WaFd Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

WaFd Bank navigates a competitive landscape shaped by the bargaining power of its customers and the constant threat of new entrants. Understanding these forces is crucial for any stakeholder looking to grasp the bank's strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WaFd Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology and Software Providers

Technology and software providers hold considerable sway over WaFd Bank due to the critical nature of their services. Core banking systems, cybersecurity solutions, and digital banking platforms are essential, making specialized vendors quite powerful, particularly when their offerings are proprietary or deeply integrated into the bank's infrastructure.

The increasing reliance on advanced technology, with community banks prioritizing AI and real-time fraud detection in 2025, further amplifies this bargaining power. As financial institutions like WaFd Bank invest more heavily in these areas, the demand for specialized software and the vendors supplying it will likely grow, potentially leading to higher costs and more stringent contract terms.

Financial Data and Information Services

Suppliers of financial data, market intelligence, and credit reporting services wield significant influence over WaFd Bank. The bank relies heavily on accurate and timely information for crucial functions like risk assessment, loan approvals, and managing client wealth.

The specialized nature and essential role of this data, combined with the potential costs associated with changing providers, grant these suppliers considerable bargaining power. For instance, in 2024, the global financial data market was valued at over $30 billion, highlighting the scale and importance of these services.

Financial institutions are prioritizing investments in data analytics and reporting, further solidifying the suppliers' leverage. The increasing demand for sophisticated data solutions means that firms like WaFd Bank are often locked into long-term relationships, making it difficult to switch without incurring substantial costs.

Labor Market for Skilled Talent

The availability of skilled labor, especially in fields like cybersecurity, artificial intelligence, and specialized lending such as SBA expertise, significantly impacts supplier power. A competitive labor market for these professionals can lead to increased wage demands, making it harder for WaFd Bank to secure and keep top talent.

Community banks, like WaFd, often encounter greater difficulties in recruiting technology professionals compared to larger institutions. For instance, in 2024, the demand for cybersecurity professionals outpaced supply by a considerable margin, with some reports indicating millions of unfilled positions globally, driving up compensation expectations.

Deposit Funding Sources

Depositors, while not suppliers in the typical sense, hold significant bargaining power as they provide the essential funding for WaFd Bank's operations. The cost of these deposits, directly tied to interest rates and the competitive landscape for attracting and retaining funds, directly influences the bank's net interest margin and overall profitability.

For 2025, projections indicate that the cost of deposits will likely remain elevated. This environment could present a challenge for midsize and regional banks like WaFd, as they may face increased difficulty in strategically adjusting their deposit rates to manage funding costs effectively amidst heightened competition for liquidity.

- Depositor Influence: Depositors are a primary funding source, and their willingness to place funds with WaFd Bank is influenced by the interest rates offered and the perceived stability of the institution.

- Cost of Funds: The interest paid on deposits represents a significant operating expense for WaFd Bank.

- 2025 Outlook: Deposit costs are anticipated to stay high in 2025, potentially increasing funding expenses for banks.

- Competitive Pressures: Midsize and regional banks may encounter greater challenges in modifying deposit rates in 2025 due to intensified competition for customer deposits.

Regulatory Bodies and Compliance Services

Regulatory bodies significantly influence the banking sector, imposing strict compliance requirements that directly impact operational costs and strategies. WaFd Bank, like its peers, must navigate a complex web of regulations, requiring substantial investment in compliance personnel and technology to ensure adherence. For instance, in 2024, the financial services industry continued to see increased regulatory focus on areas such as cybersecurity and data privacy, with penalties for non-compliance potentially reaching millions of dollars.

The evolving nature of these regulations, particularly concerning digital assets and evolving consumer protection laws, further amplifies the bargaining power of suppliers offering specialized compliance services and software solutions. These providers can command higher fees due to the critical need for banks to maintain compliance and avoid costly fines. The global cybersecurity market, for example, was projected to reach over $300 billion in 2024, highlighting the significant spending and reliance on specialized vendors.

- Increased Regulatory Scrutiny: Banks face growing pressure from regulators regarding cybersecurity and data privacy.

- Compliance Costs: Adhering to evolving regulations necessitates significant investment in compliance services and expertise.

- Supplier Dependence: The complexity of regulations increases reliance on specialized compliance technology and service providers.

- Market Growth: The cybersecurity market alone, projected to exceed $300 billion in 2024, demonstrates the scale of spending on regulatory compliance solutions.

Tech & Data Suppliers: The Unseen Power in Banking

Suppliers of essential technology and data are key influencers for WaFd Bank, given the critical nature of their services. Proprietary core banking systems, advanced cybersecurity, and specialized financial data are vital, granting these vendors significant leverage, especially when switching costs are high.

The increasing demand for sophisticated data analytics and AI solutions, a trend observed throughout 2024 and continuing into 2025, further strengthens the bargaining power of data providers. Banks like WaFd Bank are increasingly reliant on these specialized services, often leading to longer-term contracts and less flexibility.

The market for these essential services is substantial; for instance, the global financial data market exceeded $30 billion in 2024, underscoring the critical role and value of these suppliers.

The bargaining power of suppliers is influenced by the availability of specialized talent. For example, the shortage of cybersecurity professionals in 2024, with millions of unfilled positions globally, drove up compensation and strengthened the position of cybersecurity service providers.

What is included in the product

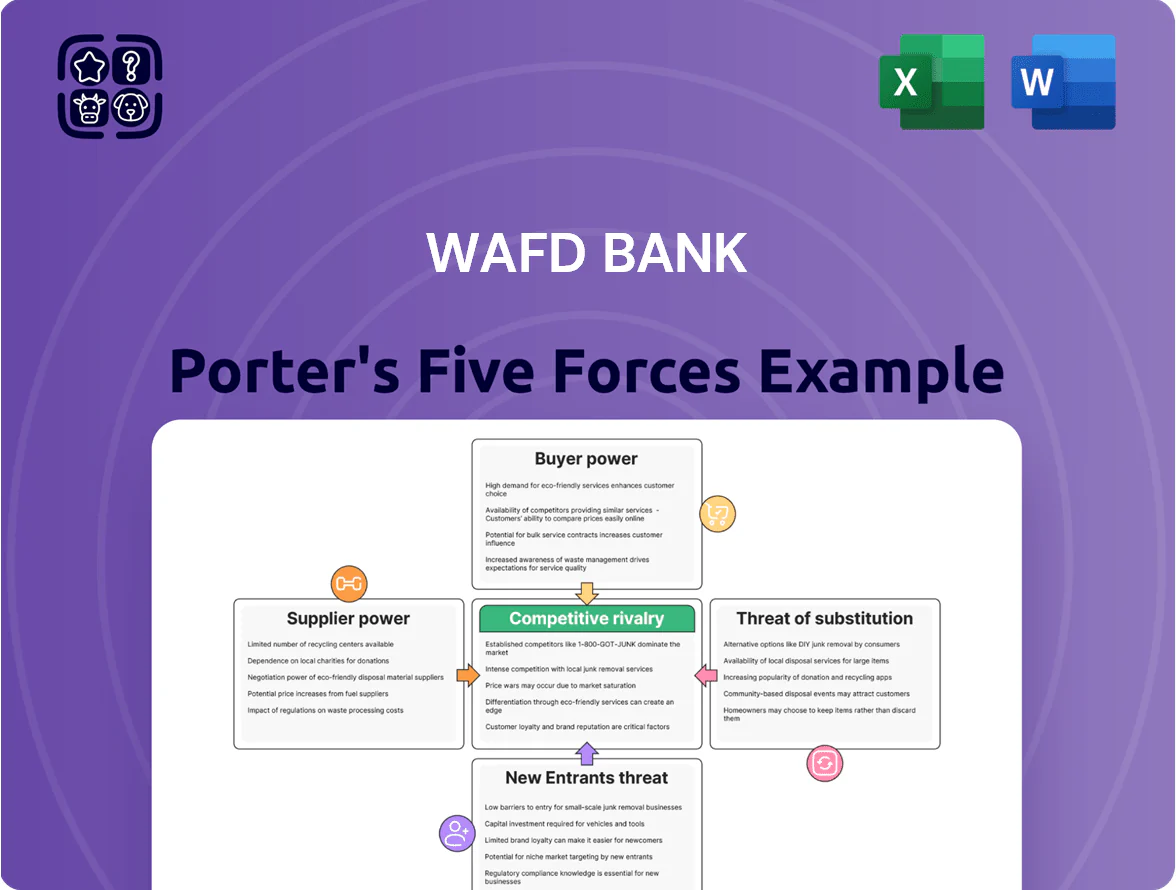

Tailored exclusively for WaFd Bank, this analysis dissects the five competitive forces shaping its market, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces dashboard, allowing WaFd Bank to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Individual and Small Business Depositors

For basic checking and savings accounts, individual and small business depositors generally have low bargaining power. This is because these services are quite standardized, and the convenience of local branches or accessible digital platforms often outweighs minor differences in offerings. WaFd Bank's focus on customer service, evidenced by its recognition in the Pacific Northwest, can influence customer loyalty and reduce their inclination to switch for slightly better rates.

Commercial Real Estate Borrowers

Commercial real estate borrowers, particularly large developers or established companies, often wield significant bargaining power. They can negotiate favorable interest rates, loan durations, and collateral stipulations, especially with a growing presence of alternative lenders in the CRE space.

The dynamic CRE market, marked by interest rate volatility and rising delinquencies in certain property types, further empowers borrowers. For instance, in Q1 2024, commercial mortgage-backed securities (CMBS) delinquency rates saw an uptick, potentially giving well-capitalized borrowers more leverage in discussions with traditional banks like WaFd.

Wealth Management Clients

Wealth management clients, particularly high-net-worth individuals and institutional investors, often wield considerable bargaining power. Their sophisticated financial requirements frequently necessitate tailored strategies, and the ease with which they can transfer their assets to competing institutions means providers must consistently deliver exceptional value and service. For instance, in 2023, the global wealth management market managed trillions in assets, highlighting the sheer scale of client influence.

Small Business Loan Applicants

Small business loan applicants typically possess moderate bargaining power. Their need for capital is significant, but this is tempered by the availability of other lenders and WaFd Bank's own assessment of risk.

WaFd Bank's strategic focus on business banking and its substantial origination of small business loans in recent years, such as a reported increase in commercial and industrial loan originations, demonstrates a commitment to serving this market. This can create a more competitive lending environment for small businesses.

- Moderate Bargaining Power: Small businesses need loans but have options.

- Influence of Alternatives: The presence of other lenders affects negotiation leverage.

- WaFd's Business Focus: The bank's expansion into business banking increases its loan origination capacity.

- Loan Origination Data: WaFd's reported increases in commercial loan originations highlight its role in the market.

Digital-Savvy Customers

Digital-savvy customers hold significant bargaining power. They expect seamless online and mobile banking experiences, readily switching to fintechs or other digitally capable banks if their needs aren't met.

WaFd Bank's investment in technology has demonstrably boosted its digital presence, with online traffic to its website seeing substantial growth. This indicates a positive response from customers who value digital convenience.

- Digital Preference: Customers increasingly favor digital channels for banking transactions and expect intuitive, user-friendly platforms.

- Switching Costs: For digitally proficient customers, the perceived cost of switching banks is often low, especially when attractive digital alternatives exist.

- Service Expectations: A demand for 24/7 access, instant transactions, and personalized digital services puts pressure on traditional banks to innovate.

- WaFd's Digital Growth: WaFd Bank reported a notable increase in website traffic, reflecting successful efforts to cater to digitally inclined customers.

Who Holds the Power? Customer Bargaining in Banking

Customers generally have low bargaining power for basic banking services like checking and savings accounts due to standardization and the importance of convenience. However, for more complex services like commercial real estate loans or wealth management, particularly for larger clients, bargaining power increases significantly as they have more options and can negotiate terms. Digital-savvy customers also wield considerable power, readily switching to competitors if digital experiences are subpar, prompting banks like WaFd to invest heavily in technology to retain them.

| Customer Segment | Bargaining Power | Key Factors |

|---|---|---|

| Individual Depositors | Low | Standardized products, convenience, brand loyalty |

| Commercial Real Estate Borrowers | High (for large clients) | Loan size, market competition, borrower's financial strength |

| Wealth Management Clients | High | Asset size, need for tailored services, ease of asset transfer |

| Small Business Borrowers | Moderate | Need for capital, availability of alternative lenders, bank's risk assessment |

| Digital-Savvy Customers | High | Expectation of seamless digital experience, low switching costs |

Same Document Delivered

WaFd Bank Porter's Five Forces Analysis

This preview shows the exact WaFd Bank Porter's Five Forces Analysis you'll receive immediately after purchase, offering a comprehensive examination of competitive forces within the banking industry. You'll gain insights into the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the availability of substitutes. This professionally formatted document is ready for your strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

WaFd Bank navigates a competitive landscape shaped by the bargaining power of its customers and the constant threat of new entrants. Understanding these forces is crucial for any stakeholder looking to grasp the bank's strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WaFd Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology and Software Providers

Technology and software providers hold considerable sway over WaFd Bank due to the critical nature of their services. Core banking systems, cybersecurity solutions, and digital banking platforms are essential, making specialized vendors quite powerful, particularly when their offerings are proprietary or deeply integrated into the bank's infrastructure.

The increasing reliance on advanced technology, with community banks prioritizing AI and real-time fraud detection in 2025, further amplifies this bargaining power. As financial institutions like WaFd Bank invest more heavily in these areas, the demand for specialized software and the vendors supplying it will likely grow, potentially leading to higher costs and more stringent contract terms.

Financial Data and Information Services

Suppliers of financial data, market intelligence, and credit reporting services wield significant influence over WaFd Bank. The bank relies heavily on accurate and timely information for crucial functions like risk assessment, loan approvals, and managing client wealth.

The specialized nature and essential role of this data, combined with the potential costs associated with changing providers, grant these suppliers considerable bargaining power. For instance, in 2024, the global financial data market was valued at over $30 billion, highlighting the scale and importance of these services.

Financial institutions are prioritizing investments in data analytics and reporting, further solidifying the suppliers' leverage. The increasing demand for sophisticated data solutions means that firms like WaFd Bank are often locked into long-term relationships, making it difficult to switch without incurring substantial costs.

Labor Market for Skilled Talent

The availability of skilled labor, especially in fields like cybersecurity, artificial intelligence, and specialized lending such as SBA expertise, significantly impacts supplier power. A competitive labor market for these professionals can lead to increased wage demands, making it harder for WaFd Bank to secure and keep top talent.

Community banks, like WaFd, often encounter greater difficulties in recruiting technology professionals compared to larger institutions. For instance, in 2024, the demand for cybersecurity professionals outpaced supply by a considerable margin, with some reports indicating millions of unfilled positions globally, driving up compensation expectations.

Deposit Funding Sources

Depositors, while not suppliers in the typical sense, hold significant bargaining power as they provide the essential funding for WaFd Bank's operations. The cost of these deposits, directly tied to interest rates and the competitive landscape for attracting and retaining funds, directly influences the bank's net interest margin and overall profitability.

For 2025, projections indicate that the cost of deposits will likely remain elevated. This environment could present a challenge for midsize and regional banks like WaFd, as they may face increased difficulty in strategically adjusting their deposit rates to manage funding costs effectively amidst heightened competition for liquidity.

- Depositor Influence: Depositors are a primary funding source, and their willingness to place funds with WaFd Bank is influenced by the interest rates offered and the perceived stability of the institution.

- Cost of Funds: The interest paid on deposits represents a significant operating expense for WaFd Bank.

- 2025 Outlook: Deposit costs are anticipated to stay high in 2025, potentially increasing funding expenses for banks.

- Competitive Pressures: Midsize and regional banks may encounter greater challenges in modifying deposit rates in 2025 due to intensified competition for customer deposits.

Regulatory Bodies and Compliance Services

Regulatory bodies significantly influence the banking sector, imposing strict compliance requirements that directly impact operational costs and strategies. WaFd Bank, like its peers, must navigate a complex web of regulations, requiring substantial investment in compliance personnel and technology to ensure adherence. For instance, in 2024, the financial services industry continued to see increased regulatory focus on areas such as cybersecurity and data privacy, with penalties for non-compliance potentially reaching millions of dollars.

The evolving nature of these regulations, particularly concerning digital assets and evolving consumer protection laws, further amplifies the bargaining power of suppliers offering specialized compliance services and software solutions. These providers can command higher fees due to the critical need for banks to maintain compliance and avoid costly fines. The global cybersecurity market, for example, was projected to reach over $300 billion in 2024, highlighting the significant spending and reliance on specialized vendors.

- Increased Regulatory Scrutiny: Banks face growing pressure from regulators regarding cybersecurity and data privacy.

- Compliance Costs: Adhering to evolving regulations necessitates significant investment in compliance services and expertise.

- Supplier Dependence: The complexity of regulations increases reliance on specialized compliance technology and service providers.

- Market Growth: The cybersecurity market alone, projected to exceed $300 billion in 2024, demonstrates the scale of spending on regulatory compliance solutions.

Tech & Data Suppliers: The Unseen Power in Banking

Suppliers of essential technology and data are key influencers for WaFd Bank, given the critical nature of their services. Proprietary core banking systems, advanced cybersecurity, and specialized financial data are vital, granting these vendors significant leverage, especially when switching costs are high.

The increasing demand for sophisticated data analytics and AI solutions, a trend observed throughout 2024 and continuing into 2025, further strengthens the bargaining power of data providers. Banks like WaFd Bank are increasingly reliant on these specialized services, often leading to longer-term contracts and less flexibility.

The market for these essential services is substantial; for instance, the global financial data market exceeded $30 billion in 2024, underscoring the critical role and value of these suppliers.

The bargaining power of suppliers is influenced by the availability of specialized talent. For example, the shortage of cybersecurity professionals in 2024, with millions of unfilled positions globally, drove up compensation and strengthened the position of cybersecurity service providers.

What is included in the product

Tailored exclusively for WaFd Bank, this analysis dissects the five competitive forces shaping its market, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces dashboard, allowing WaFd Bank to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Individual and Small Business Depositors

For basic checking and savings accounts, individual and small business depositors generally have low bargaining power. This is because these services are quite standardized, and the convenience of local branches or accessible digital platforms often outweighs minor differences in offerings. WaFd Bank's focus on customer service, evidenced by its recognition in the Pacific Northwest, can influence customer loyalty and reduce their inclination to switch for slightly better rates.

Commercial Real Estate Borrowers

Commercial real estate borrowers, particularly large developers or established companies, often wield significant bargaining power. They can negotiate favorable interest rates, loan durations, and collateral stipulations, especially with a growing presence of alternative lenders in the CRE space.

The dynamic CRE market, marked by interest rate volatility and rising delinquencies in certain property types, further empowers borrowers. For instance, in Q1 2024, commercial mortgage-backed securities (CMBS) delinquency rates saw an uptick, potentially giving well-capitalized borrowers more leverage in discussions with traditional banks like WaFd.

Wealth Management Clients

Wealth management clients, particularly high-net-worth individuals and institutional investors, often wield considerable bargaining power. Their sophisticated financial requirements frequently necessitate tailored strategies, and the ease with which they can transfer their assets to competing institutions means providers must consistently deliver exceptional value and service. For instance, in 2023, the global wealth management market managed trillions in assets, highlighting the sheer scale of client influence.

Small Business Loan Applicants

Small business loan applicants typically possess moderate bargaining power. Their need for capital is significant, but this is tempered by the availability of other lenders and WaFd Bank's own assessment of risk.

WaFd Bank's strategic focus on business banking and its substantial origination of small business loans in recent years, such as a reported increase in commercial and industrial loan originations, demonstrates a commitment to serving this market. This can create a more competitive lending environment for small businesses.

- Moderate Bargaining Power: Small businesses need loans but have options.

- Influence of Alternatives: The presence of other lenders affects negotiation leverage.

- WaFd's Business Focus: The bank's expansion into business banking increases its loan origination capacity.

- Loan Origination Data: WaFd's reported increases in commercial loan originations highlight its role in the market.

Digital-Savvy Customers

Digital-savvy customers hold significant bargaining power. They expect seamless online and mobile banking experiences, readily switching to fintechs or other digitally capable banks if their needs aren't met.

WaFd Bank's investment in technology has demonstrably boosted its digital presence, with online traffic to its website seeing substantial growth. This indicates a positive response from customers who value digital convenience.

- Digital Preference: Customers increasingly favor digital channels for banking transactions and expect intuitive, user-friendly platforms.

- Switching Costs: For digitally proficient customers, the perceived cost of switching banks is often low, especially when attractive digital alternatives exist.

- Service Expectations: A demand for 24/7 access, instant transactions, and personalized digital services puts pressure on traditional banks to innovate.

- WaFd's Digital Growth: WaFd Bank reported a notable increase in website traffic, reflecting successful efforts to cater to digitally inclined customers.

Who Holds the Power? Customer Bargaining in Banking

Customers generally have low bargaining power for basic banking services like checking and savings accounts due to standardization and the importance of convenience. However, for more complex services like commercial real estate loans or wealth management, particularly for larger clients, bargaining power increases significantly as they have more options and can negotiate terms. Digital-savvy customers also wield considerable power, readily switching to competitors if digital experiences are subpar, prompting banks like WaFd to invest heavily in technology to retain them.

| Customer Segment | Bargaining Power | Key Factors |

|---|---|---|

| Individual Depositors | Low | Standardized products, convenience, brand loyalty |

| Commercial Real Estate Borrowers | High (for large clients) | Loan size, market competition, borrower's financial strength |

| Wealth Management Clients | High | Asset size, need for tailored services, ease of asset transfer |

| Small Business Borrowers | Moderate | Need for capital, availability of alternative lenders, bank's risk assessment |

| Digital-Savvy Customers | High | Expectation of seamless digital experience, low switching costs |

Same Document Delivered

WaFd Bank Porter's Five Forces Analysis

This preview shows the exact WaFd Bank Porter's Five Forces Analysis you'll receive immediately after purchase, offering a comprehensive examination of competitive forces within the banking industry. You'll gain insights into the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the availability of substitutes. This professionally formatted document is ready for your strategic planning and decision-making.