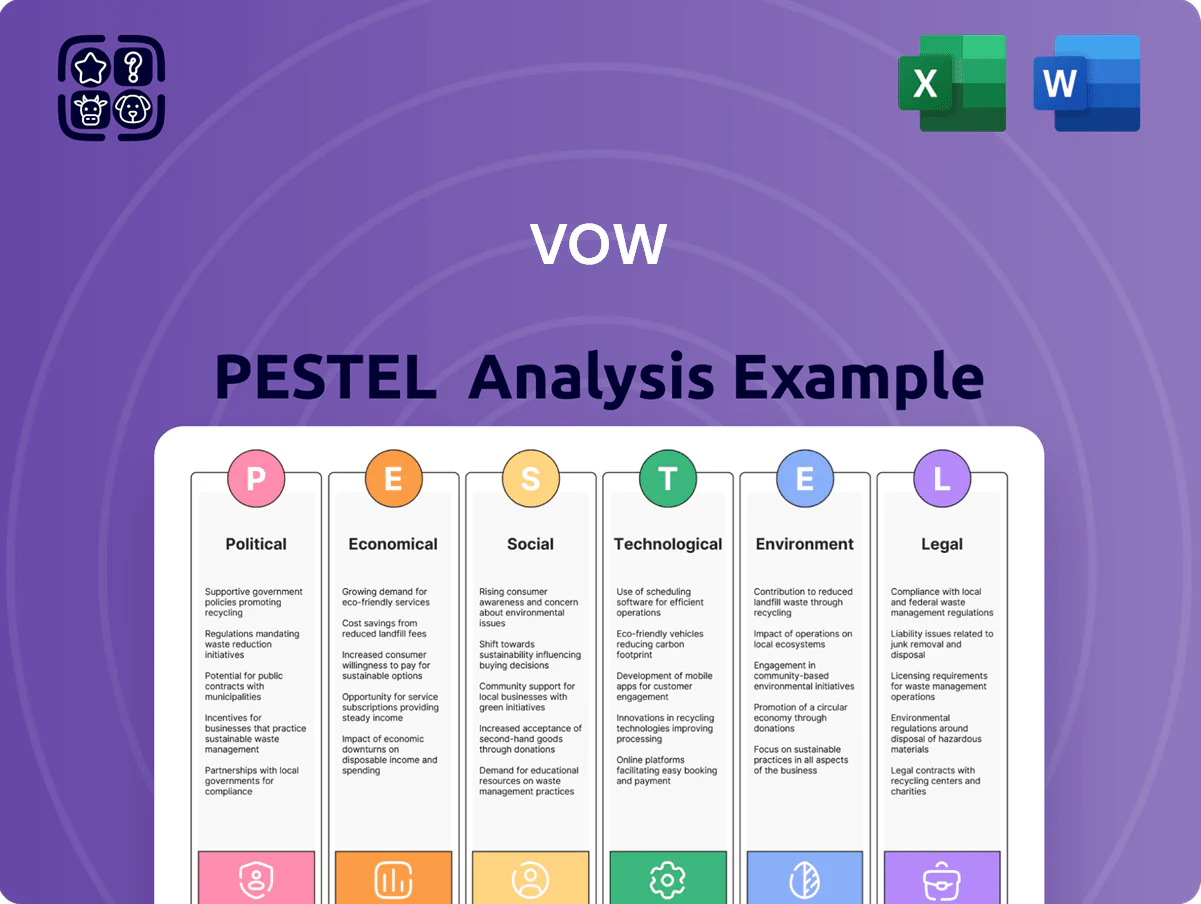

VoW PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic trends, social dynamics, and technological advances are reshaping VoW’s prospects in our concise PESTLE overview—designed to reveal risks and opportunities fast. Purchase the full PESTLE analysis to unlock in-depth insights, data-backed implications, and ready-to-use recommendations that power smarter investment and strategic decisions.

Political factors

Global decarbonization policies

Governmental commitments to net-zero by 2050—over 140 countries as of 2025—boost demand for Vow ASA waste-to-energy solutions, aligning with rising green infrastructure spending (global clean energy investment hit USD 1.1 trillion in 2023).

EU Green Deal and maritime focus

The EU Green Deal tightens maritime emissions and waste rules, with the Fit for 55 package and ETS for shipping pushing CO2 reductions; EU shipping ETS launched in 2024 covers ~50% of emissions from intra-EU voyages and imposes €/tonne pricing that rose to ~€80 in 2025, increasing demand for scrubbers and abatement tech.

Vow ASA benefits from EU grants and Norway/EU funding schemes, including Innovation Fund+/CEF co-financing that allocated €3.5bn for maritime decarbonization in 2024–25, improving project IRRs for shipowners adopting Vow systems.

Rising political pressure and IMO/EU alignment create effectively mandatory retrofit markets: 2025 estimates show >10,000 commercial vessels in scope, representing a potential TAM for Vow of €2–4bn over the next decade based on average retrofit costs of €200–400k per vessel.

Geopolitical energy security

Governments are prioritizing energy independence, with EU member states targeting a 55% reduction in net greenhouse gas emissions by 2030 and increased local energy solutions; waste-to-energy is gaining policy support. Vow ASA’s tech converts domestic waste to energy or biocarbon, potentially displacing imported fossil fuels and supporting Norway’s 2030 climate goals. The strategic fit places Vow in national security and energy resilience discussions given Europe’s 2024 gas import volatility.

Subsidy and grant landscapes

Political support often takes the form of grants and subsidies—EU green funds allocated €420bn for 2021–2027 green transition programs, and Norway’s ENOVA provided ~NOK 1.3bn in 2024 for industrial decarbonization—reducing upfront CAPEX for Vow ASA clients in land-based sectors.

Shifts in government can reallocate these funds, delaying projects and altering ROI timelines for Vow’s installations.

- EU/Norway funding reduces client CAPEX

- ENOVA ~NOK 1.3bn (2024)

- EU €420bn (2021–2027)

- Political shifts risk delays

Trade and export regulations

As a Norwegian global engineering firm, Vow ASA must comply with WTO rules and EU and US export controls; in 2024 Norway’s goods exports to the EU were NOK 1,040 billion and to the US NOK 167 billion, underscoring market exposure.

Stable Norway-EU and Norway-US relations facilitate technology transfer; disruptions risk delays for multi-year projects—Vow’s order backlog sensitivity rises with geopolitical risk.

Political stability in key markets ensures continuity of long-term engineering contracts and capital allocation for projects often spanning 3–7 years.

- Subject to WTO, EU, US export controls and sanctions

- 2024 exports: Norway–EU NOK 1,040bn; Norway–US NOK 167bn

- Project timelines (3–7 years) vulnerable to diplomatic disruptions

EU funds + €80/t ETS spur maritime retrofit boom amid 140+ net‑zero pledges

Strong net-zero commitments (140+ countries by 2025) and EU Fit for 55/ETS shipping (≈€80/t in 2025) drive retrofit demand; EU Clean Energy investment was USD 1.1tn (2023). EU/Norway funds (EU €420bn 2021–27; Innovation Fund+/CEF €3.5bn maritime 2024–25; ENOVA NOK 1.3bn 2024) lower CAPEX but political shifts risk delays; Norway 2024 exports: EU NOK 1,040bn, US NOK 167bn.

| Metric | Value |

|---|---|

| Countries net-zero | 140+ |

| EU ETS shipping price (2025) | ~€80/t |

| Clean energy investment (2023) | USD 1.1tn |

| EU green funds (2021–27) | €420bn |

| Maritime grants (2024–25) | €3.5bn |

| ENOVA 2024 | NOK 1.3bn |

| Norway exports 2024 | EU NOK 1,040bn; US NOK 167bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect the VoW across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting suitable for business plans, investor pitches, or internal strategy documents.

VoW PESTLE condenses complex external analysis into a crisp, shareable summary that teams can drop into presentations or use in planning sessions for rapid alignment and decision-making.

Economic factors

Cost of carbon and emissions trading

The EU ETS carbon price climbed to about €100/tCO2 in 2024, making Vow ASA waste-to-energy solutions economically attractive as clients face higher compliance costs.

Industrial clients can offset rising carbon taxes by converting waste streams into energy or fuels, capturing value and lowering net emissions exposure.

At €100/tCO2, payback estimates shift many Vow offerings from optional upgrades to essential cost-saving investments for heavy emitters.

Interest rates and capital access

As of late 2025, global policy rates average around 4.5–5.0%, raising borrowing costs for clients and slowing financing of large-scale environmental infrastructure projects, which can push Vow ASA order timelines out by 6–18 months. Higher rates have contributed to a 12% year-on-year decline in announced CAPEX in waste-to-energy and recycling sectors in 2024–25, constraining immediate demand. Conversely, a 1 percentage-point fall in rates historically correlates with a ~7% uptick in project starts, suggesting lower rates would accelerate adoption of Vow technology. Vow must actively manage its backlog and financing support to mitigate macro cycle impacts on order conversion.

Circular economy market growth

The global shift to a circular economy boosts Vow ASA revenue potential by monetizing recovered resources such as biocarbon, with the global circular economy market projected to reach USD 5.5 trillion by 2030 and secondary material markets growing ~6–8% annually (2024–2030). Demand for sustainable feedstocks lifted prices for carbon-neutral inputs; biocarbon premiums rose ~10–15% in 2024 versus 2022. This strengthens Vow’s client proposition as industries seek to convert waste into saleable materials, improving project IRRs and payback timelines.

Fluctuations in raw material costs

The profitability of Vow ASA is highly sensitive to steel, specialized component and energy costs; steel prices rose ~15% YoY in 2024 while European industrial electricity averages hit ~€0.18/kWh, pressuring margins in engineering segments.

Inflationary supply-chain pressures can erode margins if contracts lack indexation; in 2024 input-cost inflation for manufacturing sectors averaged ~6–8%, highlighting contract risk.

Active cost management—hedging steel, negotiating escalation clauses, improving energy efficiency—is essential to preserve EBITDA margins and project viability.

- Steel +15% YoY (2024)

- EU industrial power ~€0.18/kWh (2024)

- Input-cost inflation 6–8% (2024)

- Hedge, escalation clauses, energy efficiency

Maritime industry profitability

The cruise and shipping sectors' profits drive demand for Vow ASA systems; global cruise revenue fell 6% in 2023 but recovered in 2024 with industry capacity utilization reaching ~85%, while global container trade volumes rose 3.5% in 2024, supporting fleet investment and retrofit budgets.

Economic slowdowns see operators defer maintenance and cancel equipment orders—ship newbuilding orders dropped 18% in 2023, highlighting sensitivity to sector cashflows.

- 2024 cruise capacity utilization ~85%

- Global container trade +3.5% in 2024

- Ship newbuilding orders -18% in 2023

Higher EU ETS boosts Vow IRRs; rates and input inflation strain project execution

Higher EU ETS (~€100/tCO2 in 2024) and circular-economy demand improve Vow ASA project IRRs, while 2024–25 higher policy rates (4.5–5.0%) and input-cost inflation (steel +15%, electricity ~€0.18/kWh, input inflation 6–8%) delay order conversion; financing support and cost-hedging crucial to sustain margins.

| Metric | 2024–25 |

|---|---|

| EU ETS | ~€100/tCO2 |

| Policy rates | 4.5–5.0% |

| Steel | +15% YoY |

| Electricity | €0.18/kWh |

What You See Is What You Get

VoW PESTLE Analysis

The preview shown here is the exact VoW PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or teasers.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic trends, social dynamics, and technological advances are reshaping VoW’s prospects in our concise PESTLE overview—designed to reveal risks and opportunities fast. Purchase the full PESTLE analysis to unlock in-depth insights, data-backed implications, and ready-to-use recommendations that power smarter investment and strategic decisions.

Political factors

Global decarbonization policies

Governmental commitments to net-zero by 2050—over 140 countries as of 2025—boost demand for Vow ASA waste-to-energy solutions, aligning with rising green infrastructure spending (global clean energy investment hit USD 1.1 trillion in 2023).

EU Green Deal and maritime focus

The EU Green Deal tightens maritime emissions and waste rules, with the Fit for 55 package and ETS for shipping pushing CO2 reductions; EU shipping ETS launched in 2024 covers ~50% of emissions from intra-EU voyages and imposes €/tonne pricing that rose to ~€80 in 2025, increasing demand for scrubbers and abatement tech.

Vow ASA benefits from EU grants and Norway/EU funding schemes, including Innovation Fund+/CEF co-financing that allocated €3.5bn for maritime decarbonization in 2024–25, improving project IRRs for shipowners adopting Vow systems.

Rising political pressure and IMO/EU alignment create effectively mandatory retrofit markets: 2025 estimates show >10,000 commercial vessels in scope, representing a potential TAM for Vow of €2–4bn over the next decade based on average retrofit costs of €200–400k per vessel.

Geopolitical energy security

Governments are prioritizing energy independence, with EU member states targeting a 55% reduction in net greenhouse gas emissions by 2030 and increased local energy solutions; waste-to-energy is gaining policy support. Vow ASA’s tech converts domestic waste to energy or biocarbon, potentially displacing imported fossil fuels and supporting Norway’s 2030 climate goals. The strategic fit places Vow in national security and energy resilience discussions given Europe’s 2024 gas import volatility.

Subsidy and grant landscapes

Political support often takes the form of grants and subsidies—EU green funds allocated €420bn for 2021–2027 green transition programs, and Norway’s ENOVA provided ~NOK 1.3bn in 2024 for industrial decarbonization—reducing upfront CAPEX for Vow ASA clients in land-based sectors.

Shifts in government can reallocate these funds, delaying projects and altering ROI timelines for Vow’s installations.

- EU/Norway funding reduces client CAPEX

- ENOVA ~NOK 1.3bn (2024)

- EU €420bn (2021–2027)

- Political shifts risk delays

Trade and export regulations

As a Norwegian global engineering firm, Vow ASA must comply with WTO rules and EU and US export controls; in 2024 Norway’s goods exports to the EU were NOK 1,040 billion and to the US NOK 167 billion, underscoring market exposure.

Stable Norway-EU and Norway-US relations facilitate technology transfer; disruptions risk delays for multi-year projects—Vow’s order backlog sensitivity rises with geopolitical risk.

Political stability in key markets ensures continuity of long-term engineering contracts and capital allocation for projects often spanning 3–7 years.

- Subject to WTO, EU, US export controls and sanctions

- 2024 exports: Norway–EU NOK 1,040bn; Norway–US NOK 167bn

- Project timelines (3–7 years) vulnerable to diplomatic disruptions

EU funds + €80/t ETS spur maritime retrofit boom amid 140+ net‑zero pledges

Strong net-zero commitments (140+ countries by 2025) and EU Fit for 55/ETS shipping (≈€80/t in 2025) drive retrofit demand; EU Clean Energy investment was USD 1.1tn (2023). EU/Norway funds (EU €420bn 2021–27; Innovation Fund+/CEF €3.5bn maritime 2024–25; ENOVA NOK 1.3bn 2024) lower CAPEX but political shifts risk delays; Norway 2024 exports: EU NOK 1,040bn, US NOK 167bn.

| Metric | Value |

|---|---|

| Countries net-zero | 140+ |

| EU ETS shipping price (2025) | ~€80/t |

| Clean energy investment (2023) | USD 1.1tn |

| EU green funds (2021–27) | €420bn |

| Maritime grants (2024–25) | €3.5bn |

| ENOVA 2024 | NOK 1.3bn |

| Norway exports 2024 | EU NOK 1,040bn; US NOK 167bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect the VoW across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting suitable for business plans, investor pitches, or internal strategy documents.

VoW PESTLE condenses complex external analysis into a crisp, shareable summary that teams can drop into presentations or use in planning sessions for rapid alignment and decision-making.

Economic factors

Cost of carbon and emissions trading

The EU ETS carbon price climbed to about €100/tCO2 in 2024, making Vow ASA waste-to-energy solutions economically attractive as clients face higher compliance costs.

Industrial clients can offset rising carbon taxes by converting waste streams into energy or fuels, capturing value and lowering net emissions exposure.

At €100/tCO2, payback estimates shift many Vow offerings from optional upgrades to essential cost-saving investments for heavy emitters.

Interest rates and capital access

As of late 2025, global policy rates average around 4.5–5.0%, raising borrowing costs for clients and slowing financing of large-scale environmental infrastructure projects, which can push Vow ASA order timelines out by 6–18 months. Higher rates have contributed to a 12% year-on-year decline in announced CAPEX in waste-to-energy and recycling sectors in 2024–25, constraining immediate demand. Conversely, a 1 percentage-point fall in rates historically correlates with a ~7% uptick in project starts, suggesting lower rates would accelerate adoption of Vow technology. Vow must actively manage its backlog and financing support to mitigate macro cycle impacts on order conversion.

Circular economy market growth

The global shift to a circular economy boosts Vow ASA revenue potential by monetizing recovered resources such as biocarbon, with the global circular economy market projected to reach USD 5.5 trillion by 2030 and secondary material markets growing ~6–8% annually (2024–2030). Demand for sustainable feedstocks lifted prices for carbon-neutral inputs; biocarbon premiums rose ~10–15% in 2024 versus 2022. This strengthens Vow’s client proposition as industries seek to convert waste into saleable materials, improving project IRRs and payback timelines.

Fluctuations in raw material costs

The profitability of Vow ASA is highly sensitive to steel, specialized component and energy costs; steel prices rose ~15% YoY in 2024 while European industrial electricity averages hit ~€0.18/kWh, pressuring margins in engineering segments.

Inflationary supply-chain pressures can erode margins if contracts lack indexation; in 2024 input-cost inflation for manufacturing sectors averaged ~6–8%, highlighting contract risk.

Active cost management—hedging steel, negotiating escalation clauses, improving energy efficiency—is essential to preserve EBITDA margins and project viability.

- Steel +15% YoY (2024)

- EU industrial power ~€0.18/kWh (2024)

- Input-cost inflation 6–8% (2024)

- Hedge, escalation clauses, energy efficiency

Maritime industry profitability

The cruise and shipping sectors' profits drive demand for Vow ASA systems; global cruise revenue fell 6% in 2023 but recovered in 2024 with industry capacity utilization reaching ~85%, while global container trade volumes rose 3.5% in 2024, supporting fleet investment and retrofit budgets.

Economic slowdowns see operators defer maintenance and cancel equipment orders—ship newbuilding orders dropped 18% in 2023, highlighting sensitivity to sector cashflows.

- 2024 cruise capacity utilization ~85%

- Global container trade +3.5% in 2024

- Ship newbuilding orders -18% in 2023

Higher EU ETS boosts Vow IRRs; rates and input inflation strain project execution

Higher EU ETS (~€100/tCO2 in 2024) and circular-economy demand improve Vow ASA project IRRs, while 2024–25 higher policy rates (4.5–5.0%) and input-cost inflation (steel +15%, electricity ~€0.18/kWh, input inflation 6–8%) delay order conversion; financing support and cost-hedging crucial to sustain margins.

| Metric | 2024–25 |

|---|---|

| EU ETS | ~€100/tCO2 |

| Policy rates | 4.5–5.0% |

| Steel | +15% YoY |

| Electricity | €0.18/kWh |

What You See Is What You Get

VoW PESTLE Analysis

The preview shown here is the exact VoW PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or teasers.