Dalian Wanda Group Co Ltd. Boston Consulting Group Matrix

Actionable Strategy Starts Here

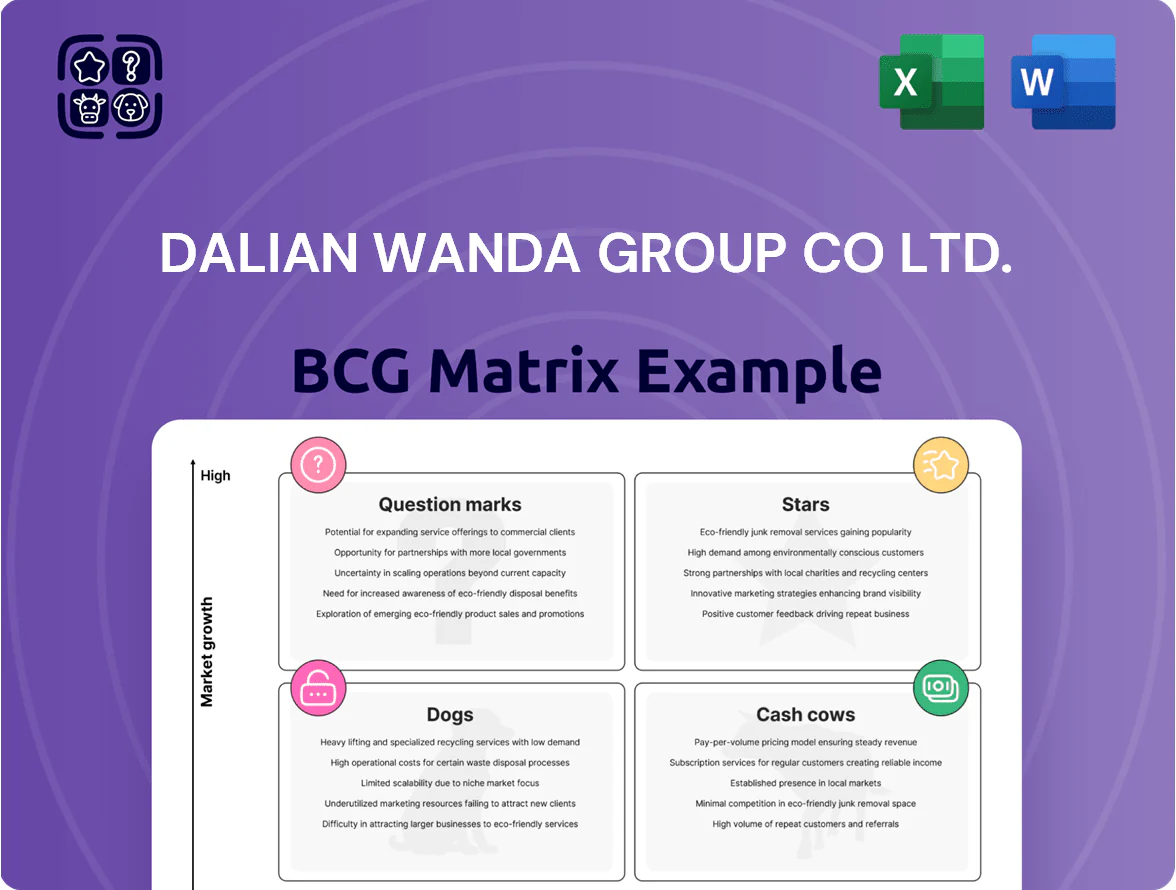

Dalian Wanda Group’s sprawling portfolio spans commercial real estate, cinema chains, tourism and cultural industries, creating a mix of Cash Cows and potential Question Marks amid regulatory and macro pressures; select segments (e.g., cinema exhibition) behave like Stars in recovering markets, while heavy property assets risk Dog-like drain without strategic recapitalization. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Wanda Film and Media Production

Wanda Film and Media Production, part of Dalian Wanda Group Co Ltd, holds a leading share of China’s box office—about 18% of 2024 domestic gross—via integrated production and distribution, making it a Star in the BCG Matrix.

With China’s box office recovering to RMB 55.8 billion in 2024 and premium domestic titles rising, continuous capital spend is needed to compete with tech-backed rivals like ByteDance and Tencent.

By end-2025, Wanda’s IP integration across 140+ cinemas and 10 theme parks boosts cross-selling and revenue growth, cementing its high-growth leader status as middle-class discretionary spend climbs.

Luxury Hotel Management

The premium hospitality segment has rebounded, with China high-end domestic travel up 28% in 2024 versus 2019; Wanda’s luxury hotels hold top-three market share in most tier-one and select tier-two cities, boosting brand strength.

These assets are capital-intensive but deliver high RevPAR—Wanda reported RMB 1,350 RevPAR in 2024 for luxury properties, 22% above group average—so they qualify as Stars in the BCG matrix.

Wanda is investing in 2025 on digital guest experiences and sustainable luxury branding, allocating RMB 1.2 billion to tech and ESG initiatives to defend against international chains and capture growing domestic demand.

Cultural Tourism Cities

Wanda’s Cultural Tourism Cities combine theme parks, malls, and hotels, tapping the fast-growing experiential economy; Wuhan Movie Park and Qingdao Wanda City drove 2024-25 visitor growth, with group tourism revenues up ~18% YoY to RMB 42.3bn in 2025.

These integrated destinations directly compete with Disney and Universal, targeting domestic leisure spend that peaked in Q4 2025; capex is heavy—Wanda allocated RMB 25bn for expansion in 2025—yet they offer highest long-term dominance potential.

Digital Retail Ecosystems

Digital Retail Ecosystems at Dalian Wanda Group Co Ltd rank as a star: AI and big data in Wanda Plaza yield high-growth smart retail management, driving targeted marketing and ops analytics from ~1.2 billion annual plaza visits (2024) and boosting tenant sales by ~8–12% per deployment.

Rapid roll-out across 300+ plazas shows strong market share; still needs ongoing R&D—Wanda spent ~RMB 600m on tech in 2024—to keep its edge and modernize brick-and-mortar commerce.

- 1.2B annual visits (2024)

- 300+ plazas deployed

- Tenant sales +8–12% post-deployment

- RMB 600m tech spend (2024)

- High growth, needs continual R&D

Premium Cinema Circuits

Wanda Cinema Line leads China with about 9,000 screens and ~1.2 billion USD box office in 2024, dominating IMAX/high-end segments where premium large-format screens grew ~18% vs 6% for standard screens in 2023–24; blockbusters now drive ~65% of its ticket revenue, pushing reinvestment into laser projection and 4D tech to sustain premium pricing.

- ~9,000 screens, 2024

- ~1.2B USD box office, 2024

- Premium LFF growth ~18% (2023–24)

- Blockbusters = ~65% ticket revenue

- Capex focus: laser projection, 4D

Wanda’s Stars Drive RMB 42.3bn Tourism, RMB 9bn Box Office and 1.2bn Plaza Visits

Wanda’s high-growth entertainment, cultural tourism, luxury hotels, and smart retail units are Stars: they led China box office (~RMB 9.0bn/US$1.2bn, 2024), drove group tourism revenues to RMB 42.3bn (2025), luxury RevPAR RMB 1,350 (2024), and 1.2bn plaza visits (2024), backed by RMB 25bn capex and RMB 1.8bn tech/ESG spend (2024–25).

| Metric | Value |

|---|---|

| Box office (Wanda Film) | RMB 9.0bn (2024) |

| Tourism rev | RMB 42.3bn (2025) |

| Luxury RevPAR | RMB 1,350 (2024) |

| Plaza visits | 1.2bn (2024) |

| Capex | RMB 25bn (2025) |

| Tech/ESG spend | RMB 1.8bn (2024–25) |

What is included in the product

Comprehensive BCG Matrix of Dalian Wanda: identifies Stars (commercial real estate redevelopment, entertainment), Cash Cows (property management), Question Marks (overseas cinema/assets), Dogs (noncore legacy businesses) with invest/hold/divest guidance and trend context.

One-page BCG matrix placing Dalian Wanda units into quadrants for quick strategic clarity and executive decision-making.

Cash Cows

Asset-Light Wanda Plazas

The asset-light Wanda Plazas business has become a top cash cow for Dalian Wanda Group Co Ltd, delivering high market share and strong margins after shifting to management contracts; in 2025 management fees contributed about CNY 8.4 billion (≈USD 1.2 billion), up 18% year-on-year.

By operating plazas owned by third parties, Wanda avoids heavy real-estate debt, earning stable recurring fees and EBITDA margins near 35%, while the Wanda brand secures anchor tenants and steady foot traffic.

In fiscal 2025 these plazas supplied core liquidity—≈CNY 6.1 billion free cash flow—funding the group’s riskier investments and capex without new property borrowing.

Commercial Property Leasing

Wanda Plazas in prime Chinese cities generate steady rental income: in 2024 Dalian Wanda’s commercial leasing reported occupancy >92% and rental revenue ~RMB 12.4 billion, making these mature assets the group’s financial bedrock.

With top-tier mall markets largely saturated, growth is low but market share stays high, so cash flows are predictable and require little new marketing spend.

Wanda uses this steady income to service corporate debt—net debt reduced 6% in 2024—and to fund newer business units and selective redevelopments.

Domestic Film Distribution

Wanda’s Domestic Film Distribution is a mature market leader, handling ~45% of China’s nationwide releases in 2024 and routing films to 2,000+ cities via its network of 20 regional hubs, giving it strong control of the theatrical window.

With fully developed infrastructure, this unit posts high margins—estimated operating margin ~28% in 2024—and low incremental costs, so it generates steady free cash flow with minimal capex through 2025.

Property Management Services

Property Management Services at Dalian Wanda are a cash cow: standardized facility, security, and FM services across ~1,200 Wanda commercial properties deliver high market share and low growth, generating recurring revenue from long-term contracts—estimated RMB 6.4 billion in 2024 service revenue and mid-20s operating margins.

This unit stabilizes operations, ensures uptime for malls and hotels, and converts scale into predictable cash flow with renewal rates above 85% in 2024.

- ~1,200 properties managed (2024)

- RMB 6.4 billion service revenue (2024)

- Mid-20s operating margin (2024)

- >85% contract renewal rate (2024)

Wanda Brand Licensing

The Wanda brand licensing unit leverages Dalian Wanda Group’s decades of commercial success to command high market share in China’s real-estate branding sector, generating recurring royalties with minimal overhead; in 2024 brand-related fees and franchising contributed an estimated RMB 1.2–1.5 billion to group revenues, making it a classic BCG Cash Cow.

In a mature market where developers pay premium to use Wanda for project viability, the unit converts stored brand equity into pure profit, supporting group cash flow and funding riskier segments like cultural tourism and cinemas; licensing margins exceed 80% per industry reports in 2023–24.

- RMB 1.2–1.5bn estimated 2024 revenue from licensing

- >80% estimated operating margin

- High market share in commercial real-estate branding

- Low incremental cost, steady cash generation

Wanda’s high‑margin cash engines fund debt cut and growth

Wanda’s cash cows—Wanda Plazas (management fees CNY 8.4bn, FCF CNY 6.1bn 2025), Domestic Film Distribution (≈45% market share 2024, ~28% op margin), Property Management (1,200 properties, CNY 6.4bn revenue 2024, mid-20s margin) and Brand Licensing (CNY 1.2–1.5bn 2024, >80% margin)—generate steady high-margin cash to cut net debt and fund growth.

| Unit | Key 2024–25 |

|---|---|

| Wanda Plazas | Fees CNY 8.4bn; FCF CNY 6.1bn (2025) |

| Film | 45% share; 28% margin (2024) |

| Prop Mgmt | 1,200 props; CNY 6.4bn (2024) |

| Brand | CNY 1.2–1.5bn; >80% margin (2024) |

Preview = Final Product

Dalian Wanda Group Co Ltd. BCG Matrix

The file you're previewing is the final Dalian Wanda Group Co Ltd BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a polished, analysis-ready report tailored for strategic planning and investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Dalian Wanda Group’s sprawling portfolio spans commercial real estate, cinema chains, tourism and cultural industries, creating a mix of Cash Cows and potential Question Marks amid regulatory and macro pressures; select segments (e.g., cinema exhibition) behave like Stars in recovering markets, while heavy property assets risk Dog-like drain without strategic recapitalization. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Wanda Film and Media Production

Wanda Film and Media Production, part of Dalian Wanda Group Co Ltd, holds a leading share of China’s box office—about 18% of 2024 domestic gross—via integrated production and distribution, making it a Star in the BCG Matrix.

With China’s box office recovering to RMB 55.8 billion in 2024 and premium domestic titles rising, continuous capital spend is needed to compete with tech-backed rivals like ByteDance and Tencent.

By end-2025, Wanda’s IP integration across 140+ cinemas and 10 theme parks boosts cross-selling and revenue growth, cementing its high-growth leader status as middle-class discretionary spend climbs.

Luxury Hotel Management

The premium hospitality segment has rebounded, with China high-end domestic travel up 28% in 2024 versus 2019; Wanda’s luxury hotels hold top-three market share in most tier-one and select tier-two cities, boosting brand strength.

These assets are capital-intensive but deliver high RevPAR—Wanda reported RMB 1,350 RevPAR in 2024 for luxury properties, 22% above group average—so they qualify as Stars in the BCG matrix.

Wanda is investing in 2025 on digital guest experiences and sustainable luxury branding, allocating RMB 1.2 billion to tech and ESG initiatives to defend against international chains and capture growing domestic demand.

Cultural Tourism Cities

Wanda’s Cultural Tourism Cities combine theme parks, malls, and hotels, tapping the fast-growing experiential economy; Wuhan Movie Park and Qingdao Wanda City drove 2024-25 visitor growth, with group tourism revenues up ~18% YoY to RMB 42.3bn in 2025.

These integrated destinations directly compete with Disney and Universal, targeting domestic leisure spend that peaked in Q4 2025; capex is heavy—Wanda allocated RMB 25bn for expansion in 2025—yet they offer highest long-term dominance potential.

Digital Retail Ecosystems

Digital Retail Ecosystems at Dalian Wanda Group Co Ltd rank as a star: AI and big data in Wanda Plaza yield high-growth smart retail management, driving targeted marketing and ops analytics from ~1.2 billion annual plaza visits (2024) and boosting tenant sales by ~8–12% per deployment.

Rapid roll-out across 300+ plazas shows strong market share; still needs ongoing R&D—Wanda spent ~RMB 600m on tech in 2024—to keep its edge and modernize brick-and-mortar commerce.

- 1.2B annual visits (2024)

- 300+ plazas deployed

- Tenant sales +8–12% post-deployment

- RMB 600m tech spend (2024)

- High growth, needs continual R&D

Premium Cinema Circuits

Wanda Cinema Line leads China with about 9,000 screens and ~1.2 billion USD box office in 2024, dominating IMAX/high-end segments where premium large-format screens grew ~18% vs 6% for standard screens in 2023–24; blockbusters now drive ~65% of its ticket revenue, pushing reinvestment into laser projection and 4D tech to sustain premium pricing.

- ~9,000 screens, 2024

- ~1.2B USD box office, 2024

- Premium LFF growth ~18% (2023–24)

- Blockbusters = ~65% ticket revenue

- Capex focus: laser projection, 4D

Wanda’s Stars Drive RMB 42.3bn Tourism, RMB 9bn Box Office and 1.2bn Plaza Visits

Wanda’s high-growth entertainment, cultural tourism, luxury hotels, and smart retail units are Stars: they led China box office (~RMB 9.0bn/US$1.2bn, 2024), drove group tourism revenues to RMB 42.3bn (2025), luxury RevPAR RMB 1,350 (2024), and 1.2bn plaza visits (2024), backed by RMB 25bn capex and RMB 1.8bn tech/ESG spend (2024–25).

| Metric | Value |

|---|---|

| Box office (Wanda Film) | RMB 9.0bn (2024) |

| Tourism rev | RMB 42.3bn (2025) |

| Luxury RevPAR | RMB 1,350 (2024) |

| Plaza visits | 1.2bn (2024) |

| Capex | RMB 25bn (2025) |

| Tech/ESG spend | RMB 1.8bn (2024–25) |

What is included in the product

Comprehensive BCG Matrix of Dalian Wanda: identifies Stars (commercial real estate redevelopment, entertainment), Cash Cows (property management), Question Marks (overseas cinema/assets), Dogs (noncore legacy businesses) with invest/hold/divest guidance and trend context.

One-page BCG matrix placing Dalian Wanda units into quadrants for quick strategic clarity and executive decision-making.

Cash Cows

Asset-Light Wanda Plazas

The asset-light Wanda Plazas business has become a top cash cow for Dalian Wanda Group Co Ltd, delivering high market share and strong margins after shifting to management contracts; in 2025 management fees contributed about CNY 8.4 billion (≈USD 1.2 billion), up 18% year-on-year.

By operating plazas owned by third parties, Wanda avoids heavy real-estate debt, earning stable recurring fees and EBITDA margins near 35%, while the Wanda brand secures anchor tenants and steady foot traffic.

In fiscal 2025 these plazas supplied core liquidity—≈CNY 6.1 billion free cash flow—funding the group’s riskier investments and capex without new property borrowing.

Commercial Property Leasing

Wanda Plazas in prime Chinese cities generate steady rental income: in 2024 Dalian Wanda’s commercial leasing reported occupancy >92% and rental revenue ~RMB 12.4 billion, making these mature assets the group’s financial bedrock.

With top-tier mall markets largely saturated, growth is low but market share stays high, so cash flows are predictable and require little new marketing spend.

Wanda uses this steady income to service corporate debt—net debt reduced 6% in 2024—and to fund newer business units and selective redevelopments.

Domestic Film Distribution

Wanda’s Domestic Film Distribution is a mature market leader, handling ~45% of China’s nationwide releases in 2024 and routing films to 2,000+ cities via its network of 20 regional hubs, giving it strong control of the theatrical window.

With fully developed infrastructure, this unit posts high margins—estimated operating margin ~28% in 2024—and low incremental costs, so it generates steady free cash flow with minimal capex through 2025.

Property Management Services

Property Management Services at Dalian Wanda are a cash cow: standardized facility, security, and FM services across ~1,200 Wanda commercial properties deliver high market share and low growth, generating recurring revenue from long-term contracts—estimated RMB 6.4 billion in 2024 service revenue and mid-20s operating margins.

This unit stabilizes operations, ensures uptime for malls and hotels, and converts scale into predictable cash flow with renewal rates above 85% in 2024.

- ~1,200 properties managed (2024)

- RMB 6.4 billion service revenue (2024)

- Mid-20s operating margin (2024)

- >85% contract renewal rate (2024)

Wanda Brand Licensing

The Wanda brand licensing unit leverages Dalian Wanda Group’s decades of commercial success to command high market share in China’s real-estate branding sector, generating recurring royalties with minimal overhead; in 2024 brand-related fees and franchising contributed an estimated RMB 1.2–1.5 billion to group revenues, making it a classic BCG Cash Cow.

In a mature market where developers pay premium to use Wanda for project viability, the unit converts stored brand equity into pure profit, supporting group cash flow and funding riskier segments like cultural tourism and cinemas; licensing margins exceed 80% per industry reports in 2023–24.

- RMB 1.2–1.5bn estimated 2024 revenue from licensing

- >80% estimated operating margin

- High market share in commercial real-estate branding

- Low incremental cost, steady cash generation

Wanda’s high‑margin cash engines fund debt cut and growth

Wanda’s cash cows—Wanda Plazas (management fees CNY 8.4bn, FCF CNY 6.1bn 2025), Domestic Film Distribution (≈45% market share 2024, ~28% op margin), Property Management (1,200 properties, CNY 6.4bn revenue 2024, mid-20s margin) and Brand Licensing (CNY 1.2–1.5bn 2024, >80% margin)—generate steady high-margin cash to cut net debt and fund growth.

| Unit | Key 2024–25 |

|---|---|

| Wanda Plazas | Fees CNY 8.4bn; FCF CNY 6.1bn (2025) |

| Film | 45% share; 28% margin (2024) |

| Prop Mgmt | 1,200 props; CNY 6.4bn (2024) |

| Brand | CNY 1.2–1.5bn; >80% margin (2024) |

Preview = Final Product

Dalian Wanda Group Co Ltd. BCG Matrix

The file you're previewing is the final Dalian Wanda Group Co Ltd BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a polished, analysis-ready report tailored for strategic planning and investor review.