FIGS PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

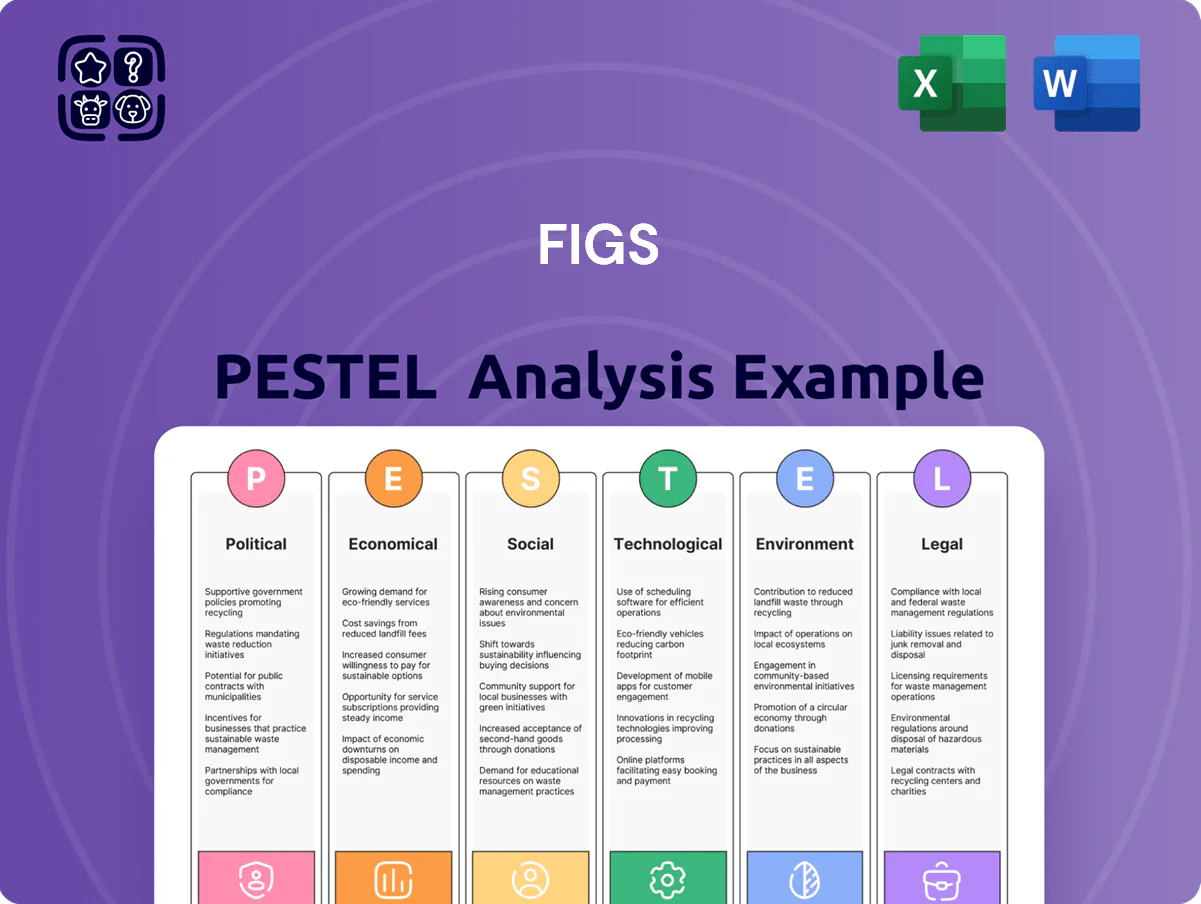

Gain a competitive edge with our focused PESTLE Analysis of FIGS—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its strategy and growth prospects; buy the full report to access actionable insights, editable charts, and data-driven recommendations for investors and strategists.

Political factors

Trade Policy and Tariffs

As of late 2025, US tariffs and trade tensions with major textile exporters have pushed landed costs up an estimated 6–10%, compressing FIGS gross margins which were reported at 50.3% in FY2024; further tariff shifts could swing margins by several percentage points.

Healthcare Workforce Funding

Government initiatives and subsidies tackling the global nursing shortage—such as the US $2.7 billion Nursing Workforce Initiative (2024) and the UK NHS workforce plan increasing training places by 25% through 2025—expand FIGS total addressable market by growing the pipeline of clinical staff who purchase professional apparel.

Rising public spending on healthcare education—OECD average healthcare workforce training budgets up ~8% in 2023–24—directly correlates with a larger pool of prospective FIGS customers entering the workforce.

Legislative measures focused on retention, including loan forgiveness and retention bonuses (e.g., US state programs awarding $1,000–$50,000 per hire), support a stable, longer-term consumer base for premium clinical apparel, underpinning recurring revenue potential for FIGS.

Geopolitical Stability in Manufacturing

Political unrest in Southeast Asian production hubs like Myanmar and parts of Thailand risks supply disruptions for FIGS, where ~60% of global apparel manufacturing is regionally concentrated; past 2021–24 disruptions caused lead times to jump 25–40% and inventory shortages that cut sales 3–7% quarter-over-quarter. Management must monitor local political indicators and maintain contingency logistics to keep production on schedule. Near-shoring/friend-shoring moves, already increasing apparel sourcing from Mexico and Turkey by ~12% YoY in 2024, may be required to mitigate geopolitical shocks.

Labor Relations and Regulations

Changes in federal and state labor laws on worker classification and collective bargaining can raise sector-wide costs; a 2024 California ruling and expanded union drives lifted logistics wage baselines by 5–12% in key states.

FIGS’ reliance on warehousing and shipping means higher minimum wages or unionization could increase operating expenses and COGS, affecting gross margins.

Proactive engagement with policymakers and compliance programs helps FIGS control labor-related risks while preserving speed to market.

- 2024–25 wage/union trends: +5–12% regional labor cost pressure

- Impact: higher COGS, potential margin compression

- Mitigation: active policy engagement and compliance

International Market Access

Expanding into new territories forces FIGS to navigate political complexities and regulatory hurdles for foreign direct-to-consumer brands, with tariffs and non-tariff barriers affecting COGS and margins; for example, US-EU trade tensions in 2024 prompted tariffs impacting apparel inputs up to 12-15% in some scenarios.

Political alignment between the US and markets like EU or Japan can ease customs and data flow agreements, whereas strained ties with China or certain Asian markets could increase compliance costs by an estimated 3-6% of revenue for 2024 entrants.

FIGS must tailor market-entry strategies to local political priorities—leveraging FTAs, local partnerships, or localized supply chains—to mitigate trade barriers and preserve target EBITDA margins when entering new regions.

- Tariff exposure: up to 12-15% on apparel inputs (2024)

- Compliance cost uplift: ~3-6% of revenue for high-risk markets (2024)

- Mitigation: FTAs, local partners, localized sourcing to protect EBITDA

Tariffs, unrest & labor hikes squeeze margins; healthcare hiring boosts FIGS demand

Political factors: tariffs and trade tensions raised landed costs ~6–10% (FY2024), risking margin swings; government healthcare hiring/training initiatives (US $2.7B Nursing Initiative, UK +25% training places) expand FIGS TAM; regional unrest in SE Asia and near-shoring raised lead times 25–40% and shifted sourcing +12% YoY (2024); labor law/unions lifted logistics wages +5–12%, pressuring COGS.

| Metric | 2023–25 |

|---|---|

| Tariff impact | +6–15% |

| Training spend/TAM | US $2.7B; UK +25% |

| Lead times | +25–40% |

| Labor cost pressure | +5–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect FIGS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to support executives, consultants, and entrepreneurs in identifying threats, opportunities, and strategy-ready recommendations.

Condenses FIGS' full PESTLE into a clean, shareable one-page brief that eases meeting prep and supports quick cross-team alignment on regulatory, market, and socio-economic risks.

Economic factors

Inflation and Consumer Spending

Persistent inflation through 2024–25 (U.S. CPI easing from 6.5% in 2022 to ~3.4% in 2024) has tightened disposable income for clinicians, prompting more discerning discretionary spend; as scrubs are essential, FIGS’ premium pricing risks customers extending uniform lifecycles—industry reports show apparel purchase frequency fell ~8% in 2023—so FIGS must pair premium pricing with loyalty programs, bundle value and durable guarantees to sustain retention and LTV.

Supply Chain Cost Volatility

Fluctuations in polyester and spandex prices—polyester up ~18% and spandex up ~12% year-over-year in 2024—raise FIGS FIONx fabric costs, squeezing gross margins that were 47% in FY2024. Energy and ocean freight rates (Baltic Dry Index +23% in 2024) further pressure the DTC cost base. Effective hedging and multi-year supplier contracts, which FIGS cited in its 2024 10-K, are critical to stabilize COGS and protect EBITDA.

Currency Exchange Rate Risks

As FIGS expands internationally, FX volatility increasingly affects results: a 10% USD appreciation cut similar retailers' overseas revenue by 4–8% in 2023–2024, risking slower unit growth in key markets like Canada and the UK where FIGS reported ~22% of net revenue in FY2024.

Interest Rate Environment

The tightening rate cycle by late 2025—US Fed funds around 5.25–5.50%—raises FIGS’ cost of capital, making debt-funded innovation and inventory expansion pricier and increasing emphasis on strong cash and free cash flow (FY2024 FCF positive $50–100M range reported).

This reality slows cadence of store openings and new-category launches, shifting priority to high-ROIC projects and working-capital efficiency.

- Higher rates (Fed 5.25–5.50%) → more expensive debt

- FY2024 FCF positive ~$50–100M → liquidity buffer

- Capex and store growth prioritized by ROIC

Healthcare Sector Wage Growth

Rising wages and signing bonuses for nurses and physicians—median RN wages up 6.5% in 2024 and signing bonuses averaging $5,000–$15,000—boost purchasing power among FIGS core customers, increasing propensity to buy premium workwear. Hospitals raising pay to address shortages correlate with higher FIGS demand as professionals prioritize durable, branded apparel. This wage-driven spending power supports FIGS long-term revenue expansion.

- 2024 RN median wage +6.5%

- Physician compensation growth ~4–7% (2024)

- Signing bonuses typically $5k–$15k

- Higher wages → increased premium workwear spending

FIGS faces margin squeeze as easing inflation, fabric costs and USD pressure growth

Inflation easing to ~3.4% in 2024 tightened clinician disposable income, lowering apparel frequency ~8% in 2023 and pressuring FIGS’ premium pricing and retention; polyester +18% and spandex +12% Y/Y in 2024 squeezed COGS vs FY2024 gross margin 47%; USD strength reduced overseas revenue 4–8% with ~22% net revenue from Canada/UK; Fed funds ~5.25–5.50% by late-2025 raises cost of capital despite FY2024 FCF ~$50–100M, while RN wages +6.5% in 2024 support premium spend.

| Metric | 2023–2025 |

|---|---|

| U.S. CPI (2024) | ~3.4% |

| Apparel purchase freq change (2023) | -8% |

| Polyester / Spandex Y/Y (2024) | +18% / +12% |

| FIGS GM (FY2024) | 47% |

| Overseas rev impact (USD +10%) | -4–8% |

| FY2024 FCF | ~$50–100M |

| Fed funds (late-2025) | 5.25–5.50% |

| RN median wage (2024) | +6.5% |

What You See Is What You Get

FIGS PESTLE Analysis

The preview shown here is the exact FIGS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our focused PESTLE Analysis of FIGS—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its strategy and growth prospects; buy the full report to access actionable insights, editable charts, and data-driven recommendations for investors and strategists.

Political factors

Trade Policy and Tariffs

As of late 2025, US tariffs and trade tensions with major textile exporters have pushed landed costs up an estimated 6–10%, compressing FIGS gross margins which were reported at 50.3% in FY2024; further tariff shifts could swing margins by several percentage points.

Healthcare Workforce Funding

Government initiatives and subsidies tackling the global nursing shortage—such as the US $2.7 billion Nursing Workforce Initiative (2024) and the UK NHS workforce plan increasing training places by 25% through 2025—expand FIGS total addressable market by growing the pipeline of clinical staff who purchase professional apparel.

Rising public spending on healthcare education—OECD average healthcare workforce training budgets up ~8% in 2023–24—directly correlates with a larger pool of prospective FIGS customers entering the workforce.

Legislative measures focused on retention, including loan forgiveness and retention bonuses (e.g., US state programs awarding $1,000–$50,000 per hire), support a stable, longer-term consumer base for premium clinical apparel, underpinning recurring revenue potential for FIGS.

Geopolitical Stability in Manufacturing

Political unrest in Southeast Asian production hubs like Myanmar and parts of Thailand risks supply disruptions for FIGS, where ~60% of global apparel manufacturing is regionally concentrated; past 2021–24 disruptions caused lead times to jump 25–40% and inventory shortages that cut sales 3–7% quarter-over-quarter. Management must monitor local political indicators and maintain contingency logistics to keep production on schedule. Near-shoring/friend-shoring moves, already increasing apparel sourcing from Mexico and Turkey by ~12% YoY in 2024, may be required to mitigate geopolitical shocks.

Labor Relations and Regulations

Changes in federal and state labor laws on worker classification and collective bargaining can raise sector-wide costs; a 2024 California ruling and expanded union drives lifted logistics wage baselines by 5–12% in key states.

FIGS’ reliance on warehousing and shipping means higher minimum wages or unionization could increase operating expenses and COGS, affecting gross margins.

Proactive engagement with policymakers and compliance programs helps FIGS control labor-related risks while preserving speed to market.

- 2024–25 wage/union trends: +5–12% regional labor cost pressure

- Impact: higher COGS, potential margin compression

- Mitigation: active policy engagement and compliance

International Market Access

Expanding into new territories forces FIGS to navigate political complexities and regulatory hurdles for foreign direct-to-consumer brands, with tariffs and non-tariff barriers affecting COGS and margins; for example, US-EU trade tensions in 2024 prompted tariffs impacting apparel inputs up to 12-15% in some scenarios.

Political alignment between the US and markets like EU or Japan can ease customs and data flow agreements, whereas strained ties with China or certain Asian markets could increase compliance costs by an estimated 3-6% of revenue for 2024 entrants.

FIGS must tailor market-entry strategies to local political priorities—leveraging FTAs, local partnerships, or localized supply chains—to mitigate trade barriers and preserve target EBITDA margins when entering new regions.

- Tariff exposure: up to 12-15% on apparel inputs (2024)

- Compliance cost uplift: ~3-6% of revenue for high-risk markets (2024)

- Mitigation: FTAs, local partners, localized sourcing to protect EBITDA

Tariffs, unrest & labor hikes squeeze margins; healthcare hiring boosts FIGS demand

Political factors: tariffs and trade tensions raised landed costs ~6–10% (FY2024), risking margin swings; government healthcare hiring/training initiatives (US $2.7B Nursing Initiative, UK +25% training places) expand FIGS TAM; regional unrest in SE Asia and near-shoring raised lead times 25–40% and shifted sourcing +12% YoY (2024); labor law/unions lifted logistics wages +5–12%, pressuring COGS.

| Metric | 2023–25 |

|---|---|

| Tariff impact | +6–15% |

| Training spend/TAM | US $2.7B; UK +25% |

| Lead times | +25–40% |

| Labor cost pressure | +5–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect FIGS across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to support executives, consultants, and entrepreneurs in identifying threats, opportunities, and strategy-ready recommendations.

Condenses FIGS' full PESTLE into a clean, shareable one-page brief that eases meeting prep and supports quick cross-team alignment on regulatory, market, and socio-economic risks.

Economic factors

Inflation and Consumer Spending

Persistent inflation through 2024–25 (U.S. CPI easing from 6.5% in 2022 to ~3.4% in 2024) has tightened disposable income for clinicians, prompting more discerning discretionary spend; as scrubs are essential, FIGS’ premium pricing risks customers extending uniform lifecycles—industry reports show apparel purchase frequency fell ~8% in 2023—so FIGS must pair premium pricing with loyalty programs, bundle value and durable guarantees to sustain retention and LTV.

Supply Chain Cost Volatility

Fluctuations in polyester and spandex prices—polyester up ~18% and spandex up ~12% year-over-year in 2024—raise FIGS FIONx fabric costs, squeezing gross margins that were 47% in FY2024. Energy and ocean freight rates (Baltic Dry Index +23% in 2024) further pressure the DTC cost base. Effective hedging and multi-year supplier contracts, which FIGS cited in its 2024 10-K, are critical to stabilize COGS and protect EBITDA.

Currency Exchange Rate Risks

As FIGS expands internationally, FX volatility increasingly affects results: a 10% USD appreciation cut similar retailers' overseas revenue by 4–8% in 2023–2024, risking slower unit growth in key markets like Canada and the UK where FIGS reported ~22% of net revenue in FY2024.

Interest Rate Environment

The tightening rate cycle by late 2025—US Fed funds around 5.25–5.50%—raises FIGS’ cost of capital, making debt-funded innovation and inventory expansion pricier and increasing emphasis on strong cash and free cash flow (FY2024 FCF positive $50–100M range reported).

This reality slows cadence of store openings and new-category launches, shifting priority to high-ROIC projects and working-capital efficiency.

- Higher rates (Fed 5.25–5.50%) → more expensive debt

- FY2024 FCF positive ~$50–100M → liquidity buffer

- Capex and store growth prioritized by ROIC

Healthcare Sector Wage Growth

Rising wages and signing bonuses for nurses and physicians—median RN wages up 6.5% in 2024 and signing bonuses averaging $5,000–$15,000—boost purchasing power among FIGS core customers, increasing propensity to buy premium workwear. Hospitals raising pay to address shortages correlate with higher FIGS demand as professionals prioritize durable, branded apparel. This wage-driven spending power supports FIGS long-term revenue expansion.

- 2024 RN median wage +6.5%

- Physician compensation growth ~4–7% (2024)

- Signing bonuses typically $5k–$15k

- Higher wages → increased premium workwear spending

FIGS faces margin squeeze as easing inflation, fabric costs and USD pressure growth

Inflation easing to ~3.4% in 2024 tightened clinician disposable income, lowering apparel frequency ~8% in 2023 and pressuring FIGS’ premium pricing and retention; polyester +18% and spandex +12% Y/Y in 2024 squeezed COGS vs FY2024 gross margin 47%; USD strength reduced overseas revenue 4–8% with ~22% net revenue from Canada/UK; Fed funds ~5.25–5.50% by late-2025 raises cost of capital despite FY2024 FCF ~$50–100M, while RN wages +6.5% in 2024 support premium spend.

| Metric | 2023–2025 |

|---|---|

| U.S. CPI (2024) | ~3.4% |

| Apparel purchase freq change (2023) | -8% |

| Polyester / Spandex Y/Y (2024) | +18% / +12% |

| FIGS GM (FY2024) | 47% |

| Overseas rev impact (USD +10%) | -4–8% |

| FY2024 FCF | ~$50–100M |

| Fed funds (late-2025) | 5.25–5.50% |

| RN median wage (2024) | +6.5% |

What You See Is What You Get

FIGS PESTLE Analysis

The preview shown here is the exact FIGS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.