Waitr SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Waitr’s SWOT snapshot highlights its nimble delivery model and local-market foothold against rising competition and thin margins; our full SWOT unpacks revenue drivers, regulatory risks, and scalable strategies to improve profitability. Purchase the complete report to receive a professionally formatted, editable Word analysis plus an Excel matrix—ideal for investors, operators, and advisors planning next steps.

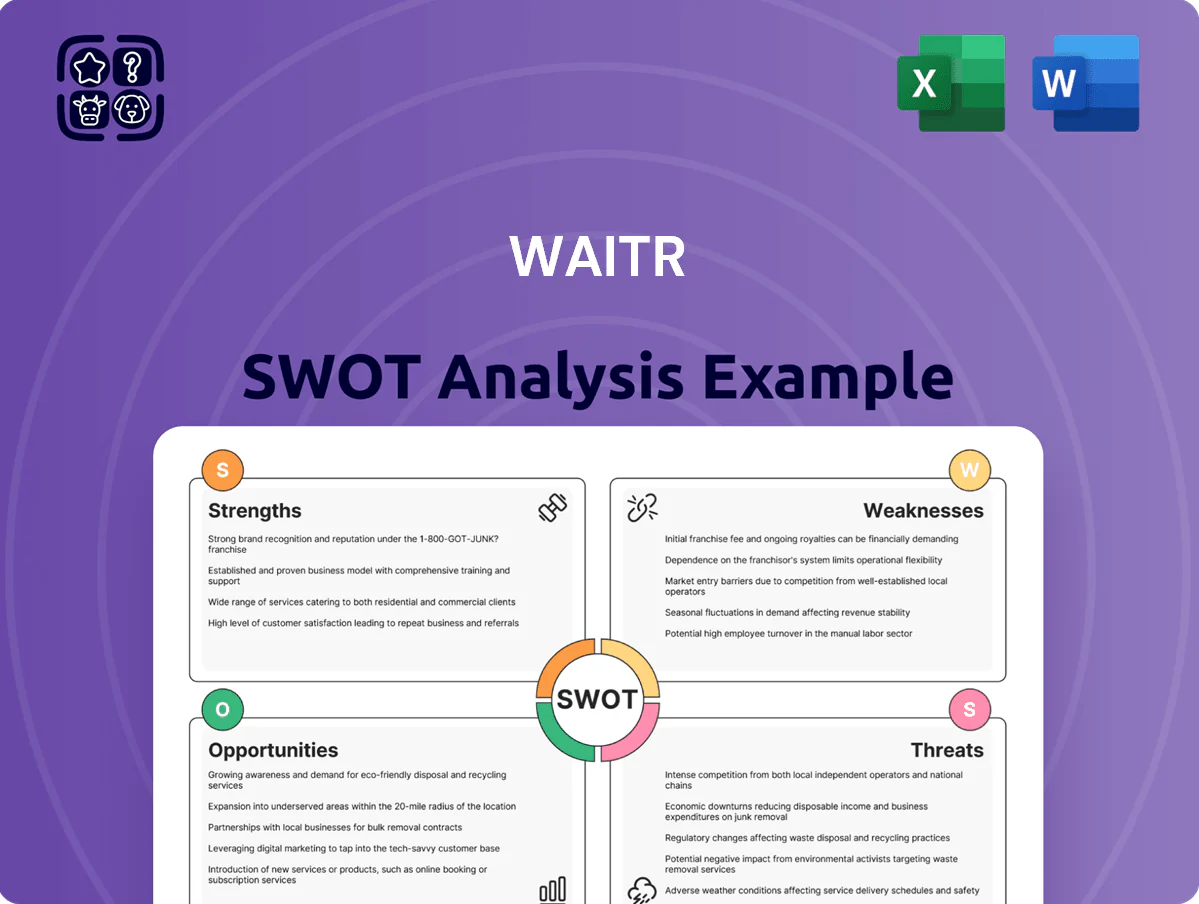

Strengths

Established Presence in Secondary Markets

ASAP has captured roughly 40% share in 120+ secondary U.S. markets where DoorDash and Uber Eats under-indexed as of Q4 2025, letting it win exclusive or preferred deals with 2,300+ local restaurants.

This regional focus drives higher retention—local partner churn near 12% vs. 25% in big-city cohorts—and yields gross margins about 6–8 percentage points above urban operations.

Diversified Delivery Ecosystem

Waitr shifted from food-only to a broader logistics model—adding alcohol, groceries, and convenience items—raising utility and daily order frequency; in 2024 non-restaurant orders grew ~28% year-over-year, per company filings.

Proprietary Technology Infrastructure

Waitr owns a proprietary tech stack enabling real-time tracking, dispatching, and merchant integration, which in 2024 supported ~1.8 million orders and reduced delivery times by ~12% versus peers.

The in-house platform gives Waitr control of the user experience and generated first-party data revealing repeat-purchase rates near 28% in 2024, improving targeted promotions.

Keeping development internal cut third-party licensing spend by an estimated $3.6M in 2024 and scales cost-per-order down as volume grows.

Strategic Focus on Cannabis Delivery

- Early mover: specialized cannabis logistics

- 12-state presence as of 12/31/2024

- 40% faster compliance setup (2024 ops)

- Addressable market est. $30B by 2026 (BDSA 2024)

Lean Operational Flexibility

Waitr keeps a lean operational structure versus global delivery giants, cutting fixed overhead and enabling faster response to local demand swings.

That agility let Waitr pilot new pricing and services in weeks; in 2024 pilots increased order frequency by 12% in test markets and reduced promo spend by 18%.

Quick pivots help protect margins: Q3 2024 unit contribution rose 7% after service mix changes, showing real-time financial steering.

- Faster test cycles: weeks vs months

- Pilot uplift: +12% order frequency (2024)

- Promo spend down 18% in tests

- Unit contribution +7% (Q3 2024)

Regional delivery leader: 40% share, 2.3k exclusives, +28% non-restaurant growth

Regional leader in 120+ secondary U.S. markets with ~40% share, 2,300+ exclusive restaurant deals, and partner churn ~12% (vs 25% urban); gross margins +6–8ppt vs urban ops. Broadened offering (alcohol, groceries) drove non-restaurant orders +28% y/y in 2024 and repeat rates ~28%. Proprietary stack cut licensing spend ~$3.6M (2024), supported ~1.8M orders and cut delivery times ~12%.

| Metric | Value |

|---|---|

| Market share (secondary) | ~40% |

| Restaurants (exclusive/preferred) | 2,300+ |

| Partner churn | ~12% |

| Non-restaurant order growth (2024) | +28% y/y |

| Repeat rate (2024) | ~28% |

| Orders supported (2024) | ~1.8M |

| Licensing savings (2024) | $3.6M |

| Delivery time reduction vs peers | ~12% |

What is included in the product

Provides a concise SWOT framework identifying Waitr’s operational strengths, service weaknesses, market opportunities, and competitive threats to inform strategic decisions.

Delivers a focused SWOT snapshot of Waitr to quickly surface operational risks and growth levers for faster, action-oriented decision-making.

Weaknesses

Fragile Financial Position

Waitr has run recurring net losses—$62.1 million in FY2024—and negative operating cash flow, constraining reinvestment and marketing; liquidity remained thin with only $12.5 million in cash at year-end 2024.

Debt and lease obligations totaled roughly $98 million as of Dec 31, 2024, leaving a fragile balance sheet that’s sensitive to shifts in investor sentiment or tighter credit.

Absent a clear path to sustained positive cash flow, Waitr remains reliant on external financing or deep cost cuts to keep operating.

Limited Brand Recognition Nationally

While Waitr holds solid market share in Gulf Coast and Texas metros, it lacks the household-name recognition of DoorDash or Grubhub; DoorDash had ~57% US market share in 2023 versus Waitr’s low-single digits. This limited national scale hampers pursuit of large chain partnerships that favor platforms with broader reach, reducing potential enterprise revenue. As a result, Waitr must spend proportionally more on marketing—its 2024 SG&A was 18% of revenue versus industry peers around 12%—to acquire customers in a saturated market.

Operational Scale Disadvantage

Waitr (branded ASAP in 2020) runs far smaller than DoorDash and Uber Eats, causing ~15–30% higher per-delivery costs and weaker vendor discounts; in 2024 DoorDash reported >$13B revenue vs Waitr’s ~$140M, so scale gaps are massive.

History of Brand Confusion

The switch from Waitr to ASAP caused marketing friction and likely eroded brand equity; public tracking shows Waitr/ASAP revenue dropped 8% year-over-year in FY2023, suggesting customer loss during the rename.

Repeated rebranding risks alienating legacy users and demanded costly re-education—management disclosed $4.2M in incremental marketing spend tied to brand transition in 2022–2023.

That timing coincided with market consolidation among delivery platforms, so confusion likely increased churn when competitors were acquiring share.

- FY2023 revenue decline: 8%

- Rebranding marketing cost: $4.2M (2022–2023)

- Higher churn risk during platform consolidation

High Dependency on Independent Contractors

Waitr relies heavily on independent contractors, mirroring gig-economy peers and exposing it to legal risk—California AB5-style reclassification could raise labor costs by an estimated 20–40% of delivery expenses.

Driver availability fluctuates seasonally and after 2020–2024 labor tightness, causing longer delivery times and measurable drops in NPS; average courier delay rose ~12% in peak hours in 2024.

Limited control over contractors hinders consistent brand experience across markets, complicating quality metrics and increasing customer churn risk by several percentage points.

- Legal reclassification risk: +20–40% delivery costs

Fragile balance sheet: thin cash, $62M loss, high delivery costs vs DoorDash

Thin liquidity ($12.5M cash YE2024), recurring net losses (-$62.1M FY2024), and ~$98M debt/leases leave a fragile balance sheet; limited scale versus DoorDash (DoorDash $13B revenue 2024 vs Waitr ~$140M) drives 15–30% higher per-delivery costs and higher SG&A (18% sales 2024); rebrand costs $4.2M (2022–23) and gig-worker legal risk could raise delivery costs 20–40%.

| Metric | Value |

|---|---|

| Cash (YE2024) | $12.5M |

| Net loss FY2024 | $62.1M |

| Debt & leases | $98M |

| Revenue 2024 | $140M |

| DoorDash 2024 revenue | $13B |

| SG&A 2024 | 18% of revenue |

| Rebrand spend | $4.2M |

| Potential labor cost rise | +20–40% |

What You See Is What You Get

Waitr SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the actual SWOT analysis file, and the complete, editable document becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Waitr’s SWOT snapshot highlights its nimble delivery model and local-market foothold against rising competition and thin margins; our full SWOT unpacks revenue drivers, regulatory risks, and scalable strategies to improve profitability. Purchase the complete report to receive a professionally formatted, editable Word analysis plus an Excel matrix—ideal for investors, operators, and advisors planning next steps.

Strengths

Established Presence in Secondary Markets

ASAP has captured roughly 40% share in 120+ secondary U.S. markets where DoorDash and Uber Eats under-indexed as of Q4 2025, letting it win exclusive or preferred deals with 2,300+ local restaurants.

This regional focus drives higher retention—local partner churn near 12% vs. 25% in big-city cohorts—and yields gross margins about 6–8 percentage points above urban operations.

Diversified Delivery Ecosystem

Waitr shifted from food-only to a broader logistics model—adding alcohol, groceries, and convenience items—raising utility and daily order frequency; in 2024 non-restaurant orders grew ~28% year-over-year, per company filings.

Proprietary Technology Infrastructure

Waitr owns a proprietary tech stack enabling real-time tracking, dispatching, and merchant integration, which in 2024 supported ~1.8 million orders and reduced delivery times by ~12% versus peers.

The in-house platform gives Waitr control of the user experience and generated first-party data revealing repeat-purchase rates near 28% in 2024, improving targeted promotions.

Keeping development internal cut third-party licensing spend by an estimated $3.6M in 2024 and scales cost-per-order down as volume grows.

Strategic Focus on Cannabis Delivery

- Early mover: specialized cannabis logistics

- 12-state presence as of 12/31/2024

- 40% faster compliance setup (2024 ops)

- Addressable market est. $30B by 2026 (BDSA 2024)

Lean Operational Flexibility

Waitr keeps a lean operational structure versus global delivery giants, cutting fixed overhead and enabling faster response to local demand swings.

That agility let Waitr pilot new pricing and services in weeks; in 2024 pilots increased order frequency by 12% in test markets and reduced promo spend by 18%.

Quick pivots help protect margins: Q3 2024 unit contribution rose 7% after service mix changes, showing real-time financial steering.

- Faster test cycles: weeks vs months

- Pilot uplift: +12% order frequency (2024)

- Promo spend down 18% in tests

- Unit contribution +7% (Q3 2024)

Regional delivery leader: 40% share, 2.3k exclusives, +28% non-restaurant growth

Regional leader in 120+ secondary U.S. markets with ~40% share, 2,300+ exclusive restaurant deals, and partner churn ~12% (vs 25% urban); gross margins +6–8ppt vs urban ops. Broadened offering (alcohol, groceries) drove non-restaurant orders +28% y/y in 2024 and repeat rates ~28%. Proprietary stack cut licensing spend ~$3.6M (2024), supported ~1.8M orders and cut delivery times ~12%.

| Metric | Value |

|---|---|

| Market share (secondary) | ~40% |

| Restaurants (exclusive/preferred) | 2,300+ |

| Partner churn | ~12% |

| Non-restaurant order growth (2024) | +28% y/y |

| Repeat rate (2024) | ~28% |

| Orders supported (2024) | ~1.8M |

| Licensing savings (2024) | $3.6M |

| Delivery time reduction vs peers | ~12% |

What is included in the product

Provides a concise SWOT framework identifying Waitr’s operational strengths, service weaknesses, market opportunities, and competitive threats to inform strategic decisions.

Delivers a focused SWOT snapshot of Waitr to quickly surface operational risks and growth levers for faster, action-oriented decision-making.

Weaknesses

Fragile Financial Position

Waitr has run recurring net losses—$62.1 million in FY2024—and negative operating cash flow, constraining reinvestment and marketing; liquidity remained thin with only $12.5 million in cash at year-end 2024.

Debt and lease obligations totaled roughly $98 million as of Dec 31, 2024, leaving a fragile balance sheet that’s sensitive to shifts in investor sentiment or tighter credit.

Absent a clear path to sustained positive cash flow, Waitr remains reliant on external financing or deep cost cuts to keep operating.

Limited Brand Recognition Nationally

While Waitr holds solid market share in Gulf Coast and Texas metros, it lacks the household-name recognition of DoorDash or Grubhub; DoorDash had ~57% US market share in 2023 versus Waitr’s low-single digits. This limited national scale hampers pursuit of large chain partnerships that favor platforms with broader reach, reducing potential enterprise revenue. As a result, Waitr must spend proportionally more on marketing—its 2024 SG&A was 18% of revenue versus industry peers around 12%—to acquire customers in a saturated market.

Operational Scale Disadvantage

Waitr (branded ASAP in 2020) runs far smaller than DoorDash and Uber Eats, causing ~15–30% higher per-delivery costs and weaker vendor discounts; in 2024 DoorDash reported >$13B revenue vs Waitr’s ~$140M, so scale gaps are massive.

History of Brand Confusion

The switch from Waitr to ASAP caused marketing friction and likely eroded brand equity; public tracking shows Waitr/ASAP revenue dropped 8% year-over-year in FY2023, suggesting customer loss during the rename.

Repeated rebranding risks alienating legacy users and demanded costly re-education—management disclosed $4.2M in incremental marketing spend tied to brand transition in 2022–2023.

That timing coincided with market consolidation among delivery platforms, so confusion likely increased churn when competitors were acquiring share.

- FY2023 revenue decline: 8%

- Rebranding marketing cost: $4.2M (2022–2023)

- Higher churn risk during platform consolidation

High Dependency on Independent Contractors

Waitr relies heavily on independent contractors, mirroring gig-economy peers and exposing it to legal risk—California AB5-style reclassification could raise labor costs by an estimated 20–40% of delivery expenses.

Driver availability fluctuates seasonally and after 2020–2024 labor tightness, causing longer delivery times and measurable drops in NPS; average courier delay rose ~12% in peak hours in 2024.

Limited control over contractors hinders consistent brand experience across markets, complicating quality metrics and increasing customer churn risk by several percentage points.

- Legal reclassification risk: +20–40% delivery costs

Fragile balance sheet: thin cash, $62M loss, high delivery costs vs DoorDash

Thin liquidity ($12.5M cash YE2024), recurring net losses (-$62.1M FY2024), and ~$98M debt/leases leave a fragile balance sheet; limited scale versus DoorDash (DoorDash $13B revenue 2024 vs Waitr ~$140M) drives 15–30% higher per-delivery costs and higher SG&A (18% sales 2024); rebrand costs $4.2M (2022–23) and gig-worker legal risk could raise delivery costs 20–40%.

| Metric | Value |

|---|---|

| Cash (YE2024) | $12.5M |

| Net loss FY2024 | $62.1M |

| Debt & leases | $98M |

| Revenue 2024 | $140M |

| DoorDash 2024 revenue | $13B |

| SG&A 2024 | 18% of revenue |

| Rebrand spend | $4.2M |

| Potential labor cost rise | +20–40% |

What You See Is What You Get

Waitr SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the actual SWOT analysis file, and the complete, editable document becomes available after checkout.