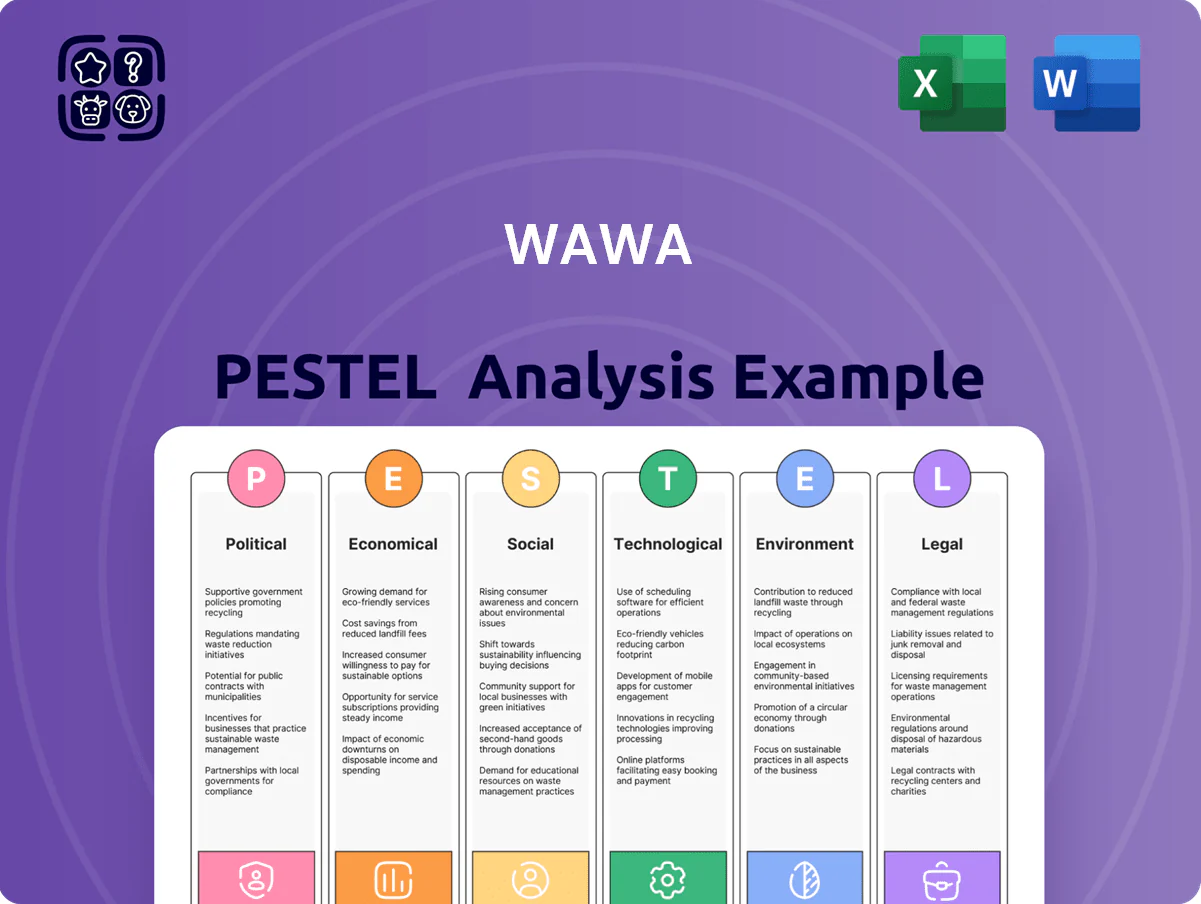

Wawa PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological advances are reshaping Wawa’s competitive edge—our concise PESTLE highlights the external forces driving risk and opportunity. Perfect for investors, strategists, and consultants, the full analysis delivers ready-to-use, editable insights to guide decisions. Purchase now to access the complete, up-to-date breakdown instantly.

Political factors

Fuel Tax Policy and Regulation

State and federal adjustments to gasoline excise taxes directly affect Wawa’s pump pricing and fuel margins; for example, the U.S. federal gas tax remains 18.4¢/gal while several Mid-Atlantic states raised combined state/local rates by up to 10–15¢/gal in 2024, squeezing retail margins unless pricing is adjusted. As governments fund infrastructure through 2025 with projected $200–300 billion state programs, agile price responses are needed to preserve margin and stay competitive. Political shifts across the Mid-Atlantic and Southern states create uneven tax burdens that alter consumer station choice and volume at the pump, with regional tax differentials of 20–40¢/gal materially impacting demand elasticity.

Minimum Wage Legislation

Mandatory minimum wage hikes in states like New Jersey (reaching 15.13 USD/hr for some employers in 2025) and Florida (15.00 USD/hr by 2026) materially raise Wawa’s labor bill across its ~2,500 stores and estimated 43,000 frontline associates, increasing annual payroll costs by an estimated low- to mid-single-digit percentage of revenue.

Wawa is offsetting pressure by investing in automation—self-checkout and digital ordering—to improve labor productivity and contain margin erosion; capital spend on store technology rose to around 120–150 million USD in recent years.

Ongoing political momentum for a higher living wage remains a core input to Wawa’s corporate strategy and financial planning, driving scenario analyses and contingency reserves to preserve EBITDA margins amid rising wage mandates.

Public Health and Tobacco Regulation

Federal and state moves to ban flavored nicotine and raise tobacco taxes—37 states increased cigarette taxes since 2023, with some flavored e-cigarette restrictions cutting flavored SKU sales by up to 30%—threaten Wawa’s ~$1.8B annual tobacco category revenue.

Wawa must comply with evolving FDA guidance and local ordinances targeting youth nicotine use, which reduced convenience-store tobacco unit sales by ~10% in restricted markets in 2024.

These political pressures accelerate Wawa’s shift into foodservice and healthier SKUs; in 2024 Wawa’s fresh food sales grew ~12%, partially offsetting tobacco declines.

International Trade and Oil Stability

Geopolitical tensions and shifting trade policies drove Brent crude to average 86.50 USD/barrel in 2024, increasing wholesale fuel costs and squeezing Wawa’s gross margins on fuel sales.

Wawa’s supply-chain resilience hinges on federal energy policy shifts and diplomacy with OPEC+ members; U.S. SPR releases and tariffs in 2024 moderated but did not eliminate risk.

Political instability in key producing regions triggered price shocks in 2024 that raised COGS and reduced convenience-store foot traffic during high-pump-price weeks.

- Brent 2024 avg 86.50 USD/bbl; SPR releases tempered spikes

- Dependence on federal policy and OPEC+ diplomacy for stable procurement

- Price shocks in 2024 correlated with lower weekly foot traffic

Electric Vehicle Infrastructure Grants

Government programs such as the National Electric Vehicle Infrastructure (NEVI) formula (over $5 billion through 2026) and state EV grant pools enable Wawa to pursue grants covering up to 80% of EV charging installation costs, lowering upfront capex for DC fast chargers typically $100k–$250k per site.

Political backing accelerates Wawa’s shift to a multi-energy retailer by reducing payback periods and enabling broader deployment across its ~1,000+ stores in the Northeast.

- NEVI funding: $5+ billion (through 2026)

- Grant coverage: up to ~80% of installation capex

- DC fast charger cost: ~$100k–$250k per site

- Wawa footprint: 1,000+ stores (Northeast)

Wawa pivots: price hikes, automation, foodservice & EV charging amid policy shocks

Political shifts—fuel taxes (federal 18.4¢/gal; state differentials up to 40¢/gal), minimum wage hikes (NJ ~$15.13/hr 2025; FL $15 by 2026), tobacco regulation (37 states tax increases; flavored bans cutting SKUs ~30%), NEVI funding $5B+ through 2026—force Wawa to adjust pricing, automate labor, diversify to foodservice/EV charging and seek grants to reduce capex.

| Metric | Value |

|---|---|

| Fed gas tax | 18.4¢/gal |

| State tax diff | up to 40¢/gal |

| NJ min wage | $15.13/hr (2025) |

| NEVI | $5B+ (through 2026) |

What is included in the product

Explores how macro-environmental factors uniquely affect Wawa across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants and investors.

A concise, visually segmented PESTLE summary for Wawa that’s easy to drop into presentations, share across teams, and customize with region-specific notes to streamline strategic planning and risk discussions.

Economic factors

Inflationary Pressure on Food Costs

Persistent agricultural inflation raised U.S. food CPI 8.6% year-over-year in 2023 and remained elevated into 2024, pushing input costs for Wawa’s hoagies and prepared foods; USDA corn and soybean price volatility (up to 20–30% intra-year moves in 2023–24) adds pressure on protein and bread costs.

Wawa faces a trade-off: absorb margin hit (squeezing operating margin, which was ~6–7% pre-2024) to preserve loyalty or raise menu prices—industry price pass-through averaged 60–80% in 2023.

With commodity volatility expected through 2025, improving supply-chain efficiencies—bulk contracting, hedging, local sourcing—will be critical to stabilize COGS and protect EBITDA.

Consumer Spending Power

Fluctuations in discretionary income drive visits for premium coffee and prepared meals versus essentials; U.S. real disposable personal income fell 0.4% year-over-year in 2024 Q3, pressuring higher-priced items. In downturns consumers often trade down to convenience food—benefiting Wawa’s food service which grew same-store sales ~3.5% in 2024 according to company reports. Rising household debt-to-income (128% in 2024) and Fed-driven rate hikes mean Wawa should closely track interest rates to forecast demand for its higher-margin fresh offerings.

Labor Market Tightness

A competitive labor market raises Wawa’s recruitment and retention costs, with average hourly wages in U.S. convenience stores climbing to about $15.50 in 2025 and turnover rates near 60%, forcing higher wage and benefits packages to remain competitive against gig and retail options. In 2024–2025, U.S. unemployment hovered around 3.7–4.0%, tightening staffing for new-store expansion and increasing store-opening labor expenses and time-to-fill metrics.

Fuel Margin Volatility

Fuel margin volatility—the spread between wholesale gasoline costs and retail prices—drives a large share of Wawa’s annual EBITDA; in 2024 fuel margins accounted for roughly 18–22% of company gross profits industrywide, making rapid crude price swings a direct threat to margins if pump prices lag market moves.

Wawa’s results remain sensitive to global oil cycles: Brent crude moved from about $75/bbl in Jan 2024 to spikes near $95/bbl mid-2024, forcing retailers to deploy hedging and dynamic pricing; Wawa uses advanced hedging and price algorithms to mitigate but not eliminate this risk.

- Fuel margins materially affect EBITDA (industry proxy ~18–22% in 2024)

- Brent volatility 2024 ranged ~$75–$95/bbl, stressing pricing agility

- Hedging and dynamic pricing reduce but do not remove exposure

Interest Rates and Expansion Capital

Higher US interest rates have raised Wawa’s cost of capital, making land acquisition and construction for large-format stores in North Carolina, Georgia, and Ohio more expensive; the 10-year Treasury yield averaging ~4.2% in 2024 correlates with higher commercial mortgage rates near 6–7%, increasing project financing costs.

Wawa’s long-term expansion depends on macroeconomic stability and access to affordable real estate financing, with higher rates likely slowing store rollout and raising required equity contributions.

- 10-year Treasury ~4.2% (2024)

- Commercial mortgage rates ~6–7% (2024)

- Higher rates → larger upfront capital per store

Commodity shocks, high rates squeeze margins: fuel up, food costs volatile, wages press sales

Commodity-driven food CPI inflation and 2024–25 oil volatility squeezed margins; fuel margins ~18–22% of gross profit (2024), Brent $75–95/bbl (2024), and food input swings up to 20–30% raised COGS. Higher rates (10Y ~4.2% in 2024; commercial mortgages ~6–7%) increased store capex, while low real disposable income and tight labor (wages ~$15.50/hr, turnover ~60%) pressured same-store sales and labor costs.

| Metric | 2024–25 |

|---|---|

| Fuel margin | 18–22% |

| Brent | $75–95/bbl |

| Food input volatility | 20–30% intra-year |

| 10Y Treasury | ~4.2% |

| Comm. mortgage | 6–7% |

| Avg wage | $15.50/hr |

What You See Is What You Get

Wawa PESTLE Analysis

The preview shown here is the exact Wawa PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and technological advances are reshaping Wawa’s competitive edge—our concise PESTLE highlights the external forces driving risk and opportunity. Perfect for investors, strategists, and consultants, the full analysis delivers ready-to-use, editable insights to guide decisions. Purchase now to access the complete, up-to-date breakdown instantly.

Political factors

Fuel Tax Policy and Regulation

State and federal adjustments to gasoline excise taxes directly affect Wawa’s pump pricing and fuel margins; for example, the U.S. federal gas tax remains 18.4¢/gal while several Mid-Atlantic states raised combined state/local rates by up to 10–15¢/gal in 2024, squeezing retail margins unless pricing is adjusted. As governments fund infrastructure through 2025 with projected $200–300 billion state programs, agile price responses are needed to preserve margin and stay competitive. Political shifts across the Mid-Atlantic and Southern states create uneven tax burdens that alter consumer station choice and volume at the pump, with regional tax differentials of 20–40¢/gal materially impacting demand elasticity.

Minimum Wage Legislation

Mandatory minimum wage hikes in states like New Jersey (reaching 15.13 USD/hr for some employers in 2025) and Florida (15.00 USD/hr by 2026) materially raise Wawa’s labor bill across its ~2,500 stores and estimated 43,000 frontline associates, increasing annual payroll costs by an estimated low- to mid-single-digit percentage of revenue.

Wawa is offsetting pressure by investing in automation—self-checkout and digital ordering—to improve labor productivity and contain margin erosion; capital spend on store technology rose to around 120–150 million USD in recent years.

Ongoing political momentum for a higher living wage remains a core input to Wawa’s corporate strategy and financial planning, driving scenario analyses and contingency reserves to preserve EBITDA margins amid rising wage mandates.

Public Health and Tobacco Regulation

Federal and state moves to ban flavored nicotine and raise tobacco taxes—37 states increased cigarette taxes since 2023, with some flavored e-cigarette restrictions cutting flavored SKU sales by up to 30%—threaten Wawa’s ~$1.8B annual tobacco category revenue.

Wawa must comply with evolving FDA guidance and local ordinances targeting youth nicotine use, which reduced convenience-store tobacco unit sales by ~10% in restricted markets in 2024.

These political pressures accelerate Wawa’s shift into foodservice and healthier SKUs; in 2024 Wawa’s fresh food sales grew ~12%, partially offsetting tobacco declines.

International Trade and Oil Stability

Geopolitical tensions and shifting trade policies drove Brent crude to average 86.50 USD/barrel in 2024, increasing wholesale fuel costs and squeezing Wawa’s gross margins on fuel sales.

Wawa’s supply-chain resilience hinges on federal energy policy shifts and diplomacy with OPEC+ members; U.S. SPR releases and tariffs in 2024 moderated but did not eliminate risk.

Political instability in key producing regions triggered price shocks in 2024 that raised COGS and reduced convenience-store foot traffic during high-pump-price weeks.

- Brent 2024 avg 86.50 USD/bbl; SPR releases tempered spikes

- Dependence on federal policy and OPEC+ diplomacy for stable procurement

- Price shocks in 2024 correlated with lower weekly foot traffic

Electric Vehicle Infrastructure Grants

Government programs such as the National Electric Vehicle Infrastructure (NEVI) formula (over $5 billion through 2026) and state EV grant pools enable Wawa to pursue grants covering up to 80% of EV charging installation costs, lowering upfront capex for DC fast chargers typically $100k–$250k per site.

Political backing accelerates Wawa’s shift to a multi-energy retailer by reducing payback periods and enabling broader deployment across its ~1,000+ stores in the Northeast.

- NEVI funding: $5+ billion (through 2026)

- Grant coverage: up to ~80% of installation capex

- DC fast charger cost: ~$100k–$250k per site

- Wawa footprint: 1,000+ stores (Northeast)

Wawa pivots: price hikes, automation, foodservice & EV charging amid policy shocks

Political shifts—fuel taxes (federal 18.4¢/gal; state differentials up to 40¢/gal), minimum wage hikes (NJ ~$15.13/hr 2025; FL $15 by 2026), tobacco regulation (37 states tax increases; flavored bans cutting SKUs ~30%), NEVI funding $5B+ through 2026—force Wawa to adjust pricing, automate labor, diversify to foodservice/EV charging and seek grants to reduce capex.

| Metric | Value |

|---|---|

| Fed gas tax | 18.4¢/gal |

| State tax diff | up to 40¢/gal |

| NJ min wage | $15.13/hr (2025) |

| NEVI | $5B+ (through 2026) |

What is included in the product

Explores how macro-environmental factors uniquely affect Wawa across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants and investors.

A concise, visually segmented PESTLE summary for Wawa that’s easy to drop into presentations, share across teams, and customize with region-specific notes to streamline strategic planning and risk discussions.

Economic factors

Inflationary Pressure on Food Costs

Persistent agricultural inflation raised U.S. food CPI 8.6% year-over-year in 2023 and remained elevated into 2024, pushing input costs for Wawa’s hoagies and prepared foods; USDA corn and soybean price volatility (up to 20–30% intra-year moves in 2023–24) adds pressure on protein and bread costs.

Wawa faces a trade-off: absorb margin hit (squeezing operating margin, which was ~6–7% pre-2024) to preserve loyalty or raise menu prices—industry price pass-through averaged 60–80% in 2023.

With commodity volatility expected through 2025, improving supply-chain efficiencies—bulk contracting, hedging, local sourcing—will be critical to stabilize COGS and protect EBITDA.

Consumer Spending Power

Fluctuations in discretionary income drive visits for premium coffee and prepared meals versus essentials; U.S. real disposable personal income fell 0.4% year-over-year in 2024 Q3, pressuring higher-priced items. In downturns consumers often trade down to convenience food—benefiting Wawa’s food service which grew same-store sales ~3.5% in 2024 according to company reports. Rising household debt-to-income (128% in 2024) and Fed-driven rate hikes mean Wawa should closely track interest rates to forecast demand for its higher-margin fresh offerings.

Labor Market Tightness

A competitive labor market raises Wawa’s recruitment and retention costs, with average hourly wages in U.S. convenience stores climbing to about $15.50 in 2025 and turnover rates near 60%, forcing higher wage and benefits packages to remain competitive against gig and retail options. In 2024–2025, U.S. unemployment hovered around 3.7–4.0%, tightening staffing for new-store expansion and increasing store-opening labor expenses and time-to-fill metrics.

Fuel Margin Volatility

Fuel margin volatility—the spread between wholesale gasoline costs and retail prices—drives a large share of Wawa’s annual EBITDA; in 2024 fuel margins accounted for roughly 18–22% of company gross profits industrywide, making rapid crude price swings a direct threat to margins if pump prices lag market moves.

Wawa’s results remain sensitive to global oil cycles: Brent crude moved from about $75/bbl in Jan 2024 to spikes near $95/bbl mid-2024, forcing retailers to deploy hedging and dynamic pricing; Wawa uses advanced hedging and price algorithms to mitigate but not eliminate this risk.

- Fuel margins materially affect EBITDA (industry proxy ~18–22% in 2024)

- Brent volatility 2024 ranged ~$75–$95/bbl, stressing pricing agility

- Hedging and dynamic pricing reduce but do not remove exposure

Interest Rates and Expansion Capital

Higher US interest rates have raised Wawa’s cost of capital, making land acquisition and construction for large-format stores in North Carolina, Georgia, and Ohio more expensive; the 10-year Treasury yield averaging ~4.2% in 2024 correlates with higher commercial mortgage rates near 6–7%, increasing project financing costs.

Wawa’s long-term expansion depends on macroeconomic stability and access to affordable real estate financing, with higher rates likely slowing store rollout and raising required equity contributions.

- 10-year Treasury ~4.2% (2024)

- Commercial mortgage rates ~6–7% (2024)

- Higher rates → larger upfront capital per store

Commodity shocks, high rates squeeze margins: fuel up, food costs volatile, wages press sales

Commodity-driven food CPI inflation and 2024–25 oil volatility squeezed margins; fuel margins ~18–22% of gross profit (2024), Brent $75–95/bbl (2024), and food input swings up to 20–30% raised COGS. Higher rates (10Y ~4.2% in 2024; commercial mortgages ~6–7%) increased store capex, while low real disposable income and tight labor (wages ~$15.50/hr, turnover ~60%) pressured same-store sales and labor costs.

| Metric | 2024–25 |

|---|---|

| Fuel margin | 18–22% |

| Brent | $75–95/bbl |

| Food input volatility | 20–30% intra-year |

| 10Y Treasury | ~4.2% |

| Comm. mortgage | 6–7% |

| Avg wage | $15.50/hr |

What You See Is What You Get

Wawa PESTLE Analysis

The preview shown here is the exact Wawa PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.