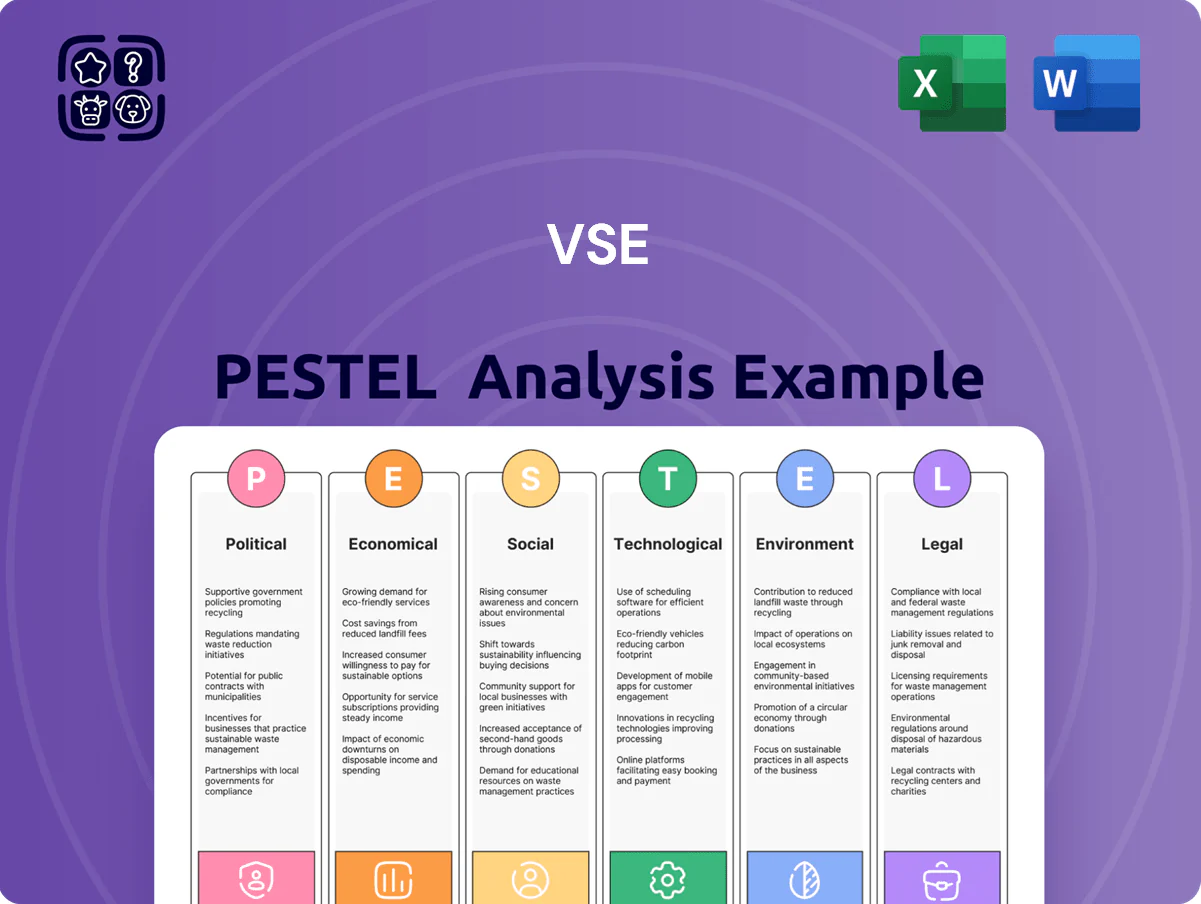

VSE PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, social trends, and tech disruptions are shaping VSE’s strategic outlook with our concise PESTLE snapshot—then dive deeper with the full report for actionable recommendations and data-backed forecasts. Purchase the complete PESTLE now to equip your investment thesis or strategic plan with timely, expert analysis.

Political factors

Defense Budget Allocations

As of late 2025, federal defense sustainment funding—roughly $220B of the FY2026 O&M and procurement envelopes—remains a primary driver for VSE operations, with sustainment-specific budgets near $45B influencing service contracts and spare-parts demand.

Congressional shifts favoring modernization over legacy maintenance risk reducing multi-year sustainment awards by an estimated 10–15%, pressuring VSE’s long-term contract stability and revenue visibility.

Annual budget cycles and the 25% chance of continuing resolutions in recent years, plus occasional shutdowns that delayed procurements by 60–90 days, require VSE to manage cashflow and program staffing tightly.

Geopolitical Tensions

Ongoing conflicts and regional instabilities drive demand for rapid supply chain solutions and equipment readiness; global defense spending rose to an estimated 2.24 trillion USD in 2023 and remained elevated in 2024, boosting VSE’s serviceable addressable market for logistics and maintenance.

Heightened military preparedness among U.S. and allied forces—U.S. defense procurement up 4% year-over-year in 2024—supports recurring revenue for VSE’s maintenance, repair, and overhaul services.

However, geopolitical tensions raise risks for international operations and global logistics security: maritime insurance premiums and freight disruptions spiked in 2023–2024, increasing operating costs and potential revenue volatility for VSE.

Federal Procurement Policies

Changes in federal acquisition regulations, such as the 2023 FAR updates raising domestic sourcing thresholds and increased small business set-aside targets (FY2024 federal small business goal 17.5%), can reshape competition for mid-tier defense contractors like VSE, which reported $1.2B revenue in FY2024.

Stricter domestic content and Buy American rules force VSE to adapt supply chains and revise bids, potentially affecting margins given its 8–10% operating margin range in recent years.

Continuous compliance with evolving contracting standards is critical to retain large sustainment programs—VSE’s services backlog of ~$2.4B (FY2024) underscores exposure to regulatory-driven award risks.

International Trade Relations

Trade policies and tariffs shape VSE’s cost base; US tariffs and export controls raised compliance costs by an estimated 4–6% of COGS for US defense suppliers in 2024, affecting component sourcing and margins.

Expanding internationally exposes VSE to political scrutiny on tech transfers and joint ventures, with licensing approvals taking 3–9 months on average in 2024 for controlled items.

US diplomatic ties with markets like UK, Japan, UAE and select NATO partners—accounting for a growing share of aerospace defense trade—determine market access and contract timelines.

- Tariff/compliance impact: ~4–6% of COGS (2024 est.)

- Export licensing delays: 3–9 months (2024)

- Key markets: UK, Japan, UAE, NATO partners

Energy Independence Initiatives

Government initiatives targeting energy independence and a $65B federal grid modernization plan through 2026 boost demand for VSE’s energy services, as resilience grants and tax credits favor contractors with legacy-system expertise.

Policies emphasizing domestic production — U.S. energy-sector capex up ~9% in 2024 to $230B — create stable, multi-year contracts for specialized engineering, maintenance, and logistics that match VSE’s competencies.

- Federal grid modernization funding: $65B (through 2026)

- U.S. energy capex 2024: ~$230B (+9% YoY)

- Increased resilience incentives favor legacy-system maintenance

Defense sustainment fuels VSE backlog amid modernization risk, tariffs and export delays

Federal defense sustainment funding (~$45B sustainment; $220B O&M/procure FY2026) and rising 2024 US defense spend (+4% YoY) underpin VSE’s backlog (~$2.4B, FY2024) but modernization preferences risk −10–15% sustainment awards; tariffs/compliance added ~4–6% COGS (2024) and export licensing delays averaged 3–9 months.

| Metric | Value |

|---|---|

| Sustainment budget | $45B |

| O&M/procure FY2026 | $220B |

| VSE backlog FY2024 | $2.4B |

| Tariff impact | 4–6% COGS |

| Export delays | 3–9 months |

What is included in the product

Explores how external macro-environmental factors uniquely affect the VSE across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data, forward-looking insights, and industry-specific examples to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

Condenses the full VSE PESTLE into a clear, shareable summary that’s visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Commercial Aviation Growth

The continued expansion of global air travel through 2025, with IATA projecting 4.1 billion passengers in 2024 and 4.6 billion by 2025, has increased demand for VSE’s aviation distribution and MRO services;

airlines extending fleet lives to cut costs drives aftermarket parts demand—commercial aftermarket estimated at $100+ billion in 2024—supporting stable, non-defense revenue for VSE;

Inflationary Pressure on Labor

Rising labor costs for skilled technicians and engineers—wages up ~4.5% YoY in aerospace/defense trades in 2025—squeeze VSE profit margins on service-heavy contracts where labor is ~45% of cost.

VSE must balance market-competitive pay (median technician wage rose to $28.50/hr in 2025) against fixed-price government/commercial agreements that limit pass-through pricing.

Persistent inflation (U.S. CPI ~3.4% in 2025) elevates raw materials and logistics costs, increasing COGS and input volatility for VSE’s supply-chain-intensive services.

Interest Rate Environment

As of late 2025, the higher US federal funds rate near 5.25–5.50% has raised VSE’s cost of debt, tightening margins on acquisition financing and increasing annual interest expense—VSE’s net interest cost could rise by an estimated 10–15% on new borrowings versus 2023 levels.

Global Supply Chain Stability

Economic fluctuations in 2024–25—including a 14% surge in global container rates in 2024 and semiconductor fab utilization above 85%—strain VSE’s role as a supply-chain integrator, risking fulfillment delays and higher logistics spend.

Despite expertise in complexity management, extreme volatility has driven inventory carrying costs up to 22% for comparable integrators, increasing risk of stockouts for VSE without resilience measures.

Strengthening resilience—nearshoring, multi-sourcing, and buffer inventory—remains a priority to limit revenue disruption and cap working-capital increases tied to external shocks.

- 2024 container rate rise ~14%

- Semiconductor capacity >85%

- Inventory carrying costs up to 22%

- Resilience: nearshoring, multi-sourcing, buffer stock

Defense Spending Cycles

The broader economic health determines fiscal space for sustained US defense spending; FY2025 enacted US defense budget was about 858 billion USD, down 1.8% real vs FY2024, signaling tighter room for new programs.

Economic downturns can trigger austerity, reducing sustainment and engineering project volumes—VSE models GDP, deficit-to-GDP (projected ~5.0% in 2025) and defense appropriations to forecast demand.

- FY2025 US defense budget ~858B USD

- Projected US deficit ~5.0% of GDP in 2025

- VSE uses GDP, deficit, appropriations to forecast sustainment demand

Air travel rebounds to 4.6B in 2025 as $100B aftermarket, rising wages, and higher costs bite

Global air travel 4.1B pax (2024) → 4.6B (2025); commercial aftermarket ~$100B (2024); technician median wage $28.50/hr (2025) with ~4.5% YoY wage growth; U.S. CPI ~3.4% (2025); federal funds ~5.25–5.50% (late 2025); FY2025 US defense budget ~$858B; container rates +14% (2024); inventory carrying costs up to 22%.

| Metric | Value |

|---|---|

| Air passengers | 4.6B (2025) |

| Aftermarket | $100B (2024) |

| Technician wage | $28.50/hr (2025) |

| U.S. CPI | 3.4% (2025) |

| Fed funds | 5.25–5.50% (late 2025) |

| Defense budget | $858B (FY2025) |

What You See Is What You Get

VSE PESTLE Analysis

The preview shown here is the exact VSE PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real snapshot of the final file, with no placeholders or teasers, and the content and structure match the downloadable product. After checkout you’ll instantly get this exact, professionally structured document. Everything displayed here is part of the finished deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, social trends, and tech disruptions are shaping VSE’s strategic outlook with our concise PESTLE snapshot—then dive deeper with the full report for actionable recommendations and data-backed forecasts. Purchase the complete PESTLE now to equip your investment thesis or strategic plan with timely, expert analysis.

Political factors

Defense Budget Allocations

As of late 2025, federal defense sustainment funding—roughly $220B of the FY2026 O&M and procurement envelopes—remains a primary driver for VSE operations, with sustainment-specific budgets near $45B influencing service contracts and spare-parts demand.

Congressional shifts favoring modernization over legacy maintenance risk reducing multi-year sustainment awards by an estimated 10–15%, pressuring VSE’s long-term contract stability and revenue visibility.

Annual budget cycles and the 25% chance of continuing resolutions in recent years, plus occasional shutdowns that delayed procurements by 60–90 days, require VSE to manage cashflow and program staffing tightly.

Geopolitical Tensions

Ongoing conflicts and regional instabilities drive demand for rapid supply chain solutions and equipment readiness; global defense spending rose to an estimated 2.24 trillion USD in 2023 and remained elevated in 2024, boosting VSE’s serviceable addressable market for logistics and maintenance.

Heightened military preparedness among U.S. and allied forces—U.S. defense procurement up 4% year-over-year in 2024—supports recurring revenue for VSE’s maintenance, repair, and overhaul services.

However, geopolitical tensions raise risks for international operations and global logistics security: maritime insurance premiums and freight disruptions spiked in 2023–2024, increasing operating costs and potential revenue volatility for VSE.

Federal Procurement Policies

Changes in federal acquisition regulations, such as the 2023 FAR updates raising domestic sourcing thresholds and increased small business set-aside targets (FY2024 federal small business goal 17.5%), can reshape competition for mid-tier defense contractors like VSE, which reported $1.2B revenue in FY2024.

Stricter domestic content and Buy American rules force VSE to adapt supply chains and revise bids, potentially affecting margins given its 8–10% operating margin range in recent years.

Continuous compliance with evolving contracting standards is critical to retain large sustainment programs—VSE’s services backlog of ~$2.4B (FY2024) underscores exposure to regulatory-driven award risks.

International Trade Relations

Trade policies and tariffs shape VSE’s cost base; US tariffs and export controls raised compliance costs by an estimated 4–6% of COGS for US defense suppliers in 2024, affecting component sourcing and margins.

Expanding internationally exposes VSE to political scrutiny on tech transfers and joint ventures, with licensing approvals taking 3–9 months on average in 2024 for controlled items.

US diplomatic ties with markets like UK, Japan, UAE and select NATO partners—accounting for a growing share of aerospace defense trade—determine market access and contract timelines.

- Tariff/compliance impact: ~4–6% of COGS (2024 est.)

- Export licensing delays: 3–9 months (2024)

- Key markets: UK, Japan, UAE, NATO partners

Energy Independence Initiatives

Government initiatives targeting energy independence and a $65B federal grid modernization plan through 2026 boost demand for VSE’s energy services, as resilience grants and tax credits favor contractors with legacy-system expertise.

Policies emphasizing domestic production — U.S. energy-sector capex up ~9% in 2024 to $230B — create stable, multi-year contracts for specialized engineering, maintenance, and logistics that match VSE’s competencies.

- Federal grid modernization funding: $65B (through 2026)

- U.S. energy capex 2024: ~$230B (+9% YoY)

- Increased resilience incentives favor legacy-system maintenance

Defense sustainment fuels VSE backlog amid modernization risk, tariffs and export delays

Federal defense sustainment funding (~$45B sustainment; $220B O&M/procure FY2026) and rising 2024 US defense spend (+4% YoY) underpin VSE’s backlog (~$2.4B, FY2024) but modernization preferences risk −10–15% sustainment awards; tariffs/compliance added ~4–6% COGS (2024) and export licensing delays averaged 3–9 months.

| Metric | Value |

|---|---|

| Sustainment budget | $45B |

| O&M/procure FY2026 | $220B |

| VSE backlog FY2024 | $2.4B |

| Tariff impact | 4–6% COGS |

| Export delays | 3–9 months |

What is included in the product

Explores how external macro-environmental factors uniquely affect the VSE across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data, forward-looking insights, and industry-specific examples to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

Condenses the full VSE PESTLE into a clear, shareable summary that’s visually segmented for quick interpretation and easily dropped into presentations or planning sessions to align teams and support external risk discussions.

Economic factors

Commercial Aviation Growth

The continued expansion of global air travel through 2025, with IATA projecting 4.1 billion passengers in 2024 and 4.6 billion by 2025, has increased demand for VSE’s aviation distribution and MRO services;

airlines extending fleet lives to cut costs drives aftermarket parts demand—commercial aftermarket estimated at $100+ billion in 2024—supporting stable, non-defense revenue for VSE;

Inflationary Pressure on Labor

Rising labor costs for skilled technicians and engineers—wages up ~4.5% YoY in aerospace/defense trades in 2025—squeeze VSE profit margins on service-heavy contracts where labor is ~45% of cost.

VSE must balance market-competitive pay (median technician wage rose to $28.50/hr in 2025) against fixed-price government/commercial agreements that limit pass-through pricing.

Persistent inflation (U.S. CPI ~3.4% in 2025) elevates raw materials and logistics costs, increasing COGS and input volatility for VSE’s supply-chain-intensive services.

Interest Rate Environment

As of late 2025, the higher US federal funds rate near 5.25–5.50% has raised VSE’s cost of debt, tightening margins on acquisition financing and increasing annual interest expense—VSE’s net interest cost could rise by an estimated 10–15% on new borrowings versus 2023 levels.

Global Supply Chain Stability

Economic fluctuations in 2024–25—including a 14% surge in global container rates in 2024 and semiconductor fab utilization above 85%—strain VSE’s role as a supply-chain integrator, risking fulfillment delays and higher logistics spend.

Despite expertise in complexity management, extreme volatility has driven inventory carrying costs up to 22% for comparable integrators, increasing risk of stockouts for VSE without resilience measures.

Strengthening resilience—nearshoring, multi-sourcing, and buffer inventory—remains a priority to limit revenue disruption and cap working-capital increases tied to external shocks.

- 2024 container rate rise ~14%

- Semiconductor capacity >85%

- Inventory carrying costs up to 22%

- Resilience: nearshoring, multi-sourcing, buffer stock

Defense Spending Cycles

The broader economic health determines fiscal space for sustained US defense spending; FY2025 enacted US defense budget was about 858 billion USD, down 1.8% real vs FY2024, signaling tighter room for new programs.

Economic downturns can trigger austerity, reducing sustainment and engineering project volumes—VSE models GDP, deficit-to-GDP (projected ~5.0% in 2025) and defense appropriations to forecast demand.

- FY2025 US defense budget ~858B USD

- Projected US deficit ~5.0% of GDP in 2025

- VSE uses GDP, deficit, appropriations to forecast sustainment demand

Air travel rebounds to 4.6B in 2025 as $100B aftermarket, rising wages, and higher costs bite

Global air travel 4.1B pax (2024) → 4.6B (2025); commercial aftermarket ~$100B (2024); technician median wage $28.50/hr (2025) with ~4.5% YoY wage growth; U.S. CPI ~3.4% (2025); federal funds ~5.25–5.50% (late 2025); FY2025 US defense budget ~$858B; container rates +14% (2024); inventory carrying costs up to 22%.

| Metric | Value |

|---|---|

| Air passengers | 4.6B (2025) |

| Aftermarket | $100B (2024) |

| Technician wage | $28.50/hr (2025) |

| U.S. CPI | 3.4% (2025) |

| Fed funds | 5.25–5.50% (late 2025) |

| Defense budget | $858B (FY2025) |

What You See Is What You Get

VSE PESTLE Analysis

The preview shown here is the exact VSE PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is a real snapshot of the final file, with no placeholders or teasers, and the content and structure match the downloadable product. After checkout you’ll instantly get this exact, professionally structured document. Everything displayed here is part of the finished deliverable.