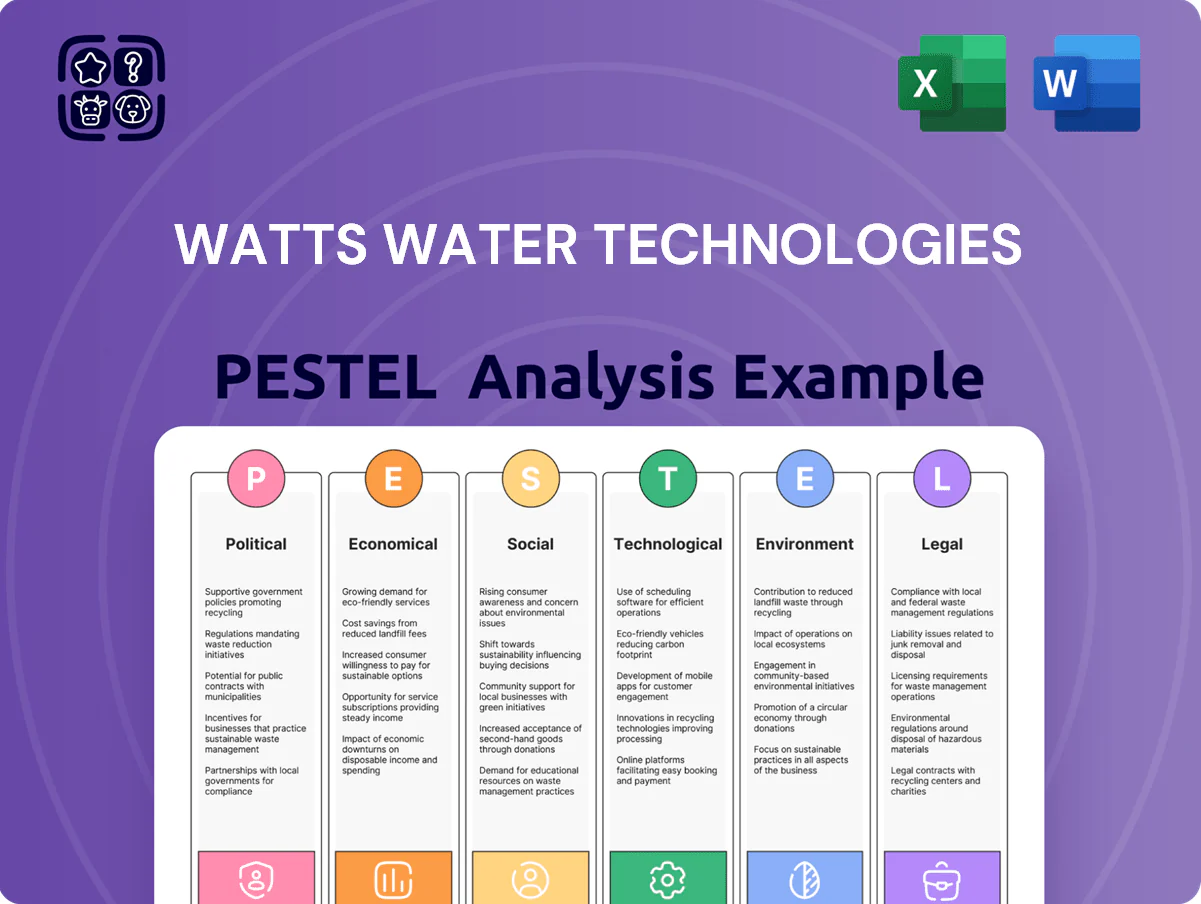

Watts Water Technologies PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE snapshot for Watts Water Technologies highlights regulatory shifts, supply-chain pressures, and tech-driven product innovation shaping its outlook—insights you can act on today. Ideal for investors and strategists, this concise review reveals where risks and opportunities intersect. Purchase the full PESTLE to unlock detailed analysis, forecasts, and practical recommendations for portfolio or strategic decisions.

Political factors

Government Infrastructure Investment

The Infrastructure Investment and Jobs Act directs about 50 billion USD toward water infrastructure through 2026, creating a multiyear tailwind for Watts Water; federal programs prioritize lead service line replacement and system modernization, driving municipal purchases of backflow preventers and flow-control products. Watts reported fiscal 2024 water segment revenue growth of 8% year-over-year, positioning it to capture increased demand as local governments deploy these allocations through 2025.

Global Trade and Tariff Policies

Trade tensions between the United States and China remain a key political risk for Watts Water Technologies, affecting supply-chain costs after 2018–2025 tariff episodes; US-China goods tariffs peaked near 19% on targeted goods and could push component costs up 3–7% for valves and fittings if renewed barriers appear by end-2025.

Tariff exposure on raw materials—brass, bronze, stainless steel—could raise input costs; US stainless-steel import duties effective 2023 averaged 7–25%, and a 5%–10% tariff shift would materially impact gross margins given raw-materials represent roughly 25%–35% of COGS in plumbing products.

Political-driven shifts to near-shoring and friend-shoring accelerated: Watts increased North American sourcing and capacity, reducing China-sourced parts by an estimated 10%–15% between 2020–2024, a move that limits tariff volatility and improves supply resilience.

Water Safety and Quality Mandates

National and regional governments in North America and Europe have tightened mandates on water safety for public buildings and healthcare sites, with Legionella control now central to updated codes affecting an estimated 1.2 million facilities across OECD countries as of 2024.

Political pressure to eliminate waterborne pathogens is driving requirements for advanced tempering and continuous monitoring systems, boosting market demand for compliant technologies projected to grow at ~6% CAGR through 2028.

Watts Water leverages its digital and mechanical mixing valve portfolio—contributing roughly 18% of 2024 revenue—to supply hospitals and public infrastructure with certified solutions that meet evolving regulatory standards.

Geopolitical Stability in Europe

With ~28% of 2024 revenue from Europe, Watts is exposed to Eurozone political stability; disruptions in trade or regulation can affect supply chains and sales.

European energy security concerns since 2022 have driven policy support for efficient hydronic heating/cooling—accelerating demand for Watts’ valves, controls and heat meters tied to EU climate targets (Fit for 55).

Watts’ product suite positions it as a partner in national green energy programs; EU recovery and green funds (billions allocated) increase retrofit and new-build spending benefiting the company.

- ~28% revenue from Europe (2024)

- EU Fit for 55 & post-2022 energy policies raising retrofit budgets

- Watts supplies key hardware for hydronic efficiency—aligned with EU green funding

Taxation and Fiscal Incentives

Changes in US federal and state corporate tax rates and the expansion of green energy tax credits directly affect Watts Water Technologies’ net margins and reinvestment ability; a 1% corporate tax shift alters after-tax operating cash flow materially given 2025 EBITDA guidance near $640M.

By end-2025, targeted fiscal incentives for water-conserving manufacturing—similar to recent federal clean energy credits—could lower production costs and enhance margins on Watts’ water-efficiency product lines, improving competitive positioning.

Tightening fiscal policy or reduced capital allowances may compress capex among commercial/industrial customers (US business capex growth slowed to ~1.5% YoY in 2024), potentially dampening demand for Watts’ higher-ticket installations.

- 2025 EBITDA guidance reference: ~$640M

- 1% tax-rate change meaningfully impacts after-tax cash flow

- 2024 US business capex growth: ~1.5% YoY

- Potential green credits could reduce manufacturing costs and boost margins

Watts poised to ride $50B water spend—mixing valves & regs boost growth amid tariff risk

Federal water infrastructure funding (~$50B through 2026) and tightening Legionella/energy regs drive municipal and healthcare demand; Watts’ 2024 water revenue +8% and 18% from mixing valves position it to capture growth. Tariff and raw-material duty risk (stainless 7–25% in 2023) and US-China trade tensions could raise component costs 3–7%; ~28% 2024 revenue exposure to Europe links results to EU Fit for 55 funding.

| Metric | Value |

|---|---|

| Federal water funding | $50B (through 2026) |

| Watts water rev growth (2024) | +8% YoY |

| Mixing valves revenue | ~18% of 2024 rev |

| Europe revenue | ~28% (2024) |

| Stainless duties (2023) | 7–25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Watts Water Technologies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE snapshot of Watts Water Technologies that’s presentation-ready, easily shareable, and editable so teams can quickly align on external risks, market positioning, and region-specific action points during planning sessions.

Economic factors

Residential and Commercial Construction Cycles

The financial performance of Watts Water Technologies is closely tied to global construction activity, with new housing starts and commercial development influencing demand for valves, fittings, and controls; US housing starts fell about 12% year-over-year in 2023 but showed signs of stabilization in 2024 with starts up ~4% through Q3 2024. High interest rates through 2022–2024 dampened new builds, yet consensus forecasts in late 2025 project partial recovery in construction permitting and starts. Watts mitigates cyclicality via its repair and replacement segment, which historically contributes roughly 60–70% of revenue and proved resilient during downturns, supporting cash flow and margins while new construction recovers.

Raw Material Price Volatility

Volatility in copper, steel and resins—copper rose ~25% in 2021–22 then softened, while global resin prices swung 15–30% in 2023—directly pressures Watts Water Technologies gross margins and pricing; the company has used agile surcharge programs and passed through costs, helping protect margins (Watts reported 2023 gross margin ~30.8%); through 2025 robust supply‑chain management and hedging of key industrial inputs remain essential to manage inflationary/deflationary cycles.

Interest Rate Environment

Prevailing central bank rates affect Watts Water Technologies’ borrowing costs and customer credit; higher rates raised corporate borrowing spreads in 2024–2025, with US Fed funds averaging 4.25–5.25% in 2024 and edging toward 4.5% by late 2025, increasing debt servicing burdens on capex.

Global Inflationary Trends

Persistent global inflation elevated Watts Water Technologies' input and labor costs in 2023–2025, with U.S. core CPI averaging ~4.5% in 2024, pressuring margins and prompting productivity and SG&A efficiencies to protect operating margin (adjusted operating margin ~13.5% in FY2024).

Price-sensitive customers force careful cost-structure management; Watts used targeted price increases (mid-single digits in 2024) and mix optimization to sustain revenue growth (+8% organic in 2024) while leveraging brand strength to pass through costs.

- U.S. core CPI ~4.5% (2024)

- Adjusted operating margin ~13.5% (FY2024)

- Organic revenue growth +8% (2024)

- Implemented mid-single-digit price increases (2024)

Currency Exchange Fluctuations

As a global entity, Watts Water faces transaction and translation risks from USD, EUR and other currencies; in FY2024 roughly 30% of revenues were sourced outside the US, amplifying FX exposure.

A strong US dollar can raise prices for US-made products abroad and lowered international earnings reported in USD, contributing to a 3–5% FX headwind on adjusted EPS in 2024.

Watts uses hedging (forwards/options), netting and localized manufacturing—over 40% of production capacity is regionalized—to mitigate volatile FX impacts and protect margins.

- ~30% FY2024 revenue non-US, creating FX exposure

- Estimated 3–5% FX headwind to adjusted EPS in 2024

- Hedging, netting and regional manufacturing (≈40% regionalized capacity)

Watts weathers commodity, rate and FX pressures with +8% organic growth, 13.5% OPM

Global construction cycles, input-price volatility (copper/steel/resins), interest-rate-driven demand shifts, inflationary wage/input pressures, and FX exposure materially affect Watts’ revenue, margins and cash flow; FY2024 metrics: organic revenue +8%, adjusted operating margin ~13.5%, gross margin ~30.8%, ~30% revenue non‑US, estimated 3–5% FX EPS headwind.

| Metric | 2024 |

|---|---|

| Organic revenue growth | +8% |

| Adj. operating margin | ~13.5% |

| Gross margin | ~30.8% |

| Non‑US revenue | ~30% |

| FX EPS headwind | 3–5% |

What You See Is What You Get

Watts Water Technologies PESTLE Analysis

The preview shown here is the exact Watts Water Technologies PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the downloadable file you’ll get immediately after payment.

What you see is the final document—concise political, economic, social, technological, legal, and environmental analysis tailored for decision-makers and investors.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our PESTLE snapshot for Watts Water Technologies highlights regulatory shifts, supply-chain pressures, and tech-driven product innovation shaping its outlook—insights you can act on today. Ideal for investors and strategists, this concise review reveals where risks and opportunities intersect. Purchase the full PESTLE to unlock detailed analysis, forecasts, and practical recommendations for portfolio or strategic decisions.

Political factors

Government Infrastructure Investment

The Infrastructure Investment and Jobs Act directs about 50 billion USD toward water infrastructure through 2026, creating a multiyear tailwind for Watts Water; federal programs prioritize lead service line replacement and system modernization, driving municipal purchases of backflow preventers and flow-control products. Watts reported fiscal 2024 water segment revenue growth of 8% year-over-year, positioning it to capture increased demand as local governments deploy these allocations through 2025.

Global Trade and Tariff Policies

Trade tensions between the United States and China remain a key political risk for Watts Water Technologies, affecting supply-chain costs after 2018–2025 tariff episodes; US-China goods tariffs peaked near 19% on targeted goods and could push component costs up 3–7% for valves and fittings if renewed barriers appear by end-2025.

Tariff exposure on raw materials—brass, bronze, stainless steel—could raise input costs; US stainless-steel import duties effective 2023 averaged 7–25%, and a 5%–10% tariff shift would materially impact gross margins given raw-materials represent roughly 25%–35% of COGS in plumbing products.

Political-driven shifts to near-shoring and friend-shoring accelerated: Watts increased North American sourcing and capacity, reducing China-sourced parts by an estimated 10%–15% between 2020–2024, a move that limits tariff volatility and improves supply resilience.

Water Safety and Quality Mandates

National and regional governments in North America and Europe have tightened mandates on water safety for public buildings and healthcare sites, with Legionella control now central to updated codes affecting an estimated 1.2 million facilities across OECD countries as of 2024.

Political pressure to eliminate waterborne pathogens is driving requirements for advanced tempering and continuous monitoring systems, boosting market demand for compliant technologies projected to grow at ~6% CAGR through 2028.

Watts Water leverages its digital and mechanical mixing valve portfolio—contributing roughly 18% of 2024 revenue—to supply hospitals and public infrastructure with certified solutions that meet evolving regulatory standards.

Geopolitical Stability in Europe

With ~28% of 2024 revenue from Europe, Watts is exposed to Eurozone political stability; disruptions in trade or regulation can affect supply chains and sales.

European energy security concerns since 2022 have driven policy support for efficient hydronic heating/cooling—accelerating demand for Watts’ valves, controls and heat meters tied to EU climate targets (Fit for 55).

Watts’ product suite positions it as a partner in national green energy programs; EU recovery and green funds (billions allocated) increase retrofit and new-build spending benefiting the company.

- ~28% revenue from Europe (2024)

- EU Fit for 55 & post-2022 energy policies raising retrofit budgets

- Watts supplies key hardware for hydronic efficiency—aligned with EU green funding

Taxation and Fiscal Incentives

Changes in US federal and state corporate tax rates and the expansion of green energy tax credits directly affect Watts Water Technologies’ net margins and reinvestment ability; a 1% corporate tax shift alters after-tax operating cash flow materially given 2025 EBITDA guidance near $640M.

By end-2025, targeted fiscal incentives for water-conserving manufacturing—similar to recent federal clean energy credits—could lower production costs and enhance margins on Watts’ water-efficiency product lines, improving competitive positioning.

Tightening fiscal policy or reduced capital allowances may compress capex among commercial/industrial customers (US business capex growth slowed to ~1.5% YoY in 2024), potentially dampening demand for Watts’ higher-ticket installations.

- 2025 EBITDA guidance reference: ~$640M

- 1% tax-rate change meaningfully impacts after-tax cash flow

- 2024 US business capex growth: ~1.5% YoY

- Potential green credits could reduce manufacturing costs and boost margins

Watts poised to ride $50B water spend—mixing valves & regs boost growth amid tariff risk

Federal water infrastructure funding (~$50B through 2026) and tightening Legionella/energy regs drive municipal and healthcare demand; Watts’ 2024 water revenue +8% and 18% from mixing valves position it to capture growth. Tariff and raw-material duty risk (stainless 7–25% in 2023) and US-China trade tensions could raise component costs 3–7%; ~28% 2024 revenue exposure to Europe links results to EU Fit for 55 funding.

| Metric | Value |

|---|---|

| Federal water funding | $50B (through 2026) |

| Watts water rev growth (2024) | +8% YoY |

| Mixing valves revenue | ~18% of 2024 rev |

| Europe revenue | ~28% (2024) |

| Stainless duties (2023) | 7–25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Watts Water Technologies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, visually segmented PESTLE snapshot of Watts Water Technologies that’s presentation-ready, easily shareable, and editable so teams can quickly align on external risks, market positioning, and region-specific action points during planning sessions.

Economic factors

Residential and Commercial Construction Cycles

The financial performance of Watts Water Technologies is closely tied to global construction activity, with new housing starts and commercial development influencing demand for valves, fittings, and controls; US housing starts fell about 12% year-over-year in 2023 but showed signs of stabilization in 2024 with starts up ~4% through Q3 2024. High interest rates through 2022–2024 dampened new builds, yet consensus forecasts in late 2025 project partial recovery in construction permitting and starts. Watts mitigates cyclicality via its repair and replacement segment, which historically contributes roughly 60–70% of revenue and proved resilient during downturns, supporting cash flow and margins while new construction recovers.

Raw Material Price Volatility

Volatility in copper, steel and resins—copper rose ~25% in 2021–22 then softened, while global resin prices swung 15–30% in 2023—directly pressures Watts Water Technologies gross margins and pricing; the company has used agile surcharge programs and passed through costs, helping protect margins (Watts reported 2023 gross margin ~30.8%); through 2025 robust supply‑chain management and hedging of key industrial inputs remain essential to manage inflationary/deflationary cycles.

Interest Rate Environment

Prevailing central bank rates affect Watts Water Technologies’ borrowing costs and customer credit; higher rates raised corporate borrowing spreads in 2024–2025, with US Fed funds averaging 4.25–5.25% in 2024 and edging toward 4.5% by late 2025, increasing debt servicing burdens on capex.

Global Inflationary Trends

Persistent global inflation elevated Watts Water Technologies' input and labor costs in 2023–2025, with U.S. core CPI averaging ~4.5% in 2024, pressuring margins and prompting productivity and SG&A efficiencies to protect operating margin (adjusted operating margin ~13.5% in FY2024).

Price-sensitive customers force careful cost-structure management; Watts used targeted price increases (mid-single digits in 2024) and mix optimization to sustain revenue growth (+8% organic in 2024) while leveraging brand strength to pass through costs.

- U.S. core CPI ~4.5% (2024)

- Adjusted operating margin ~13.5% (FY2024)

- Organic revenue growth +8% (2024)

- Implemented mid-single-digit price increases (2024)

Currency Exchange Fluctuations

As a global entity, Watts Water faces transaction and translation risks from USD, EUR and other currencies; in FY2024 roughly 30% of revenues were sourced outside the US, amplifying FX exposure.

A strong US dollar can raise prices for US-made products abroad and lowered international earnings reported in USD, contributing to a 3–5% FX headwind on adjusted EPS in 2024.

Watts uses hedging (forwards/options), netting and localized manufacturing—over 40% of production capacity is regionalized—to mitigate volatile FX impacts and protect margins.

- ~30% FY2024 revenue non-US, creating FX exposure

- Estimated 3–5% FX headwind to adjusted EPS in 2024

- Hedging, netting and regional manufacturing (≈40% regionalized capacity)

Watts weathers commodity, rate and FX pressures with +8% organic growth, 13.5% OPM

Global construction cycles, input-price volatility (copper/steel/resins), interest-rate-driven demand shifts, inflationary wage/input pressures, and FX exposure materially affect Watts’ revenue, margins and cash flow; FY2024 metrics: organic revenue +8%, adjusted operating margin ~13.5%, gross margin ~30.8%, ~30% revenue non‑US, estimated 3–5% FX EPS headwind.

| Metric | 2024 |

|---|---|

| Organic revenue growth | +8% |

| Adj. operating margin | ~13.5% |

| Gross margin | ~30.8% |

| Non‑US revenue | ~30% |

| FX EPS headwind | 3–5% |

What You See Is What You Get

Watts Water Technologies PESTLE Analysis

The preview shown here is the exact Watts Water Technologies PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are identical to the downloadable file you’ll get immediately after payment.

What you see is the final document—concise political, economic, social, technological, legal, and environmental analysis tailored for decision-makers and investors.