Waste Connections Boston Consulting Group Matrix

Unlock Strategic Clarity

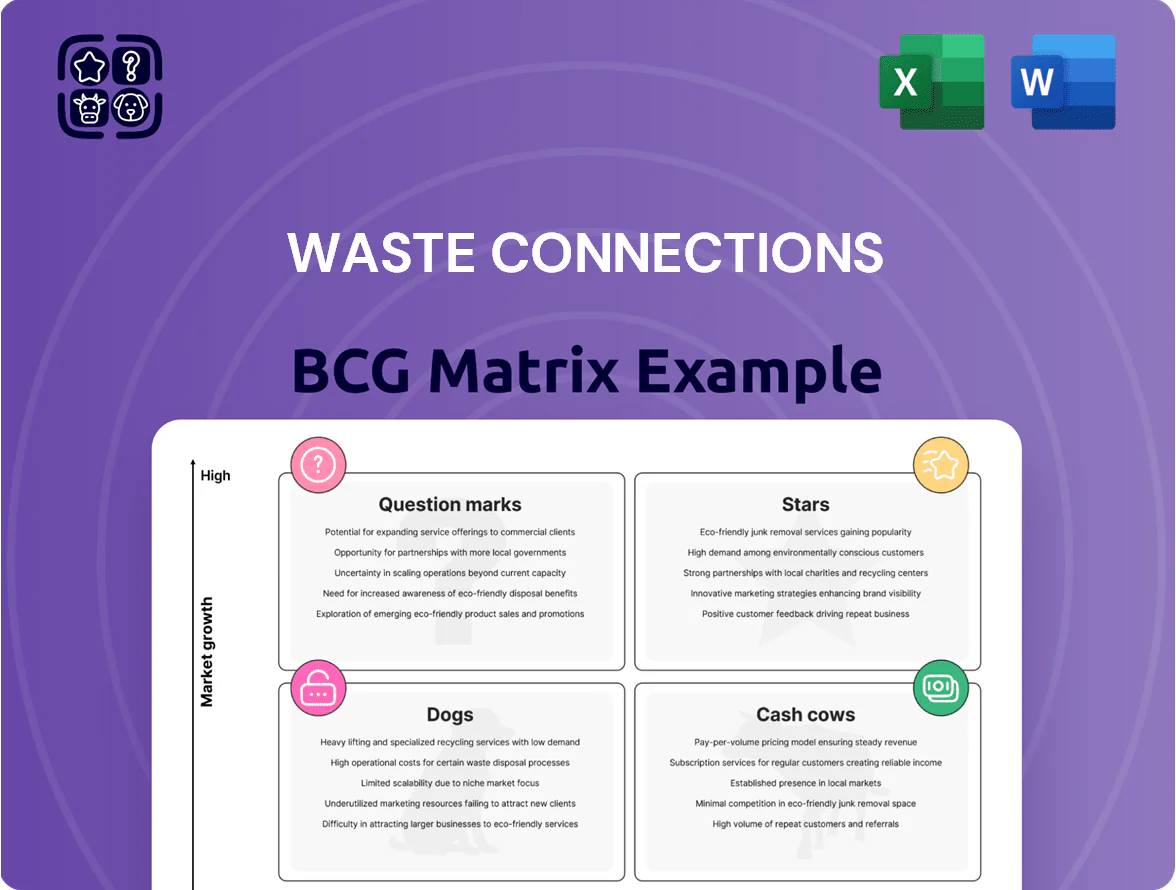

Waste Connections' BCG Matrix snapshot highlights where its service lines and regional segments sit amid steady cash generation and pockets of growth potential, revealing which units are reliable cash cows versus those needing investment or divestment; this preview teases quadrant placement and strategic implications. Purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and operational strategy.

Stars

Renewable Natural Gas Infrastructure

Waste Connections has scaled landfill gas-to-energy projects, converting methane to pipeline-quality renewable natural gas (RNG) and expanding capacity by ~40% from 2020–2025 to capture decarbonization demand.

RNG sales and renewable energy credits grew revenues in this segment by an estimated $55–70 million in 2025, aided by corporate sustainability mandates and federal/state incentives (LCFS, RINs).

As one of the largest landfill owners, Waste Connections holds a leading market share in RNG infrastructure, positioning it as a Star in the BCG matrix within a high-growth energy sub-sector.

Strategic Secondary Market Acquisitions

Waste Connections targets secondary U.S. markets—suburban and rural hubs—where it builds dominant local share; in 2024 these regions grew population by ~0.8% annually, boosting volume and pricing power.

Acquisitions cost tens to hundreds of millions per market but create localized monopolies; Waste Connections reported 2024 adjusted EBITDA margin of ~30% in smaller markets, lifting long‑term cash flow.

Advanced Robotic Recycling Facilities

Waste Connections’ AI-driven robotic Material Recovery Facilities (MRFs) have raised recovery purity to over 95%, cutting residue rates and boosting sellable commodity yields; in 2024 MRF throughput rose ~18% year-over-year, driving incremental EBITDA margins near 6 percentage points for the unit.

High-Growth Sun Belt Operations

Waste Connections has concentrated assets across the Sun Belt, where 2020–2025 net migration added ~4.6 million people and GDP growth averaged ~3.1% annually, letting the company convert high local market share into rising residential and commercial volumes.

Serving these fast-growing metros requires ongoing capex—for example 2024 fleet and infrastructure capex was $1.3B—plus hiring drivers and technicians, but yields some of the sector’s strongest revenue growth and margin expansion.

- Sun Belt population +4.6M (2020–2025)

- Region GDP ~3.1% CAGR (2020–2024)

- Waste Connections 2024 capex ~$1.3B

- High local market share → volume-driven revenue

Integrated Digital Customer Platforms

Integrated Digital Customer Platforms are a Star: Waste Connections’ real-time logistics and automated billing for industrial clients drove a 12% rise in commercial customer retention in 2024 and supported 6% revenue growth in the services segment year-over-year.

The platforms boost stickiness and market share by offering data transparency smaller rivals lack; customers reduced route waste 8–10%, lowering client costs and raising switching costs.

Ongoing investment—about $45 million in IT capex in 2024—cements a modern position in a low-tech industry and enables upsell of higher-margin services.

- 12% retention gain 2024

- 6% services revenue growth

- 8–10% client route efficiency

- $45M IT capex 2024

Waste Connections: RNG lift, AI MRFs & Sun‑Belt growth drive $55–70M upside

Waste Connections’ RNG, Sun Belt market share, AI MRFs, and digital platforms form Stars: 2024–25 RNG revenue +$55–70M, 2024 capex $1.3B, MRF throughput +18% YoY (2024), IT capex $45M, Sun Belt pop +4.6M (2020–25), 2024 local-market EBITDA ~30%.

| Metric | Value |

|---|---|

| RNG revenue (2025) | $55–70M |

| 2024 capex | $1.3B |

| MRF throughput YoY (2024) | +18% |

| IT capex (2024) | $45M |

| Sun Belt pop (2020–25) | +4.6M |

What is included in the product

Comprehensive BCG Matrix for Waste Connections: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page overview placing each Waste Connections business unit in a BCG quadrant for quick strategic decisions

Cash Cows

Municipal Solid Waste Landfills

Landfills are Waste Connections’ primary cash cow: as of 2024 the company operated ~200 MSW (municipal solid waste) landfills and disposal sites, a network that yields high free cash flow because new permits are scarce and capital is front‑loaded for cell construction.

After initial cell build, maintenance capex is low, so disposal margins run above collection margins; Waste Connections reported consolidated adjusted EBITDA margin of ~38% in 2024, driven largely by landfill economics.

High regional market share for disposal gives pricing power—industry tipping fee increases averaged 3–5% annually (2021–2024), letting Waste Connections fund acquisitions and growth projects across services.

Exclusive Franchise Residential Contracts

A large share of Waste Connections revenue—about 55% of 2024 consolidated revenue ($7.8B of $14.2B)—comes from long-term exclusive municipal franchise contracts that guarantee steady residential volumes.

These mature service territories grow low (roughly 1–2% annual volume growth) but yield predictable, recession-resistant cash flows and 2024 adjusted EBITDA margins near 32% in franchise segments.

Stable competition lets management chase operational efficiency—route density, fuel optimization, and pricing—boosting free cash flow conversion; in 2024 FCF was $1.9B, up 6% year-over-year.

Commercial and Industrial Collection

The Commercial and Industrial Collection segment is a mature cash cow for Waste Connections, holding a leading US market share in municipal and industrial hauling with ~35–40% regional penetration and stable 90%+ contract retention in 2024.

Low incremental marketing spend is needed because the company leverages its network of 2023–2024 routed assets and long-term service agreements, keeping EBITDA margins around 28% in 2024 for collection operations.

Cash from these steady contracts funded roughly $900 million in net interest and reduced leverage in 2024 and supported dividend payouts and $200–300 million in share repurchases that year.

Established Canadian Market Operations

Waste Connections’ mature Canadian operations deliver steady revenue—about CA$1.9 billion in 2024—and hold top market share in Ontario and British Columbia, making them classic cash cows in the BCG matrix.

Market growth in these provinces is stable at roughly 2–3% annually, letting management target margin expansion (operating margin improved to ~18% in 2024) rather than rapid footprint growth.

These operations generate predictable free cash flow—estimated CA$320 million in 2024—which funds R&D and experimental U.S. projects without stressing the balance sheet.

- 2024 revenue CA$1.9B

- Operating margin ~18%

- Free cash flow ~CA$320M

- Provincial growth 2–3%/yr

Regional Transfer Station Networks

Regional transfer station networks are cash cows for Waste Connections, consolidating municipal and commercial waste to cut long-haul costs and improve route density; as of FY2024 the company reported 2024 adjusted EBITDA margin ~26% overall, with transfer operations contributing outsized free cash flow via efficient throughput.

These mature stations hold high regional market share—often 50%+ in key markets—need minimal promotion, and generate steady revenue from third-party tipping fees averaging $40–65 per ton in 2024, funding capex and dividends.

- High share in region: typically >50%

- Low promo spend, high operating efficiency

- Tipping fees (2024): $40–65/ton

- Supports EBITDA margin ~26% (2024)

Waste Connections’ cash-cow assets: $7.8B revenue, ~32–38% EBITDA, $1.9B FCF

Landfills, transfer stations, franchise collection, and Canadian ops are Waste Connections’ cash cows—together they generated ~55% of 2024 revenue ($7.8B), adjusted EBITDA margins ~32–38%, FCF $1.9B, and funded $200–300M repurchases and $900M net interest. These mature assets grow ~1–3% yearly, have high regional shares (often 35–50%+), and tipping fees ~$40–65/ton (2024).

| Asset | 2024 Revenue | Adj EBITDA Margin | FCF | Growth |

|---|---|---|---|---|

| Landfills | — | ~38% | — | 1–2% |

| Franchise Collection | $7.8B total* | ~32% | — | 1–2% |

| Transfer Stations | — | ~26% | — | 1–3% |

| Canada | CA$1.9B | ~18% | CA$320M | 2–3% |

Full Transparency, Always

Waste Connections BCG Matrix

The file you're previewing on this page is the exact Waste Connections BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the finalized, fully formatted analysis for strategic use. This preview reflects the same data-driven quadrant mapping and insights included in the downloadable file, crafted for clarity and immediate presentation. Upon purchase, the complete document is delivered ready to edit, print, or integrate into your planning materials with no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Waste Connections' BCG Matrix snapshot highlights where its service lines and regional segments sit amid steady cash generation and pockets of growth potential, revealing which units are reliable cash cows versus those needing investment or divestment; this preview teases quadrant placement and strategic implications. Purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and operational strategy.

Stars

Renewable Natural Gas Infrastructure

Waste Connections has scaled landfill gas-to-energy projects, converting methane to pipeline-quality renewable natural gas (RNG) and expanding capacity by ~40% from 2020–2025 to capture decarbonization demand.

RNG sales and renewable energy credits grew revenues in this segment by an estimated $55–70 million in 2025, aided by corporate sustainability mandates and federal/state incentives (LCFS, RINs).

As one of the largest landfill owners, Waste Connections holds a leading market share in RNG infrastructure, positioning it as a Star in the BCG matrix within a high-growth energy sub-sector.

Strategic Secondary Market Acquisitions

Waste Connections targets secondary U.S. markets—suburban and rural hubs—where it builds dominant local share; in 2024 these regions grew population by ~0.8% annually, boosting volume and pricing power.

Acquisitions cost tens to hundreds of millions per market but create localized monopolies; Waste Connections reported 2024 adjusted EBITDA margin of ~30% in smaller markets, lifting long‑term cash flow.

Advanced Robotic Recycling Facilities

Waste Connections’ AI-driven robotic Material Recovery Facilities (MRFs) have raised recovery purity to over 95%, cutting residue rates and boosting sellable commodity yields; in 2024 MRF throughput rose ~18% year-over-year, driving incremental EBITDA margins near 6 percentage points for the unit.

High-Growth Sun Belt Operations

Waste Connections has concentrated assets across the Sun Belt, where 2020–2025 net migration added ~4.6 million people and GDP growth averaged ~3.1% annually, letting the company convert high local market share into rising residential and commercial volumes.

Serving these fast-growing metros requires ongoing capex—for example 2024 fleet and infrastructure capex was $1.3B—plus hiring drivers and technicians, but yields some of the sector’s strongest revenue growth and margin expansion.

- Sun Belt population +4.6M (2020–2025)

- Region GDP ~3.1% CAGR (2020–2024)

- Waste Connections 2024 capex ~$1.3B

- High local market share → volume-driven revenue

Integrated Digital Customer Platforms

Integrated Digital Customer Platforms are a Star: Waste Connections’ real-time logistics and automated billing for industrial clients drove a 12% rise in commercial customer retention in 2024 and supported 6% revenue growth in the services segment year-over-year.

The platforms boost stickiness and market share by offering data transparency smaller rivals lack; customers reduced route waste 8–10%, lowering client costs and raising switching costs.

Ongoing investment—about $45 million in IT capex in 2024—cements a modern position in a low-tech industry and enables upsell of higher-margin services.

- 12% retention gain 2024

- 6% services revenue growth

- 8–10% client route efficiency

- $45M IT capex 2024

Waste Connections: RNG lift, AI MRFs & Sun‑Belt growth drive $55–70M upside

Waste Connections’ RNG, Sun Belt market share, AI MRFs, and digital platforms form Stars: 2024–25 RNG revenue +$55–70M, 2024 capex $1.3B, MRF throughput +18% YoY (2024), IT capex $45M, Sun Belt pop +4.6M (2020–25), 2024 local-market EBITDA ~30%.

| Metric | Value |

|---|---|

| RNG revenue (2025) | $55–70M |

| 2024 capex | $1.3B |

| MRF throughput YoY (2024) | +18% |

| IT capex (2024) | $45M |

| Sun Belt pop (2020–25) | +4.6M |

What is included in the product

Comprehensive BCG Matrix for Waste Connections: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page overview placing each Waste Connections business unit in a BCG quadrant for quick strategic decisions

Cash Cows

Municipal Solid Waste Landfills

Landfills are Waste Connections’ primary cash cow: as of 2024 the company operated ~200 MSW (municipal solid waste) landfills and disposal sites, a network that yields high free cash flow because new permits are scarce and capital is front‑loaded for cell construction.

After initial cell build, maintenance capex is low, so disposal margins run above collection margins; Waste Connections reported consolidated adjusted EBITDA margin of ~38% in 2024, driven largely by landfill economics.

High regional market share for disposal gives pricing power—industry tipping fee increases averaged 3–5% annually (2021–2024), letting Waste Connections fund acquisitions and growth projects across services.

Exclusive Franchise Residential Contracts

A large share of Waste Connections revenue—about 55% of 2024 consolidated revenue ($7.8B of $14.2B)—comes from long-term exclusive municipal franchise contracts that guarantee steady residential volumes.

These mature service territories grow low (roughly 1–2% annual volume growth) but yield predictable, recession-resistant cash flows and 2024 adjusted EBITDA margins near 32% in franchise segments.

Stable competition lets management chase operational efficiency—route density, fuel optimization, and pricing—boosting free cash flow conversion; in 2024 FCF was $1.9B, up 6% year-over-year.

Commercial and Industrial Collection

The Commercial and Industrial Collection segment is a mature cash cow for Waste Connections, holding a leading US market share in municipal and industrial hauling with ~35–40% regional penetration and stable 90%+ contract retention in 2024.

Low incremental marketing spend is needed because the company leverages its network of 2023–2024 routed assets and long-term service agreements, keeping EBITDA margins around 28% in 2024 for collection operations.

Cash from these steady contracts funded roughly $900 million in net interest and reduced leverage in 2024 and supported dividend payouts and $200–300 million in share repurchases that year.

Established Canadian Market Operations

Waste Connections’ mature Canadian operations deliver steady revenue—about CA$1.9 billion in 2024—and hold top market share in Ontario and British Columbia, making them classic cash cows in the BCG matrix.

Market growth in these provinces is stable at roughly 2–3% annually, letting management target margin expansion (operating margin improved to ~18% in 2024) rather than rapid footprint growth.

These operations generate predictable free cash flow—estimated CA$320 million in 2024—which funds R&D and experimental U.S. projects without stressing the balance sheet.

- 2024 revenue CA$1.9B

- Operating margin ~18%

- Free cash flow ~CA$320M

- Provincial growth 2–3%/yr

Regional Transfer Station Networks

Regional transfer station networks are cash cows for Waste Connections, consolidating municipal and commercial waste to cut long-haul costs and improve route density; as of FY2024 the company reported 2024 adjusted EBITDA margin ~26% overall, with transfer operations contributing outsized free cash flow via efficient throughput.

These mature stations hold high regional market share—often 50%+ in key markets—need minimal promotion, and generate steady revenue from third-party tipping fees averaging $40–65 per ton in 2024, funding capex and dividends.

- High share in region: typically >50%

- Low promo spend, high operating efficiency

- Tipping fees (2024): $40–65/ton

- Supports EBITDA margin ~26% (2024)

Waste Connections’ cash-cow assets: $7.8B revenue, ~32–38% EBITDA, $1.9B FCF

Landfills, transfer stations, franchise collection, and Canadian ops are Waste Connections’ cash cows—together they generated ~55% of 2024 revenue ($7.8B), adjusted EBITDA margins ~32–38%, FCF $1.9B, and funded $200–300M repurchases and $900M net interest. These mature assets grow ~1–3% yearly, have high regional shares (often 35–50%+), and tipping fees ~$40–65/ton (2024).

| Asset | 2024 Revenue | Adj EBITDA Margin | FCF | Growth |

|---|---|---|---|---|

| Landfills | — | ~38% | — | 1–2% |

| Franchise Collection | $7.8B total* | ~32% | — | 1–2% |

| Transfer Stations | — | ~26% | — | 1–3% |

| Canada | CA$1.9B | ~18% | CA$320M | 2–3% |

Full Transparency, Always

Waste Connections BCG Matrix

The file you're previewing on this page is the exact Waste Connections BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the finalized, fully formatted analysis for strategic use. This preview reflects the same data-driven quadrant mapping and insights included in the downloadable file, crafted for clarity and immediate presentation. Upon purchase, the complete document is delivered ready to edit, print, or integrate into your planning materials with no surprises.