Weichai Power PESTLE Analysis

Your Shortcut to Market Insight Starts Here

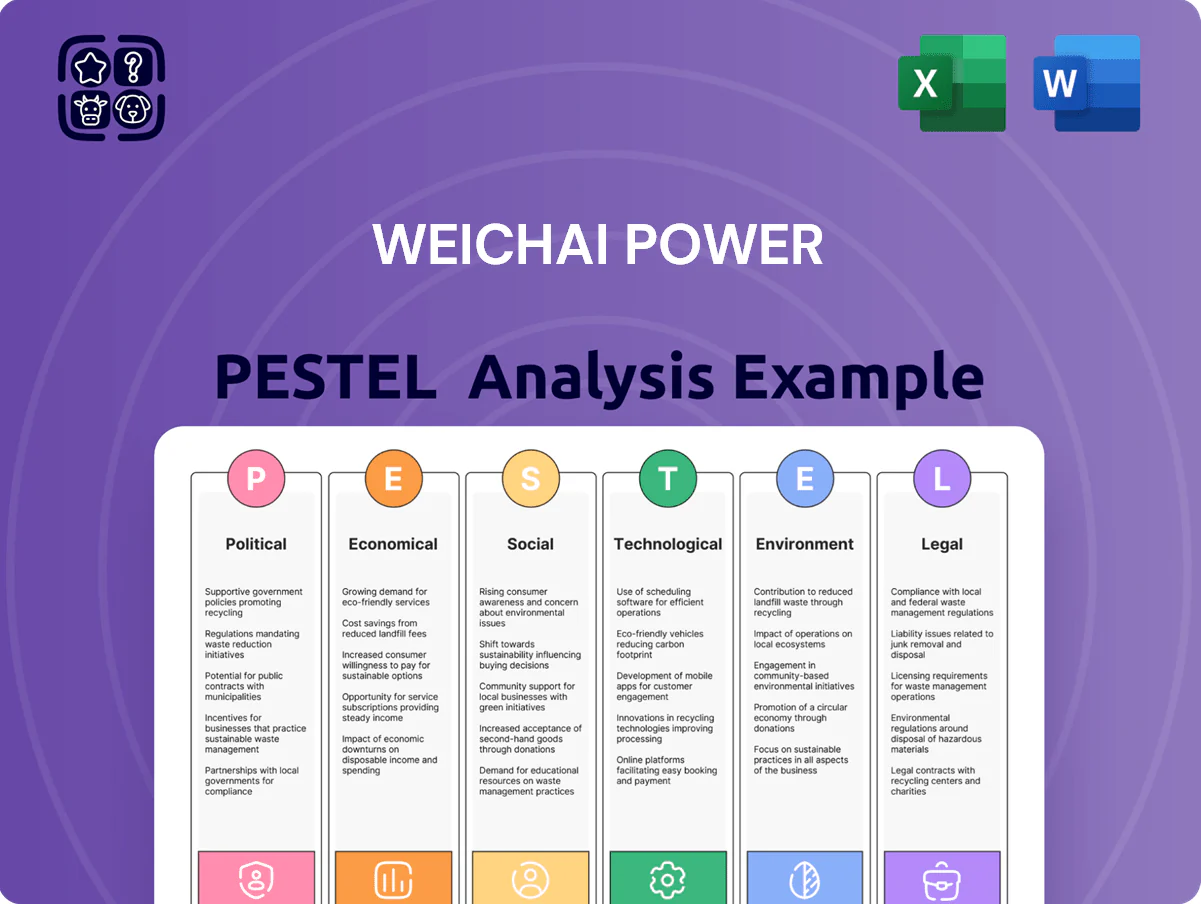

Gain a strategic edge with our PESTLE Analysis of Weichai Power—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists seeking actionable insights. Purchase the full report to access detailed risk assessments, opportunity maps, and editable data you can use immediately.

Political factors

Government Industrial Policy Support

Chinese government emphasis on New Quality Productive Forces channels subsidies and enhanced R&D tax credits to Weichai Power; in 2024 Beijing extended preferential R&D super-deductions up to 175% and provincial grants covering up to 20% of core project CAPEX, benefiting heavy-duty engine makers. Weichai, aligned with national high-end manufacturing targets, captured RMB 3.8bn in state-backed R&D funding and strategic project support in 2023–24, reinforcing large-scale powertrain innovation.

Belt and Road Initiative Expansion

The Belt and Road Initiative remains central to China’s foreign policy, expanding export avenues for Weichai Power—which reported 2024 overseas engine sales growth of 12%—into Central Asia, Africa and Southeast Asia, boosting demand for its heavy-duty trucks and power systems.

State-led infrastructure projects generated stable orders, with Weichai supplying power equipment to projects worth over $850 million across BRI corridors in 2023–2024, underpinning revenue visibility.

Political instability and security risks in some partner countries threaten timelines and receivables: in 2024 delayed payments from two African projects exceeded $60 million, highlighting credit and execution exposure.

International Trade Barriers and Tariffs

Increasing trade protectionism in North America and Europe—tariffs on Chinese-made automotive components rose by about 15–25% since 2021—threatens Weichai Power’s global expansion by raising landed costs and reducing competitiveness.

Specific tariffs on heavy-duty vehicles and engines can compress margins; a 20% tariff could cut export price competitiveness by roughly the same magnitude, pushing Weichai toward higher-cost local production.

Navigating these geopolitical tensions will require strategic lobbying, localized joint ventures, and partnerships with regional OEMs to mitigate tariffs and maintain market access.

State-Owned Enterprise Reform

As a major state-controlled entity under Shandong Heavy Industry Group, Weichai Power faces SOE reforms focused on efficiency and market-oriented competitiveness, including restructuring and performance-linked management incentives; in 2024 Shandong pushed for SOE profit-margin improvements averaging 2.8 percentage points across provincial champions.

These reforms introduce stricter performance evaluations and governance upgrades, helping Weichai sustain domestic leadership—Weichai reported 2024 revenue of RMB 101.6 billion and net profit margin near 6.4%—while promoting a more agile corporate culture aligned with global peers.

- State-driven restructuring, incentives, stricter KPIs

- 2024 revenue RMB 101.6bn; net margin ~6.4%

- Provincial SOE profit-margin gains ~2.8 pp (2024)

- Supports domestic dominance and agility

Geopolitical Stability in Emerging Markets

Weichai Power’s substantial exposure in Russia and the Middle East—regions accounting for an estimated 18–22% of overseas engine and powertrain revenue in 2024—makes it vulnerable to sanctions, trade curbs, and sudden import-rule changes that can hit margins and production timing.

Political volatility can disrupt parts supply and logistics; for example, Russia-related trade restrictions since 2022 raised component lead times by ~30% for some OEMs, risking higher inventory costs for Weichai.

Diversifying sales and manufacturing footprints—reducing any single region below ~10–12% of total revenue—remains a key mitigation to limit sanction and regulation concentration risk.

- 2024: Russia/Middle East ~18–22% of overseas revenue

- Component lead times up ~30% in sanction-affected corridors

- Target: cap single-region exposure to ~10–12% of revenue

RMB 101.6bn firm gains from R&D breaks and BRI (+12%) amid tariff and sanction risks

Strong state support (R&D super-deductions to 175%, RMB 3.8bn in 2023–24), BRI export growth (+12% overseas sales 2024), SOE reforms boosting margins (~+2.8 pp) and 2024 revenue RMB 101.6bn; risks: tariffs (+15–25%), sanctions exposure (Russia/Middle East 18–22% of overseas revenue), delayed payments >$60m (2024).

| Item | 2024 |

|---|---|

| Revenue | RMB 101.6bn |

| R&D funding | RMB 3.8bn |

| Overseas growth | +12% |

| Risk exposure | Russia/ME 18–22% |

What is included in the product

Explores how macro-environmental factors uniquely affect Weichai Power across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Weichai Power that clarifies regulatory, economic, and technological risks for fast alignment in meetings or client reports.

Economic factors

Infrastructure Investment Cycles

Weichai’s engine and construction machinery sales closely track infrastructure investment cycles; China’s 2024 fiscal stimulus allocated about CNY 1.2 trillion to transport and energy, lifting heavy-truck demand and supporting Weichai’s 2024 Q3 engine shipments, which rose ~8% YoY.

Fluctuations in Raw Material Costs

Weichai Power is highly sensitive to volatility in steel, aluminum and rare earth prices, which contributed to a 12% rise in raw-material costs in 2024 versus 2023, pressuring gross margins. Global inflation and supply-chain disruptions—container rates up ~30% in 2024 and semiconductor shortages—have increased manufacturing expenses, forcing tighter cost controls and sourcing diversification. To protect a 2024 gross margin near 19%, Weichai must weigh passing costs to customers against risking market-share loss in a competitive diesel-engine and powertrain market.

Currency Exchange Rate Volatility

With ~30% of 2024 revenue from overseas exports and KION Group stake, Weichai is exposed to RMB moves vs USD/EUR; RMB depreciation in 2023–2024 (around 6.9–7.3 CNY/USD) boosted export competitiveness but raised import costs for tech and components.

In 2024 forex losses accounted for ~RMB 1.2bn in net finance items, underscoring the need for robust hedging (forwards/options) to stabilize earnings against volatile USD/EUR swings.

Global Supply Chain Integration

The economic health of Weichai increasingly depends on stable global logistics for its intelligent logistics and auto parts; in 2024 global port congestion added average delays of 2.3 days, raising shipping costs ~7% year-on-year and pressuring margins.

Disruptions in shipping routes can delay deliveries and increase operational expenses; Weichai reported logistics costs of RMB 5.4 billion in 2023, up 6% from 2022.

Investment in smart logistics—IoT, route optimization and digital warehouses—reduced transit times by ~12% in pilot programs, lowering supply-chain costs and mitigating risk.

- 2023 logistics costs RMB 5.4 billion, +6% YoY

- Global port delays averaged 2.3 days in 2024, shipping costs +7% YoY

- Smart logistics pilots cut transit times ~12%

Growth of the Intelligent Logistics Market

The global intelligent logistics market reached about USD 48.5 billion in 2024 and is forecast to grow at ~12% CAGR to 2030, driven by e-commerce; KION, owned by Weichai, benefits as demand for automated forklifts and warehouse robots rises.

Shift toward automation reduces labor reliance and supports KION’s recurring-service revenues, cushioning Weichai against cyclicality in heavy equipment sales—KION reported ~€9.2bn revenue in 2024 with growing aftermarket services.

- Market size 2024: ~USD 48.5bn; CAGR ~12% to 2030

- KION 2024 revenue: ~€9.2bn; expanding services

- Automation lowers labor costs and stabilizes revenue

China transport stimulus boosts engine demand but margins squeezed by rising costs

Economic drivers: 2024 China transport/energy stimulus ~CNY 1.2tn lifted heavy-truck demand; 2024 Q3 engine shipments +8% YoY. Raw-materials +12% in 2024 pressured gross margin (~19% in 2024). Exports ~30% of revenue; RMB ~6.9–7.3 CNY/USD in 2023–24; 2024 forex losses ~RMB 1.2bn. Logistics costs RMB 5.4bn (2023), port delays +2.3 days (2024), shipping +7% YoY.

| Metric | 2023–24 |

|---|---|

| China stimulus | CNY 1.2tn (2024) |

| Engine shipments Q3 | +8% YoY (2024) |

| Raw-material cost change | +12% (2024 vs 2023) |

| Gross margin | ~19% (2024) |

| Export share | ~30% (2024) |

| RMB/USD | 6.9–7.3 (2023–24) |

| Forex losses | ~RMB 1.2bn (2024) |

| Logistics costs | RMB 5.4bn (2023) |

| Port delays | +2.3 days (2024) |

| Shipping cost change | +7% YoY (2024) |

Same Document Delivered

Weichai Power PESTLE Analysis

The preview shown here is the exact Weichai Power PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the complete analysis with political, economic, social, technological, legal, and environmental insights included.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Weichai Power—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists seeking actionable insights. Purchase the full report to access detailed risk assessments, opportunity maps, and editable data you can use immediately.

Political factors

Government Industrial Policy Support

Chinese government emphasis on New Quality Productive Forces channels subsidies and enhanced R&D tax credits to Weichai Power; in 2024 Beijing extended preferential R&D super-deductions up to 175% and provincial grants covering up to 20% of core project CAPEX, benefiting heavy-duty engine makers. Weichai, aligned with national high-end manufacturing targets, captured RMB 3.8bn in state-backed R&D funding and strategic project support in 2023–24, reinforcing large-scale powertrain innovation.

Belt and Road Initiative Expansion

The Belt and Road Initiative remains central to China’s foreign policy, expanding export avenues for Weichai Power—which reported 2024 overseas engine sales growth of 12%—into Central Asia, Africa and Southeast Asia, boosting demand for its heavy-duty trucks and power systems.

State-led infrastructure projects generated stable orders, with Weichai supplying power equipment to projects worth over $850 million across BRI corridors in 2023–2024, underpinning revenue visibility.

Political instability and security risks in some partner countries threaten timelines and receivables: in 2024 delayed payments from two African projects exceeded $60 million, highlighting credit and execution exposure.

International Trade Barriers and Tariffs

Increasing trade protectionism in North America and Europe—tariffs on Chinese-made automotive components rose by about 15–25% since 2021—threatens Weichai Power’s global expansion by raising landed costs and reducing competitiveness.

Specific tariffs on heavy-duty vehicles and engines can compress margins; a 20% tariff could cut export price competitiveness by roughly the same magnitude, pushing Weichai toward higher-cost local production.

Navigating these geopolitical tensions will require strategic lobbying, localized joint ventures, and partnerships with regional OEMs to mitigate tariffs and maintain market access.

State-Owned Enterprise Reform

As a major state-controlled entity under Shandong Heavy Industry Group, Weichai Power faces SOE reforms focused on efficiency and market-oriented competitiveness, including restructuring and performance-linked management incentives; in 2024 Shandong pushed for SOE profit-margin improvements averaging 2.8 percentage points across provincial champions.

These reforms introduce stricter performance evaluations and governance upgrades, helping Weichai sustain domestic leadership—Weichai reported 2024 revenue of RMB 101.6 billion and net profit margin near 6.4%—while promoting a more agile corporate culture aligned with global peers.

- State-driven restructuring, incentives, stricter KPIs

- 2024 revenue RMB 101.6bn; net margin ~6.4%

- Provincial SOE profit-margin gains ~2.8 pp (2024)

- Supports domestic dominance and agility

Geopolitical Stability in Emerging Markets

Weichai Power’s substantial exposure in Russia and the Middle East—regions accounting for an estimated 18–22% of overseas engine and powertrain revenue in 2024—makes it vulnerable to sanctions, trade curbs, and sudden import-rule changes that can hit margins and production timing.

Political volatility can disrupt parts supply and logistics; for example, Russia-related trade restrictions since 2022 raised component lead times by ~30% for some OEMs, risking higher inventory costs for Weichai.

Diversifying sales and manufacturing footprints—reducing any single region below ~10–12% of total revenue—remains a key mitigation to limit sanction and regulation concentration risk.

- 2024: Russia/Middle East ~18–22% of overseas revenue

- Component lead times up ~30% in sanction-affected corridors

- Target: cap single-region exposure to ~10–12% of revenue

RMB 101.6bn firm gains from R&D breaks and BRI (+12%) amid tariff and sanction risks

Strong state support (R&D super-deductions to 175%, RMB 3.8bn in 2023–24), BRI export growth (+12% overseas sales 2024), SOE reforms boosting margins (~+2.8 pp) and 2024 revenue RMB 101.6bn; risks: tariffs (+15–25%), sanctions exposure (Russia/Middle East 18–22% of overseas revenue), delayed payments >$60m (2024).

| Item | 2024 |

|---|---|

| Revenue | RMB 101.6bn |

| R&D funding | RMB 3.8bn |

| Overseas growth | +12% |

| Risk exposure | Russia/ME 18–22% |

What is included in the product

Explores how macro-environmental factors uniquely affect Weichai Power across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Weichai Power that clarifies regulatory, economic, and technological risks for fast alignment in meetings or client reports.

Economic factors

Infrastructure Investment Cycles

Weichai’s engine and construction machinery sales closely track infrastructure investment cycles; China’s 2024 fiscal stimulus allocated about CNY 1.2 trillion to transport and energy, lifting heavy-truck demand and supporting Weichai’s 2024 Q3 engine shipments, which rose ~8% YoY.

Fluctuations in Raw Material Costs

Weichai Power is highly sensitive to volatility in steel, aluminum and rare earth prices, which contributed to a 12% rise in raw-material costs in 2024 versus 2023, pressuring gross margins. Global inflation and supply-chain disruptions—container rates up ~30% in 2024 and semiconductor shortages—have increased manufacturing expenses, forcing tighter cost controls and sourcing diversification. To protect a 2024 gross margin near 19%, Weichai must weigh passing costs to customers against risking market-share loss in a competitive diesel-engine and powertrain market.

Currency Exchange Rate Volatility

With ~30% of 2024 revenue from overseas exports and KION Group stake, Weichai is exposed to RMB moves vs USD/EUR; RMB depreciation in 2023–2024 (around 6.9–7.3 CNY/USD) boosted export competitiveness but raised import costs for tech and components.

In 2024 forex losses accounted for ~RMB 1.2bn in net finance items, underscoring the need for robust hedging (forwards/options) to stabilize earnings against volatile USD/EUR swings.

Global Supply Chain Integration

The economic health of Weichai increasingly depends on stable global logistics for its intelligent logistics and auto parts; in 2024 global port congestion added average delays of 2.3 days, raising shipping costs ~7% year-on-year and pressuring margins.

Disruptions in shipping routes can delay deliveries and increase operational expenses; Weichai reported logistics costs of RMB 5.4 billion in 2023, up 6% from 2022.

Investment in smart logistics—IoT, route optimization and digital warehouses—reduced transit times by ~12% in pilot programs, lowering supply-chain costs and mitigating risk.

- 2023 logistics costs RMB 5.4 billion, +6% YoY

- Global port delays averaged 2.3 days in 2024, shipping costs +7% YoY

- Smart logistics pilots cut transit times ~12%

Growth of the Intelligent Logistics Market

The global intelligent logistics market reached about USD 48.5 billion in 2024 and is forecast to grow at ~12% CAGR to 2030, driven by e-commerce; KION, owned by Weichai, benefits as demand for automated forklifts and warehouse robots rises.

Shift toward automation reduces labor reliance and supports KION’s recurring-service revenues, cushioning Weichai against cyclicality in heavy equipment sales—KION reported ~€9.2bn revenue in 2024 with growing aftermarket services.

- Market size 2024: ~USD 48.5bn; CAGR ~12% to 2030

- KION 2024 revenue: ~€9.2bn; expanding services

- Automation lowers labor costs and stabilizes revenue

China transport stimulus boosts engine demand but margins squeezed by rising costs

Economic drivers: 2024 China transport/energy stimulus ~CNY 1.2tn lifted heavy-truck demand; 2024 Q3 engine shipments +8% YoY. Raw-materials +12% in 2024 pressured gross margin (~19% in 2024). Exports ~30% of revenue; RMB ~6.9–7.3 CNY/USD in 2023–24; 2024 forex losses ~RMB 1.2bn. Logistics costs RMB 5.4bn (2023), port delays +2.3 days (2024), shipping +7% YoY.

| Metric | 2023–24 |

|---|---|

| China stimulus | CNY 1.2tn (2024) |

| Engine shipments Q3 | +8% YoY (2024) |

| Raw-material cost change | +12% (2024 vs 2023) |

| Gross margin | ~19% (2024) |

| Export share | ~30% (2024) |

| RMB/USD | 6.9–7.3 (2023–24) |

| Forex losses | ~RMB 1.2bn (2024) |

| Logistics costs | RMB 5.4bn (2023) |

| Port delays | +2.3 days (2024) |

| Shipping cost change | +7% YoY (2024) |

Same Document Delivered

Weichai Power PESTLE Analysis

The preview shown here is the exact Weichai Power PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the complete analysis with political, economic, social, technological, legal, and environmental insights included.