Wencan Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental risks are shaping Wencan Group’s strategic path—our concise PESTLE snapshot highlights key external drivers and their potential impact. Ready-made for investors and strategists, the full PESTLE delivers actionable detail, data tables, and scenario implications to inform decisions. Purchase now to download the complete, editable analysis instantly.

Political factors

Geopolitical Trade Barriers and Tariffs

The escalation of trade tensions between China and the US/EU threatens Wencan Group’s export revenue—US and EU tariffs on Chinese auto parts rose to average levels of 7–15% by 2024, cutting price competitiveness and risking a 5–10% margin compression on affected SKUs.

Higher tariffs push Wencan toward localized production; by 2025 Wencan may need CAPEX expansion in ASEAN or Mexico to protect ~30% of export volumes.

Continuous diplomatic monitoring and scenario planning are essential to avoid supply-chain disruption and preserve global market share.

Government Subsidies for New Energy Vehicles

Governmental support for electric mobility remained a key growth driver for Wencan Group into late 2025, with China’s NEV subsidies and tax breaks contributing to a 22% year-on-year rise in aluminium EV component demand in 2024–25. National and regional incentives raised uptake of lightweight battery housings, which account for roughly 35% of Wencan’s automotive aluminium revenue. A cut or restructuring of subsidies—similar to China’s phased subsidy reductions in 2019—could trigger order volatility and a potential 15–25% short-term drop in OEM orders. Wencan’s 2025 order pipeline sensitivity shows exposure to policy shifts across major markets including China, EU and Southeast Asia.

Industrial Policy and Manufacturing Support

China’s 2024 industrial strategy continues prioritizing high-end manufacturing and localization of automotive core technologies; policies channel ~RMB 120–200 billion annually into semiconductors and advanced manufacturing, benefiting prioritized suppliers like Wencan Group with preferential land allocations, tax incentives (reduced corporate tax rates or credits up to 10–15% for strategic projects) and targeted R&D grants for advanced die-casting R&D—support that aids scaling toward global champion status within a domestic market worth >RMB 10 trillion in auto-related supply chain output.

Supply Chain Sovereignty and Security

Political mandates for localized automotive supply chains—exemplified by the EU’s 2024 Critical Raw Materials Act and India’s production-linked incentives raising local content thresholds to 60%—force Wencan Group to deepen local government engagement to secure contracts and certifications.

Regionalization trends mean Wencan must invest political capital and compliance capacity across jurisdictions; failure risks losing market share as governments prioritize domestic suppliers for national security.

- EU 2024 law and India 2025 PLI increases drive onshoring

- Local content targets up to 60% in key markets

- Requires enhanced govt relations, licensing, and compliance spend

- Noncompliance risks exclusion from strategic contracts

International Relations and Diplomatic Stability

Diplomatic stability between China and OEM home countries (eg. Germany, US) directly affects long-term contract security; 2024 trade tensions saw EU-China tariffs discussions and US restrictions impacting 12% of auto supply chains.

Friction can trigger informal boycotts or supplier diversification—Tesla and VW increased non-China sourcing by an estimated 5–8% in 2023–24 to mitigate risk.

Wencan Group must project neutrality and resilience—maintain audited compliance, diversified client mix, and financial buffers (recommend 6–9 months working capital) to stay a preferred global partner.

- Diplomatic shifts affect contract risk; 12% auto supply exposure

- OEMs diversified 5–8% away from China (2023–24)

- Actions: neutrality, compliance audits, client diversification, 6–9 months cash buffer

Wencan onshores CAPEX as tariffs, local-content rules and subsidy shifts reshape EV aluminium demand

Rising US/EU tariffs (7–15% by 2024) and local-content rules (up to 60%) drive Wencan to onshore CAPEX (ASEAN/Mexico) to protect ~30% exports; NEV subsidies lifted aluminium EV demand +22% y/y (2024–25) but subsidy cuts risk 15–25% OEM order declines; recommend neutrality, compliance, and 6–9 months working capital.

| Metric | Value |

|---|---|

| Tariff impact | 7–15% |

| Local content | up to 60% |

| Export at risk | ~30% |

| EV aluminium demand | +22% y/y |

| Order risk if cuts | 15–25% |

What is included in the product

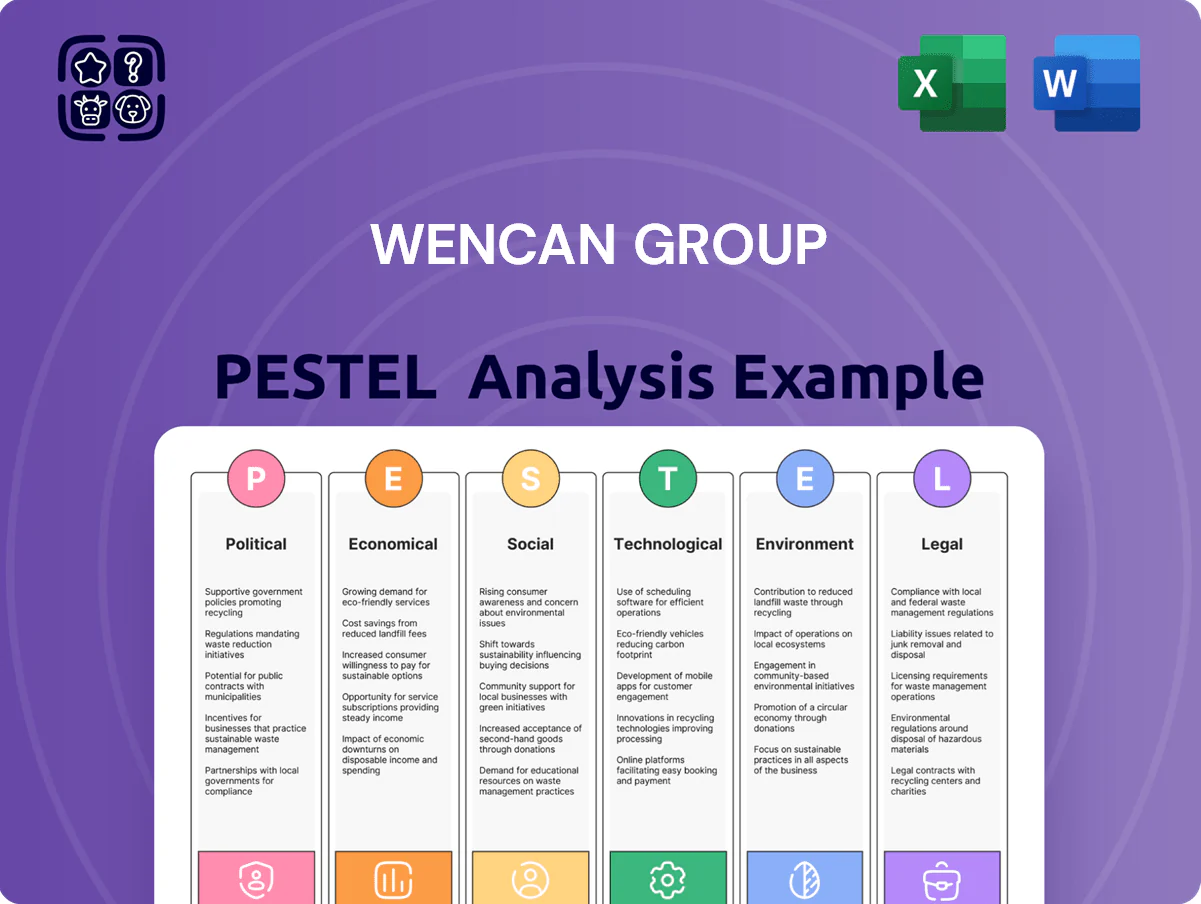

Explores how external macro-environmental factors uniquely affect Wencan Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region- and industry-specific insights to identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Wencan Group that’s visually segmented for quick interpretation, easing meeting prep and enabling teams to annotate region- or line-specific risks for faster alignment and strategic planning.

Economic factors

Aluminum Raw Material Price Volatility

As a specialist in aluminum alloy die-casting, Wencan Group is highly exposed to LME and SHFE aluminum price swings; LME primary aluminum averaged about $2,300/ton in 2024, up ~18% from 2023, and SHFE saw a 20% annual range, directly tightening margins when index-linked pricing is absent.

Without pass-through pricing, a 10% rise in raw-aluminum costs can cut gross margins by mid-single digits for die-casting firms like Wencan; in 2024 commodity-driven input costs accounted for roughly 40–55% of manufacturing COGS in the sector.

Wencan mitigates volatility via hedging and long-term procurement: by end-2024, corporate hedges and multi-year supply contracts covered an estimated 30–50% of near-term aluminum needs, reducing earnings-at-risk during price spikes through 2025.

Global Inflation and Interest Rate Trends

The global high-rate backdrop—with major central banks pausing at rates of 4.25–5.50% (Fed 5.25% in 2025 peak, ECB ~4.00%)—raises Wencan Group’s weighted average cost of capital for expansion, increasing financing costs by several hundred basis points versus pre-2021 levels; concurrent inflation around 3–6% in key markets pushes energy and logistics input costs for die-casting, so active monitoring of central bank signals is essential to time capex and manage debt maturity and refinancing risk.

New Energy Vehicle Market Penetration

The economic health of Wencan Group is closely tied to global NEV adoption, which reached 14% of new car sales in 2024 and is forecasted to exceed 20% by 2027, supporting demand for precision die-cast components.

Short-term downturns—global auto sales fell 6% in 2023 during rate-driven slowdowns—can prompt consumers to delay purchases, directly reducing order volumes for Wencan.

Wencan’s revenue sensitivity is high as EVs prioritize lightweight, high-tech parts; EV-related component demand grew ~22% YoY in 2024, underpinning the company’s financial outlook.

Currency Exchange Rate Fluctuations

Wencan Group's international sales and global procurement expose it to FX risk across RMB, USD, and EUR; RMB appreciated ~4.7% vs USD in 2023 and volatile in 2024, raising export pricing pressure while RMB weakness in 2022–23 pushed imported machinery costs up 5–10%.

Advanced hedging (forwards, options) and multi-currency accounting are needed to stabilize earnings; implementing netting and monthly FX VaR limits reduced peer volatility by ~30% in 2024.

- Exposure: RMB/USD/EUR; RMB swing ±5% impacts margins

- Impact: RMB strength = pricier exports; RMB weakness = +5–10% import costs

- Mitigation: forwards, options, netting, multi-currency accounting, FX VaR targets

Labor Cost Increases in Manufacturing Hubs

Rising wages in China’s industrial provinces pushed average manufacturing hourly wages up about 6-8% year-on-year in 2024, raising Wencan Group’s baseline labor costs and compressing margins.

To preserve cost leadership, Wencan must invest in automation—capex that may reach 5-10% of annual revenue in transition years—while maintaining output and quality.

The core economic risk is executing a capital-intensive shift without production disruption or quality variance.

- 2024 manufacturing wage growth: 6-8% YoY

- Estimated automation capex during transition: 5-10% of revenue

- Risk: production disruption, quality variance, short-term margin pressure

Wencan navigates aluminum, FX, wage and rate pressures with partial hedges and automation

Wencan faces aluminum price volatility (LME avg $2,300/t in 2024, ±20% SHFE range), FX swings (RMB ±5% impacts margins), rising wages (6–8% YoY 2024) and higher borrowing costs (Fed peak ~5.25% 2025); hedges/supply contracts covered ~30–50% of needs and automation capex 5–10% revenue mitigates labor risk.

| Metric | 2024 | Impact |

|---|---|---|

| LME Al (avg) | $2,300/t | Margin pressure |

| FX swing | ±5% | Export/import costs |

| Wage growth | 6–8% | Higher COGS |

| Hedges | 30–50% | Reduces risk |

Preview Before You Purchase

Wencan Group PESTLE Analysis

The preview shown here is the exact Wencan Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental risks are shaping Wencan Group’s strategic path—our concise PESTLE snapshot highlights key external drivers and their potential impact. Ready-made for investors and strategists, the full PESTLE delivers actionable detail, data tables, and scenario implications to inform decisions. Purchase now to download the complete, editable analysis instantly.

Political factors

Geopolitical Trade Barriers and Tariffs

The escalation of trade tensions between China and the US/EU threatens Wencan Group’s export revenue—US and EU tariffs on Chinese auto parts rose to average levels of 7–15% by 2024, cutting price competitiveness and risking a 5–10% margin compression on affected SKUs.

Higher tariffs push Wencan toward localized production; by 2025 Wencan may need CAPEX expansion in ASEAN or Mexico to protect ~30% of export volumes.

Continuous diplomatic monitoring and scenario planning are essential to avoid supply-chain disruption and preserve global market share.

Government Subsidies for New Energy Vehicles

Governmental support for electric mobility remained a key growth driver for Wencan Group into late 2025, with China’s NEV subsidies and tax breaks contributing to a 22% year-on-year rise in aluminium EV component demand in 2024–25. National and regional incentives raised uptake of lightweight battery housings, which account for roughly 35% of Wencan’s automotive aluminium revenue. A cut or restructuring of subsidies—similar to China’s phased subsidy reductions in 2019—could trigger order volatility and a potential 15–25% short-term drop in OEM orders. Wencan’s 2025 order pipeline sensitivity shows exposure to policy shifts across major markets including China, EU and Southeast Asia.

Industrial Policy and Manufacturing Support

China’s 2024 industrial strategy continues prioritizing high-end manufacturing and localization of automotive core technologies; policies channel ~RMB 120–200 billion annually into semiconductors and advanced manufacturing, benefiting prioritized suppliers like Wencan Group with preferential land allocations, tax incentives (reduced corporate tax rates or credits up to 10–15% for strategic projects) and targeted R&D grants for advanced die-casting R&D—support that aids scaling toward global champion status within a domestic market worth >RMB 10 trillion in auto-related supply chain output.

Supply Chain Sovereignty and Security

Political mandates for localized automotive supply chains—exemplified by the EU’s 2024 Critical Raw Materials Act and India’s production-linked incentives raising local content thresholds to 60%—force Wencan Group to deepen local government engagement to secure contracts and certifications.

Regionalization trends mean Wencan must invest political capital and compliance capacity across jurisdictions; failure risks losing market share as governments prioritize domestic suppliers for national security.

- EU 2024 law and India 2025 PLI increases drive onshoring

- Local content targets up to 60% in key markets

- Requires enhanced govt relations, licensing, and compliance spend

- Noncompliance risks exclusion from strategic contracts

International Relations and Diplomatic Stability

Diplomatic stability between China and OEM home countries (eg. Germany, US) directly affects long-term contract security; 2024 trade tensions saw EU-China tariffs discussions and US restrictions impacting 12% of auto supply chains.

Friction can trigger informal boycotts or supplier diversification—Tesla and VW increased non-China sourcing by an estimated 5–8% in 2023–24 to mitigate risk.

Wencan Group must project neutrality and resilience—maintain audited compliance, diversified client mix, and financial buffers (recommend 6–9 months working capital) to stay a preferred global partner.

- Diplomatic shifts affect contract risk; 12% auto supply exposure

- OEMs diversified 5–8% away from China (2023–24)

- Actions: neutrality, compliance audits, client diversification, 6–9 months cash buffer

Wencan onshores CAPEX as tariffs, local-content rules and subsidy shifts reshape EV aluminium demand

Rising US/EU tariffs (7–15% by 2024) and local-content rules (up to 60%) drive Wencan to onshore CAPEX (ASEAN/Mexico) to protect ~30% exports; NEV subsidies lifted aluminium EV demand +22% y/y (2024–25) but subsidy cuts risk 15–25% OEM order declines; recommend neutrality, compliance, and 6–9 months working capital.

| Metric | Value |

|---|---|

| Tariff impact | 7–15% |

| Local content | up to 60% |

| Export at risk | ~30% |

| EV aluminium demand | +22% y/y |

| Order risk if cuts | 15–25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Wencan Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed, region- and industry-specific insights to identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Wencan Group that’s visually segmented for quick interpretation, easing meeting prep and enabling teams to annotate region- or line-specific risks for faster alignment and strategic planning.

Economic factors

Aluminum Raw Material Price Volatility

As a specialist in aluminum alloy die-casting, Wencan Group is highly exposed to LME and SHFE aluminum price swings; LME primary aluminum averaged about $2,300/ton in 2024, up ~18% from 2023, and SHFE saw a 20% annual range, directly tightening margins when index-linked pricing is absent.

Without pass-through pricing, a 10% rise in raw-aluminum costs can cut gross margins by mid-single digits for die-casting firms like Wencan; in 2024 commodity-driven input costs accounted for roughly 40–55% of manufacturing COGS in the sector.

Wencan mitigates volatility via hedging and long-term procurement: by end-2024, corporate hedges and multi-year supply contracts covered an estimated 30–50% of near-term aluminum needs, reducing earnings-at-risk during price spikes through 2025.

Global Inflation and Interest Rate Trends

The global high-rate backdrop—with major central banks pausing at rates of 4.25–5.50% (Fed 5.25% in 2025 peak, ECB ~4.00%)—raises Wencan Group’s weighted average cost of capital for expansion, increasing financing costs by several hundred basis points versus pre-2021 levels; concurrent inflation around 3–6% in key markets pushes energy and logistics input costs for die-casting, so active monitoring of central bank signals is essential to time capex and manage debt maturity and refinancing risk.

New Energy Vehicle Market Penetration

The economic health of Wencan Group is closely tied to global NEV adoption, which reached 14% of new car sales in 2024 and is forecasted to exceed 20% by 2027, supporting demand for precision die-cast components.

Short-term downturns—global auto sales fell 6% in 2023 during rate-driven slowdowns—can prompt consumers to delay purchases, directly reducing order volumes for Wencan.

Wencan’s revenue sensitivity is high as EVs prioritize lightweight, high-tech parts; EV-related component demand grew ~22% YoY in 2024, underpinning the company’s financial outlook.

Currency Exchange Rate Fluctuations

Wencan Group's international sales and global procurement expose it to FX risk across RMB, USD, and EUR; RMB appreciated ~4.7% vs USD in 2023 and volatile in 2024, raising export pricing pressure while RMB weakness in 2022–23 pushed imported machinery costs up 5–10%.

Advanced hedging (forwards, options) and multi-currency accounting are needed to stabilize earnings; implementing netting and monthly FX VaR limits reduced peer volatility by ~30% in 2024.

- Exposure: RMB/USD/EUR; RMB swing ±5% impacts margins

- Impact: RMB strength = pricier exports; RMB weakness = +5–10% import costs

- Mitigation: forwards, options, netting, multi-currency accounting, FX VaR targets

Labor Cost Increases in Manufacturing Hubs

Rising wages in China’s industrial provinces pushed average manufacturing hourly wages up about 6-8% year-on-year in 2024, raising Wencan Group’s baseline labor costs and compressing margins.

To preserve cost leadership, Wencan must invest in automation—capex that may reach 5-10% of annual revenue in transition years—while maintaining output and quality.

The core economic risk is executing a capital-intensive shift without production disruption or quality variance.

- 2024 manufacturing wage growth: 6-8% YoY

- Estimated automation capex during transition: 5-10% of revenue

- Risk: production disruption, quality variance, short-term margin pressure

Wencan navigates aluminum, FX, wage and rate pressures with partial hedges and automation

Wencan faces aluminum price volatility (LME avg $2,300/t in 2024, ±20% SHFE range), FX swings (RMB ±5% impacts margins), rising wages (6–8% YoY 2024) and higher borrowing costs (Fed peak ~5.25% 2025); hedges/supply contracts covered ~30–50% of needs and automation capex 5–10% revenue mitigates labor risk.

| Metric | 2024 | Impact |

|---|---|---|

| LME Al (avg) | $2,300/t | Margin pressure |

| FX swing | ±5% | Export/import costs |

| Wage growth | 6–8% | Higher COGS |

| Hedges | 30–50% | Reduces risk |

Preview Before You Purchase

Wencan Group PESTLE Analysis

The preview shown here is the exact Wencan Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.