Webjet Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

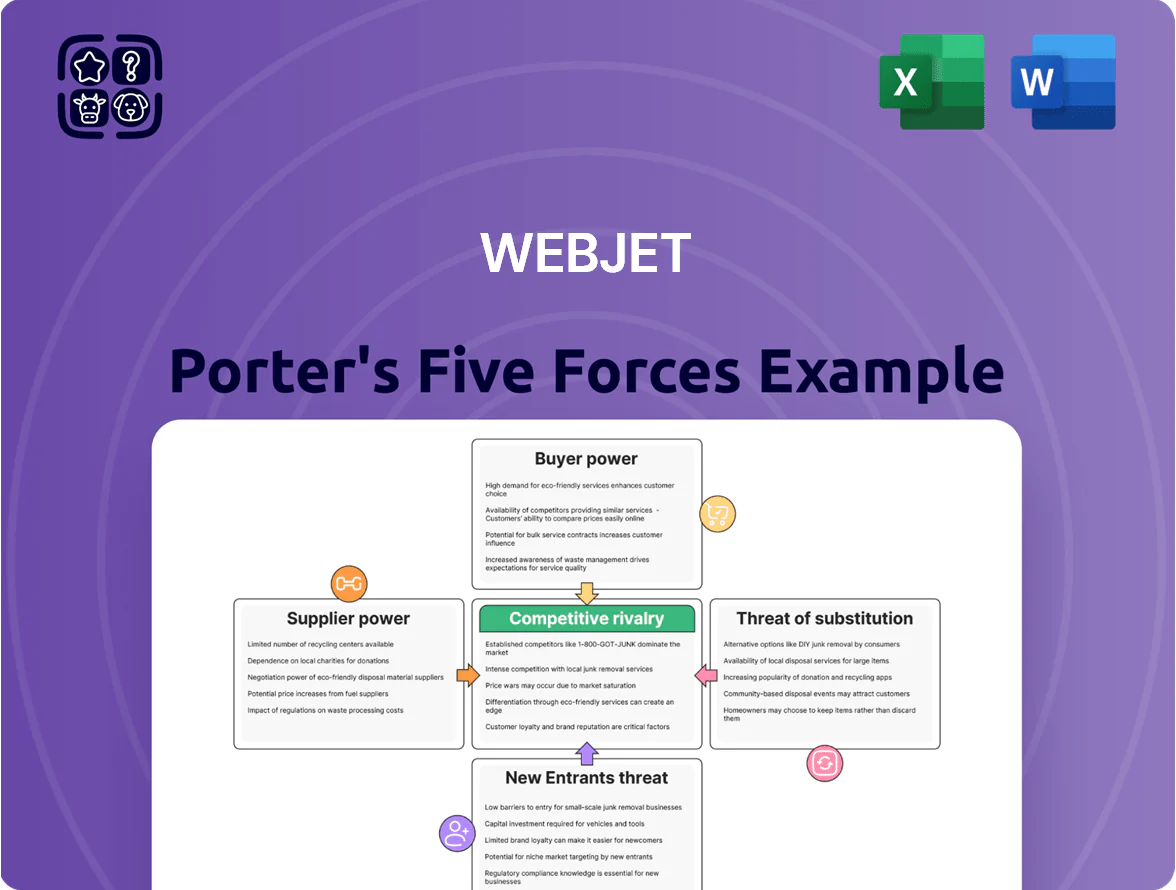

Webjet operates in a high-volume, margin-sensitive travel market where rivalry is fierce, buyer price sensitivity is strong, suppliers (airlines/hotels) hold moderate leverage, substitutes (direct bookings/OTAs) pose real threats, and entry barriers are moderate due to tech scale and brand—this snapshot highlights strategic pressure points and defensive needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Webjet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Domestic Airlines

The Australian and New Zealand aviation markets are highly concentrated: Qantas Group held ~66% domestic market share in Australia in 2024 and Air New Zealand ~60% in NZ, giving them strong leverage over distribution terms. This concentration lets carriers dictate commission rates and fare access, squeezing Webjet OTA margins—Webjet reported 2024 gross margins pressured by ticketing mix shifts. Webjet must keep close ties to secure full inventories and competitive fares for customers.

Fragmentation of Global Hotel Inventory

The global hotel market is highly fragmented versus airlines, shrinking individual supplier power; over 80% of hotels worldwide are independent or in small groups, so few single hotels can dictate terms. WebBeds, Webjet’s B2B arm, aggregates inventory from thousands of such properties—Webjet reported WebBeds had ~200,000 properties in 2024—giving it scale to drive distribution. Because many suppliers lack direct international reach, Webjet secures better rates and flexible payment terms, improving margins and reducing supply-side risk.

Role of Global Distribution Systems

Webjet depends on Global Distribution Systems such as Amadeus and Sabre for live fares and inventory; in 2024 Amadeus reported €6.7bn revenue, showing the scale and leverage of these suppliers.

These GDSs act as critical suppliers via proprietary APIs and standard protocols, so fee hikes or new tech mandates could raise Webjet’s operating costs materially.

Webjet’s FY2024 gross transaction value of ~A$6.1bn gives some bargaining buffer, but supplier power remains high due to limited alternatives.

Direct Distribution Strategies

Airlines and hotel groups pushed direct booking: by 2024, global carriers reported a 12–18% lift in direct web bookings after loyalty incentives, cutting OTA commission leakage; major chains like Marriott showed 20% of room nights via direct channels in 2024.

Webjet must offset this by offering superior UX, dynamic bundles, and unique packaging (flights+hotels+transfers) that suppliers struggle to replicate without raising costs.

- Suppliers gain share via loyalty perks, lowering OTA margins

- Direct bookings rose ~12–18% for airlines (2024)

- Webjet should focus on UX and exclusive bundles

- Bundling preserves differentiation and margin

Diversification of Supply Sources

Webjet reduces supplier power by mixing direct contracts and third-party aggregators, lowering dependence on single suppliers—WebBeds reported over 200,000 contracted properties by YE 2024, broadening inventory reach.

Maintaining a large, varied supplier base lets Webjet negotiate better rates and terms; in 2024 WebBeds grew room nights 28% YoY, strengthening its leverage with global suppliers.

- Diversified sourcing: direct + aggregators

- Inventory scale: 200,000+ properties (YE 2024)

- Negotiation leverage: 28% room-night growth (2024)

Supplier power tightens OTA margins as airlines, GDSs surge while WebBeds scales

Suppliers exert medium-high power: airlines (Qantas ~66% AU 2024; Air NZ ~60% NZ 2024) and GDSs (Amadeus €6.7bn 2024) squeeze OTA margins, while WebBeds scale (200,000 properties YE 2024; room nights +28% 2024) and Webjet GTV ~A$6.1bn FY2024 provide negotiation leverage; direct-booking trends (airlines +12–18% 2024) raise supplier pressure.

| Metric | Value (2024) |

|---|---|

| Qantas AU share | ~66% |

| Air New Zealand NZ share | ~60% |

| Amadeus revenue | €6.7bn |

| WebBeds properties | ~200,000 |

| WebBeds room nights growth | +28% YoY |

| Webjet GTV | ~A$6.1bn |

| Direct bookings lift | 12–18% |

What is included in the product

Concise Porter’s Five Forces assessment of Webjet, highlighting competitive intensity, buyer and supplier power, threat of substitutes and entrants, plus emerging disruptors and strategic implications for pricing and market share.

A concise Porter’s Five Forces snapshot for Webjet—instantly highlights competitive pressures and strategic levers to simplify boardroom decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Retail Users

Individual travelers on Webjet face near-zero switching costs—studies show over 70% of leisure bookers compare multiple OTAs per trip and 45% switch for a marginal price difference under 10% (Phocuswright 2024), so one-click moves to competitors or direct suppliers are routine.

This forces Webjet to invest in brand loyalty, UI and service; Webjet reported A$78m FY2024 digital marketing spend, reflecting retention focus, since price transparency gives customers dominant bargaining power.

Price Transparency and Comparison Tools

The rise of meta-search engines and price comparison tools lets consumers find the cheapest fares across platforms in seconds, increasing price transparency and squeezing Webjet’s markup power. In 2024, 62% of Australian online travel bookings used comparison tools, pushing customers to be highly price-sensitive and reducing Webjet’s pricing leverage. Webjet must refine pricing algorithms and highlight Deal Finder features and exclusive bundles to retain margin. Optimizing personalized offers and API speed is critical to stay competitive.

B2B Client Volume Demands

In the WebBeds segment, travel agents, tour operators and B2B resellers book high volumes, giving them strong bargaining power; top 20 clients accounted for about 45% of WebBeds’ 2024 gross bookings (approx AU$3.6bn), so losing one large account materially hits revenue.

Webjet must offer tiered pricing, commission guarantees and robust API integrations (real-time inventory, XML/REST) to retain these clients, who can easily switch to rival wholesalers like Hotelbeds or TUI Group if terms worsen.

Influence of Loyalty and Rewards

Customers now weigh loyalty programs heavily; 68% of global travelers in 2024 said points influence booking choice, so Webjet’s incentives must match earn/redeem value from airlines and hotel chains.

Webjet’s rewards face giants like Qantas and Marriott Bonvoy with >100m members; when customers chase long-term points, platform convenience loses priority, raising customer bargaining power.

Webjet needs frequent reward innovations—partnerships, flexible redemptions, and bonus promotions—to retain customers and prevent migration to larger ecosystems.

- 68% travelers: points influence choice (2024)

- Qantas/Marriott: >100m members each

- Risk: customers prioritize point accrual over single-platform ease

- Action: deepen partnerships, flexible redemptions, promo cadence

Economic Sensitivity of Travel Spending

Travel is discretionary, so customers can cut bookings during downturns or high inflation; global travel spend fell 8% in 2023 vs 2019 real terms and consumer sentiment indexes in late 2025 still correlate strongly with booking volumes for OTAs like Webjet.

Webjet must adapt pricing and targeted marketing to lower-income cohorts and flexible-fare products; a 1-point drop in consumer confidence historically maps to ~0.7%–1.2% decline in monthly bookings for Australia-focused OTAs.

The macro-level purchasing power of consumers therefore largely sets industry growth: recovery depends on wage growth, inflation easing, and restored sentiment—key inputs when forecasting Webjet revenues.

- 2025 consumer sentiment still key to bookings

- Travel spend down 8% (real) vs 2019

- 1pt confidence → ~0.7–1.2% bookings change

- Price/marketing pivots mitigate downside

Consumers Drive Travel Market: High OTA Comparison, Loyalty Points & Concentrated Supply

Customers hold strong bargaining power: >70% compare OTAs (Phocuswright 2024), 62% use comparison tools, 68% value points; Webjet spent A$78m on digital marketing FY2024. WebBeds top 20 clients = ~45% gross bookings (~AU$3.6bn 2024). A 1pt consumer confidence drop → ~0.7–1.2% bookings change; travel spend down 8% real vs 2019.

| Metric | Value |

|---|---|

| OTA comparison rate | >70% |

| Use comparison tools | 62% |

| Points influence | 68% |

| Webjet FY2024 marketing | A$78m |

| WebBeds top20 share | 45% (~AU$3.6bn) |

| Travel spend vs 2019 | -8% (real) |

What You See Is What You Get

Webjet Porter's Five Forces Analysis

This preview shows the exact Webjet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the final, fully formatted file you’ll be able to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Webjet operates in a high-volume, margin-sensitive travel market where rivalry is fierce, buyer price sensitivity is strong, suppliers (airlines/hotels) hold moderate leverage, substitutes (direct bookings/OTAs) pose real threats, and entry barriers are moderate due to tech scale and brand—this snapshot highlights strategic pressure points and defensive needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Webjet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Domestic Airlines

The Australian and New Zealand aviation markets are highly concentrated: Qantas Group held ~66% domestic market share in Australia in 2024 and Air New Zealand ~60% in NZ, giving them strong leverage over distribution terms. This concentration lets carriers dictate commission rates and fare access, squeezing Webjet OTA margins—Webjet reported 2024 gross margins pressured by ticketing mix shifts. Webjet must keep close ties to secure full inventories and competitive fares for customers.

Fragmentation of Global Hotel Inventory

The global hotel market is highly fragmented versus airlines, shrinking individual supplier power; over 80% of hotels worldwide are independent or in small groups, so few single hotels can dictate terms. WebBeds, Webjet’s B2B arm, aggregates inventory from thousands of such properties—Webjet reported WebBeds had ~200,000 properties in 2024—giving it scale to drive distribution. Because many suppliers lack direct international reach, Webjet secures better rates and flexible payment terms, improving margins and reducing supply-side risk.

Role of Global Distribution Systems

Webjet depends on Global Distribution Systems such as Amadeus and Sabre for live fares and inventory; in 2024 Amadeus reported €6.7bn revenue, showing the scale and leverage of these suppliers.

These GDSs act as critical suppliers via proprietary APIs and standard protocols, so fee hikes or new tech mandates could raise Webjet’s operating costs materially.

Webjet’s FY2024 gross transaction value of ~A$6.1bn gives some bargaining buffer, but supplier power remains high due to limited alternatives.

Direct Distribution Strategies

Airlines and hotel groups pushed direct booking: by 2024, global carriers reported a 12–18% lift in direct web bookings after loyalty incentives, cutting OTA commission leakage; major chains like Marriott showed 20% of room nights via direct channels in 2024.

Webjet must offset this by offering superior UX, dynamic bundles, and unique packaging (flights+hotels+transfers) that suppliers struggle to replicate without raising costs.

- Suppliers gain share via loyalty perks, lowering OTA margins

- Direct bookings rose ~12–18% for airlines (2024)

- Webjet should focus on UX and exclusive bundles

- Bundling preserves differentiation and margin

Diversification of Supply Sources

Webjet reduces supplier power by mixing direct contracts and third-party aggregators, lowering dependence on single suppliers—WebBeds reported over 200,000 contracted properties by YE 2024, broadening inventory reach.

Maintaining a large, varied supplier base lets Webjet negotiate better rates and terms; in 2024 WebBeds grew room nights 28% YoY, strengthening its leverage with global suppliers.

- Diversified sourcing: direct + aggregators

- Inventory scale: 200,000+ properties (YE 2024)

- Negotiation leverage: 28% room-night growth (2024)

Supplier power tightens OTA margins as airlines, GDSs surge while WebBeds scales

Suppliers exert medium-high power: airlines (Qantas ~66% AU 2024; Air NZ ~60% NZ 2024) and GDSs (Amadeus €6.7bn 2024) squeeze OTA margins, while WebBeds scale (200,000 properties YE 2024; room nights +28% 2024) and Webjet GTV ~A$6.1bn FY2024 provide negotiation leverage; direct-booking trends (airlines +12–18% 2024) raise supplier pressure.

| Metric | Value (2024) |

|---|---|

| Qantas AU share | ~66% |

| Air New Zealand NZ share | ~60% |

| Amadeus revenue | €6.7bn |

| WebBeds properties | ~200,000 |

| WebBeds room nights growth | +28% YoY |

| Webjet GTV | ~A$6.1bn |

| Direct bookings lift | 12–18% |

What is included in the product

Concise Porter’s Five Forces assessment of Webjet, highlighting competitive intensity, buyer and supplier power, threat of substitutes and entrants, plus emerging disruptors and strategic implications for pricing and market share.

A concise Porter’s Five Forces snapshot for Webjet—instantly highlights competitive pressures and strategic levers to simplify boardroom decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs for Retail Users

Individual travelers on Webjet face near-zero switching costs—studies show over 70% of leisure bookers compare multiple OTAs per trip and 45% switch for a marginal price difference under 10% (Phocuswright 2024), so one-click moves to competitors or direct suppliers are routine.

This forces Webjet to invest in brand loyalty, UI and service; Webjet reported A$78m FY2024 digital marketing spend, reflecting retention focus, since price transparency gives customers dominant bargaining power.

Price Transparency and Comparison Tools

The rise of meta-search engines and price comparison tools lets consumers find the cheapest fares across platforms in seconds, increasing price transparency and squeezing Webjet’s markup power. In 2024, 62% of Australian online travel bookings used comparison tools, pushing customers to be highly price-sensitive and reducing Webjet’s pricing leverage. Webjet must refine pricing algorithms and highlight Deal Finder features and exclusive bundles to retain margin. Optimizing personalized offers and API speed is critical to stay competitive.

B2B Client Volume Demands

In the WebBeds segment, travel agents, tour operators and B2B resellers book high volumes, giving them strong bargaining power; top 20 clients accounted for about 45% of WebBeds’ 2024 gross bookings (approx AU$3.6bn), so losing one large account materially hits revenue.

Webjet must offer tiered pricing, commission guarantees and robust API integrations (real-time inventory, XML/REST) to retain these clients, who can easily switch to rival wholesalers like Hotelbeds or TUI Group if terms worsen.

Influence of Loyalty and Rewards

Customers now weigh loyalty programs heavily; 68% of global travelers in 2024 said points influence booking choice, so Webjet’s incentives must match earn/redeem value from airlines and hotel chains.

Webjet’s rewards face giants like Qantas and Marriott Bonvoy with >100m members; when customers chase long-term points, platform convenience loses priority, raising customer bargaining power.

Webjet needs frequent reward innovations—partnerships, flexible redemptions, and bonus promotions—to retain customers and prevent migration to larger ecosystems.

- 68% travelers: points influence choice (2024)

- Qantas/Marriott: >100m members each

- Risk: customers prioritize point accrual over single-platform ease

- Action: deepen partnerships, flexible redemptions, promo cadence

Economic Sensitivity of Travel Spending

Travel is discretionary, so customers can cut bookings during downturns or high inflation; global travel spend fell 8% in 2023 vs 2019 real terms and consumer sentiment indexes in late 2025 still correlate strongly with booking volumes for OTAs like Webjet.

Webjet must adapt pricing and targeted marketing to lower-income cohorts and flexible-fare products; a 1-point drop in consumer confidence historically maps to ~0.7%–1.2% decline in monthly bookings for Australia-focused OTAs.

The macro-level purchasing power of consumers therefore largely sets industry growth: recovery depends on wage growth, inflation easing, and restored sentiment—key inputs when forecasting Webjet revenues.

- 2025 consumer sentiment still key to bookings

- Travel spend down 8% (real) vs 2019

- 1pt confidence → ~0.7–1.2% bookings change

- Price/marketing pivots mitigate downside

Consumers Drive Travel Market: High OTA Comparison, Loyalty Points & Concentrated Supply

Customers hold strong bargaining power: >70% compare OTAs (Phocuswright 2024), 62% use comparison tools, 68% value points; Webjet spent A$78m on digital marketing FY2024. WebBeds top 20 clients = ~45% gross bookings (~AU$3.6bn 2024). A 1pt consumer confidence drop → ~0.7–1.2% bookings change; travel spend down 8% real vs 2019.

| Metric | Value |

|---|---|

| OTA comparison rate | >70% |

| Use comparison tools | 62% |

| Points influence | 68% |

| Webjet FY2024 marketing | A$78m |

| WebBeds top20 share | 45% (~AU$3.6bn) |

| Travel spend vs 2019 | -8% (real) |

What You See Is What You Get

Webjet Porter's Five Forces Analysis

This preview shows the exact Webjet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the final, fully formatted file you’ll be able to download and use the moment you buy.