Wendy's SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Wendy’s strong brand recognition, menu innovation, and growing digital sales drive competitive advantage, while franchise concentration and rising commodity/labor costs pose clear risks; expansion into delivery and value-segment strategies highlight growth opportunities amid intense QSR competition. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

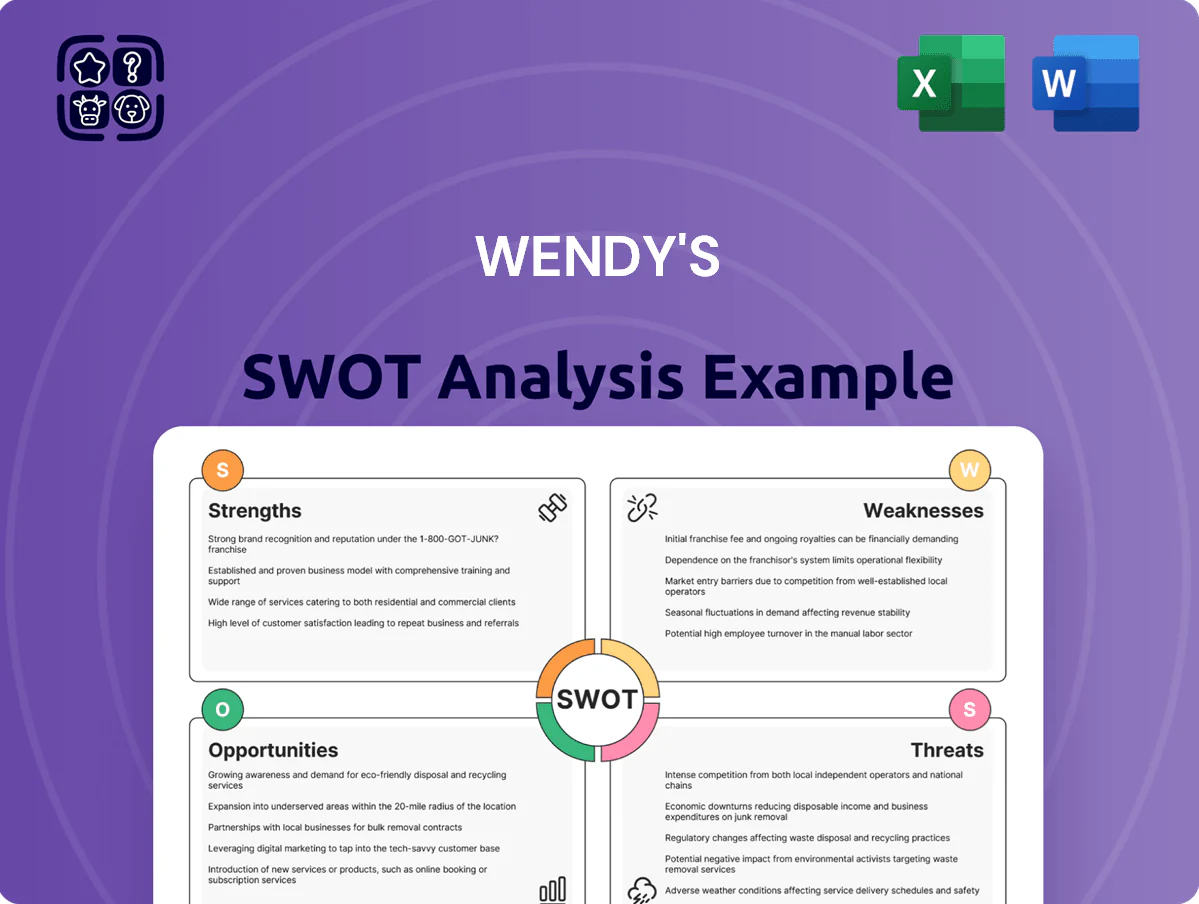

Strengths

Premium Product Differentiation

Wendy's uses fresh, never-frozen beef for core burgers, giving a clear quality edge versus rivals with frozen patties and supporting a premium positioning in quick-service. By end-2025 Wendy's reported same-store sales growth of 4.2% and systemwide average check increases ~3.5%, driven partly by premium menu mix and higher visit spend. This freshness claim sustains loyalty among quality-focused diners and higher margin per transaction.

Successful Breakfast Daypart Integration

Since its 2020 national launch, Wendy's breakfast has grown to roughly 10–12% of U.S. systemwide sales by 2024, creating a stable revenue stream and lowering sales volatility.

Wendy's captured share from incumbents by emphasizing higher-quality ingredients and steady promotions; same-store sales lifted 2–3% in morning dayparts in 2023–2024.

The breakfast mix diversifies income and boosts kitchen utilization across dayparts, improving unit-level throughput and contributing to margin resilience.

Robust Digital and Loyalty Ecosystem

By late 2025 Wendy’s Rewards and mobile app reached ~40–45% penetration of core customers, boosting digital sales to about 25% of total company-operated sales in FY2024–25; this lets Wendy’s collect granular purchase data to run personalized promos that lift visit frequency by an estimated 8–12%.

Digital ordering and app integration cut average ticket-to-kitchen time by ~15%, improved drive-thru throughput, and lowered order errors—helping delivery and carry-out margins and supporting company same-store sales growth of 3–4% in 2025.

Asset-Light Franchised Business Model

Wendy's operates an asset-light, highly franchised model—about 95% franchised as of FY 2024—generating steady royalty and rental income and cutting corporate capital spending.

This raises EBITDA margins and gives more predictable cash flow; Wendy's reported adjusted EBITDA margin of ~27% in 2024, appealing to yield-focused investors.

Shifting store-level risk to franchisees lets corporate focus on brand, menu innovation, and international growth—Wendy's opened 425 net new restaurants globally in 2024.

- ~95% franchised (2024)

- Adjusted EBITDA margin ~27% (2024)

- 425 net new restaurants opened (2024)

Effective Modern Marketing and Social Voice

Wendy’s distinct, snarky social voice drives engagement with younger users; in 2024 its social campaigns helped lift brand favorability by 6 percentage points among 18–34-year-olds vs 2022, per Kantar.

The viral, low-cost content strategy cuts paid-media needs—earned impressions accounted for an estimated 40% of Wendy’s total digital reach in 2024, lowering CPM-equivalent spend.

High sentiment and shareable posts support traffic: comparable-store sales rose 3.5% in FY2024, helped by digital-driven promotions and higher off-premises orders.

- Brand favorability +6 pts (18–34), 2024

- Earned impressions ~40% of digital reach, 2024

- Comparable-store sales +3.5% FY2024

Wendy’s growth: fresh beef, digital lift, 4.2% SSS and 27% EBITDA margin

Wendy’s fresh, never-frozen beef and premium mix lifted same-store sales ~4.2% (2025) and avg check +3.5%; breakfast grew to ~10–12% of U.S. sales (2024). Digital/app penetration ~40–45%, digital sales ~25% (FY2024–25), driving visit frequency +8–12%. Asset-light model ~95% franchised (2024) and adjusted EBITDA margin ~27% (2024) support cash flow and expansion (425 net new restaurants, 2024).

| Metric | Value |

|---|---|

| SSS growth (2025) | ~4.2% |

| Avg check change | ~+3.5% |

| Breakfast mix (2024) | 10–12% |

| Digital penetration | 40–45% |

| Digital sales | ~25% |

| Franchised | ~95% |

| Adj. EBITDA margin | ~27% |

| Net new restaurants (2024) | 425 |

What is included in the product

Analyzes Wendy's competitive position by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise Wendy's SWOT snapshot for quick strategic alignment and stakeholder-ready summaries.

Weaknesses

Geographic Concentration in North America

A vast majority of Wendy’s revenue and roughly 75% of its ~7,200 global restaurants (2025 company filings) are in the United States and Canada, concentrating exposure to North American demand cycles. This geographic focus raises risk from U.S./Canadian recessions and local market saturation—U.S. same-store sales swings directly hit consolidated results. Compared with McDonald’s and Yum! Brands, Wendy’s much smaller international footprint limits currency diversification and offsets when North American growth slows.

Complex Fresh Supply Chain Logistics

Wendy’s fresh, never-frozen beef policy raises logistics costs—transport and refrigerated deliveries are ~15–25% higher than frozen supply chains, adding to COGS and store-level overhead.

Frequent deliveries and strict cold-chain controls increase spoilage risk; industry data show fresh-produce waste can hit 4–6% of inventory value, raising operating expenses.

Localized supply disruptions—weather, plant outages, or transport strikes—can quickly force menu cuts, making this a structural vulnerability to service continuity.

Higher Price Point Relative to Value Rivals

Wendy’s premium positioning drives higher menu prices—average check near $8–9 in 2024 versus $6–7 for value rivals—so price-sensitive customers shift to dollar/value menus during 2022–24 inflation spikes.

Higher perceived quality hasn’t closed the gap: Wendy’s US same-store sales grew 3.2% in 2024, but competitors with aggressive value platforms captured larger share of low-income and young consumers.

That leaves Wendy’s struggling to win the extreme value-seeker segment, which still accounts for roughly 30–40% of quick-service restaurant (QSR) transactions nationwide.

Limited International Brand Awareness

- Brand awareness gap: ~20–40% vs incumbents (2024–25)

- Estimated city launch cost: $10–25M

- Target initial share: single digits

- Competes with decades-old local players

Debt Obligations and Financial Leverage

Wendy's has used heavy debt for buybacks and remodels, leaving net debt/EBITDA around 3.0x in 2024 (company-adjusted), which raises leverage risk.

Higher interest rates since 2022 boosted interest expense, narrowing free cash flow and could constrain capital for new stores or marketing during tight credit periods.

Analysts flag leverage as a flexibility limiter in downturns; refinancing or covenant pressure would restrict strategic moves.

- Net debt/EBITDA ~3.0x (2024)

- Rising interest expense reduced FCF in 2023–24

- Leverage limits M&A, expansion, and buybacks

North‑America centric chain faces margin, growth and leverage headwinds

Heavy North American concentration (~75% of ~7,200 restaurants, 2025 filings), higher COGS from fresh beef (+15–25% logistics), spoilage risk (4–6% inventory), weaker value proposition (avg check $8–9 vs $6–7 rivals), limited international awareness (-20–40% vs incumbents) and net debt/EBITDA ~3.0x (2024) constrain growth and flexibility.

| Metric | Value |

|---|---|

| US/CA share of restaurants | ~75% |

| Total restaurants (2025) | ~7,200 |

| Logistics premium (fresh beef) | 15–25% |

| Spoilage rate | 4–6% |

| Avg check (2024) | $8–9 |

| Rivals avg check | $6–7 |

| Brand gap (intl) | -20–40% |

| Net debt/EBITDA (2024) | ~3.0x |

Same Document Delivered

Wendy's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, structured and ready to use—buy now to access the complete, detailed report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Wendy’s strong brand recognition, menu innovation, and growing digital sales drive competitive advantage, while franchise concentration and rising commodity/labor costs pose clear risks; expansion into delivery and value-segment strategies highlight growth opportunities amid intense QSR competition. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Premium Product Differentiation

Wendy's uses fresh, never-frozen beef for core burgers, giving a clear quality edge versus rivals with frozen patties and supporting a premium positioning in quick-service. By end-2025 Wendy's reported same-store sales growth of 4.2% and systemwide average check increases ~3.5%, driven partly by premium menu mix and higher visit spend. This freshness claim sustains loyalty among quality-focused diners and higher margin per transaction.

Successful Breakfast Daypart Integration

Since its 2020 national launch, Wendy's breakfast has grown to roughly 10–12% of U.S. systemwide sales by 2024, creating a stable revenue stream and lowering sales volatility.

Wendy's captured share from incumbents by emphasizing higher-quality ingredients and steady promotions; same-store sales lifted 2–3% in morning dayparts in 2023–2024.

The breakfast mix diversifies income and boosts kitchen utilization across dayparts, improving unit-level throughput and contributing to margin resilience.

Robust Digital and Loyalty Ecosystem

By late 2025 Wendy’s Rewards and mobile app reached ~40–45% penetration of core customers, boosting digital sales to about 25% of total company-operated sales in FY2024–25; this lets Wendy’s collect granular purchase data to run personalized promos that lift visit frequency by an estimated 8–12%.

Digital ordering and app integration cut average ticket-to-kitchen time by ~15%, improved drive-thru throughput, and lowered order errors—helping delivery and carry-out margins and supporting company same-store sales growth of 3–4% in 2025.

Asset-Light Franchised Business Model

Wendy's operates an asset-light, highly franchised model—about 95% franchised as of FY 2024—generating steady royalty and rental income and cutting corporate capital spending.

This raises EBITDA margins and gives more predictable cash flow; Wendy's reported adjusted EBITDA margin of ~27% in 2024, appealing to yield-focused investors.

Shifting store-level risk to franchisees lets corporate focus on brand, menu innovation, and international growth—Wendy's opened 425 net new restaurants globally in 2024.

- ~95% franchised (2024)

- Adjusted EBITDA margin ~27% (2024)

- 425 net new restaurants opened (2024)

Effective Modern Marketing and Social Voice

Wendy’s distinct, snarky social voice drives engagement with younger users; in 2024 its social campaigns helped lift brand favorability by 6 percentage points among 18–34-year-olds vs 2022, per Kantar.

The viral, low-cost content strategy cuts paid-media needs—earned impressions accounted for an estimated 40% of Wendy’s total digital reach in 2024, lowering CPM-equivalent spend.

High sentiment and shareable posts support traffic: comparable-store sales rose 3.5% in FY2024, helped by digital-driven promotions and higher off-premises orders.

- Brand favorability +6 pts (18–34), 2024

- Earned impressions ~40% of digital reach, 2024

- Comparable-store sales +3.5% FY2024

Wendy’s growth: fresh beef, digital lift, 4.2% SSS and 27% EBITDA margin

Wendy’s fresh, never-frozen beef and premium mix lifted same-store sales ~4.2% (2025) and avg check +3.5%; breakfast grew to ~10–12% of U.S. sales (2024). Digital/app penetration ~40–45%, digital sales ~25% (FY2024–25), driving visit frequency +8–12%. Asset-light model ~95% franchised (2024) and adjusted EBITDA margin ~27% (2024) support cash flow and expansion (425 net new restaurants, 2024).

| Metric | Value |

|---|---|

| SSS growth (2025) | ~4.2% |

| Avg check change | ~+3.5% |

| Breakfast mix (2024) | 10–12% |

| Digital penetration | 40–45% |

| Digital sales | ~25% |

| Franchised | ~95% |

| Adj. EBITDA margin | ~27% |

| Net new restaurants (2024) | 425 |

What is included in the product

Analyzes Wendy's competitive position by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise Wendy's SWOT snapshot for quick strategic alignment and stakeholder-ready summaries.

Weaknesses

Geographic Concentration in North America

A vast majority of Wendy’s revenue and roughly 75% of its ~7,200 global restaurants (2025 company filings) are in the United States and Canada, concentrating exposure to North American demand cycles. This geographic focus raises risk from U.S./Canadian recessions and local market saturation—U.S. same-store sales swings directly hit consolidated results. Compared with McDonald’s and Yum! Brands, Wendy’s much smaller international footprint limits currency diversification and offsets when North American growth slows.

Complex Fresh Supply Chain Logistics

Wendy’s fresh, never-frozen beef policy raises logistics costs—transport and refrigerated deliveries are ~15–25% higher than frozen supply chains, adding to COGS and store-level overhead.

Frequent deliveries and strict cold-chain controls increase spoilage risk; industry data show fresh-produce waste can hit 4–6% of inventory value, raising operating expenses.

Localized supply disruptions—weather, plant outages, or transport strikes—can quickly force menu cuts, making this a structural vulnerability to service continuity.

Higher Price Point Relative to Value Rivals

Wendy’s premium positioning drives higher menu prices—average check near $8–9 in 2024 versus $6–7 for value rivals—so price-sensitive customers shift to dollar/value menus during 2022–24 inflation spikes.

Higher perceived quality hasn’t closed the gap: Wendy’s US same-store sales grew 3.2% in 2024, but competitors with aggressive value platforms captured larger share of low-income and young consumers.

That leaves Wendy’s struggling to win the extreme value-seeker segment, which still accounts for roughly 30–40% of quick-service restaurant (QSR) transactions nationwide.

Limited International Brand Awareness

- Brand awareness gap: ~20–40% vs incumbents (2024–25)

- Estimated city launch cost: $10–25M

- Target initial share: single digits

- Competes with decades-old local players

Debt Obligations and Financial Leverage

Wendy's has used heavy debt for buybacks and remodels, leaving net debt/EBITDA around 3.0x in 2024 (company-adjusted), which raises leverage risk.

Higher interest rates since 2022 boosted interest expense, narrowing free cash flow and could constrain capital for new stores or marketing during tight credit periods.

Analysts flag leverage as a flexibility limiter in downturns; refinancing or covenant pressure would restrict strategic moves.

- Net debt/EBITDA ~3.0x (2024)

- Rising interest expense reduced FCF in 2023–24

- Leverage limits M&A, expansion, and buybacks

North‑America centric chain faces margin, growth and leverage headwinds

Heavy North American concentration (~75% of ~7,200 restaurants, 2025 filings), higher COGS from fresh beef (+15–25% logistics), spoilage risk (4–6% inventory), weaker value proposition (avg check $8–9 vs $6–7 rivals), limited international awareness (-20–40% vs incumbents) and net debt/EBITDA ~3.0x (2024) constrain growth and flexibility.

| Metric | Value |

|---|---|

| US/CA share of restaurants | ~75% |

| Total restaurants (2025) | ~7,200 |

| Logistics premium (fresh beef) | 15–25% |

| Spoilage rate | 4–6% |

| Avg check (2024) | $8–9 |

| Rivals avg check | $6–7 |

| Brand gap (intl) | -20–40% |

| Net debt/EBITDA (2024) | ~3.0x |

Same Document Delivered

Wendy's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live excerpt of the real file, structured and ready to use—buy now to access the complete, detailed report immediately after checkout.