Wayfair Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

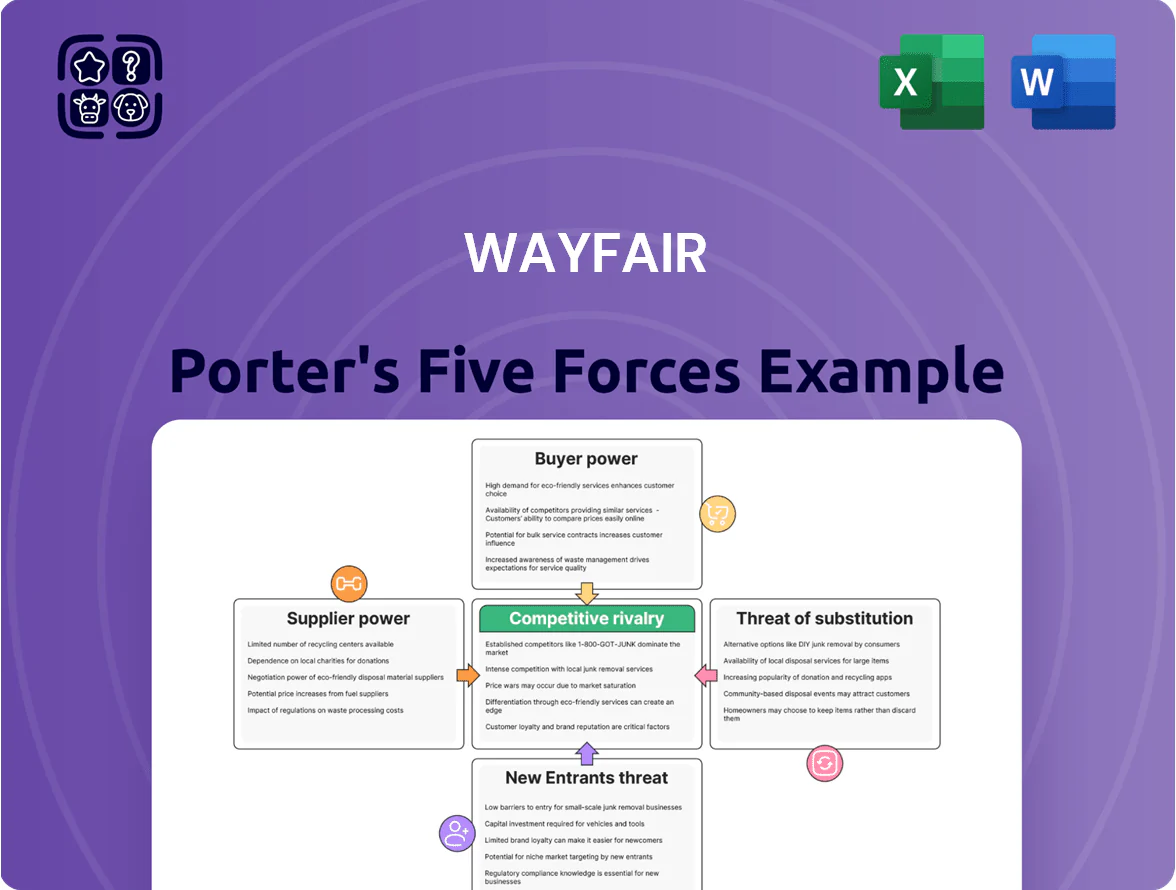

Wayfair faces intense rivalry from e-commerce giants and niche home retailers, while customer price sensitivity and logistics costs heighten competitive pressure; supplier leverage is moderate due to scale but product differentiation limits full control.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wayfair’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Supplier Network

Wayfair partners with over 20,000 suppliers, so no single vendor can command pricing or terms; supplier concentration is low and bargaining power is minimal. This fragmentation lets Wayfair swap underperforming sellers quickly, protecting catalog depth and revenue—Wayfair reported ~13,000 active sellers on Marketplace in 2024 but cites over 20,000 total supplier relationships through 2025. Low supplier leverage limits margin pressure.

Integration into CastleGate Logistics

Suppliers using Wayfair’s proprietary CastleGate logistics network become operationally integrated, creating lock-in since switching fulfillment would require complex rerouting and data migration across SKUs and EDI systems.

That lock-in lets Wayfair extract favorable terms: CastleGate-enabled suppliers accounted for about 42% of its active merchant volume in Q3 2025, supporting lower per-unit freight costs and extended payment terms.

Moving off CastleGate typically raises logistics cost estimates by 10–18% and increases lead-time variability, so partners tend to accept tighter pricing to stay within the ecosystem.

Expansion of House Brands

Wayfair’s push into house brands cut supplier leverage: private-label sales grew to about 18% of GMV in 2024, reducing reliance on external names and pushing third-party vendors to lower prices or improve quality to keep search placement; suppliers face higher promo spend and thinner margins as Wayfair controls branding on many top-selling SKUs, weakening manufacturer bargaining power and concentrating negotiating leverage with the platform.

Low Differentiation in Mass Market Goods

- High SKU fungibility limits supplier pricing power

- Multiple global sources enable rapid procurement shifts

- 2024 GMV $13.7B supports scale-driven bargaining

- Generic items lower supplier differentiation and margins

Supplier Dependence on Digital Traffic

Wayfair’s supplier power weak—scale, CastleGate and private labels lock pricing

Suppliers have low bargaining power: over 20,000 suppliers and ~13,000 active sellers in 2024 dilute leverage, while Wayfair’s CastleGate logistics (≈42% merchant volume Q3 2025) and 18% private-label GMV in 2024 create switching costs and pricing power for Wayfair, with typical commissions 15–25% and vendor dependence of 60–80% of sales.

| Metric | Value |

|---|---|

| Suppliers (total) | 20,000+ |

| Active sellers (2024) | ~13,000 |

| CastleGate share (Q3 2025) | ≈42% |

| Private-label of GMV (2024) | 18% |

| GMV (2024) | $13.7B |

| Vendor dependence | 60–80% |

| Typical commissions | 15–25% |

What is included in the product

Tailored exclusively for Wayfair, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its pricing, profitability, and market position.

Quickly assess Wayfair’s competitive landscape with a one-sheet Porter's Five Forces summary—ideal for board slides or rapid investment calls, customizable to reflect shifts in supplier power, buyer behavior, new entrants, substitutes, and competitive rivalry.

Customers Bargaining Power

Minimal Switching Costs

Customers can jump from Wayfair to Amazon or Walmart in seconds via web or app, and with no contracts or subscriptions blocking them; in 2024 US ecommerce, 44% of consumers shopped across multiple marketplaces monthly, raising churn risk.

High Price Transparency

Online shoppers in 2025 use comparison engines and AI assistants to find lowest prices for specific furniture styles, and 68% of US consumers report using at least one price-comparison tool when buying home goods (2024 Pew/Commerce survey). Because Wayfair sells many non-exclusive items in a transparent digital market, it struggles to hide price gaps or sustain high margins on those SKUs. This visibility lets customers demand top value, pressuring gross margins and forcing frequent promotions.

Abundance of Choice

The market is saturated with retailers from discount giants like Walmart and Amazon to high-end showrooms; US furniture e‑commerce sales hit $80.8B in 2023, up 6% year-over-year, giving customers near-infinite style and price options so they can easily switch platforms. That abundance forces Wayfair to invest in UX, logistics, and curated assortments—Wayfair spent $1.1B on marketing and fulfillment in 2024—to retain share.

Access to Peer Reviews

Shoppers on Wayfair rely heavily on millions of user reviews and photos—Wayfair reported 80+ million product reviews sitewide in 2024—so social proof strongly shapes purchase decisions.

Negative feedback is immediate and public; a drop in product or service quality can shift traffic fast to Amazon or Overstock, cutting conversion and raising return rates.

This collective voice gives customers real bargaining power over Wayfair’s reputation and quality standards.

- 80+ million reviews (2024)

- Instant public feedback shifts traffic

- Social proof drives returns and conversion

Expectations for Free Shipping

Expectations for free shipping have become non-negotiable; US e-commerce data shows 80% of shoppers in 2024 expect free shipping and 46% abandon carts over shipping costs, pressuring Wayfair to subsidize logistics to retain volume.

This forces Wayfair to absorb higher fulfillment costs—shipping and handling rose as a percent of revenue to ~9% in FY2024—squeezing gross margins while keeping prices competitive.

- 80% of US shoppers expect free shipping (2024)

- 46% abandon carts for high shipping costs (2024)

- Wayfair shipping/fulfillment ≈9% of revenue (FY2024)

- Customer unwillingness to pay delivery premium

Customers Hold Power: Price Tools, Reviews Drive Promotions & $1.1B Fulfillment Costs

Customers hold strong leverage: easy switching to Amazon/Walmart, 68% use price-comparison tools (2024), and social proof (80+M reviews in 2024) rapidly shifts demand, forcing frequent promotions and heavy spend on UX/logistics (Wayfair spent $1.1B on marketing/fulfillment in 2024; shipping ≈9% of revenue FY2024).

| Metric | Value |

|---|---|

| Price tools use | 68% (2024) |

| Product reviews | 80+M (2024) |

| Marketing/fulfillment spend | $1.1B (2024) |

| Shipping % of revenue | ~9% (FY2024) |

Full Version Awaits

Wayfair Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Wayfair you'll receive immediately after purchase—no placeholders or abridgments.

The document displayed is the full, professionally formatted file, ready for download and use the moment you buy.

No mockups or samples: this is the actual deliverable and will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Wayfair faces intense rivalry from e-commerce giants and niche home retailers, while customer price sensitivity and logistics costs heighten competitive pressure; supplier leverage is moderate due to scale but product differentiation limits full control.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wayfair’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Supplier Network

Wayfair partners with over 20,000 suppliers, so no single vendor can command pricing or terms; supplier concentration is low and bargaining power is minimal. This fragmentation lets Wayfair swap underperforming sellers quickly, protecting catalog depth and revenue—Wayfair reported ~13,000 active sellers on Marketplace in 2024 but cites over 20,000 total supplier relationships through 2025. Low supplier leverage limits margin pressure.

Integration into CastleGate Logistics

Suppliers using Wayfair’s proprietary CastleGate logistics network become operationally integrated, creating lock-in since switching fulfillment would require complex rerouting and data migration across SKUs and EDI systems.

That lock-in lets Wayfair extract favorable terms: CastleGate-enabled suppliers accounted for about 42% of its active merchant volume in Q3 2025, supporting lower per-unit freight costs and extended payment terms.

Moving off CastleGate typically raises logistics cost estimates by 10–18% and increases lead-time variability, so partners tend to accept tighter pricing to stay within the ecosystem.

Expansion of House Brands

Wayfair’s push into house brands cut supplier leverage: private-label sales grew to about 18% of GMV in 2024, reducing reliance on external names and pushing third-party vendors to lower prices or improve quality to keep search placement; suppliers face higher promo spend and thinner margins as Wayfair controls branding on many top-selling SKUs, weakening manufacturer bargaining power and concentrating negotiating leverage with the platform.

Low Differentiation in Mass Market Goods

- High SKU fungibility limits supplier pricing power

- Multiple global sources enable rapid procurement shifts

- 2024 GMV $13.7B supports scale-driven bargaining

- Generic items lower supplier differentiation and margins

Supplier Dependence on Digital Traffic

Wayfair’s supplier power weak—scale, CastleGate and private labels lock pricing

Suppliers have low bargaining power: over 20,000 suppliers and ~13,000 active sellers in 2024 dilute leverage, while Wayfair’s CastleGate logistics (≈42% merchant volume Q3 2025) and 18% private-label GMV in 2024 create switching costs and pricing power for Wayfair, with typical commissions 15–25% and vendor dependence of 60–80% of sales.

| Metric | Value |

|---|---|

| Suppliers (total) | 20,000+ |

| Active sellers (2024) | ~13,000 |

| CastleGate share (Q3 2025) | ≈42% |

| Private-label of GMV (2024) | 18% |

| GMV (2024) | $13.7B |

| Vendor dependence | 60–80% |

| Typical commissions | 15–25% |

What is included in the product

Tailored exclusively for Wayfair, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its pricing, profitability, and market position.

Quickly assess Wayfair’s competitive landscape with a one-sheet Porter's Five Forces summary—ideal for board slides or rapid investment calls, customizable to reflect shifts in supplier power, buyer behavior, new entrants, substitutes, and competitive rivalry.

Customers Bargaining Power

Minimal Switching Costs

Customers can jump from Wayfair to Amazon or Walmart in seconds via web or app, and with no contracts or subscriptions blocking them; in 2024 US ecommerce, 44% of consumers shopped across multiple marketplaces monthly, raising churn risk.

High Price Transparency

Online shoppers in 2025 use comparison engines and AI assistants to find lowest prices for specific furniture styles, and 68% of US consumers report using at least one price-comparison tool when buying home goods (2024 Pew/Commerce survey). Because Wayfair sells many non-exclusive items in a transparent digital market, it struggles to hide price gaps or sustain high margins on those SKUs. This visibility lets customers demand top value, pressuring gross margins and forcing frequent promotions.

Abundance of Choice

The market is saturated with retailers from discount giants like Walmart and Amazon to high-end showrooms; US furniture e‑commerce sales hit $80.8B in 2023, up 6% year-over-year, giving customers near-infinite style and price options so they can easily switch platforms. That abundance forces Wayfair to invest in UX, logistics, and curated assortments—Wayfair spent $1.1B on marketing and fulfillment in 2024—to retain share.

Access to Peer Reviews

Shoppers on Wayfair rely heavily on millions of user reviews and photos—Wayfair reported 80+ million product reviews sitewide in 2024—so social proof strongly shapes purchase decisions.

Negative feedback is immediate and public; a drop in product or service quality can shift traffic fast to Amazon or Overstock, cutting conversion and raising return rates.

This collective voice gives customers real bargaining power over Wayfair’s reputation and quality standards.

- 80+ million reviews (2024)

- Instant public feedback shifts traffic

- Social proof drives returns and conversion

Expectations for Free Shipping

Expectations for free shipping have become non-negotiable; US e-commerce data shows 80% of shoppers in 2024 expect free shipping and 46% abandon carts over shipping costs, pressuring Wayfair to subsidize logistics to retain volume.

This forces Wayfair to absorb higher fulfillment costs—shipping and handling rose as a percent of revenue to ~9% in FY2024—squeezing gross margins while keeping prices competitive.

- 80% of US shoppers expect free shipping (2024)

- 46% abandon carts for high shipping costs (2024)

- Wayfair shipping/fulfillment ≈9% of revenue (FY2024)

- Customer unwillingness to pay delivery premium

Customers Hold Power: Price Tools, Reviews Drive Promotions & $1.1B Fulfillment Costs

Customers hold strong leverage: easy switching to Amazon/Walmart, 68% use price-comparison tools (2024), and social proof (80+M reviews in 2024) rapidly shifts demand, forcing frequent promotions and heavy spend on UX/logistics (Wayfair spent $1.1B on marketing/fulfillment in 2024; shipping ≈9% of revenue FY2024).

| Metric | Value |

|---|---|

| Price tools use | 68% (2024) |

| Product reviews | 80+M (2024) |

| Marketing/fulfillment spend | $1.1B (2024) |

| Shipping % of revenue | ~9% (FY2024) |

Full Version Awaits

Wayfair Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Wayfair you'll receive immediately after purchase—no placeholders or abridgments.

The document displayed is the full, professionally formatted file, ready for download and use the moment you buy.

No mockups or samples: this is the actual deliverable and will be available to you instantly after payment.