Waitr Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

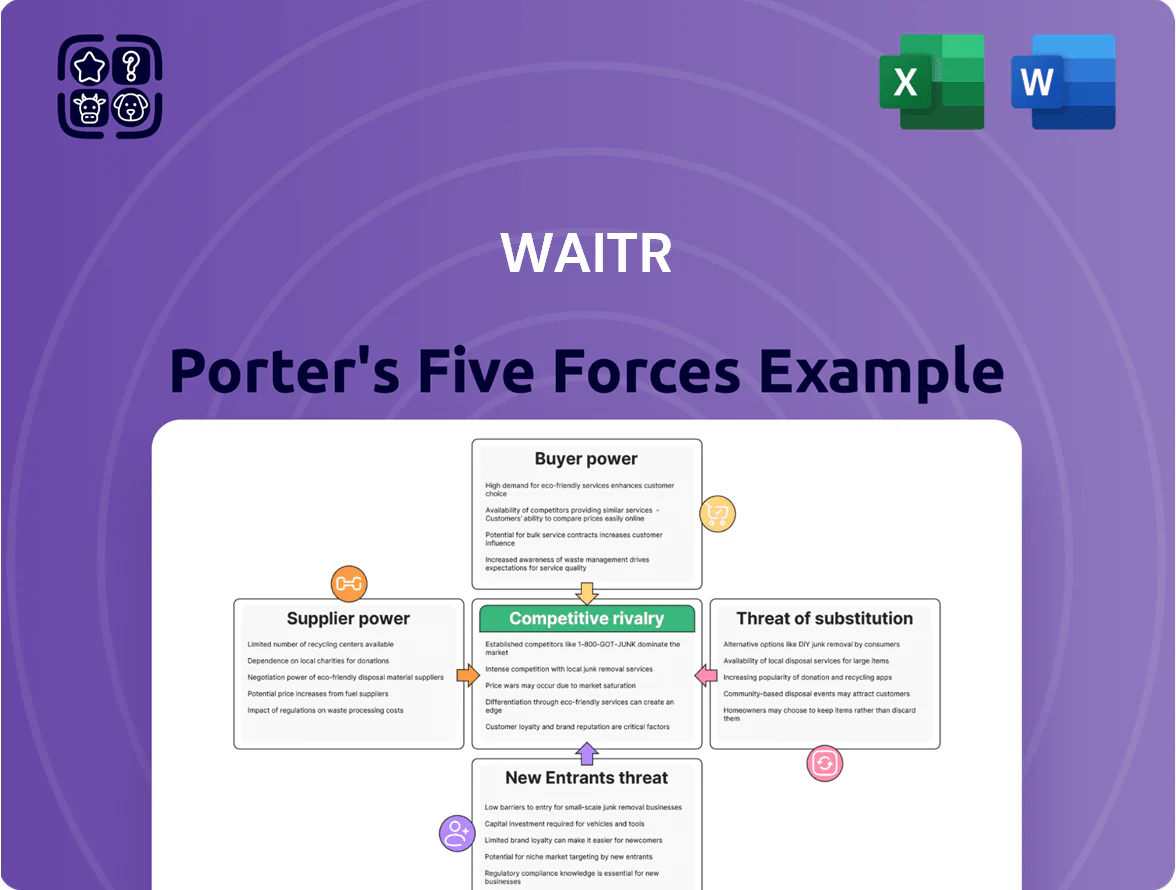

Waitr faces intense local competition, shifting customer loyalty, and rising delivery costs that pressure margins; supplier and regulatory risks also shape its growth outlook. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore Waitr’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Restaurant Base

The majority of ASAP’s suppliers are local, independent restaurants with low individual volumes, so they lack bargaining power to cut commission rates and rely on the platform for digital reach; in 2024, 68% of US independent restaurants used third-party delivery platforms, giving ASAP leverage over pricing.

Still, by 2025–2026 a countertrend emerged: restaurants pushed back on fees—direct ordering rose 22% year-over-year at some chains—pressuring platforms to offer lower commissions or marketing credits to retain partners.

Gig Economy Labor Supply

Delivery drivers are a critical supplier group; local unemployment rates (US 3.9% Dec 2025) and gig alternatives (DoorDash 2025 revenue $8.8B) affect their bargaining power.

Individually they lack leverage, but collective shortages—Turnover for gig drivers often >100% annually—force ASAP to raise incentives or base pay.

Worker-classification rules, like California AB5 impacts and 2025 UK gig-worker rulings, can sharply raise labor costs and shift ASAP’s margin.

Major National Chains

Major national chains hold strong supplier power over Waitr (ASAP) because their brand recognition and bulk order volume let them push for lower commission rates; in 2024, top chains accounted for roughly 35% of delivery platform order value, enabling rate cuts of 2–5 percentage points versus independents.

They also demand exclusive marketing placements and POS integrations, which cost ASAP upfront tech and promo spend; ASAP often accepts margins as low as 8–12% on these partners to keep menu breadth and user retention.

Technology and Infrastructure Providers

ASAP depends on third-party cloud, mapping, and payment providers for core ops; in 2024 cloud services accounted for an estimated 6–9% of comparable gig-economy peers’ variable cost base.

Multiple suppliers exist, but high switching complexity (integration, downtime, compliance) creates supplier stickiness that weakens ASAP’s bargaining power.

Price hikes by major providers (AWS, Google Cloud, Stripe) flow directly into OPEX and can cut EBITDA margins—1–3 percentage points from a 10% vendor price rise is plausible.

- Cloud/mapping/payments = critical fixed costs

- Several vendors, high switching cost → limited leverage

- Vendor price rises can trim EBITDA by ~1–3 pts

Alternative Distribution Channels

Restaurants increasingly buy white-label delivery software to run in-house fleets or hire third-party logistics, cutting reliance on Waitr/ASAP and its ~20–30% commission range; this reduces supplier lock-in and squeezes platform margins.

As of 2024, ~28% of US chains used in-house or third-party delivery tech, shifting bargaining power toward restaurants and pressuring long-term commission pricing.

- In-house/3PL tech reduces platform fees

- Waitr faces margin pressure from 20–30% commissions

- 28% of chains used alternatives in 2024

Delivery dynamics shift: platforms dominate independents, chains regain leverage

Suppliers show mixed power: many small restaurants lack leverage so ASAP controls commissions (68% of independents used third-party delivery in 2024), but rising direct orders (+22% YoY at some chains) and 28% of chains using in-house/3PL in 2024 shift power back to restaurants. Drivers have limited individual power but high turnover (>100% annually) raises incentive costs; cloud/payment vendor price hikes can cut EBITDA ~1–3 pts.

| Metric | 2024–2025 |

|---|---|

| Independents on platforms | 68% |

| Chains using in-house/3PL | 28% |

| Direct order growth (some chains) | +22% YoY |

| Driver turnover | >100% annually |

| Cloud/vendor EBITDA impact | −1–3 pts |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Waitr, detailing each Porter’s force with insights on suppliers, buyers, substitutes, new entrants, and intra-industry rivalry to highlight threats and strategic levers.

Compact five-forces snapshot tailored to Waitr—quickly spot competitive pain points and prioritize strategic fixes.

Customers Bargaining Power

Low Switching Costs

High Price Sensitivity

End-users of delivery platforms show high price sensitivity to service fees, delivery charges, and menu markups; NielsenIQ found 62% of US consumers in 2024 said higher fees made them order less often. Even a $1–2 fee rise can cut order volume by ~5–10% in gig-economy apps, so ASAP (Waitr) is constrained from raising fees without risking churn of active users.

Access to Information

Demand for Diversification

By 2025 consumers expect delivery apps to cover meals, groceries, alcohol and retail; global on-demand groceries grew 28% CAGR 2019–24 and reached $150B in 2024, so ASAP risks losing spend to super-apps if it stays meal-only.

Power shifts to buyers who set service scope, forcing ASAP into costly expansions—engineering, logistics, and COGS increases—that can cut margins; adding grocery/retail can raise fulfillment costs 10–25% per order.

- Consumer demand: groceries +28% CAGR (2019–24)

- Market size: $150B on-demand groceries 2024

- Margin pressure: fulfillment costs +10–25%

- Risk: customer migration to super-apps

Influence of Promotions and Discounts

Promotions and loyalty rewards dominate delivery demand; 2024 US food-delivery coupon usage topped 45%, training customers to wait for deals and cutting full-margin sales for Waitr (ASAP).

That shifts pricing power to customers, forcing ASAP to fund discounts that compress take rates—average effective take rates fell ~3–4 percentage points industry-wide in 2023–24.

ASAP must weigh incentive costs versus retention: if promotions drop, orders can fall 10–20%; if they continue, margins stay squeezed.

- Coupon use ~45% (2024, US delivery)

- Industry take-rate drop ~3–4 pp (2023–24)

- Order drop if promos cut: 10–20%

Promo-dependent: Waitr’s take-rates cut 3–4pp as 15% promos fend off 10–20% order loss

| Metric | Value |

|---|---|

| Users with multiple apps (2024) | 68% |

| Compare platforms before ordering (2024) | 78% |

| Order sensitivity to higher fees (2024) | 62% |

| Promo share of order value (2024) | ~15% |

| Take-rate decline (2023–24) | 3–4 pp |

| Order drop if promos cut | 10–20% |

Full Version Awaits

Waitr Porter's Five Forces Analysis

This preview shows the exact Waitr Porter's Five Forces analysis you'll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.

The document displayed here is the same professionally written file included with your order, containing complete competitive insights, force evaluations, and concise implications for strategy and valuation.

You're viewing the final deliverable: instant access to this exact analysis the moment you complete your purchase—ready to use in presentations or decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Waitr faces intense local competition, shifting customer loyalty, and rising delivery costs that pressure margins; supplier and regulatory risks also shape its growth outlook. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore Waitr’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Restaurant Base

The majority of ASAP’s suppliers are local, independent restaurants with low individual volumes, so they lack bargaining power to cut commission rates and rely on the platform for digital reach; in 2024, 68% of US independent restaurants used third-party delivery platforms, giving ASAP leverage over pricing.

Still, by 2025–2026 a countertrend emerged: restaurants pushed back on fees—direct ordering rose 22% year-over-year at some chains—pressuring platforms to offer lower commissions or marketing credits to retain partners.

Gig Economy Labor Supply

Delivery drivers are a critical supplier group; local unemployment rates (US 3.9% Dec 2025) and gig alternatives (DoorDash 2025 revenue $8.8B) affect their bargaining power.

Individually they lack leverage, but collective shortages—Turnover for gig drivers often >100% annually—force ASAP to raise incentives or base pay.

Worker-classification rules, like California AB5 impacts and 2025 UK gig-worker rulings, can sharply raise labor costs and shift ASAP’s margin.

Major National Chains

Major national chains hold strong supplier power over Waitr (ASAP) because their brand recognition and bulk order volume let them push for lower commission rates; in 2024, top chains accounted for roughly 35% of delivery platform order value, enabling rate cuts of 2–5 percentage points versus independents.

They also demand exclusive marketing placements and POS integrations, which cost ASAP upfront tech and promo spend; ASAP often accepts margins as low as 8–12% on these partners to keep menu breadth and user retention.

Technology and Infrastructure Providers

ASAP depends on third-party cloud, mapping, and payment providers for core ops; in 2024 cloud services accounted for an estimated 6–9% of comparable gig-economy peers’ variable cost base.

Multiple suppliers exist, but high switching complexity (integration, downtime, compliance) creates supplier stickiness that weakens ASAP’s bargaining power.

Price hikes by major providers (AWS, Google Cloud, Stripe) flow directly into OPEX and can cut EBITDA margins—1–3 percentage points from a 10% vendor price rise is plausible.

- Cloud/mapping/payments = critical fixed costs

- Several vendors, high switching cost → limited leverage

- Vendor price rises can trim EBITDA by ~1–3 pts

Alternative Distribution Channels

Restaurants increasingly buy white-label delivery software to run in-house fleets or hire third-party logistics, cutting reliance on Waitr/ASAP and its ~20–30% commission range; this reduces supplier lock-in and squeezes platform margins.

As of 2024, ~28% of US chains used in-house or third-party delivery tech, shifting bargaining power toward restaurants and pressuring long-term commission pricing.

- In-house/3PL tech reduces platform fees

- Waitr faces margin pressure from 20–30% commissions

- 28% of chains used alternatives in 2024

Delivery dynamics shift: platforms dominate independents, chains regain leverage

Suppliers show mixed power: many small restaurants lack leverage so ASAP controls commissions (68% of independents used third-party delivery in 2024), but rising direct orders (+22% YoY at some chains) and 28% of chains using in-house/3PL in 2024 shift power back to restaurants. Drivers have limited individual power but high turnover (>100% annually) raises incentive costs; cloud/payment vendor price hikes can cut EBITDA ~1–3 pts.

| Metric | 2024–2025 |

|---|---|

| Independents on platforms | 68% |

| Chains using in-house/3PL | 28% |

| Direct order growth (some chains) | +22% YoY |

| Driver turnover | >100% annually |

| Cloud/vendor EBITDA impact | −1–3 pts |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Waitr, detailing each Porter’s force with insights on suppliers, buyers, substitutes, new entrants, and intra-industry rivalry to highlight threats and strategic levers.

Compact five-forces snapshot tailored to Waitr—quickly spot competitive pain points and prioritize strategic fixes.

Customers Bargaining Power

Low Switching Costs

High Price Sensitivity

End-users of delivery platforms show high price sensitivity to service fees, delivery charges, and menu markups; NielsenIQ found 62% of US consumers in 2024 said higher fees made them order less often. Even a $1–2 fee rise can cut order volume by ~5–10% in gig-economy apps, so ASAP (Waitr) is constrained from raising fees without risking churn of active users.

Access to Information

Demand for Diversification

By 2025 consumers expect delivery apps to cover meals, groceries, alcohol and retail; global on-demand groceries grew 28% CAGR 2019–24 and reached $150B in 2024, so ASAP risks losing spend to super-apps if it stays meal-only.

Power shifts to buyers who set service scope, forcing ASAP into costly expansions—engineering, logistics, and COGS increases—that can cut margins; adding grocery/retail can raise fulfillment costs 10–25% per order.

- Consumer demand: groceries +28% CAGR (2019–24)

- Market size: $150B on-demand groceries 2024

- Margin pressure: fulfillment costs +10–25%

- Risk: customer migration to super-apps

Influence of Promotions and Discounts

Promotions and loyalty rewards dominate delivery demand; 2024 US food-delivery coupon usage topped 45%, training customers to wait for deals and cutting full-margin sales for Waitr (ASAP).

That shifts pricing power to customers, forcing ASAP to fund discounts that compress take rates—average effective take rates fell ~3–4 percentage points industry-wide in 2023–24.

ASAP must weigh incentive costs versus retention: if promotions drop, orders can fall 10–20%; if they continue, margins stay squeezed.

- Coupon use ~45% (2024, US delivery)

- Industry take-rate drop ~3–4 pp (2023–24)

- Order drop if promos cut: 10–20%

Promo-dependent: Waitr’s take-rates cut 3–4pp as 15% promos fend off 10–20% order loss

| Metric | Value |

|---|---|

| Users with multiple apps (2024) | 68% |

| Compare platforms before ordering (2024) | 78% |

| Order sensitivity to higher fees (2024) | 62% |

| Promo share of order value (2024) | ~15% |

| Take-rate decline (2023–24) | 3–4 pp |

| Order drop if promos cut | 10–20% |

Full Version Awaits

Waitr Porter's Five Forces Analysis

This preview shows the exact Waitr Porter's Five Forces analysis you'll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.

The document displayed here is the same professionally written file included with your order, containing complete competitive insights, force evaluations, and concise implications for strategy and valuation.

You're viewing the final deliverable: instant access to this exact analysis the moment you complete your purchase—ready to use in presentations or decision-making.