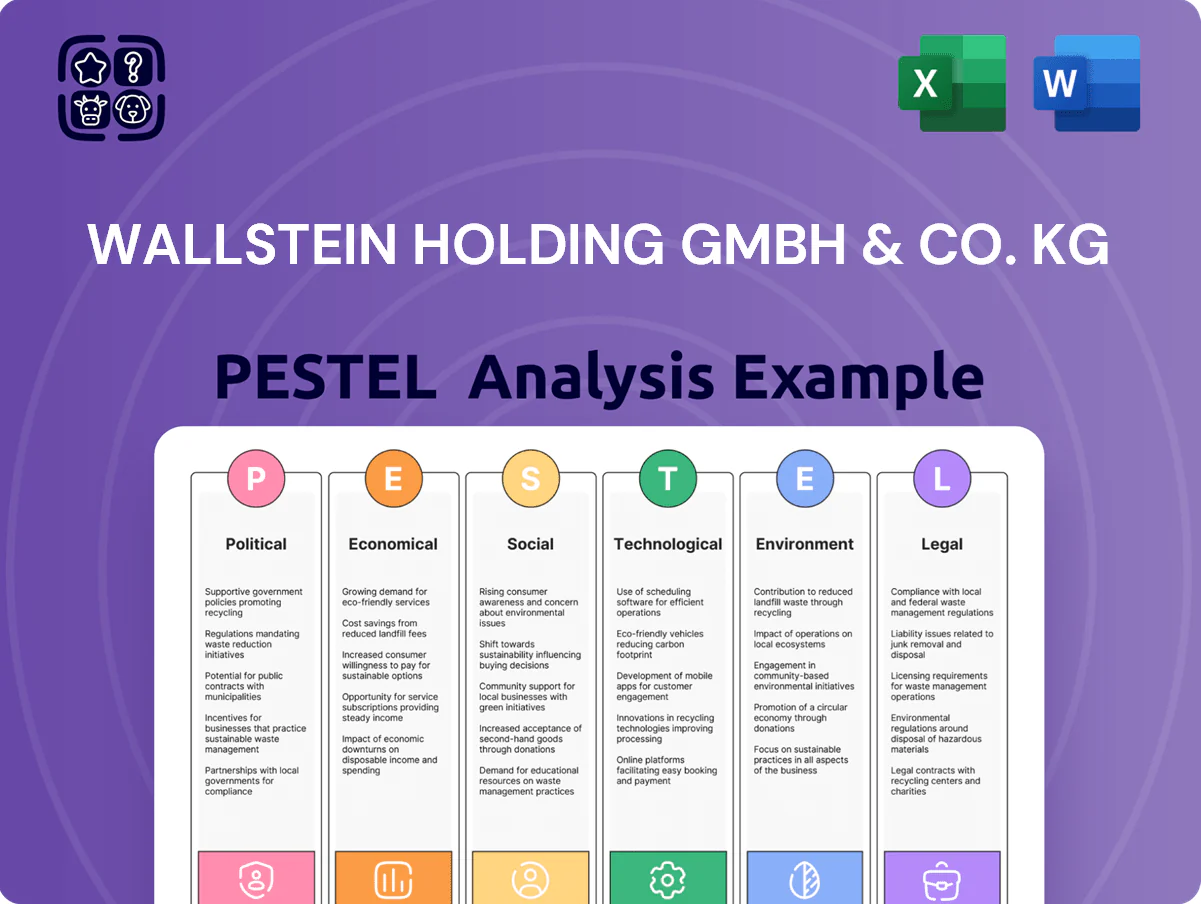

Wallstein Holding GmbH & Co. KG PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Wallstein Holding GmbH & Co. KG—pinpoint political, economic, social, technological, legal, and environmental forces shaping its trajectory and prepare smarter moves. Ideal for investors, consultants, and executives, this concise briefing highlights risks and opportunities you won’t want to miss. Purchase the full report for the complete, actionable breakdown ready for immediate use.

Political factors

EU Green Deal Implementation

The EU Fit for 55 package tightens 2030 CO2 targets, driving demand for Wallstein’s flue gas cleaning and heat recovery systems; EU industrial emissions must fall ~55% vs 1990, pushing retrofit spending—EU estimates €400–500bn industrial green investments by 2030.

As of late 2025, orders for emission control grew ~18% YoY for companies like Wallstein, with flue gas and heat-recovery retrofit contracts averaging €1.2–3.5m each, boosting revenue visibility.

Political mandates and stricter permitting accelerate modernization cycles, positioning Wallstein to capture mandated upgrades as EU Member States enforce Fit for 55 compliance to meet 2030 benchmarks.

Energy Security and Sovereignty

Subsidies for Industrial Decarbonization

German and EU programs like Germanys KfW Energiewende loans and the EU ETS Innovation Fund, which allocated about €25.8 billion through 2024 for decarbonization, lower capex barriers for green tech adoption.

Wallstein heat exchangers—reducing primary energy use by up to 20–30% in industrial applications—frequently qualify for grants, tax credits and accelerated depreciation schemes.

Such sovereign support lifted industrial energy-efficiency investment: German industry investment in climate tech grew ~12% y/y in 2023–24, sustaining Wallsteins order pipeline despite macro volatility.

Geopolitical Supply Chain Stability

The current geopolitical climate keeps supply-chain costs volatile; 2024 EU tariffs and trade measures raised stainless alloy import costs by ~6-9%, directly affecting Wallstein’s margins on corrosion-resistant components.

Dependency on high-performance plastics sourced from Asia exposes Wallstein to shipping delays and 2023–24 container rate swings (peak freight volatility ±40%), impacting project timelines in power generation exports.

Political stability in non-EU markets—notably Turkey and North Africa, which comprised ~12% of EU heavy-equipment imports in 2024—shapes expansion risk and contract viability for Wallstein.

- Tariff-driven material cost increases ~6–9%

- Freight volatility ±40% through 2023–24

- Non-EU market exposure ~12% of relevant imports

Stricter National Emission Standards

National governments increasingly adopt emission limits stricter than international minima to tackle local air quality; 2024 EU proposals target a 55% NOx reduction for power plants by 2030 versus 1990 levels, raising compliance demand.

Wallstein offers sulfur and NOx abatement systems and is positioned to capture rising retrofit and new-install markets as countries tighten standards.

Revenue growth hinges on political enforcement: stronger laws in key markets (EU, China, India) could lift sector demand by an estimated 10–20% CAGR through 2028.

- Stricter national limits (e.g., EU 55% NOx cut by 2030)

- Wallstein = compliance solutions for SOx/NOx

- Growth tied to enforcement; potential 10–20% sector CAGR to 2028

EU Fit-for-55 Spurs €400–500bn Green Industrial Retrofit Wave; Emission Orders +18%

EU Fit for 55 and stricter national limits (e.g., 55% NOx cut by 2030) drive retrofit demand; EU industrial green investments estimated €400–500bn by 2030 and orders for emission control rose ~18% YoY to late 2025. Germany 2025 energy-security budget €15bn; EU renewables/efficiency funding €210bn in 2024; tariffs raised alloy costs ~6–9%, freight volatility ±40%.

| Metric | Value |

|---|---|

| EU industrial green invest (by 2030) | €400–500bn |

| Emission-control order growth (2025 YoY) | ~18% |

| Germany 2025 energy budget | €15bn |

| EU 2024 renewables/efficiency | €210bn |

| Alloy tariff impact | +6–9% |

| Freight volatility (2023–24) | ±40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Wallstein Holding GmbH & Co. KG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to its region and industry to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise PESTLE snapshot for Wallstein Holding GmbH & Co. KG that clarifies external risks and opportunities for swift decision-making in meetings or presentations, easily customizable with team notes and exportable for slides or strategy packs.

Economic factors

Energy Price Volatility

Fluctuating natural gas and electricity prices—European wholesale gas up ~50% in 2024 vs 2020 and EU industrial power prices averaging €120/MWh in 2024—drive demand for Wallstein’s heat recovery systems as firms seek to curb fuel spend. High energy costs shorten typical payback from 4–7 years toward 2–3 years, boosting ROI for efficiency upgrades. Reduced operational overhead preserves margins for industrial clients, making Wallstein’s value proposition more compelling amid price volatility.

Capital Expenditure Interest Rates

As of late 2025, elevated borrowing costs—with average Eurozone corporate lending rates around 4.5–5.5% and project finance spreads commonly adding 200–400 bps—continue to constrain large power and waste infrastructure projects, prompting deferrals of major overhauls where Wallstein systems would integrate.

Global Industrial Production Trends

Wallstein’s revenues closely track global manufacturing: world industrial production grew 2.1% in 2024 after a 0.5% decline in 2023, with chemicals up 3.4% and pharmaceuticals 4.1%, boosting demand for thermal management and flue gas systems.

A 2025 IMF baseline projecting 3.2% global GDP growth suggests continued investment, but a 1–2% output contraction in EU heavy industry would shift demand from new installations to service and maintenance.

Inflationary Pressure on Specialized Materials

Inflation in specialized fluoroplastics and high-grade metals raised Wallstein’s input costs by an estimated 6–9% in 2024, compressing manufacturing margins for custom engineering components.

Persistent supply‑chain inflation forces use of advanced procurement (long‑term contracts, hedging) and dynamic pricing to protect margins while meeting global demand.

Effective input‑cost management is critical to sustain profitability on complex, high‑margin projects.

- 2024 raw‑material inflation: 6–9%

- Mitigations: long‑term contracts, hedging, tiered pricing

- Impact: margin pressure on customized engineering sales

Growth of the Circular Economy

The global waste-to-energy market was valued at about USD 33.8 billion in 2024 and is projected to reach ~USD 44.5 billion by 2030 (CAGR ~4.8%), supporting strong demand for Wallstein’s flue gas cleaning and heat exchanger systems.

Higher landfill taxes and EU Landfill Directive enforcement have pushed EU diversion rates above 60% in 2024, prompting municipal and industrial investment in incineration and energy recovery technologies that align with Wallstein’s offerings.

The shift reduces long-term disposal costs and creates recurring revenue opportunities for Wallstein through equipment sales, service contracts, and retrofit projects across Europe’s expanding WtE fleet.

- 2024 market size USD 33.8bn; 2030 forecast USD 44.5bn (CAGR ~4.8%)

High EU power, inflation and lending reshape WtE—shorter paybacks, retrofit demand

High 2024 energy prices (EU power ≈ €120/MWh) and 2024 raw‑material inflation (6–9%) shortened paybacks to 2–3 years and pressured margins; Eurozone corporate lending ~4.5–5.5% in late 2025 constrained large projects, shifting demand to retrofits and services; global WtE market USD 33.8bn (2024), CAGR ~4.8% to USD 44.5bn (2030); IMF 2025 global GDP baseline +3.2%.

| Metric | 2024/2025 |

|---|---|

| EU industrial power | €120/MWh (2024) |

| Raw‑material inflation | 6–9% (2024) |

| Eurozone lending | 4.5–5.5% (late 2025) |

| WtE market | USD 33.8bn (2024); USD 44.5bn (2030) |

| Global GDP forecast | +3.2% (IMF 2025) |

Preview Before You Purchase

Wallstein Holding GmbH & Co. KG PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Wallstein Holding GmbH & Co. KG you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Wallstein Holding GmbH & Co. KG—pinpoint political, economic, social, technological, legal, and environmental forces shaping its trajectory and prepare smarter moves. Ideal for investors, consultants, and executives, this concise briefing highlights risks and opportunities you won’t want to miss. Purchase the full report for the complete, actionable breakdown ready for immediate use.

Political factors

EU Green Deal Implementation

The EU Fit for 55 package tightens 2030 CO2 targets, driving demand for Wallstein’s flue gas cleaning and heat recovery systems; EU industrial emissions must fall ~55% vs 1990, pushing retrofit spending—EU estimates €400–500bn industrial green investments by 2030.

As of late 2025, orders for emission control grew ~18% YoY for companies like Wallstein, with flue gas and heat-recovery retrofit contracts averaging €1.2–3.5m each, boosting revenue visibility.

Political mandates and stricter permitting accelerate modernization cycles, positioning Wallstein to capture mandated upgrades as EU Member States enforce Fit for 55 compliance to meet 2030 benchmarks.

Energy Security and Sovereignty

Subsidies for Industrial Decarbonization

German and EU programs like Germanys KfW Energiewende loans and the EU ETS Innovation Fund, which allocated about €25.8 billion through 2024 for decarbonization, lower capex barriers for green tech adoption.

Wallstein heat exchangers—reducing primary energy use by up to 20–30% in industrial applications—frequently qualify for grants, tax credits and accelerated depreciation schemes.

Such sovereign support lifted industrial energy-efficiency investment: German industry investment in climate tech grew ~12% y/y in 2023–24, sustaining Wallsteins order pipeline despite macro volatility.

Geopolitical Supply Chain Stability

The current geopolitical climate keeps supply-chain costs volatile; 2024 EU tariffs and trade measures raised stainless alloy import costs by ~6-9%, directly affecting Wallstein’s margins on corrosion-resistant components.

Dependency on high-performance plastics sourced from Asia exposes Wallstein to shipping delays and 2023–24 container rate swings (peak freight volatility ±40%), impacting project timelines in power generation exports.

Political stability in non-EU markets—notably Turkey and North Africa, which comprised ~12% of EU heavy-equipment imports in 2024—shapes expansion risk and contract viability for Wallstein.

- Tariff-driven material cost increases ~6–9%

- Freight volatility ±40% through 2023–24

- Non-EU market exposure ~12% of relevant imports

Stricter National Emission Standards

National governments increasingly adopt emission limits stricter than international minima to tackle local air quality; 2024 EU proposals target a 55% NOx reduction for power plants by 2030 versus 1990 levels, raising compliance demand.

Wallstein offers sulfur and NOx abatement systems and is positioned to capture rising retrofit and new-install markets as countries tighten standards.

Revenue growth hinges on political enforcement: stronger laws in key markets (EU, China, India) could lift sector demand by an estimated 10–20% CAGR through 2028.

- Stricter national limits (e.g., EU 55% NOx cut by 2030)

- Wallstein = compliance solutions for SOx/NOx

- Growth tied to enforcement; potential 10–20% sector CAGR to 2028

EU Fit-for-55 Spurs €400–500bn Green Industrial Retrofit Wave; Emission Orders +18%

EU Fit for 55 and stricter national limits (e.g., 55% NOx cut by 2030) drive retrofit demand; EU industrial green investments estimated €400–500bn by 2030 and orders for emission control rose ~18% YoY to late 2025. Germany 2025 energy-security budget €15bn; EU renewables/efficiency funding €210bn in 2024; tariffs raised alloy costs ~6–9%, freight volatility ±40%.

| Metric | Value |

|---|---|

| EU industrial green invest (by 2030) | €400–500bn |

| Emission-control order growth (2025 YoY) | ~18% |

| Germany 2025 energy budget | €15bn |

| EU 2024 renewables/efficiency | €210bn |

| Alloy tariff impact | +6–9% |

| Freight volatility (2023–24) | ±40% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Wallstein Holding GmbH & Co. KG across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored to its region and industry to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise PESTLE snapshot for Wallstein Holding GmbH & Co. KG that clarifies external risks and opportunities for swift decision-making in meetings or presentations, easily customizable with team notes and exportable for slides or strategy packs.

Economic factors

Energy Price Volatility

Fluctuating natural gas and electricity prices—European wholesale gas up ~50% in 2024 vs 2020 and EU industrial power prices averaging €120/MWh in 2024—drive demand for Wallstein’s heat recovery systems as firms seek to curb fuel spend. High energy costs shorten typical payback from 4–7 years toward 2–3 years, boosting ROI for efficiency upgrades. Reduced operational overhead preserves margins for industrial clients, making Wallstein’s value proposition more compelling amid price volatility.

Capital Expenditure Interest Rates

As of late 2025, elevated borrowing costs—with average Eurozone corporate lending rates around 4.5–5.5% and project finance spreads commonly adding 200–400 bps—continue to constrain large power and waste infrastructure projects, prompting deferrals of major overhauls where Wallstein systems would integrate.

Global Industrial Production Trends

Wallstein’s revenues closely track global manufacturing: world industrial production grew 2.1% in 2024 after a 0.5% decline in 2023, with chemicals up 3.4% and pharmaceuticals 4.1%, boosting demand for thermal management and flue gas systems.

A 2025 IMF baseline projecting 3.2% global GDP growth suggests continued investment, but a 1–2% output contraction in EU heavy industry would shift demand from new installations to service and maintenance.

Inflationary Pressure on Specialized Materials

Inflation in specialized fluoroplastics and high-grade metals raised Wallstein’s input costs by an estimated 6–9% in 2024, compressing manufacturing margins for custom engineering components.

Persistent supply‑chain inflation forces use of advanced procurement (long‑term contracts, hedging) and dynamic pricing to protect margins while meeting global demand.

Effective input‑cost management is critical to sustain profitability on complex, high‑margin projects.

- 2024 raw‑material inflation: 6–9%

- Mitigations: long‑term contracts, hedging, tiered pricing

- Impact: margin pressure on customized engineering sales

Growth of the Circular Economy

The global waste-to-energy market was valued at about USD 33.8 billion in 2024 and is projected to reach ~USD 44.5 billion by 2030 (CAGR ~4.8%), supporting strong demand for Wallstein’s flue gas cleaning and heat exchanger systems.

Higher landfill taxes and EU Landfill Directive enforcement have pushed EU diversion rates above 60% in 2024, prompting municipal and industrial investment in incineration and energy recovery technologies that align with Wallstein’s offerings.

The shift reduces long-term disposal costs and creates recurring revenue opportunities for Wallstein through equipment sales, service contracts, and retrofit projects across Europe’s expanding WtE fleet.

- 2024 market size USD 33.8bn; 2030 forecast USD 44.5bn (CAGR ~4.8%)

High EU power, inflation and lending reshape WtE—shorter paybacks, retrofit demand

High 2024 energy prices (EU power ≈ €120/MWh) and 2024 raw‑material inflation (6–9%) shortened paybacks to 2–3 years and pressured margins; Eurozone corporate lending ~4.5–5.5% in late 2025 constrained large projects, shifting demand to retrofits and services; global WtE market USD 33.8bn (2024), CAGR ~4.8% to USD 44.5bn (2030); IMF 2025 global GDP baseline +3.2%.

| Metric | 2024/2025 |

|---|---|

| EU industrial power | €120/MWh (2024) |

| Raw‑material inflation | 6–9% (2024) |

| Eurozone lending | 4.5–5.5% (late 2025) |

| WtE market | USD 33.8bn (2024); USD 44.5bn (2030) |

| Global GDP forecast | +3.2% (IMF 2025) |

Preview Before You Purchase

Wallstein Holding GmbH & Co. KG PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Wallstein Holding GmbH & Co. KG you’ll receive after purchase—fully formatted, professionally structured, and ready to use.