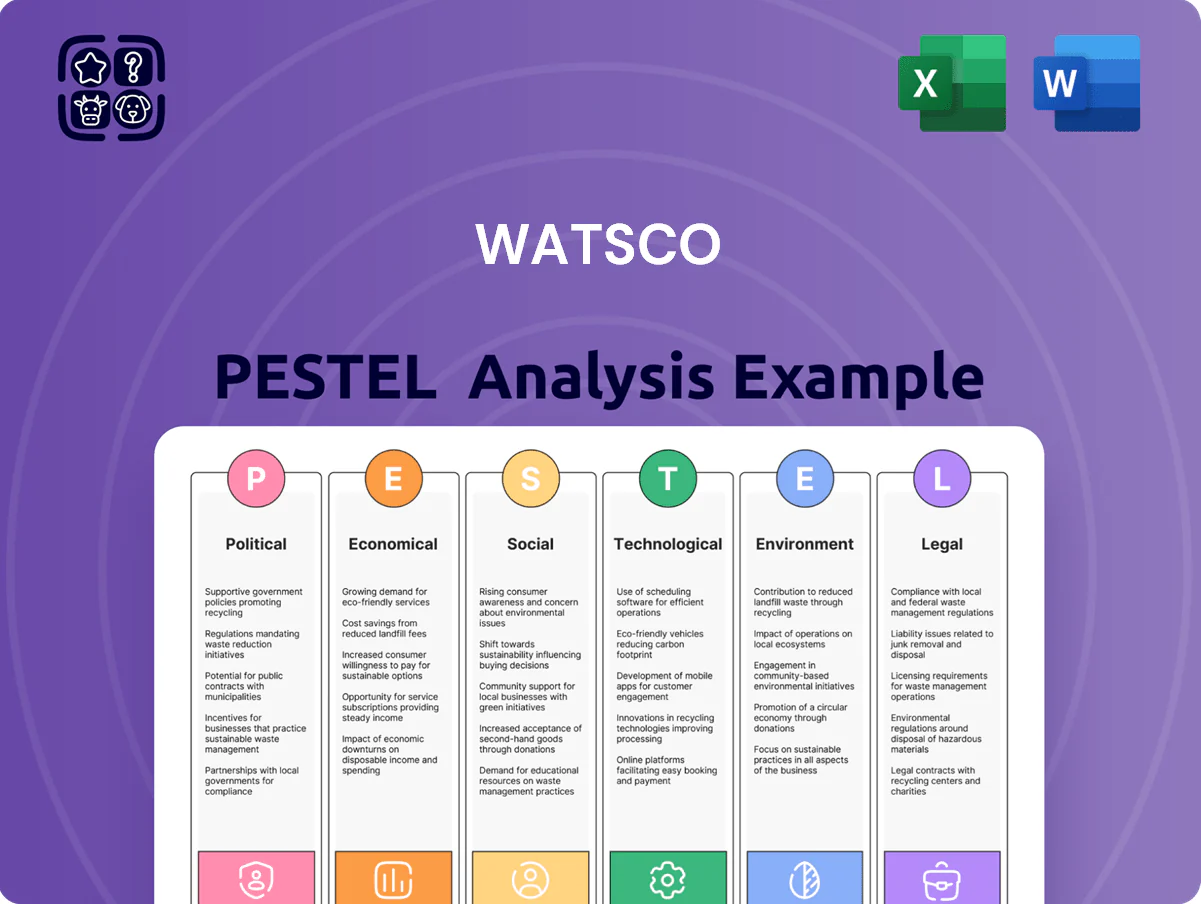

Watsco PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unpack how regulatory shifts, supply-chain dynamics, and energy-transition trends are shaping Watsco’s growth and risk profile—our PESTLE snapshot highlights the most consequential external forces investors and strategists must watch. Purchase the full PESTLE to get actionable, editable insights that power smarter forecasts, due diligence, and strategic moves.

Political factors

Federal Tax Incentive Extensions

The Inflation Reduction Act tax credits through 2025, covering up to 30% of heat pump and high-SEER system costs, are accelerating residential adoption and support Watsco’s premium SKU mix; DOE data shows heat pump shipments rose ~22% YoY in 2024, boosting Watsco’s high-margin sales.

Trade Policy and Import Tariffs

Department of Energy Efficiency Mandates

Strict DOE efficiency standards (notably recent SEER2 rules) force phase-out of low-efficiency units, pushing demand toward higher-cost systems; HVAC retail prices rose ~6–8% industry-wide in 2024 as manufacturers transitioned production.

Watsco educates 8,700+ contractor partners through training and inventory programs, ensuring compliant stock and capturing upsell to premium units that boosted 2024 parts & supplies margin by ~120 bps.

Mandates incentivize full system replacements over repairs: industry replacement volumes grew ~10% in 2024, benefiting Watsco’s higher-margin installation-related sales.

State-Level Electrification Policies

State mandates in New York, California, Massachusetts and others push toward electrification, accelerating demand for heat pumps—Watsco’s HVAC distribution sales to light-commercial/residential heat pump lines grew ~12% in FY2024 per company reports.

Watsco’s strong market share in ducted and ductless heat pumps benefits from these localized policies, but navigating 50-state regulatory variations requires tailored inventory, training and financing support to contractors.

- Key states: NY, CA, MA driving adoption

- Watsco FY2024 heat-pump-related sales growth ~12%

- Requires localized distribution, contractor training, rebate/financing alignment

Geopolitical Supply Chain Security

Political stability in Southeast Asia and Mexico is vital for Watsco’s inventory; Vietnam and Mexico accounted for an estimated 18–22% of HVAC components for North American supply chains in 2024, so disruptions materially risk consistency.

Near-shoring incentives in the US and Mexico (tariff savings up to 10–15% and $20B+ in US tax incentives 2024–25) push suppliers like Carrier to reconfigure logistics, affecting Watsco’s long-term sourcing and capex planning.

Border bottlenecks and unrest can trigger temporary shortages and raise freight costs—USMCA-related delays increased transit times by 12% and spot freight rates jumped 25% in 2023–24, pressuring margins.

- Key risk: regional instability in SE Asia/Mexico → inventory volatility

- Near-shoring: tariff savings 10–15%, $20B+ incentives reshape supplier footprints

- Impact: transit times +12%, spot freight +25% (2023–24) → margin pressure

Watsco Faces Margin Pressure as Electrification Boosts Sales but Tariffs, Near‑shoring Raise Costs

Federal incentives (IRA) and state electrification mandates drove ~12–22% heat-pump sales growth in 2024, while tariffs and Section 301 duties raised landed costs ~5–12%, pressuring Watsco’s 2024 gross margin (22.8%); near-shoring incentives ($20B+ 2024–25) and supply risk in Vietnam/Mexico (18–22% of components) shifted sourcing, increasing transit times ~12% and spot freight +25% (2023–24).

| Metric | 2023–24 / 2024 |

|---|---|

| Watsco revenue | $8.9B (FY2024) |

| Gross margin | 22.8% (2024) |

| Heat-pump sales growth | ~12% (FY2024) |

| Tariff cost impact | +5–12% |

| Component sourcing from VN/MX | 18–22% |

| Transit times | +12% (2023–24) |

| Spot freight | +25% (2023–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Watsco, with data-backed trends and region-specific regulatory context to identify threats and opportunities.

Condenses Watsco's PESTLE into a concise, shareable brief that highlights regulatory, economic, and technological risks for quick use in presentations, team alignment, or client reports.

Economic factors

Interest Rate Environment

As of late 2025, the US federal funds rate near 5.25–5.50% has pressured new housing starts, which fell 8% year-over-year in 2024, steering Watsco toward repair/replacement demand that represented about 65% of residential HVAC spend in 2024.

Inflationary Trends in Raw Materials

Fluctuations in global copper, aluminum and steel prices—copper up ~28% and aluminum up ~18% year-over-year in 2024—raise Watsco’s HVAC unit and parts costs, pressuring gross margins if not passed to contractors.

Watsco’s ability to pass costs through is evidenced by its 2024 gross margin remaining near 24.5%, signaling some pricing power.

Persistent service labor inflation (wage growth ~4–6% in 2024–25) raises installation costs and can dampen discretionary replacements and upgrades.

Housing Market Turnover

Economic health in real estate drives HVAC demand, since inspections and replacements spike during home sales; U.S. existing-home sales fell 10.3% year-over-year in 2024 Q4, pressuring replacement volumes. A stagnant market with low turnover reduces full-system installs—national turnover rates dropped to about 3.7% in 2024. Watsco tracks regional home sales, inventory days, and migration trends to calibrate inventory and avoid overstocking.

Consumer Disposable Income

Consumer disposable income drives whether homeowners buy high-end energy-efficient HVAC systems or choose basic repairs; US real disposable personal income rose 3.9% YoY in 2024, supporting upgrade demand in premium segments.

Economic downturns push consumers toward delay and temporary 'band-aid' fixes—residential replacement rates fell 7% during the 2023–2024 slowdown in key markets, reducing average ticket sizes.

Watsco offsets variability by stocking a wide product range and price tiers; in 2024 Watsco reported diversified sales with 28% of revenue from premium units and broad coverage across value segments to capture shifting demand.

- Disposable income +3.9% YoY (2024)

- Replacement rates down ~7% in 2023–24 slowdown

- Watsco premium unit revenue ~28% (2024)

Skilled Labor Shortages

The U.S. skilled labor shortage in HVAC—an estimated 50,000+ technician deficit in 2024 per industry reports—constrains contractors' installation capacity, increasing backlogs and slowing Watsco’s inventory turnover from 4.5 to 3.9 annual turns in peak months; revenue mix pressure prompted Watsco to invest over $100 million in digital tools (mobile ordering, dispatch, training) to boost contractor productivity and reduce service cycle time.

- ~50,000 technician shortfall (2024)

- Inventory turns dip from 4.5 to 3.9 in peak periods

- $100M+ invested in digital productivity tools

- Investment aims to shorten service cycles and raise install throughput

Watsco weathers commodity costs, tech shortfall; replacement demand fuels 2024 resilience

Higher rates and weaker housing reduced new installs; replacement/rebuilds ~65% of residential spend (2024), US disposable income +3.9% YoY (2024), commodity inflation (copper +28%, aluminum +18% YoY 2024) pressures margins though 2024 gross margin ~24.5%; ~50,000 HVAC technician shortfall (2024) slowed inventory turns from 4.5 to 3.9; Watsco invested $100M+ in digital tools.

| Metric | 2024 |

|---|---|

| Replacement share | 65% |

| Real disposable income YoY | +3.9% |

| Copper price YoY | +28% |

| Gross margin | 24.5% |

| Technician shortfall | ~50,000 |

| Digital investment | $100M+ |

Full Version Awaits

Watsco PESTLE Analysis

The preview shown here is the exact Watsco PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unpack how regulatory shifts, supply-chain dynamics, and energy-transition trends are shaping Watsco’s growth and risk profile—our PESTLE snapshot highlights the most consequential external forces investors and strategists must watch. Purchase the full PESTLE to get actionable, editable insights that power smarter forecasts, due diligence, and strategic moves.

Political factors

Federal Tax Incentive Extensions

The Inflation Reduction Act tax credits through 2025, covering up to 30% of heat pump and high-SEER system costs, are accelerating residential adoption and support Watsco’s premium SKU mix; DOE data shows heat pump shipments rose ~22% YoY in 2024, boosting Watsco’s high-margin sales.

Trade Policy and Import Tariffs

Department of Energy Efficiency Mandates

Strict DOE efficiency standards (notably recent SEER2 rules) force phase-out of low-efficiency units, pushing demand toward higher-cost systems; HVAC retail prices rose ~6–8% industry-wide in 2024 as manufacturers transitioned production.

Watsco educates 8,700+ contractor partners through training and inventory programs, ensuring compliant stock and capturing upsell to premium units that boosted 2024 parts & supplies margin by ~120 bps.

Mandates incentivize full system replacements over repairs: industry replacement volumes grew ~10% in 2024, benefiting Watsco’s higher-margin installation-related sales.

State-Level Electrification Policies

State mandates in New York, California, Massachusetts and others push toward electrification, accelerating demand for heat pumps—Watsco’s HVAC distribution sales to light-commercial/residential heat pump lines grew ~12% in FY2024 per company reports.

Watsco’s strong market share in ducted and ductless heat pumps benefits from these localized policies, but navigating 50-state regulatory variations requires tailored inventory, training and financing support to contractors.

- Key states: NY, CA, MA driving adoption

- Watsco FY2024 heat-pump-related sales growth ~12%

- Requires localized distribution, contractor training, rebate/financing alignment

Geopolitical Supply Chain Security

Political stability in Southeast Asia and Mexico is vital for Watsco’s inventory; Vietnam and Mexico accounted for an estimated 18–22% of HVAC components for North American supply chains in 2024, so disruptions materially risk consistency.

Near-shoring incentives in the US and Mexico (tariff savings up to 10–15% and $20B+ in US tax incentives 2024–25) push suppliers like Carrier to reconfigure logistics, affecting Watsco’s long-term sourcing and capex planning.

Border bottlenecks and unrest can trigger temporary shortages and raise freight costs—USMCA-related delays increased transit times by 12% and spot freight rates jumped 25% in 2023–24, pressuring margins.

- Key risk: regional instability in SE Asia/Mexico → inventory volatility

- Near-shoring: tariff savings 10–15%, $20B+ incentives reshape supplier footprints

- Impact: transit times +12%, spot freight +25% (2023–24) → margin pressure

Watsco Faces Margin Pressure as Electrification Boosts Sales but Tariffs, Near‑shoring Raise Costs

Federal incentives (IRA) and state electrification mandates drove ~12–22% heat-pump sales growth in 2024, while tariffs and Section 301 duties raised landed costs ~5–12%, pressuring Watsco’s 2024 gross margin (22.8%); near-shoring incentives ($20B+ 2024–25) and supply risk in Vietnam/Mexico (18–22% of components) shifted sourcing, increasing transit times ~12% and spot freight +25% (2023–24).

| Metric | 2023–24 / 2024 |

|---|---|

| Watsco revenue | $8.9B (FY2024) |

| Gross margin | 22.8% (2024) |

| Heat-pump sales growth | ~12% (FY2024) |

| Tariff cost impact | +5–12% |

| Component sourcing from VN/MX | 18–22% |

| Transit times | +12% (2023–24) |

| Spot freight | +25% (2023–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Watsco, with data-backed trends and region-specific regulatory context to identify threats and opportunities.

Condenses Watsco's PESTLE into a concise, shareable brief that highlights regulatory, economic, and technological risks for quick use in presentations, team alignment, or client reports.

Economic factors

Interest Rate Environment

As of late 2025, the US federal funds rate near 5.25–5.50% has pressured new housing starts, which fell 8% year-over-year in 2024, steering Watsco toward repair/replacement demand that represented about 65% of residential HVAC spend in 2024.

Inflationary Trends in Raw Materials

Fluctuations in global copper, aluminum and steel prices—copper up ~28% and aluminum up ~18% year-over-year in 2024—raise Watsco’s HVAC unit and parts costs, pressuring gross margins if not passed to contractors.

Watsco’s ability to pass costs through is evidenced by its 2024 gross margin remaining near 24.5%, signaling some pricing power.

Persistent service labor inflation (wage growth ~4–6% in 2024–25) raises installation costs and can dampen discretionary replacements and upgrades.

Housing Market Turnover

Economic health in real estate drives HVAC demand, since inspections and replacements spike during home sales; U.S. existing-home sales fell 10.3% year-over-year in 2024 Q4, pressuring replacement volumes. A stagnant market with low turnover reduces full-system installs—national turnover rates dropped to about 3.7% in 2024. Watsco tracks regional home sales, inventory days, and migration trends to calibrate inventory and avoid overstocking.

Consumer Disposable Income

Consumer disposable income drives whether homeowners buy high-end energy-efficient HVAC systems or choose basic repairs; US real disposable personal income rose 3.9% YoY in 2024, supporting upgrade demand in premium segments.

Economic downturns push consumers toward delay and temporary 'band-aid' fixes—residential replacement rates fell 7% during the 2023–2024 slowdown in key markets, reducing average ticket sizes.

Watsco offsets variability by stocking a wide product range and price tiers; in 2024 Watsco reported diversified sales with 28% of revenue from premium units and broad coverage across value segments to capture shifting demand.

- Disposable income +3.9% YoY (2024)

- Replacement rates down ~7% in 2023–24 slowdown

- Watsco premium unit revenue ~28% (2024)

Skilled Labor Shortages

The U.S. skilled labor shortage in HVAC—an estimated 50,000+ technician deficit in 2024 per industry reports—constrains contractors' installation capacity, increasing backlogs and slowing Watsco’s inventory turnover from 4.5 to 3.9 annual turns in peak months; revenue mix pressure prompted Watsco to invest over $100 million in digital tools (mobile ordering, dispatch, training) to boost contractor productivity and reduce service cycle time.

- ~50,000 technician shortfall (2024)

- Inventory turns dip from 4.5 to 3.9 in peak periods

- $100M+ invested in digital productivity tools

- Investment aims to shorten service cycles and raise install throughput

Watsco weathers commodity costs, tech shortfall; replacement demand fuels 2024 resilience

Higher rates and weaker housing reduced new installs; replacement/rebuilds ~65% of residential spend (2024), US disposable income +3.9% YoY (2024), commodity inflation (copper +28%, aluminum +18% YoY 2024) pressures margins though 2024 gross margin ~24.5%; ~50,000 HVAC technician shortfall (2024) slowed inventory turns from 4.5 to 3.9; Watsco invested $100M+ in digital tools.

| Metric | 2024 |

|---|---|

| Replacement share | 65% |

| Real disposable income YoY | +3.9% |

| Copper price YoY | +28% |

| Gross margin | 24.5% |

| Technician shortfall | ~50,000 |

| Digital investment | $100M+ |

Full Version Awaits

Watsco PESTLE Analysis

The preview shown here is the exact Watsco PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.