Vertex Pharmaceuticals PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

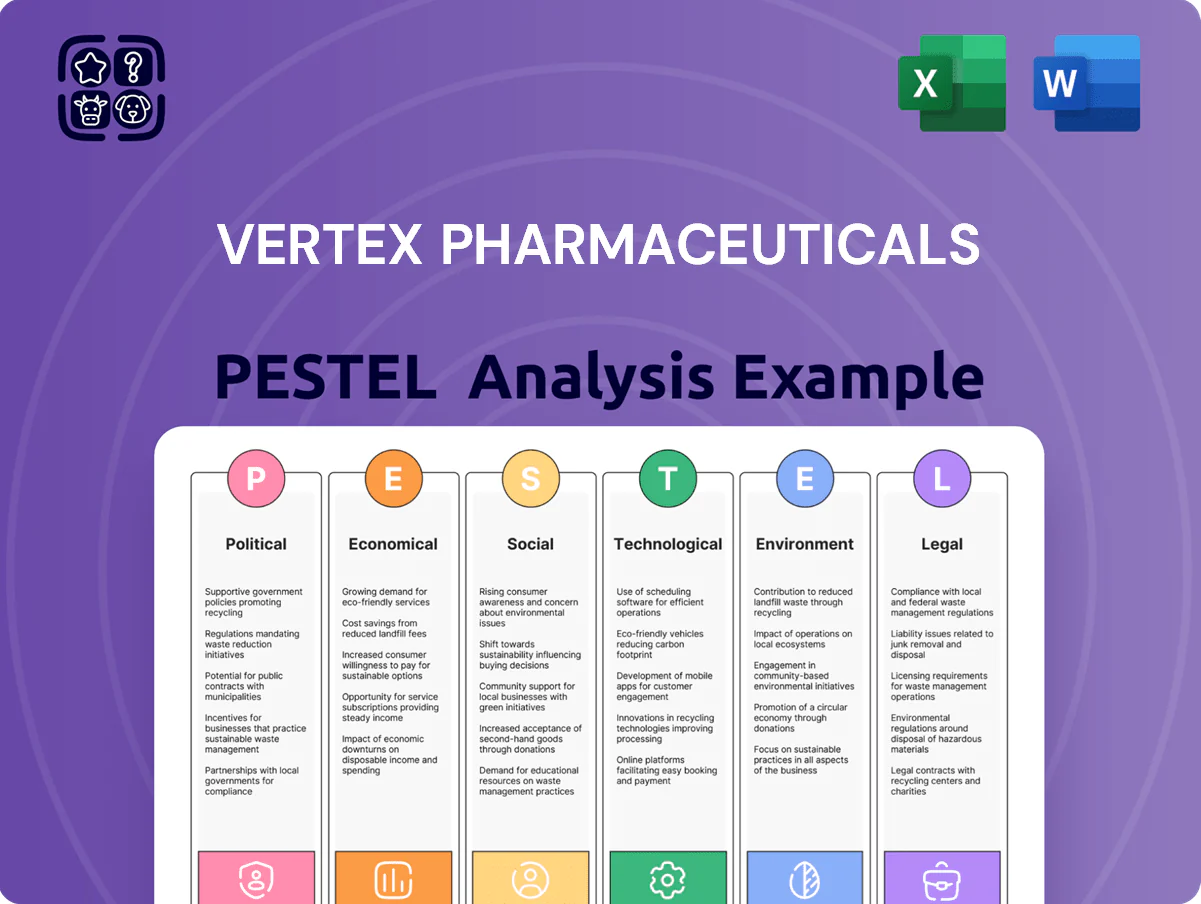

Unlock strategic clarity with our PESTLE Analysis of Vertex Pharmaceuticals—concise insights into regulatory challenges, market dynamics, technological innovation, and socio-environmental trends shaping its outlook; ideal for investors and strategists. Purchase the full report to access the complete, ready-to-use breakdown and actionable recommendations for immediate decision-making.

Political factors

Impact of US Drug Pricing Legislation

The Inflation Reduction Act’s drug price negotiation program targets high-cost specialty medicines and could affect Vertex’s US revenue, with Medicare negotiations starting in 2026 and projected savings of $100+ billion through 2029; Vertex’s 2025 CF product sales were $10.7B, exposing its franchise to pricing pressure if selected.

Vertex is engaging lawmakers to preserve orphan drug exemptions that underpin its R&D model; orphan-designated therapies accounted for over 40% of its pipeline, and loss of incentives could raise its effective tax and development costs, altering ROI on rare-disease programs.

Global Regulatory Approval Pathways

Vertex depends on FDA and EMA streamlined pathways to commercialize its gene-editing and small-molecule drugs; FDA accelerated approvals grew 18% from 2019–2023, benefiting fast-to-market assets like exa-cel (Vertex/CRISPR) whose €1.6bn 2024 revenue outlook hinges on timely approvals.

Shifts in regulatory leadership or priority toward curative therapies could compress or extend timelines—FDA review times averaged ~10 months for priority reviews in 2023—directly affecting Vertex’s R&D ROI and peak-sales projections.

Maintaining collaborative agency relations is critical for launching new pain and kidney indications, where Vertex projects combined addressable markets of $40–60bn by 2030 and relies on adaptive approval pathways to reach patients and revenue targets.

International Trade and Geopolitical Stability

As a global biopharma, Vertex faces trade tensions and geopolitical shifts that could disrupt distribution of its cystic fibrosis medicines, with 2024 revenue of $10.6B exposing global supply vulnerabilities. Tariffs or instability in key manufacturing hubs—notably Ireland and Singapore where Vertex has operations—could raise raw material costs; global pharma supply-chain disruptions increased lead times by ~22% in 2022–24. Vertex lists supply-chain diversification as a strategic priority to mitigate political risk and protect cross-border research collaborations.

Government Healthcare Spending and Reimbursement

- Reimbursement influenced by national budgets and HTA decisions

- Typical CF therapy list prices > $250,000/year

- Lengthy negotiations delay access and revenue realization

- Growing political push for cost-control and outcome-based pricing

Public Health Policy and Opioid Crisis Response

Government emphasis on the opioid crisis favors development of non-opioid treatments like suzetrigine; US overdose deaths rose to ~109,000 in 2022, sustaining political pressure for alternatives.

Vertex can leverage fast-track designations and public funding initiatives—FDA fast-track and NIH grants—improving approval timelines and reducing development costs.

This alignment boosts Vertex’s ability to secure government contracts, reimbursement support, and faster market uptake for its pain portfolio.

- Opioid deaths ~109,000 (2022), sustaining policy focus

- Regulatory fast-track pathways available (FDA/NIH)

- Potential for government contracts and favorable reimbursement

Vertex faces IRA, orphan-incentive and supply-chain risks that could dent $10.7B sales

Political risks: IRA negotiation (Medicare drug price talks from 2026) could hit Vertex’s $10.7B CF sales; orphan incentive changes risk raising R&D costs for >40% orphan pipeline; FDA/EMA accelerated pathways (priority review ~10 months in 2023) crucial for exa-cel and gene-editing launches; trade tensions/supply-chain lead times up ~22% (2022–24) threaten global distribution and costs.

| Metric | Value |

|---|---|

| 2024 CF sales | $10.7B |

| Orphan pipeline (%) | 40%+ |

| Priority review avg | ~10 months (2023) |

| Supply lead-time rise | ~22% (2022–24) |

What is included in the product

Explores how macro-environmental factors uniquely affect Vertex Pharmaceuticals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and sector-specific examples to identify risks and opportunities.

A concise, visually segmented Vertex Pharmaceuticals PESTLE summary for quick reference in meetings—easy to drop into slides, annotate for regional context, and share across teams to streamline risk discussions and strategic planning.

Economic factors

High Research and Development Investment

Vertex directs roughly 30% of revenue to R&D—about $3.3 billion in 2024—sustaining its leadership in cystic fibrosis and expanding into gene and cell therapies.

Clinical trials for gene and cell treatments often run into hundreds of millions per program, requiring long-term capital and multi-year financing plans.

Rising interest rates in 2022–2024 increased cost of capital, so efficient allocation and prioritization of programs are critical to preserve pipeline momentum and shareholder returns.

Revenue Concentration in Cystic Fibrosis

In 2024 Vertex generated roughly 85% of revenue from cystic fibrosis products, concentrating cash flow and creating material exposure to pricing pressure or competitive entry.

Strong margins supported $10.8B in 2024 revenue and $7.6B operating cash flow, but an economic downturn or biosimilar/novel-entry risks could materially reduce these streams.

Diversification into pain management and sickle cell—programs progressing in late-stage trials—is economically necessary to stabilize long-term revenue and reduce dependency on CF sales.

Global Currency Fluctuations

Operating across 40+ countries, Vertex faces FX volatility that in 2024 saw a ~6% appreciation of the US dollar versus major currencies, which reduced reported non‑US revenue by an estimated $180–220 million; a strong dollar thus dampens top‑line growth. Management reported using forward contracts and cross‑currency swaps, with hedges covering portions of anticipated cash flows and a 2024 FX loss (net of hedging) disclosed in filings to limit currency impact.

Insurance Coverage and Patient Affordability

The economic viability of Vertex’s pipeline hinges on payer willingness to cover high-cost therapies; US specialty drug spend reached $260B in 2024, pressuring coverage decisions.

High out-of-pocket costs can suppress uptake—average annual patient cost-sharing for specialty drugs often exceeds $3,000—limiting adoption despite clinical benefit.

Vertex must prove long-term cost-effectiveness; value dossiers citing reduced hospitalizations and QALY gains are key to justify list prices that contributed to Vertex’s 2024 revenue of $9.6B.

- Payer coverage pivotal amid $260B specialty spend (2024)

- Average patient specialty cost-sharing >$3,000/year

- Need robust cost-effectiveness (QALYs, reduced hospitalizations)

- High prices reflected in Vertex 2024 revenue $9.6B

Market Competition and Biosimilars

As key CF drug patents near expiration by 2026–2028, biosimilar entrants could pressure Vertex’s revenues; Vertex reported CF drug sales of $9.4B in 2024, making market protection critical.

Vertex must accelerate patient switches to next‑gen combination therapies—R&D spend was $2.6B in 2024—to defend share against lower‑cost rivals.

The economic imperative to improve efficacy and delivery is ongoing as pricing pressure grows and payer scrutiny rises.

- 2024 CF sales $9.4B

- R&D spend $2.6B (2024)

- Patent expiries 2026–2028 (CF portfolio)

Vertex 2024: $10.8B revenue, $7.6B OCF, heavy R&D, patent cliff 2026–28

Vertex’s 2024 economics: $10.8B revenue, $7.6B operating cash flow, ~30% revenue to R&D (~$3.3B); CF sales ~$9.4B (85% of revenue), R&D $2.6B; US specialty drug spend $260B (2024), average patient cost-sharing >$3,000; USD appreciation reduced reported non‑US revenue by ~$180–220M; CF patents expire 2026–2028 risking biosimilar pressure.

| Metric | 2024 |

|---|---|

| Revenue | $10.8B |

| Operating cash flow | $7.6B |

| CF sales | $9.4B |

| R&D spend | $2.6–3.3B |

| US specialty spend | $260B |

| FX headwind | -$180–220M |

Preview the Actual Deliverable

Vertex Pharmaceuticals PESTLE Analysis

The preview shown here is the exact Vertex Pharmaceuticals PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Vertex Pharmaceuticals—concise insights into regulatory challenges, market dynamics, technological innovation, and socio-environmental trends shaping its outlook; ideal for investors and strategists. Purchase the full report to access the complete, ready-to-use breakdown and actionable recommendations for immediate decision-making.

Political factors

Impact of US Drug Pricing Legislation

The Inflation Reduction Act’s drug price negotiation program targets high-cost specialty medicines and could affect Vertex’s US revenue, with Medicare negotiations starting in 2026 and projected savings of $100+ billion through 2029; Vertex’s 2025 CF product sales were $10.7B, exposing its franchise to pricing pressure if selected.

Vertex is engaging lawmakers to preserve orphan drug exemptions that underpin its R&D model; orphan-designated therapies accounted for over 40% of its pipeline, and loss of incentives could raise its effective tax and development costs, altering ROI on rare-disease programs.

Global Regulatory Approval Pathways

Vertex depends on FDA and EMA streamlined pathways to commercialize its gene-editing and small-molecule drugs; FDA accelerated approvals grew 18% from 2019–2023, benefiting fast-to-market assets like exa-cel (Vertex/CRISPR) whose €1.6bn 2024 revenue outlook hinges on timely approvals.

Shifts in regulatory leadership or priority toward curative therapies could compress or extend timelines—FDA review times averaged ~10 months for priority reviews in 2023—directly affecting Vertex’s R&D ROI and peak-sales projections.

Maintaining collaborative agency relations is critical for launching new pain and kidney indications, where Vertex projects combined addressable markets of $40–60bn by 2030 and relies on adaptive approval pathways to reach patients and revenue targets.

International Trade and Geopolitical Stability

As a global biopharma, Vertex faces trade tensions and geopolitical shifts that could disrupt distribution of its cystic fibrosis medicines, with 2024 revenue of $10.6B exposing global supply vulnerabilities. Tariffs or instability in key manufacturing hubs—notably Ireland and Singapore where Vertex has operations—could raise raw material costs; global pharma supply-chain disruptions increased lead times by ~22% in 2022–24. Vertex lists supply-chain diversification as a strategic priority to mitigate political risk and protect cross-border research collaborations.

Government Healthcare Spending and Reimbursement

- Reimbursement influenced by national budgets and HTA decisions

- Typical CF therapy list prices > $250,000/year

- Lengthy negotiations delay access and revenue realization

- Growing political push for cost-control and outcome-based pricing

Public Health Policy and Opioid Crisis Response

Government emphasis on the opioid crisis favors development of non-opioid treatments like suzetrigine; US overdose deaths rose to ~109,000 in 2022, sustaining political pressure for alternatives.

Vertex can leverage fast-track designations and public funding initiatives—FDA fast-track and NIH grants—improving approval timelines and reducing development costs.

This alignment boosts Vertex’s ability to secure government contracts, reimbursement support, and faster market uptake for its pain portfolio.

- Opioid deaths ~109,000 (2022), sustaining policy focus

- Regulatory fast-track pathways available (FDA/NIH)

- Potential for government contracts and favorable reimbursement

Vertex faces IRA, orphan-incentive and supply-chain risks that could dent $10.7B sales

Political risks: IRA negotiation (Medicare drug price talks from 2026) could hit Vertex’s $10.7B CF sales; orphan incentive changes risk raising R&D costs for >40% orphan pipeline; FDA/EMA accelerated pathways (priority review ~10 months in 2023) crucial for exa-cel and gene-editing launches; trade tensions/supply-chain lead times up ~22% (2022–24) threaten global distribution and costs.

| Metric | Value |

|---|---|

| 2024 CF sales | $10.7B |

| Orphan pipeline (%) | 40%+ |

| Priority review avg | ~10 months (2023) |

| Supply lead-time rise | ~22% (2022–24) |

What is included in the product

Explores how macro-environmental factors uniquely affect Vertex Pharmaceuticals across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and sector-specific examples to identify risks and opportunities.

A concise, visually segmented Vertex Pharmaceuticals PESTLE summary for quick reference in meetings—easy to drop into slides, annotate for regional context, and share across teams to streamline risk discussions and strategic planning.

Economic factors

High Research and Development Investment

Vertex directs roughly 30% of revenue to R&D—about $3.3 billion in 2024—sustaining its leadership in cystic fibrosis and expanding into gene and cell therapies.

Clinical trials for gene and cell treatments often run into hundreds of millions per program, requiring long-term capital and multi-year financing plans.

Rising interest rates in 2022–2024 increased cost of capital, so efficient allocation and prioritization of programs are critical to preserve pipeline momentum and shareholder returns.

Revenue Concentration in Cystic Fibrosis

In 2024 Vertex generated roughly 85% of revenue from cystic fibrosis products, concentrating cash flow and creating material exposure to pricing pressure or competitive entry.

Strong margins supported $10.8B in 2024 revenue and $7.6B operating cash flow, but an economic downturn or biosimilar/novel-entry risks could materially reduce these streams.

Diversification into pain management and sickle cell—programs progressing in late-stage trials—is economically necessary to stabilize long-term revenue and reduce dependency on CF sales.

Global Currency Fluctuations

Operating across 40+ countries, Vertex faces FX volatility that in 2024 saw a ~6% appreciation of the US dollar versus major currencies, which reduced reported non‑US revenue by an estimated $180–220 million; a strong dollar thus dampens top‑line growth. Management reported using forward contracts and cross‑currency swaps, with hedges covering portions of anticipated cash flows and a 2024 FX loss (net of hedging) disclosed in filings to limit currency impact.

Insurance Coverage and Patient Affordability

The economic viability of Vertex’s pipeline hinges on payer willingness to cover high-cost therapies; US specialty drug spend reached $260B in 2024, pressuring coverage decisions.

High out-of-pocket costs can suppress uptake—average annual patient cost-sharing for specialty drugs often exceeds $3,000—limiting adoption despite clinical benefit.

Vertex must prove long-term cost-effectiveness; value dossiers citing reduced hospitalizations and QALY gains are key to justify list prices that contributed to Vertex’s 2024 revenue of $9.6B.

- Payer coverage pivotal amid $260B specialty spend (2024)

- Average patient specialty cost-sharing >$3,000/year

- Need robust cost-effectiveness (QALYs, reduced hospitalizations)

- High prices reflected in Vertex 2024 revenue $9.6B

Market Competition and Biosimilars

As key CF drug patents near expiration by 2026–2028, biosimilar entrants could pressure Vertex’s revenues; Vertex reported CF drug sales of $9.4B in 2024, making market protection critical.

Vertex must accelerate patient switches to next‑gen combination therapies—R&D spend was $2.6B in 2024—to defend share against lower‑cost rivals.

The economic imperative to improve efficacy and delivery is ongoing as pricing pressure grows and payer scrutiny rises.

- 2024 CF sales $9.4B

- R&D spend $2.6B (2024)

- Patent expiries 2026–2028 (CF portfolio)

Vertex 2024: $10.8B revenue, $7.6B OCF, heavy R&D, patent cliff 2026–28

Vertex’s 2024 economics: $10.8B revenue, $7.6B operating cash flow, ~30% revenue to R&D (~$3.3B); CF sales ~$9.4B (85% of revenue), R&D $2.6B; US specialty drug spend $260B (2024), average patient cost-sharing >$3,000; USD appreciation reduced reported non‑US revenue by ~$180–220M; CF patents expire 2026–2028 risking biosimilar pressure.

| Metric | 2024 |

|---|---|

| Revenue | $10.8B |

| Operating cash flow | $7.6B |

| CF sales | $9.4B |

| R&D spend | $2.6–3.3B |

| US specialty spend | $260B |

| FX headwind | -$180–220M |

Preview the Actual Deliverable

Vertex Pharmaceuticals PESTLE Analysis

The preview shown here is the exact Vertex Pharmaceuticals PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.