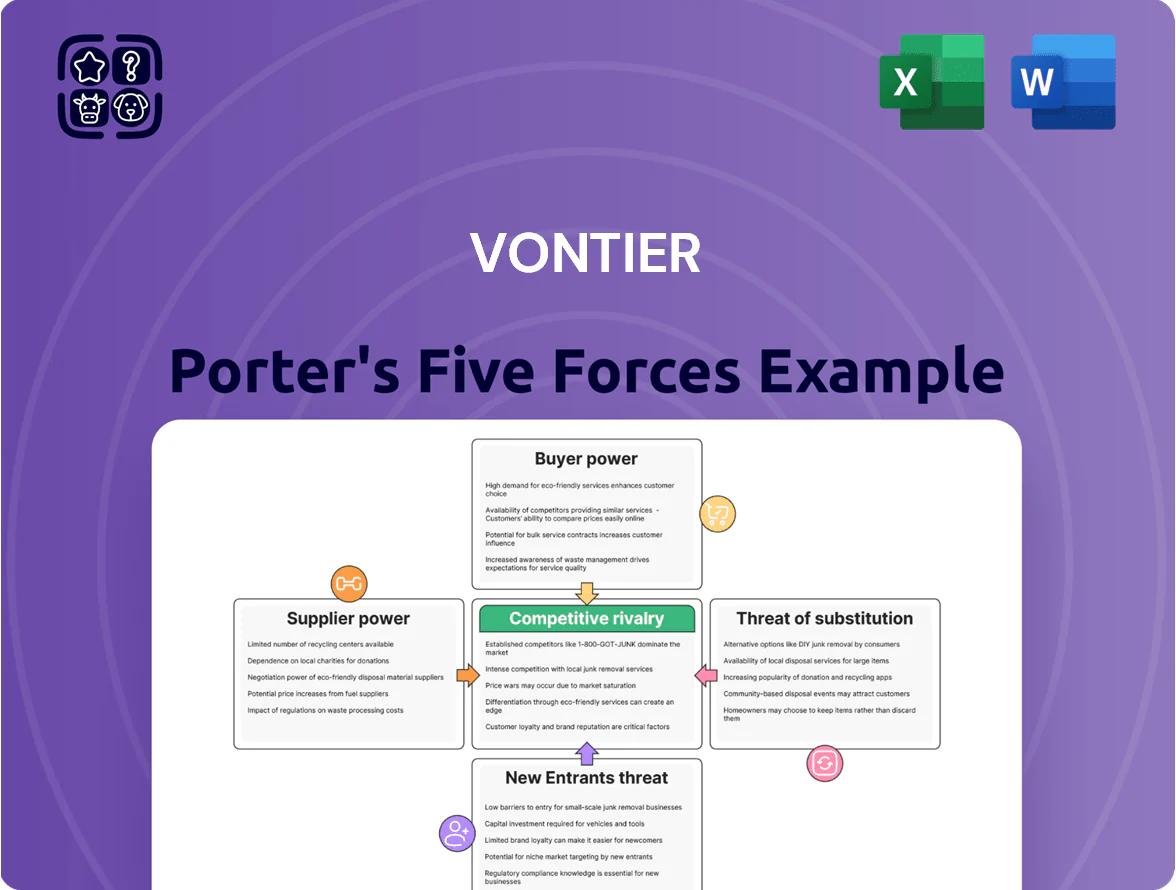

Vontier Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Vontier operates in a capital-intensive, innovation-driven market where supplier bargaining, buyer concentration, and regulatory shifts materially shape margins and growth prospects.

Our brief highlights core pressures—competitive rivalry, substitution risks, and entry barriers—but a granular force-by-force assessment reveals strategic levers and hidden vulnerabilities.

This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vontier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor and Electronic Component Access

Vontier depends on advanced microchips and sensors for smart fueling and telematics; by late 2025 the global chip backlog eased but 5–10nm high-performance processors remain concentrated among a few suppliers, giving them pricing and delivery leverage. To hedge production risk Vontier kept inventory covering roughly 12–16 weeks of demand in FY2025 and signed multi-year contracts covering ~40% of critical components, reducing potential downtime.

Raw Material Price Volatility for Industrial Manufacturing

Suppliers of steel, aluminum, and engineering plastics hold moderate-to-high bargaining power for Vontier’s Gilbarco Veeder-Root and Matco Tools lines, as these inputs made up ~24% of COGS in FY2024 and saw LME steel plate up 18% and aluminum 12% in H2 2025 amid trade tensions.

Vontier uses hedges and long-term contracts to cap exposure, but a 15–25% sudden raw-material spike in late 2025 could compress manufacturing gross margins by ~2–4 percentage points.

Dependency on Niche Software and Cloud Service Providers

Vontier’s SaaS push raises supplier power as cloud giants AWS and Microsoft Azure control infrastructure; AWS and Azure together held ~64% of global cloud IaaS/PaaS market in 2024, so switching costs and technical risk are high.

These providers can influence pricing and uptime, directly affecting Vontier’s remote asset management margins and SLAs; a 1–2% increase in cloud spend could cut adjusted EBIT margins by several hundred basis points on software revenue.

Limited Availability of Skilled Technical Talent

The specialized nature of Vontier's industrial tech demands elite R&D and manufacturing talent, and in 2025 specialized engineers and software developers command strong bargaining power in a tight market.

That power raised wage pressure: US median pay for robotics/control engineers rose ~8% YoY in 2024–25 and Vontier reported R&D payroll growth of ~12% in FY2024, forcing higher hiring and retention spend to keep innovation pace.

- High supplier power: niche engineers/devs

- Wage inflation ~8% YoY (2024–25) for key roles

- Vontier R&D payroll +12% in FY2024

- Higher recruitment/retention spend required

Concentration of Component Suppliers for EV Infrastructure

Vontier faces supplier concentration in battery management ICs and high-voltage components, where top suppliers (eg. Infineon, NXP, Analog Devices) control ~60–70% of market share, letting them favor large OEMs over industrial tech firms.

That leverage raises lead times and price volatility; securing multi-sourced contracts and long‑term purchase agreements is critical for meeting projected EV infrastructure demand (global charger installations forecast +40% in 2025 vs 2024).

- Top suppliers hold ~60–70% share

- Lead times can extend 20–30 weeks

- Long-term contracts reduce supply risk

- Charger installations up ~40% in 2025

Supplier concentration, input shocks and wage inflation squeeze margins

Suppliers exert moderate-to-high power: chip and HV component concentration (top vendors 60–70% share) and cloud providers (AWS+Azure ~64% IaaS/PaaS 2024) raise costs and lead times; raw-material spikes (steel +18%, aluminum +12% H2 2025) could cut manufacturing margins ~2–4 pts; wage inflation for key engineers ~8% YoY and Vontier R&D payroll +12% FY2024.

| Metric | Value |

|---|---|

| Chip/HV supplier share | 60–70% |

| AWS+Azure IaaS/PaaS | ~64% (2024) |

| Steel/Alum price change H2 2025 | +18% / +12% |

| Engineer wage change | ~+8% YoY |

| Vontier R&D payroll | +12% FY2024 |

What is included in the product

Tailored for Vontier, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and identifies disruptive forces and entry barriers shaping Vontier’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces snapshot for Vontier—quickly pinpoint competitive pressures and relief strategies to streamline strategic decisions.

Customers Bargaining Power

Consolidation of Major Retail Fueling Chains

Large convenience chains and global fuel retailers account for roughly 60% of Vontier’s 2024 revenue, so consolidation into fewer buyers increases customer bargaining power and pressurizes pricing.

As chains merge, they demand deeper volume discounts and stricter SLAs; a 10–15% price concession can follow multi-site contracts, cutting supplier margins.

Vontier must prove superior ROI—examples: 8–12% fuel-loss reduction and 20% lower maintenance costs over 3 years—to retain pricing power against these massive buyers.

Price Sensitivity of Independent Automotive Repair Shops

Matco Tools serves ~25,000 independent technicians and small shops that research price and financing; surveys show 62% cite price as primary purchase driver and 48% switch brands after one poor service experience.

These buyers face low switching costs and broad access to competitors (Snap-on, Mac Tools, Tekton), raising customer bargaining power and compressing margins.

Vontier offsets that by expanding its franchise model and a high-touch service network—Matco reports 6% same-store sales growth in 2024—aiming to lock in loyalty beyond price.

Low Switching Costs for Telematics and Fleet Software

The telematics and fleet software market is crowded—over 500 global vendors by 2024—so customers face low switching costs and can migrate quickly to cheaper platforms.

In 2025 fleet operators favor open-architecture solutions to integrate mixed hardware and SaaS, increasing pressure on proprietary lock-in models.

Vontier must make Teletrac Navman deliver unique, indispensable data insights—like predictive maintenance ROI lifts of 10–20%—to deter migration to lower-cost rivals.

Demand for Multi-Energy Dispensing Solutions

Modern customers now demand integrated stations offering gasoline, EV charging, and hydrogen, shifting bargaining power toward buyers who can require multi-modal, costly systems.

This raises switching costs and gives large fleets and global retailers leverage to favor suppliers like Vontier that act as one-stop shops for hardware, software, and maintenance.

Vontier’s 2025 revenue of $3.3B and service footprint across 70+ countries strengthen retention of sophisticated clients.

- Buyers push for multi-energy solutions

- Higher development & maintenance costs

- One-stop capability reduces churn

- Vontier: $3.3B revenue, 70+ countries

Influence of Government and Municipal Fleet Requirements

Public sector and municipal fleets use strict competitive bids that favor lowest cost and set environmental specs; Vontier must meet procurement rules to win these often multi-year contracts worth tens of millions—U.S. federal/state fleet spending exceeded $20B in 2024, raising stakes.

These buyers wield strong bargaining power: contracts give stable revenue but compress margins, and Vontier must comply with emissions rules and sustainability mandates (e.g., CA ZEV targets) to stay preferred.

- Large, multi-year contracts: stable revenue, thin margins

- 2024 U.S. public fleet spend ≈ $20B

- Bids prioritize low cost + environmental specs

- Regulatory compliance (ZEV, emissions) is mandatory

Buyer Power Compresses Margins: Vontier Scale vs. Price-Sensitive Fleets & 500+ Telematics Vendors

Buyers are highly powerful: top convenience chains and fuel retailers drove ~60% of Vontier’s 2024 revenue, forcing price concessions (10–15%) on multi-site deals; Matco’s ~25,000 independents show 62% price sensitivity; telematics market had 500+ vendors in 2024; public fleet procurement (~$20B U.S. 2024) favors low-cost bids—Vontier’s $3.3B 2025 scale and 70+ country footprint partly offsets this pressure.

| Metric | Value |

|---|---|

| 2024 revenue conc. from large buyers | ~60% |

| Price concession on multi-site deals | 10–15% |

| Matco buyers price-sensitive | 62% |

| Telematics vendors (2024) | 500+ |

| U.S. public fleet spend (2024) | ≈$20B |

| Vontier revenue (2025) | $3.3B; 70+ countries |

Same Document Delivered

Vontier Porter's Five Forces Analysis

This preview shows the exact Vontier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final, professionally written document; once you buy, you'll get instant access to this same file for download and implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Vontier operates in a capital-intensive, innovation-driven market where supplier bargaining, buyer concentration, and regulatory shifts materially shape margins and growth prospects.

Our brief highlights core pressures—competitive rivalry, substitution risks, and entry barriers—but a granular force-by-force assessment reveals strategic levers and hidden vulnerabilities.

This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vontier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor and Electronic Component Access

Vontier depends on advanced microchips and sensors for smart fueling and telematics; by late 2025 the global chip backlog eased but 5–10nm high-performance processors remain concentrated among a few suppliers, giving them pricing and delivery leverage. To hedge production risk Vontier kept inventory covering roughly 12–16 weeks of demand in FY2025 and signed multi-year contracts covering ~40% of critical components, reducing potential downtime.

Raw Material Price Volatility for Industrial Manufacturing

Suppliers of steel, aluminum, and engineering plastics hold moderate-to-high bargaining power for Vontier’s Gilbarco Veeder-Root and Matco Tools lines, as these inputs made up ~24% of COGS in FY2024 and saw LME steel plate up 18% and aluminum 12% in H2 2025 amid trade tensions.

Vontier uses hedges and long-term contracts to cap exposure, but a 15–25% sudden raw-material spike in late 2025 could compress manufacturing gross margins by ~2–4 percentage points.

Dependency on Niche Software and Cloud Service Providers

Vontier’s SaaS push raises supplier power as cloud giants AWS and Microsoft Azure control infrastructure; AWS and Azure together held ~64% of global cloud IaaS/PaaS market in 2024, so switching costs and technical risk are high.

These providers can influence pricing and uptime, directly affecting Vontier’s remote asset management margins and SLAs; a 1–2% increase in cloud spend could cut adjusted EBIT margins by several hundred basis points on software revenue.

Limited Availability of Skilled Technical Talent

The specialized nature of Vontier's industrial tech demands elite R&D and manufacturing talent, and in 2025 specialized engineers and software developers command strong bargaining power in a tight market.

That power raised wage pressure: US median pay for robotics/control engineers rose ~8% YoY in 2024–25 and Vontier reported R&D payroll growth of ~12% in FY2024, forcing higher hiring and retention spend to keep innovation pace.

- High supplier power: niche engineers/devs

- Wage inflation ~8% YoY (2024–25) for key roles

- Vontier R&D payroll +12% in FY2024

- Higher recruitment/retention spend required

Concentration of Component Suppliers for EV Infrastructure

Vontier faces supplier concentration in battery management ICs and high-voltage components, where top suppliers (eg. Infineon, NXP, Analog Devices) control ~60–70% of market share, letting them favor large OEMs over industrial tech firms.

That leverage raises lead times and price volatility; securing multi-sourced contracts and long‑term purchase agreements is critical for meeting projected EV infrastructure demand (global charger installations forecast +40% in 2025 vs 2024).

- Top suppliers hold ~60–70% share

- Lead times can extend 20–30 weeks

- Long-term contracts reduce supply risk

- Charger installations up ~40% in 2025

Supplier concentration, input shocks and wage inflation squeeze margins

Suppliers exert moderate-to-high power: chip and HV component concentration (top vendors 60–70% share) and cloud providers (AWS+Azure ~64% IaaS/PaaS 2024) raise costs and lead times; raw-material spikes (steel +18%, aluminum +12% H2 2025) could cut manufacturing margins ~2–4 pts; wage inflation for key engineers ~8% YoY and Vontier R&D payroll +12% FY2024.

| Metric | Value |

|---|---|

| Chip/HV supplier share | 60–70% |

| AWS+Azure IaaS/PaaS | ~64% (2024) |

| Steel/Alum price change H2 2025 | +18% / +12% |

| Engineer wage change | ~+8% YoY |

| Vontier R&D payroll | +12% FY2024 |

What is included in the product

Tailored for Vontier, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and identifies disruptive forces and entry barriers shaping Vontier’s pricing, profitability, and strategic positioning.

Concise Porter's Five Forces snapshot for Vontier—quickly pinpoint competitive pressures and relief strategies to streamline strategic decisions.

Customers Bargaining Power

Consolidation of Major Retail Fueling Chains

Large convenience chains and global fuel retailers account for roughly 60% of Vontier’s 2024 revenue, so consolidation into fewer buyers increases customer bargaining power and pressurizes pricing.

As chains merge, they demand deeper volume discounts and stricter SLAs; a 10–15% price concession can follow multi-site contracts, cutting supplier margins.

Vontier must prove superior ROI—examples: 8–12% fuel-loss reduction and 20% lower maintenance costs over 3 years—to retain pricing power against these massive buyers.

Price Sensitivity of Independent Automotive Repair Shops

Matco Tools serves ~25,000 independent technicians and small shops that research price and financing; surveys show 62% cite price as primary purchase driver and 48% switch brands after one poor service experience.

These buyers face low switching costs and broad access to competitors (Snap-on, Mac Tools, Tekton), raising customer bargaining power and compressing margins.

Vontier offsets that by expanding its franchise model and a high-touch service network—Matco reports 6% same-store sales growth in 2024—aiming to lock in loyalty beyond price.

Low Switching Costs for Telematics and Fleet Software

The telematics and fleet software market is crowded—over 500 global vendors by 2024—so customers face low switching costs and can migrate quickly to cheaper platforms.

In 2025 fleet operators favor open-architecture solutions to integrate mixed hardware and SaaS, increasing pressure on proprietary lock-in models.

Vontier must make Teletrac Navman deliver unique, indispensable data insights—like predictive maintenance ROI lifts of 10–20%—to deter migration to lower-cost rivals.

Demand for Multi-Energy Dispensing Solutions

Modern customers now demand integrated stations offering gasoline, EV charging, and hydrogen, shifting bargaining power toward buyers who can require multi-modal, costly systems.

This raises switching costs and gives large fleets and global retailers leverage to favor suppliers like Vontier that act as one-stop shops for hardware, software, and maintenance.

Vontier’s 2025 revenue of $3.3B and service footprint across 70+ countries strengthen retention of sophisticated clients.

- Buyers push for multi-energy solutions

- Higher development & maintenance costs

- One-stop capability reduces churn

- Vontier: $3.3B revenue, 70+ countries

Influence of Government and Municipal Fleet Requirements

Public sector and municipal fleets use strict competitive bids that favor lowest cost and set environmental specs; Vontier must meet procurement rules to win these often multi-year contracts worth tens of millions—U.S. federal/state fleet spending exceeded $20B in 2024, raising stakes.

These buyers wield strong bargaining power: contracts give stable revenue but compress margins, and Vontier must comply with emissions rules and sustainability mandates (e.g., CA ZEV targets) to stay preferred.

- Large, multi-year contracts: stable revenue, thin margins

- 2024 U.S. public fleet spend ≈ $20B

- Bids prioritize low cost + environmental specs

- Regulatory compliance (ZEV, emissions) is mandatory

Buyer Power Compresses Margins: Vontier Scale vs. Price-Sensitive Fleets & 500+ Telematics Vendors

Buyers are highly powerful: top convenience chains and fuel retailers drove ~60% of Vontier’s 2024 revenue, forcing price concessions (10–15%) on multi-site deals; Matco’s ~25,000 independents show 62% price sensitivity; telematics market had 500+ vendors in 2024; public fleet procurement (~$20B U.S. 2024) favors low-cost bids—Vontier’s $3.3B 2025 scale and 70+ country footprint partly offsets this pressure.

| Metric | Value |

|---|---|

| 2024 revenue conc. from large buyers | ~60% |

| Price concession on multi-site deals | 10–15% |

| Matco buyers price-sensitive | 62% |

| Telematics vendors (2024) | 500+ |

| U.S. public fleet spend (2024) | ≈$20B |

| Vontier revenue (2025) | $3.3B; 70+ countries |

Same Document Delivered

Vontier Porter's Five Forces Analysis

This preview shows the exact Vontier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final, professionally written document; once you buy, you'll get instant access to this same file for download and implementation.