Wesfarmers PESTLE Analysis

Skip the Research. Get the Strategy.

Wesfarmers faces a complex mix of political oversight, commodity-driven economic swings, and rapid retail tech disruption that will shape its growth trajectory; our PESTLE distills these forces into clear strategic implications. Purchase the full analysis to access sector-specific risks, regulatory mapping, and actionable scenarios that investors and strategists can deploy immediately.

Political factors

Government trade policy and international relations

Australia's trade ties with China and ASEAN shape Wesfarmers' procurement and export mix; in 2024 China accounted for about 28% of Australian goods trade, meaning tariff shifts could materially alter input costs for Kmart and Bunnings.

Tariff or agreement changes—e.g., revisions to AANZFTA or unexpected tariffs—can raise landed costs and squeeze gross margins; import-dependent retail margins (Wesfarmers 2024 group gross margin ~27%) are sensitive to such moves.

Strategists must track geopolitical risk indicators and supplier diversification: in 2023-24 Bunnings’ imports and inventory policies helped mitigate supply shocks, preserving same-store sales resilience amid volatile freight rates and FX.

Industrial relations and labor market reforms

Federal moves to raise minimum pay (Fair Work Commission 2024 decision: 5.75% increase to national minimum wage) and proposals for multi-employer bargaining raise operating expenses across Wesfarmers’ ~230,000 retail employees, squeezing FY25 margins in Bunnings, Kmart and Coles.

Infrastructure and housing development initiatives

Political commitments to boost housing supply and A$120bn+ infrastructure pipeline to 2025–26 boost demand for Bunnings’ DIY/building materials and Wesfarmers’ industrial supplies, with Infrastructure Australia forecasting construction activity rising ~3–5% pa through 2026.

Federal incentives—eg, first-home buyer grants and state social housing programs totalling >A$5bn in 2024—raise home renovation activity, benefiting margins in home improvement retail.

Analysts cite these policy levers as key long-term revenue indicators for Wesfarmers’ hardware and building segments, linking projected housing starts growth of ~10% YoY (2024) to sustained sales upside.

Energy security and transition policy

Government mandates to cut emissions and shift to renewables impact Wesfarmers' chemicals, energy and fertilisers arm, where Scope 1–3 targets push capital towards low-carbon processes; Australia’s 2030 target of a 43% emissions reduction vs 2005 increases compliance costs for industrial operators.

Federal incentives for critical minerals and green hydrogen—backed by AU- government commitments including A$2.0bn in critical minerals funding (2024–25)—open investment avenues such as the Mt Holland lithium project for Wesfarmers.

Navigating subsidies, carbon pricing and potential industrial electricity reforms is vital: Australia’s Safeguard Mechanism and rising wholesale power prices (up ~40% in parts of 2023–24) materially affect margins in large-scale chemical and fertiliser production.

- Decarbonization mandates raise compliance and capex needs

- A$2.0bn critical minerals funding supports Mt Holland-style investments

- Carbon pricing and higher electricity costs threaten industrial margins

Geopolitical stability and supply chain resilience

Ongoing global tensions (e.g., 2024 trade disruptions and a 12% rise in shipping insurance premiums in 2023–24) force Wesfarmers to assess political risk in sourcing regions to avoid supply shocks for retail and industrial segments.

The Australian government’s 2024 sovereign capability initiatives, including A$2.5bn manufacturing grants, incentivize Wesfarmers to diversify away from high-risk suppliers, reducing concentration in single-source countries.

Business strategists view alignment with government policy as key to preventing inventory shortages and cost spikes; Wesfarmers’ inventory-to-sales ratio of 1.35 (FY2024) underscores sensitivity to supply-chain risk.

- Assess political risk in key sourcing countries

- Leverage A$2.5bn grants to localize supply

- Target inventory resilience given 1.35 inventory/sales

- Mitigate 12% shipping insurance cost rise

Australia: Trade, rising wages and power costs squeeze industry as stimulus spurs reshoring

Political risks—from China trade exposure (28% of AU trade, 2024) and rising wages (Fair Work +5.75% 2024)—can raise input and labour costs, while A$120bn infrastructure pipeline and A$2.5bn manufacturing/ A$2.0bn critical-minerals funding present growth and reshoring opportunities; higher power prices (~+40% 2023–24) and carbon rules raise capex and margins pressure for industrial segments.

| Metric | Value |

|---|---|

| China share of AU trade (2024) | ~28% |

| Min wage rise (2024) | +5.75% |

| Infrastructure pipeline | A$120bn to 2025–26 |

| Critical minerals funding | A$2.0bn (2024–25) |

| Manufacturing grants | A$2.5bn (2024) |

| Wholesale power rise | ~+40% (2023–24) |

What is included in the product

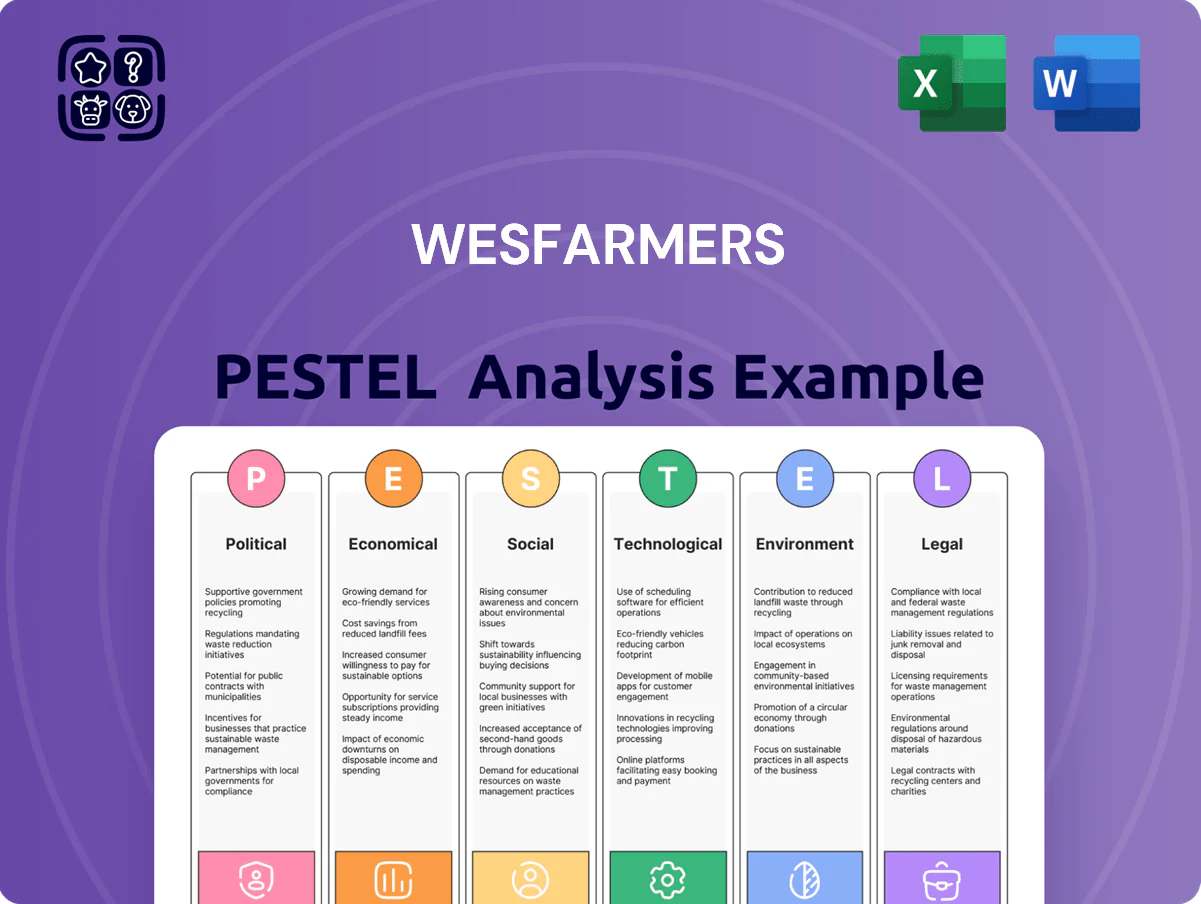

Explores how external macro-environmental factors uniquely affect Wesfarmers across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and strategic responses for executives, investors, and consultants.

A concise Wesfarmers PESTLE summary that’s visually segmented by category for quick meeting references, easily dropped into presentations or shared across teams to streamline external risk discussion and strategic alignment.

Economic factors

Interest rate environment and consumer spending

The Reserve Bank of Australia maintained a cash rate of 4.35% into early 2025, constraining discretionary income as Sydney mortgage repayments rose; household saving ratio fell to about 3.6% in late 2024. High rates have historically shifted spending to value retailers—Kmart—and dampened Bunnings’ DIY volumes, with home-improvement sales growth slowing to under 2% in 2024. Investors factor these cycles into lower price-to-earnings multiples for Wesfarmers’ retail segment.

Inflationary pressures on operating costs

Persistent inflation in logistics, utilities and raw materials squeezed Wesfarmers' margins in FY2025; COGS inflation for Bunnings and Industrial divisions rose ~6–8% year-on-year, pressuring gross margins despite group revenue growth of 6.1% to A$78.9bn in 2024–25.

Analysts track Wesfarmers' price pass-through: the firm increased retail prices ~3–5% while retaining market share, indicating limited demand elasticity in key categories.

Management emphasizes operational efficiencies and scale—productivity initiatives and A$400m cost-out targets in FY2025—aimed at absorbing shocks and sustaining price leadership.

Commodity price volatility and industrial earnings

Fluctuations in lithium, ammonia and natural gas prices materially affect WesCEF earnings; for FY2024 Wesfarmers reported a 12% segment EBIT swing linked to commodity moves, with ammonia feedstock costs up ~18% year-on-year to mid-2024 levels.

Currency exchange rate fluctuations

A volatile Australian dollar alters costs for Wesfarmers: a 10% AUD depreciation in 2023 raised import costs for Kmart/Target inventory materially, contributing to retail gross margin pressure as ~65% of general merchandise is sourced offshore.

For industrial operations, a stronger AUD in 2024 reduced export competitiveness, trimming earnings for manufacturing and chemicals segments exposed to FX moves.

Wesfarmers employs currency hedging—forward contracts and currency swaps—to mitigate FX risk; management reported AUD hedges covering portions of 2024–25 import flows in the FY2024 results.

- ~65% of Kmart/Target stocked from overseas

- 10% AUD depreciation in 2023 increased import COGS materially

- Hedging via forwards/swaps used to protect 2024–25 import flows

Labor market participation and wage growth

Tight labor markets in Australia and New Zealand pushed unemployment to ~3.6% and ~3.8% in 2024, raising recruitment and retention costs across Wesfarmers; the group noted wage-driven cost pressures in FY24, with enterprise wage growth ~4–5% in retail segments.

Stronger wages support consumer spending—household consumption rose ~2.5% YoY in 2024—benefiting Bunnings and Coles, but Officeworks and Priceline face margin squeeze as labor is a larger share of operating costs.

- Unemployment: Australia ~3.6%, NZ ~3.8% (2024)

- Enterprise wage growth in retail: ~4–5% (FY24)

- Household consumption growth: ~2.5% YoY (2024)

- Focus: optimize staffing, productivity, and pricing to balance spend uplift vs internal costs

Higher rates and COGS squeeze margins as shoppers hunt value; revenue up 6.1% to A$78.9bn

Higher rates (RBA cash rate 4.35% into 2025) and 2024 household saving ~3.6% shifted spending to value retailers, while COGS inflation (~6–8% YoY for Bunnings/WesCEF in FY2025) squeezed margins; group revenue rose 6.1% to A$78.9bn (2024–25). AUD volatility (10% 2023 depreciation) and commodity swings drove earnings volatility; wage growth ~4–5% and unemployment AU 3.6%/NZ 3.8% (2024) raised operating costs.

| Metric | Value |

|---|---|

| Revenue (2024–25) | A$78.9bn (+6.1%) |

| COGS inflation FY25 | ~6–8% YoY |

| RBA cash rate | 4.35% |

| Household saving ratio | ~3.6% (late 2024) |

| AUD move | 10% depreciation (2023) |

| Unemployment AU/NZ (2024) | 3.6% / 3.8% |

| Wage growth (retail) | ~4–5% |

Preview the Actual Deliverable

Wesfarmers PESTLE Analysis

The preview shown here is the exact Wesfarmers PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Wesfarmers faces a complex mix of political oversight, commodity-driven economic swings, and rapid retail tech disruption that will shape its growth trajectory; our PESTLE distills these forces into clear strategic implications. Purchase the full analysis to access sector-specific risks, regulatory mapping, and actionable scenarios that investors and strategists can deploy immediately.

Political factors

Government trade policy and international relations

Australia's trade ties with China and ASEAN shape Wesfarmers' procurement and export mix; in 2024 China accounted for about 28% of Australian goods trade, meaning tariff shifts could materially alter input costs for Kmart and Bunnings.

Tariff or agreement changes—e.g., revisions to AANZFTA or unexpected tariffs—can raise landed costs and squeeze gross margins; import-dependent retail margins (Wesfarmers 2024 group gross margin ~27%) are sensitive to such moves.

Strategists must track geopolitical risk indicators and supplier diversification: in 2023-24 Bunnings’ imports and inventory policies helped mitigate supply shocks, preserving same-store sales resilience amid volatile freight rates and FX.

Industrial relations and labor market reforms

Federal moves to raise minimum pay (Fair Work Commission 2024 decision: 5.75% increase to national minimum wage) and proposals for multi-employer bargaining raise operating expenses across Wesfarmers’ ~230,000 retail employees, squeezing FY25 margins in Bunnings, Kmart and Coles.

Infrastructure and housing development initiatives

Political commitments to boost housing supply and A$120bn+ infrastructure pipeline to 2025–26 boost demand for Bunnings’ DIY/building materials and Wesfarmers’ industrial supplies, with Infrastructure Australia forecasting construction activity rising ~3–5% pa through 2026.

Federal incentives—eg, first-home buyer grants and state social housing programs totalling >A$5bn in 2024—raise home renovation activity, benefiting margins in home improvement retail.

Analysts cite these policy levers as key long-term revenue indicators for Wesfarmers’ hardware and building segments, linking projected housing starts growth of ~10% YoY (2024) to sustained sales upside.

Energy security and transition policy

Government mandates to cut emissions and shift to renewables impact Wesfarmers' chemicals, energy and fertilisers arm, where Scope 1–3 targets push capital towards low-carbon processes; Australia’s 2030 target of a 43% emissions reduction vs 2005 increases compliance costs for industrial operators.

Federal incentives for critical minerals and green hydrogen—backed by AU- government commitments including A$2.0bn in critical minerals funding (2024–25)—open investment avenues such as the Mt Holland lithium project for Wesfarmers.

Navigating subsidies, carbon pricing and potential industrial electricity reforms is vital: Australia’s Safeguard Mechanism and rising wholesale power prices (up ~40% in parts of 2023–24) materially affect margins in large-scale chemical and fertiliser production.

- Decarbonization mandates raise compliance and capex needs

- A$2.0bn critical minerals funding supports Mt Holland-style investments

- Carbon pricing and higher electricity costs threaten industrial margins

Geopolitical stability and supply chain resilience

Ongoing global tensions (e.g., 2024 trade disruptions and a 12% rise in shipping insurance premiums in 2023–24) force Wesfarmers to assess political risk in sourcing regions to avoid supply shocks for retail and industrial segments.

The Australian government’s 2024 sovereign capability initiatives, including A$2.5bn manufacturing grants, incentivize Wesfarmers to diversify away from high-risk suppliers, reducing concentration in single-source countries.

Business strategists view alignment with government policy as key to preventing inventory shortages and cost spikes; Wesfarmers’ inventory-to-sales ratio of 1.35 (FY2024) underscores sensitivity to supply-chain risk.

- Assess political risk in key sourcing countries

- Leverage A$2.5bn grants to localize supply

- Target inventory resilience given 1.35 inventory/sales

- Mitigate 12% shipping insurance cost rise

Australia: Trade, rising wages and power costs squeeze industry as stimulus spurs reshoring

Political risks—from China trade exposure (28% of AU trade, 2024) and rising wages (Fair Work +5.75% 2024)—can raise input and labour costs, while A$120bn infrastructure pipeline and A$2.5bn manufacturing/ A$2.0bn critical-minerals funding present growth and reshoring opportunities; higher power prices (~+40% 2023–24) and carbon rules raise capex and margins pressure for industrial segments.

| Metric | Value |

|---|---|

| China share of AU trade (2024) | ~28% |

| Min wage rise (2024) | +5.75% |

| Infrastructure pipeline | A$120bn to 2025–26 |

| Critical minerals funding | A$2.0bn (2024–25) |

| Manufacturing grants | A$2.5bn (2024) |

| Wholesale power rise | ~+40% (2023–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Wesfarmers across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and strategic responses for executives, investors, and consultants.

A concise Wesfarmers PESTLE summary that’s visually segmented by category for quick meeting references, easily dropped into presentations or shared across teams to streamline external risk discussion and strategic alignment.

Economic factors

Interest rate environment and consumer spending

The Reserve Bank of Australia maintained a cash rate of 4.35% into early 2025, constraining discretionary income as Sydney mortgage repayments rose; household saving ratio fell to about 3.6% in late 2024. High rates have historically shifted spending to value retailers—Kmart—and dampened Bunnings’ DIY volumes, with home-improvement sales growth slowing to under 2% in 2024. Investors factor these cycles into lower price-to-earnings multiples for Wesfarmers’ retail segment.

Inflationary pressures on operating costs

Persistent inflation in logistics, utilities and raw materials squeezed Wesfarmers' margins in FY2025; COGS inflation for Bunnings and Industrial divisions rose ~6–8% year-on-year, pressuring gross margins despite group revenue growth of 6.1% to A$78.9bn in 2024–25.

Analysts track Wesfarmers' price pass-through: the firm increased retail prices ~3–5% while retaining market share, indicating limited demand elasticity in key categories.

Management emphasizes operational efficiencies and scale—productivity initiatives and A$400m cost-out targets in FY2025—aimed at absorbing shocks and sustaining price leadership.

Commodity price volatility and industrial earnings

Fluctuations in lithium, ammonia and natural gas prices materially affect WesCEF earnings; for FY2024 Wesfarmers reported a 12% segment EBIT swing linked to commodity moves, with ammonia feedstock costs up ~18% year-on-year to mid-2024 levels.

Currency exchange rate fluctuations

A volatile Australian dollar alters costs for Wesfarmers: a 10% AUD depreciation in 2023 raised import costs for Kmart/Target inventory materially, contributing to retail gross margin pressure as ~65% of general merchandise is sourced offshore.

For industrial operations, a stronger AUD in 2024 reduced export competitiveness, trimming earnings for manufacturing and chemicals segments exposed to FX moves.

Wesfarmers employs currency hedging—forward contracts and currency swaps—to mitigate FX risk; management reported AUD hedges covering portions of 2024–25 import flows in the FY2024 results.

- ~65% of Kmart/Target stocked from overseas

- 10% AUD depreciation in 2023 increased import COGS materially

- Hedging via forwards/swaps used to protect 2024–25 import flows

Labor market participation and wage growth

Tight labor markets in Australia and New Zealand pushed unemployment to ~3.6% and ~3.8% in 2024, raising recruitment and retention costs across Wesfarmers; the group noted wage-driven cost pressures in FY24, with enterprise wage growth ~4–5% in retail segments.

Stronger wages support consumer spending—household consumption rose ~2.5% YoY in 2024—benefiting Bunnings and Coles, but Officeworks and Priceline face margin squeeze as labor is a larger share of operating costs.

- Unemployment: Australia ~3.6%, NZ ~3.8% (2024)

- Enterprise wage growth in retail: ~4–5% (FY24)

- Household consumption growth: ~2.5% YoY (2024)

- Focus: optimize staffing, productivity, and pricing to balance spend uplift vs internal costs

Higher rates and COGS squeeze margins as shoppers hunt value; revenue up 6.1% to A$78.9bn

Higher rates (RBA cash rate 4.35% into 2025) and 2024 household saving ~3.6% shifted spending to value retailers, while COGS inflation (~6–8% YoY for Bunnings/WesCEF in FY2025) squeezed margins; group revenue rose 6.1% to A$78.9bn (2024–25). AUD volatility (10% 2023 depreciation) and commodity swings drove earnings volatility; wage growth ~4–5% and unemployment AU 3.6%/NZ 3.8% (2024) raised operating costs.

| Metric | Value |

|---|---|

| Revenue (2024–25) | A$78.9bn (+6.1%) |

| COGS inflation FY25 | ~6–8% YoY |

| RBA cash rate | 4.35% |

| Household saving ratio | ~3.6% (late 2024) |

| AUD move | 10% depreciation (2023) |

| Unemployment AU/NZ (2024) | 3.6% / 3.8% |

| Wage growth (retail) | ~4–5% |

Preview the Actual Deliverable

Wesfarmers PESTLE Analysis

The preview shown here is the exact Wesfarmers PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and analysis visible in this preview are identical to the downloadable file you’ll get immediately after payment, with no placeholders or surprises.